Best Study Material for Commerce Exam

Commerce Exam > Commerce Notes > Financial Statements with Adjustments (Part - 2)

Financial Statements with Adjustments (Part - 2) - Commerce PDF Download

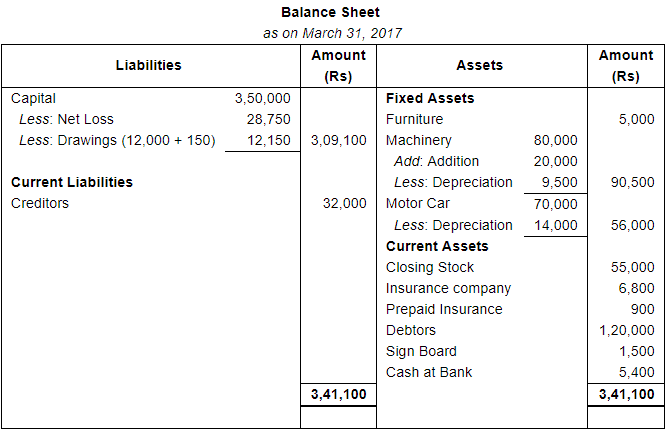

Page No 22.90:

Question 11(B):

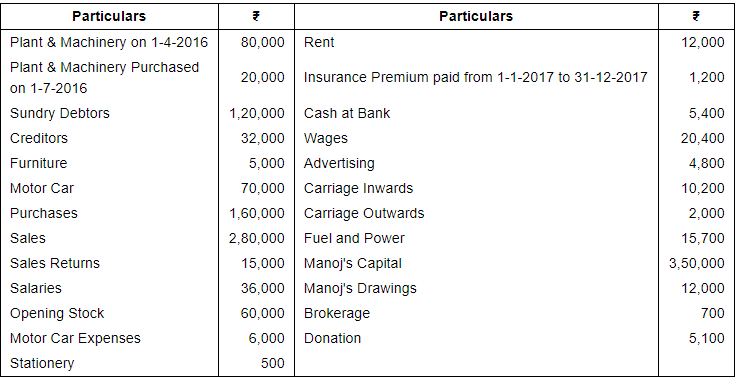

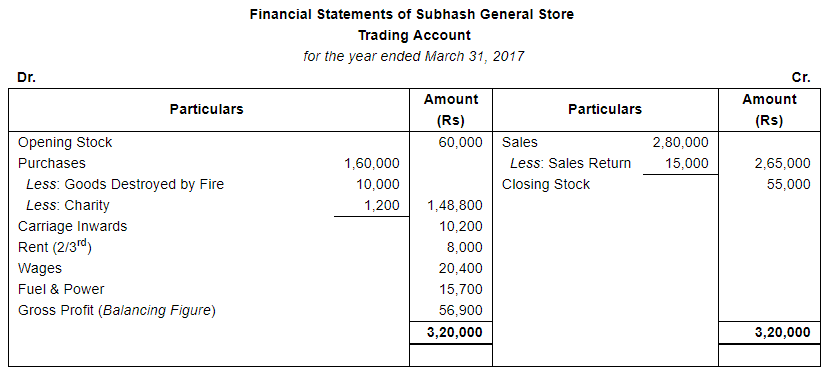

From the following particulars taken out from the books of Subhash General Store, prepare Trading and Profit & Loss Account for the year ended 31st March, 2017 and Balance Sheet as at the date:-

The following information is relevant:-

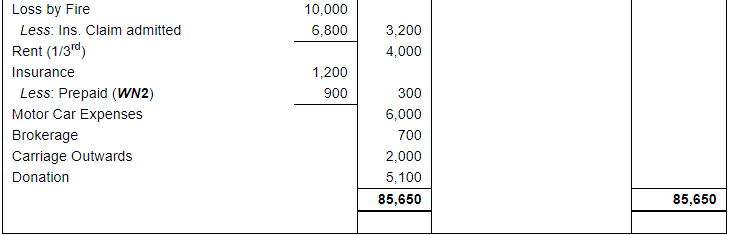

1. Closing Stock ₹ 55,000. Stock valued at ₹ 10,000 was destroyed by fire on 18th March, 2017 but the Insurance Company admitted a claim of ₹ 6,800 only which was received in April, 2017.

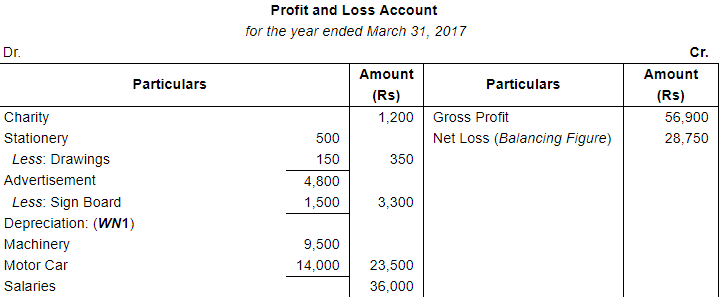

2. Stationery for ₹ 150 was consumed by the Proprietor.

3. Goods costing ₹ 1,200 were given away as charity.

4. A new Signboard costing ₹ 1,500 is included in Advertising.

5. Rent is to be allocated 2/3rd to Factory and 1/3rd to Office.

6. Depreciate machinery by 10% and Motor Car by 20%.

ANSWER:

Working Notes:

WN1: Calculation of Depreciation

Depreciationon Plant & Machinery

Depreciationon Motor Car

WN2: Calculation of Prepaid Insurance

Page No 22.91:

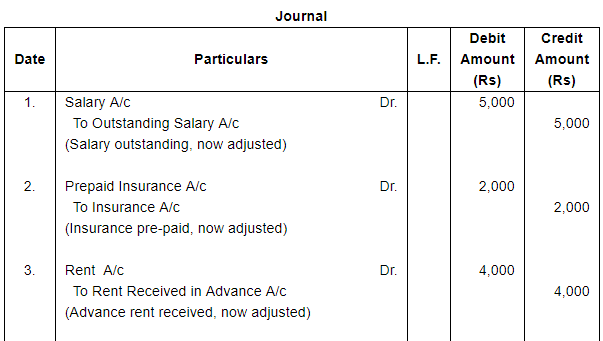

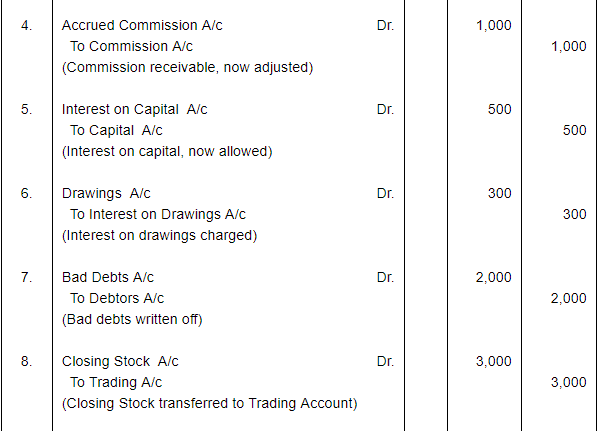

Question 12:

Give journal entries for the following adjustments in final accounts:

(i) Salaries ₹ 5,000 are outstanding.

(ii) Insurance amounting to ₹ 2,000 is paid in advance.

(iii) ₹ 4,000 for rent have been received in advance.

(iv) Commission earned but not received ₹ 1,000.

(v) Interest on capital ₹ 1,500.

(vi) Interest on Drawings ₹ 300.

(vii) Write off ₹ 2,000 as further bad-debts.

(viii) Closing Stock ₹ 3,000.

ANSWER:

Page No 22.91:

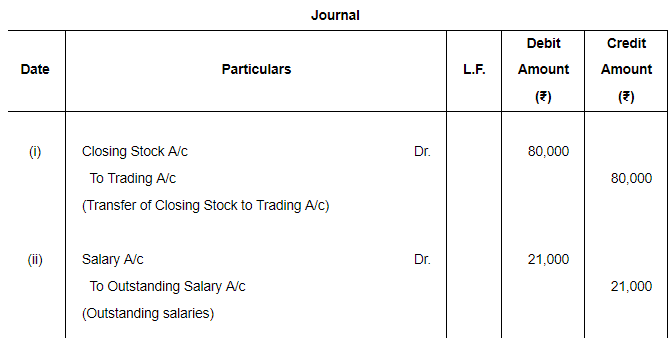

Question 13:

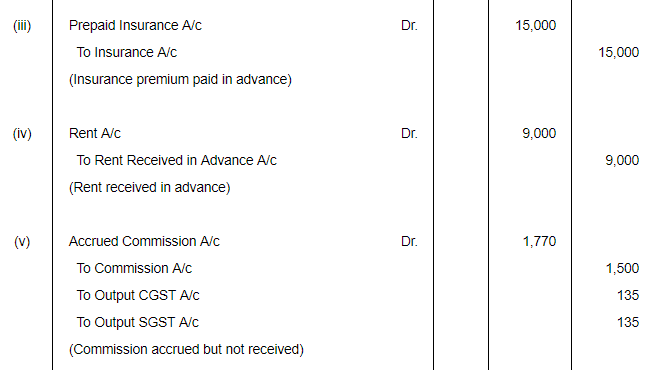

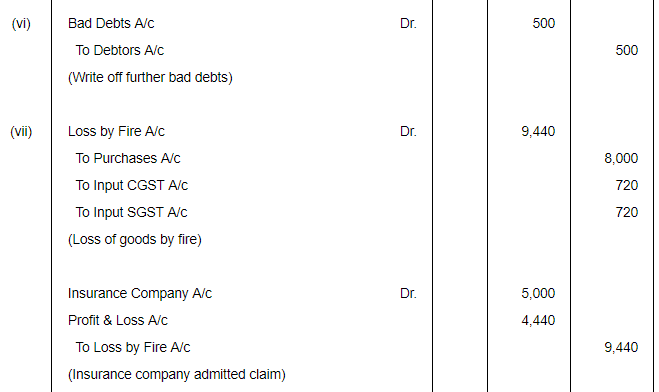

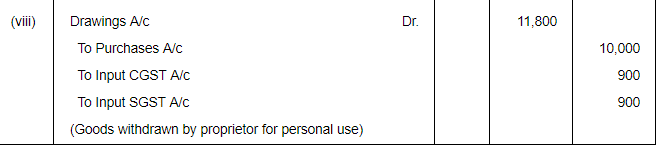

Give journal entries for the following adjustments in final accounts assuming CGST and SGST @ 9% each:

(i) Closing Stock ₹ 80,000.

(ii) Outstanding salaries ₹ 21,000.

(iii) Insurance premium amounting to ₹ 15,000 is paid in advance.

(iv) ₹ 9,000 received for rent related to the next accounting period.

(v) Commission accrued but not received during the accounting year ₹ 1,500.

(vi) Write off ₹ 500 as further bad debts.

(vii) Goods costing ₹ 8,000 destroyed by fire and insurance company admitted a claim for ₹ 5,000 only.

(viii) Goods costing ₹ 10,000 (Market value ₹ 11,000) were taken by proprietor for personal use.

ANSWER:

Page No 22.92:

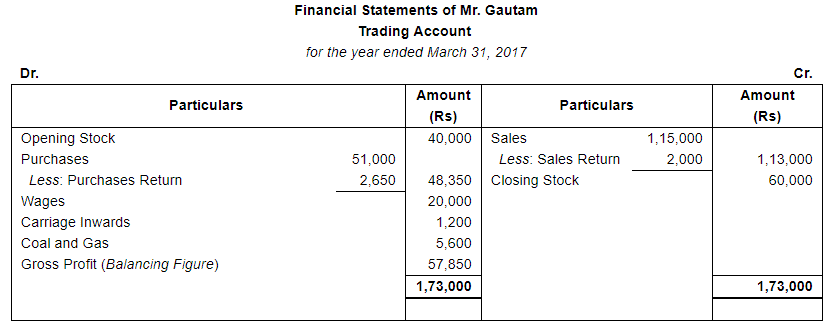

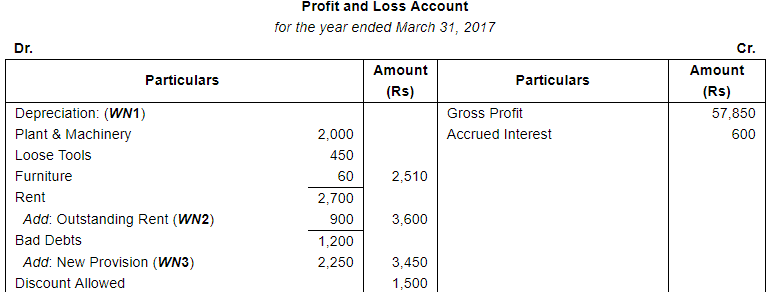

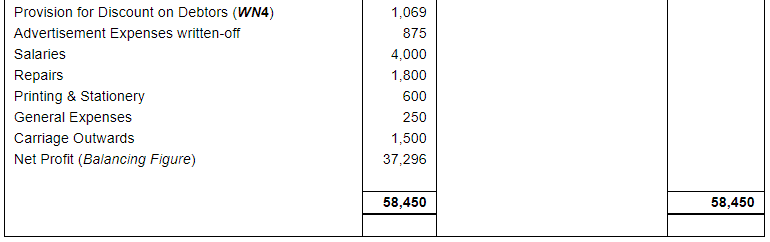

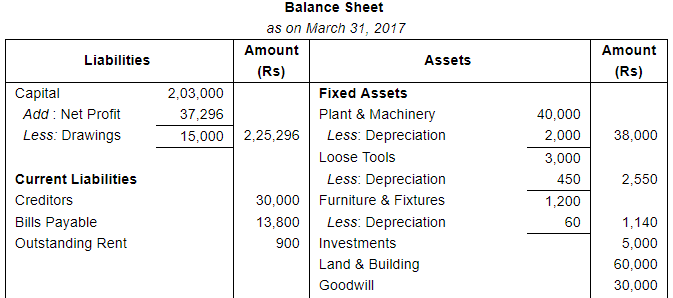

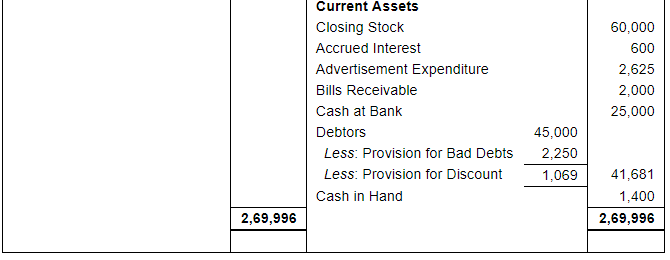

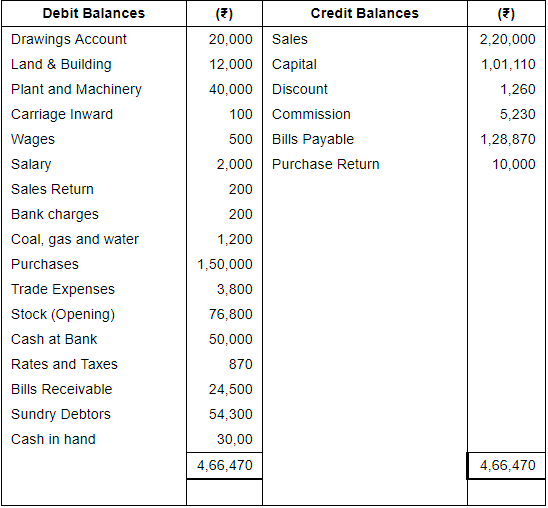

Question 14:

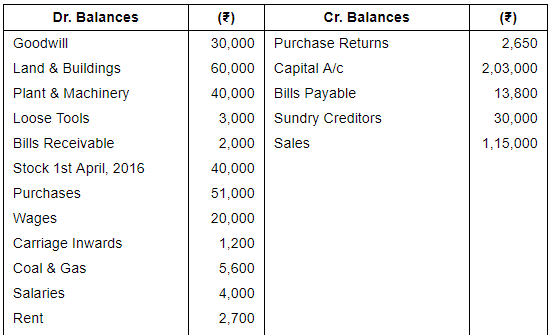

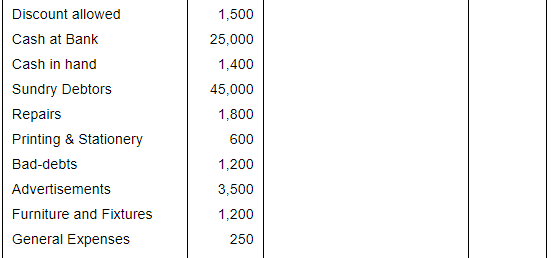

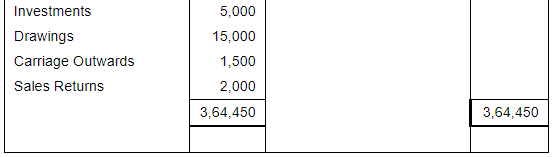

Following is the Trial Balance of Mr. Gautam as at 31st March, 2017:

You are required to prepare Final Accounts after taking into account the following adjustments:

(a) Closing Stock on 31st March, 2017 was ₹ 60,000.

(b) Depreciate Plant and Machinery at 5%, Loose Tools at 15% and Furniture and fixtures at 5%.

(c) Provide  for discount on Sundry Debtors and also provide 5% for Bad and Doubtful Debts on Sundry Debtors.

for discount on Sundry Debtors and also provide 5% for Bad and Doubtful Debts on Sundry Debtors.

(d) Only three quarter's rent has been paid, the last quarter's rent being outstanding.

(e) Interest earned but not received ₹ 600.

(f) Write off 1/4th of Advertisement expenses.

ANSWER:

Working Notes:

WN1: Calculation of Depreciation

WN2: Calculation of Outstanding Rent

WN3: Calculation of Provision for Doubtful Debts

WN4: Calculation of Provision for Discount on Debtors

Page No 22.93:

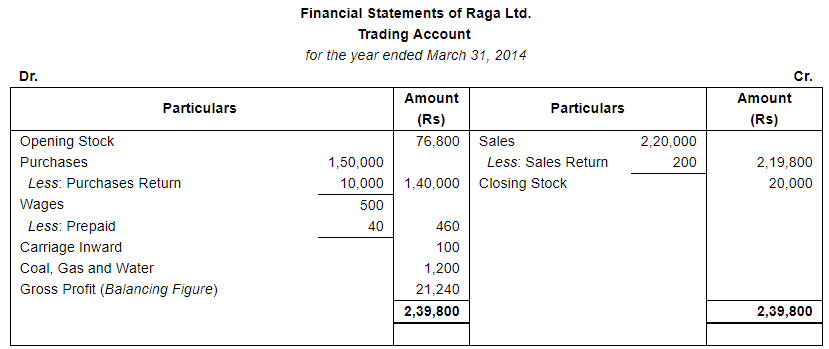

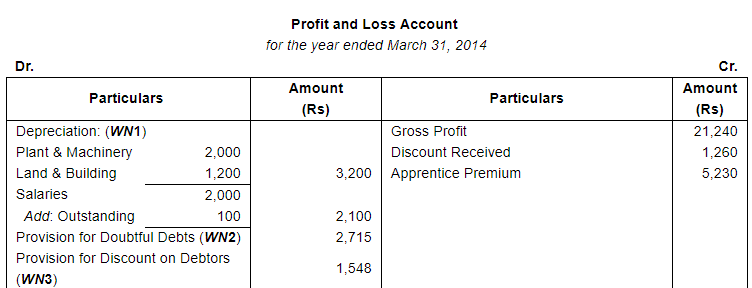

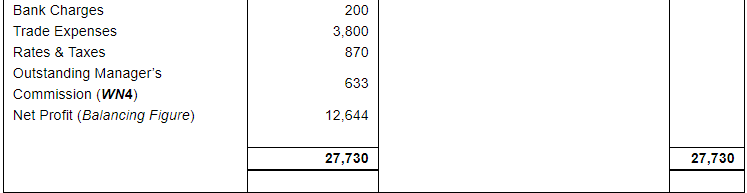

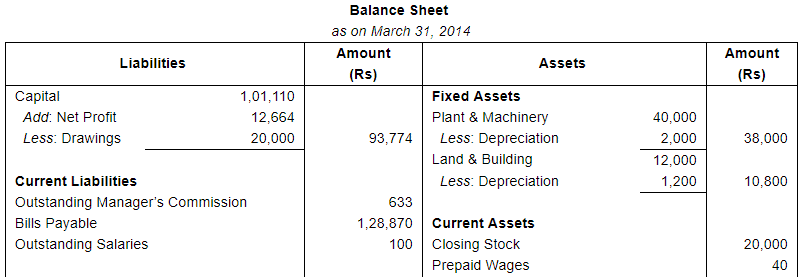

Question 15:

From the following Trial Balance, extracted from the books of Raga Ltd., prepare a Profit and Loss Account for the year ended 31st March, 2014 and a Balance Sheet as at that date:

The additional informations are as under:

(i) Closing stock was valued at the end of the year at ₹ 20,000.

(ii) Depreciation on Plant and Machinery charged at 5% and on Land and Building at 10%.

(iii) Make a provision for discount on debtors at 3%.

(iv) Make a provision at 5% on debtors for Bad-debts.

(v) Salary outstanding was ₹ 100 and Wages prepaid were ₹ 40.

(vi) The manager is entitled to a Commission of 5% on Net Profit after charging such Commission.

ANSWER:

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Provision for Doubtful Debts WN3: Calculation of Provision for Discount on Debtors

WN3: Calculation of Provision for Discount on Debtors

WN4: Calculation of Manager’s Commission

Page No 22.94:

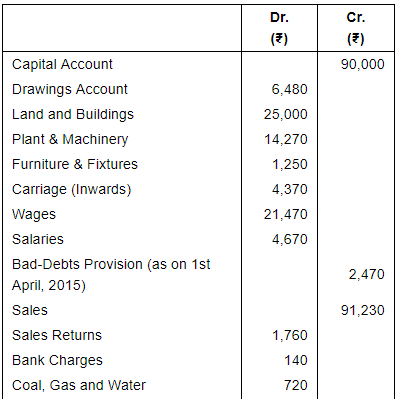

Question 16:

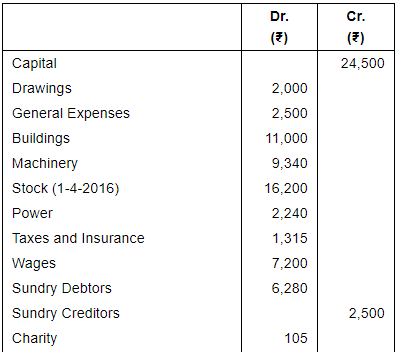

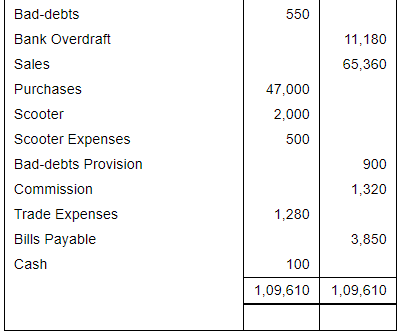

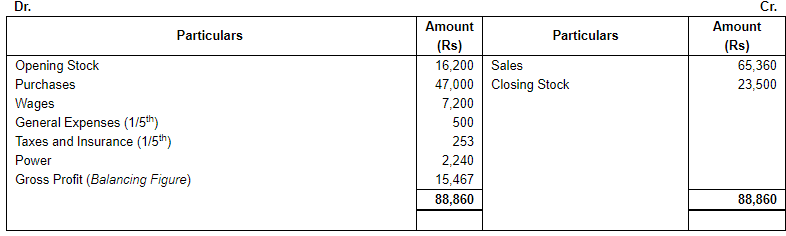

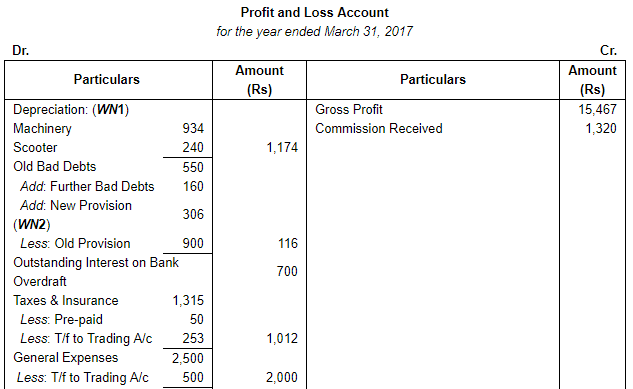

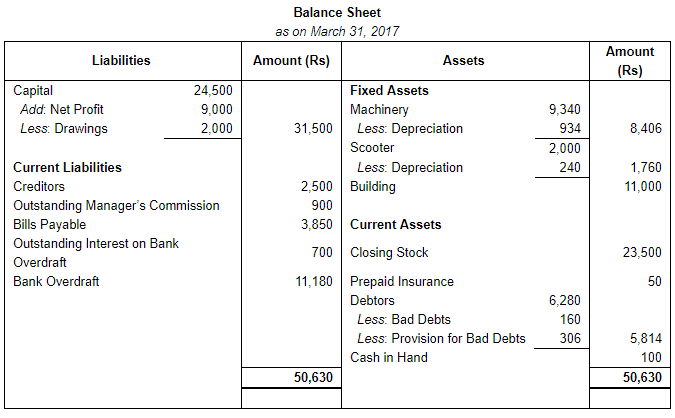

The following balances were extracted from the books of Shri Krishan Kumar as at 31st March, 2017:

Adjustments:-

(i) Stock on 31st March, 2017 was valued at ₹ 23,500.

(ii) 1\5th of general expenses and taxes & insurance to be charged to factory and the balance to the office.

(iii) Write off a further Bad-debts of ₹ 160 and maintain the provision for Bad-debts at 5% on Debtors.

(iv) Depreciate Machinery at 10% and Scooter by ₹ 240.

(v) Provide ₹ 700 for outstanding interest on Bank Overdraft.

(vi) Prepaid Insurance is to the extent of ₹ 50.

(vii) Provide for Manager's Commission at 10% on the Net Profit after charging such Commission.

Prepare final accounts for the year ended 31st March, 2017 after giving effect to the above adjustments.

ANSWER:

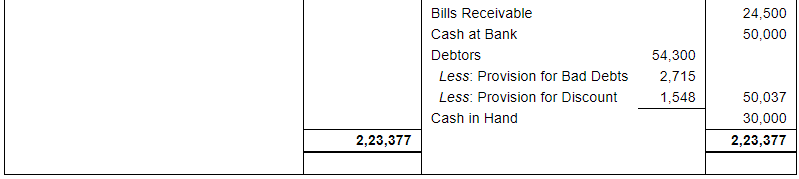

Financial Statements of Shri Krishan Kumar

Trading Account

for the year ended March 31, 2017

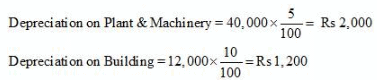

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Provision for Doubtful Debts

Provision for Doubtful Debts

WN3: Calculation of Manager’s Commission

Page No 22.95:

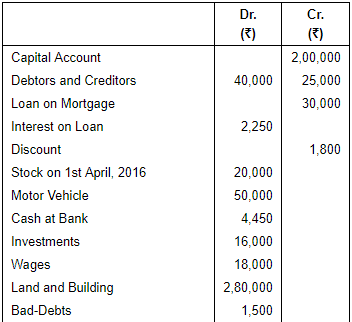

Question 17(A):

On 31st March, 2017 the following Trial Balance was extracted from the books of Sh. Ghanshyam Das:-

Prepare Trading and Profit & Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date, after making adjustments for the following matters:

1. Depreciate Land and Building at 2.5% and Motor Vehicles at 20%.

2. Interest on Loan at 15% p.a. is unpaid for six months.

3. Ghanshyam Das withdrew ₹ 2,000 for his private use. This amount was included in general expenses.

4. Interest on Investments is receivable for full year @ 10%.

5. Provide for Manager's Commission at 10% on Net Profit after charging such commission.

6. Stock in hand on 31st March, 2017 was valued at ₹ 25,000 (Realisable value ₹ 22,000).

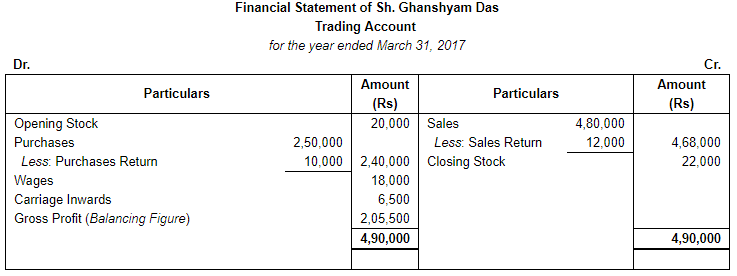

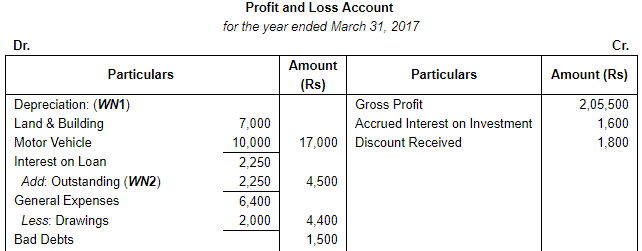

ANSWER:

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Outstanding Interest on Loan

WN3: Calculation of Manager’s Commission

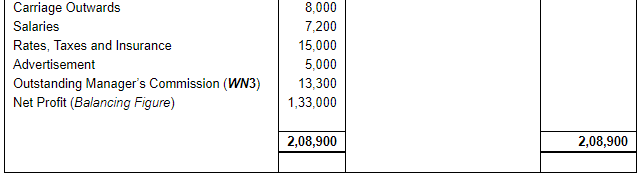

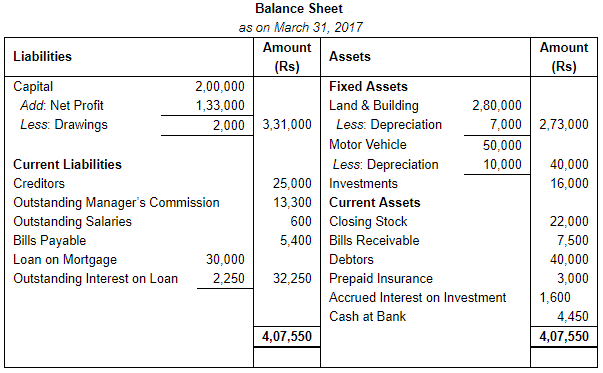

Page No 22.96:

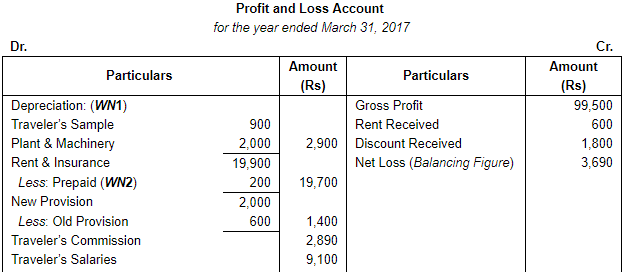

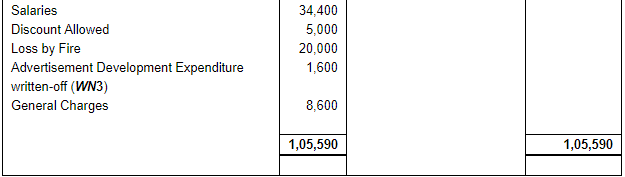

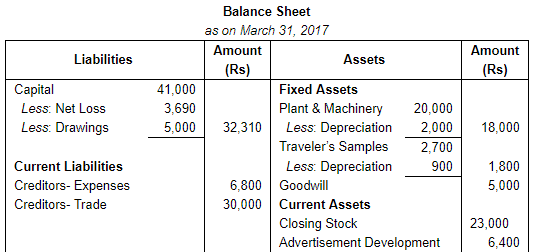

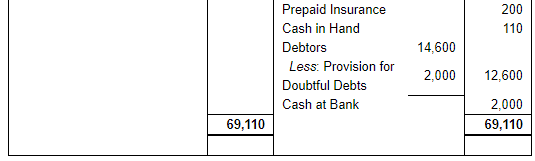

Question 17(B):

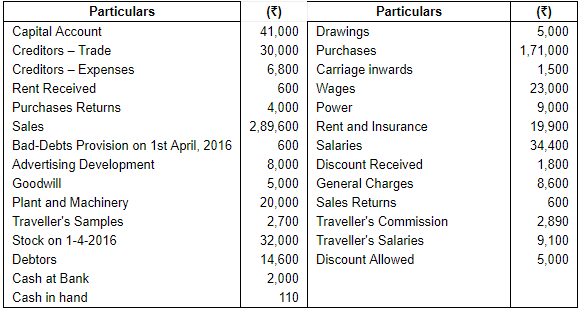

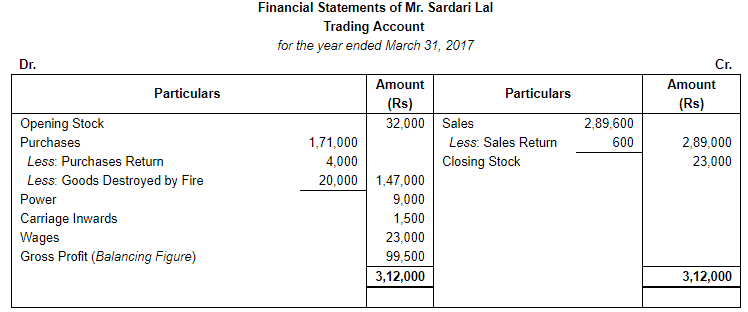

Prepare Trading and Profit and Loss Account and Balance Sheet as at 31st March, 2017 from the following Balances of Mr. Sardari Lal:

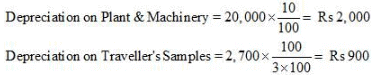

Adjustments:- The Closing stock was ₹ 23,000 but there has been a loss by fire on 20th March, 2017, to the extent of ₹ 20,000, not covered by insurance. Depreciate Plant and Machinery by 10% and Traveller's Samples by  . Increase the Bad-debts Provision to ₹ 2,000. Write 20% off Advertising Development Account. Annual premium on insurance expiring 1st June, 2017 was ₹ 1,200. Provide for Manager's commission @ 5% on Net Profits after charging such Commission.

. Increase the Bad-debts Provision to ₹ 2,000. Write 20% off Advertising Development Account. Annual premium on insurance expiring 1st June, 2017 was ₹ 1,200. Provide for Manager's commission @ 5% on Net Profits after charging such Commission.

ANSWER:

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Prepaid Insurance

WN3: Calculation of Advertisement Expenditure Written-off

WN4: Calculation of Manager’s Commission

Manager will not be entitled to any commission because there is a net loss.

Page No 22.97:

Question 18:

State with reasons whether the following are capital or revenue expenditures:

(i) A new machine is purchased for ₹ 60,000, ₹ 800 were spent on its carriage and ₹ 1,500 were paid as wages for its installation.

(ii) A sum of ₹ 40,000 was spent on painting the new factory.

(iii) ₹ 6,000 were paid for annual insurance premium.

(iv) ₹ 20,000 were spent on repairs before using a second hand generator purchased recently.

(v) ₹ 5,000 were spent on the repair of a machinery.

(vi) ₹ 50,000 were spent for airconditioning of the office of the manager.

ANSWER:

| 1. Capital Expenditure Reason: When a fixed asset is purchased, then all the expenses up to the date at which the asset is put to use are capitalised. So, expenses incurred on carriage and installation of new machinery will be considered as capital expenditure. |

| 2. Capital Expenditure Reason: Whitewashing (or painting) expenses incurred on the building will increase the revenue generating capacity of the building, thus, it will be capitalised and treated as capital expenditure. |

| 3. Revenue Expenditure Reason: Annual insurance premium is a recurring expenditure to carry on day-to-day business activities. Thus, it is a revenue expense. |

| 4. Capital Expenditure Reason: Expenditure incurred once in many years to increase the working capacity and revenue generating capacity of the asset, and then it is termed as capital expenditure. Thus, repairs made to the second hand machinery (purchased recently) are a one-time expense and thus, will be capitalised and treated as capital expenditure. |

| 5. Revenue Expenditure Reason: The amount spent on repairs of machinery is a recurring expenditure and helps in increasing the working capacity of the machinery but does not add value to it. Thus, it is a revenue expense. |

| 6. Capital Expenditure Reason: Expenditure incurred once in many years to increase the working capacity and revenue generating capacity of the asset, and then it is termed as capital expenditure. Thus, amount spent for air conditioning of the manager’s will increase the value of the asset and thus, it is a capital expenditure. |

Page No 22.97:

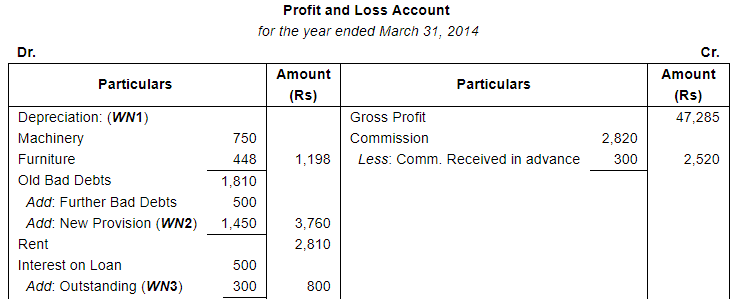

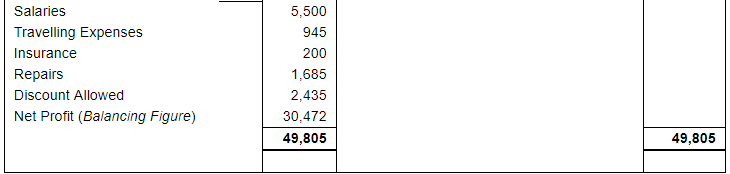

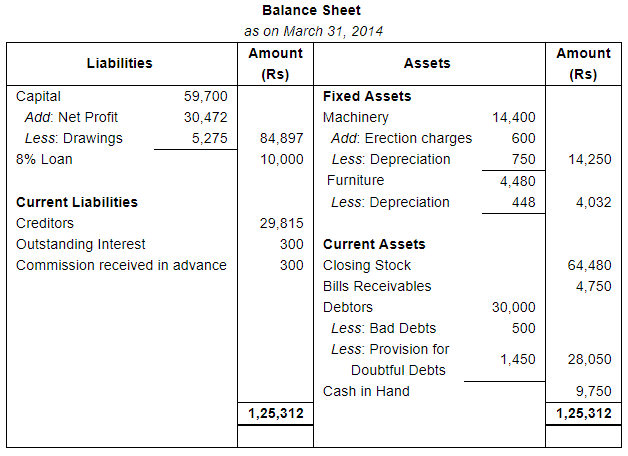

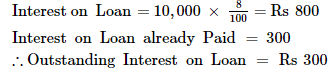

Question 19:

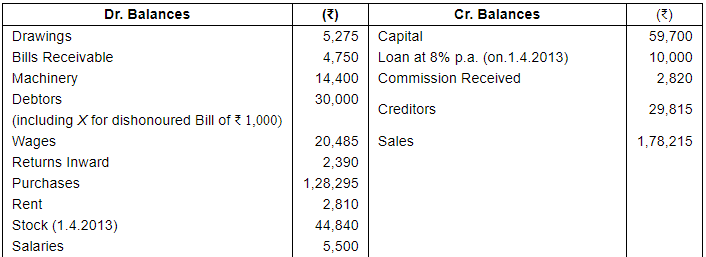

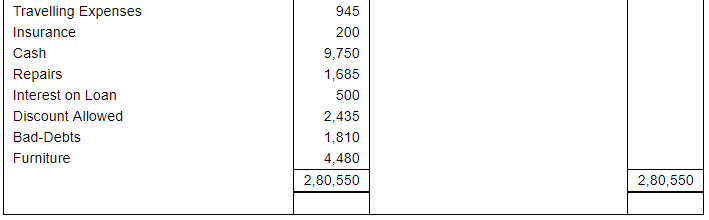

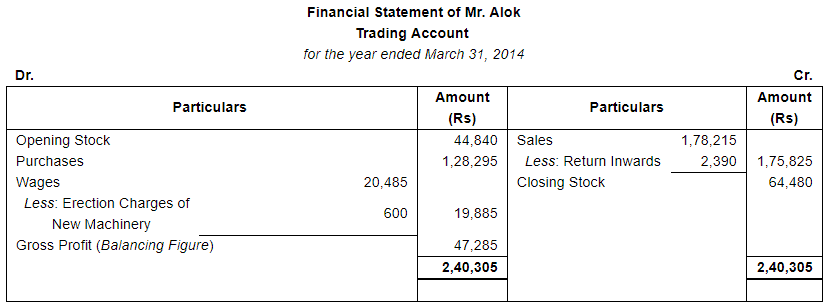

From the following Trial Balance of Mr. Alok, prepare Trading and Profit & Loss Account for the year ending 31st March, 2014, and a Balance Sheet as at that date:-

The following adjustments are to be made:

(i) Stock in the shop on 31st March, 2014 was ₹ 64,480.

(ii) Half the amount of X's Bill is irrecoverable.

(iii) Create a provision of 5% on other debtors.

(iv) Wages include ₹ 600 for erection of new Machinery.

(v) Depreciate Machinery by 5% and Furniture by 10%.

(vi) Commission includes ₹ 300 being Commission received in advance.

ANSWER:

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Provision for Doubtful Debts

Provision for Doubtful Debts

WN3: Calculation of Outstanding Interest on Loan

Page No 22.98:

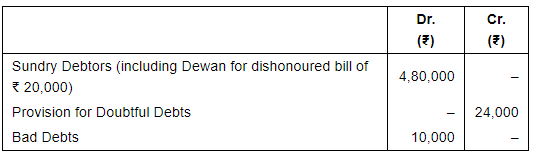

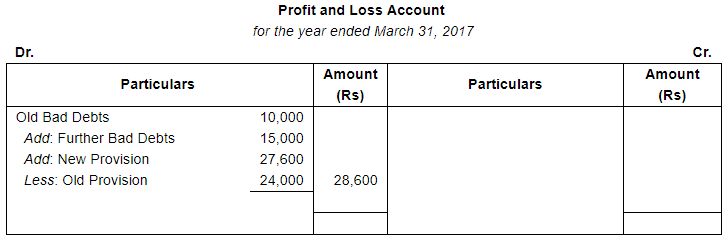

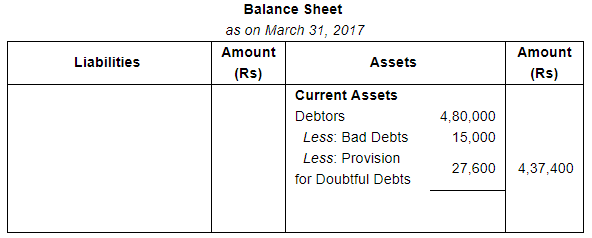

Question 20:

Extracts of Trial Balance as at 31st March, 2017:

Adjustments:

(i) 3/4th of Dewan's bill is irrecoverable.

(ii) Create a provision of 6% on Sundry Debtors.

Show the effect on Profit and Loss Account and Balance Sheet.

ANSWER:

Working Note:

WN1: Calculation of Provision for Doubtful Debts

Provision for Doubtful Debts

*Provision is to be maintained on Debtors other than Dewan

Page No 22.99:

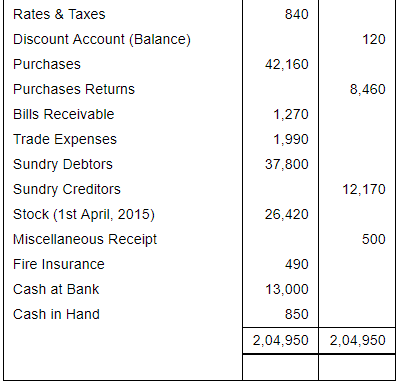

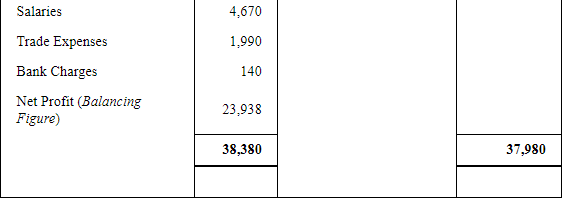

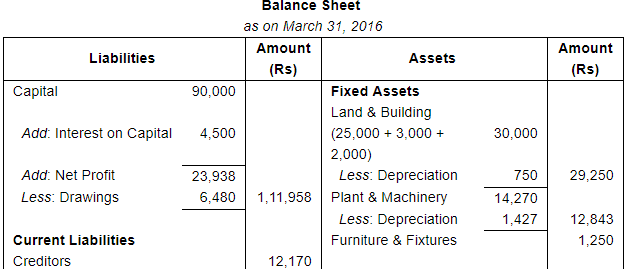

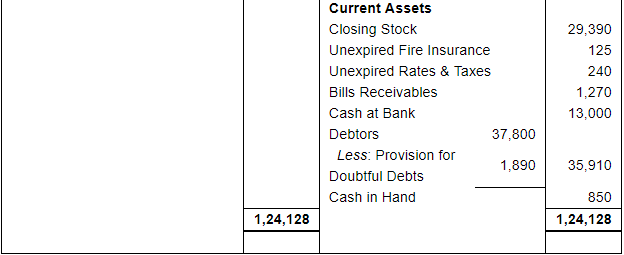

Question 21:

From the following Trial Balance extracted from the books of S. Sujan Singh, prepare a Trading and Profit & Loss Account for the year ended 31st March, 2016 and a Balance Sheet as at that date:

Adjustments:-

1. Carry forward the following unexpired amounts:-

(i) Fire Insurance - ₹ 125

(ii) Rates and Taxes - ₹ 240

2. Transfer to Building Account ₹ 3,000 from purchases and ₹ 2,000 from wages, representing cost of material and labour spent on additions to Building made during the year.

3. Charge Depreciation on Land and Buildings at 2.5% and on Plant & Machinery at 10%.

4. Make a Provision of 5% on Sundry Debtors for Bad-debts.

5. Charge 5% Interest on Capital but not on Drawings.

6. The value of Stock as on 31st March, 2016 was ₹ 29,390.

ANSWER:

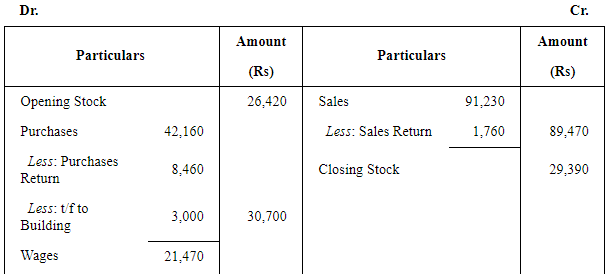

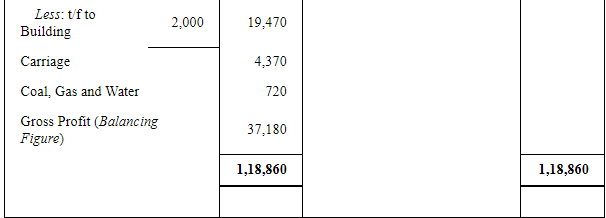

Financial Statements of S. Sujan Singh

Trading Account

for the year ended March 31, 2016

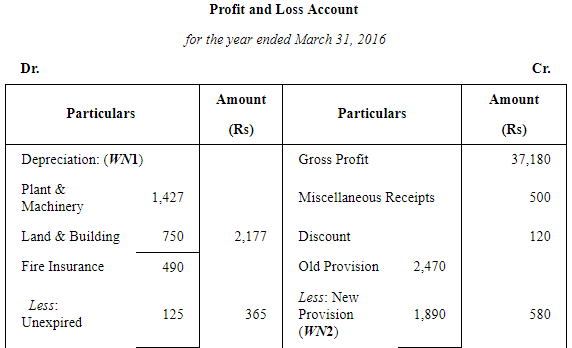

Working Notes:

WN1: Calculation of Amount of Depreciation

WN2: Calculation of Provision for Doubtful Debts

Provision for Doubtful Debts

FAQs on Financial Statements with Adjustments (Part - 2) - Commerce

| 1. What are financial statements with adjustments? |  |

| 2. Why are adjustments necessary in financial statements? | |

Ans. Adjustments are necessary in financial statements to ensure that the financial statements accurately represent the financial position of the business. These adjustments are made to correct errors, record additional transactions and accruals, and to comply with accounting standards and principles. Adjustments are necessary to ensure that the financial statements provide the users with reliable and relevant information for decision-making.

| 3. What is the process of making adjustments in financial statements? | |

Ans. The process of making adjustments in financial statements involves identifying the necessary adjustments, analyzing the impact of the adjustments on the financial statements, and making the adjustments in the trial balance. The adjustments are made to correct errors, record additional transactions and accruals, and to comply with accounting standards and principles. Once the adjustments have been made, the adjusted trial balance is used to prepare the financial statements.

| 4. What are the types of adjustments made in financial statements? | |

Ans. The types of adjustments made in financial statements include accruals, deferrals, depreciation, bad debts, and inventory adjustments. Accruals are adjustments made for revenues or expenses that have been earned or incurred but have not been recorded in the accounting system. Deferrals are adjustments made for revenues or expenses that have been received or paid but have not been earned or incurred in the current period. Depreciation adjustments are made to account for the wear and tear of fixed assets. Bad debt adjustments are made to account for the non-payment of accounts receivable. Inventory adjustments are made to account for the change in the value of inventory.

| 5. What is the importance of financial statements with adjustments? | |

Ans. Financial statements with adjustments are important because they provide the users with accurate and relevant information about the financial position of the business. The adjustments ensure that the financial statements comply with accounting standards and principles and accurately represent the financial position of the business. Financial statements with adjustments provide the users with a better understanding of the business's financial performance and enable them to make informed decisions. Additionally, financial statements with adjustments can help the business identify areas for improvement and make better financial decisions.

Related Exams

About this Document

13.6K Views

4.76/5

Rating

Mar 02, 2025

Last updated

Document Description: Financial Statements with Adjustments (Part - 2) for Commerce 2025 is part of Commerce preparation. The notes and questions for Financial Statements with Adjustments (Part - 2) have been prepared according to the Commerce exam syllabus. Information about Financial Statements with Adjustments (Part - 2) covers topics like and Financial Statements with Adjustments (Part - 2) Example, for Commerce 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Financial Statements with Adjustments (Part - 2).

Introduction of Financial Statements with Adjustments (Part - 2) in English is available as part of

our Commerce preparation & Financial Statements with Adjustments (Part - 2) in Hindi for Commerce

courses. Download more important topics, notes, lectures and mock test series for Commerce

Exam by signing up for free. Commerce: Financial Statements with Adjustments (Part - 2) - Commerce

Description

Full syllabus notes, lecture & questions for Financial Statements with Adjustments (Part - 2) - Commerce - Commerce | Plus excerises question with solution to help you revise complete syllabus | Best notes, free PDF download

Information about Financial Statements with Adjustments (Part - 2)

In this doc you can find the meaning of Financial Statements with Adjustments (Part - 2) defined & explained in the simplest way possible.

Besides explaining types of Financial Statements with Adjustments (Part - 2) theory,

EduRev gives you an ample number of questions to practice Financial Statements with Adjustments (Part - 2) tests, examples and also practice Commerce tests.

Related Searches

practice quizzes

,ppt

,Extra Questions

,Important questions

,past year papers

,Financial Statements with Adjustments (Part - 2) - Commerce

,study material

,mock tests for examination

,Viva Questions

,Sample Paper

,Summary

,Exam

,Financial Statements with Adjustments (Part - 2) - Commerce

,video lectures

,Financial Statements with Adjustments (Part - 2) - Commerce

,Free

,Objective type Questions

,MCQs

,Previous Year Questions with Solutions

,shortcuts and tricks

,Semester Notes

;

Additional Information about Financial Statements with Adjustments (Part - 2) for Commerce Preparation

Financial Statements with Adjustments (Part - 2) Free PDF Download

The Financial Statements with Adjustments (Part - 2) is an invaluable resource that delves deep into the core of the Commerce exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Financial Statements with Adjustments (Part - 2) now and kickstart your journey towards success in the Commerce exam.

Importance of Financial Statements with Adjustments (Part - 2)

The importance of Financial Statements with Adjustments (Part - 2) cannot be overstated, especially for Commerce aspirants.

This document holds the key to success in the Commerce exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Financial Statements with Adjustments (Part - 2) Notes

Financial Statements with Adjustments (Part - 2) Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Financial Statements with Adjustments (Part - 2).

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Financial Statements with Adjustments (Part - 2) Notes on EduRev are your ultimate resource for success.

Financial Statements with Adjustments (Part - 2) Commerce Questions

The "Financial Statements with Adjustments (Part - 2) Commerce Questions" guide is a valuable resource for all aspiring students preparing for the

Commerce exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Financial Statements with Adjustments (Part - 2) on the App

Students of Commerce can study Financial Statements with Adjustments (Part - 2) alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Financial Statements with Adjustments (Part - 2),

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Financial Statements with Adjustments (Part - 2) is prepared as per the latest Commerce syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup