Forms Of Market Class 12 Economics

| Table of contents |

|

| Market |

|

| Perfect competition |

|

| Monopoly |

|

| Monopolistic Competition |

|

| Oligopoly |

|

| Collusive and Non-Collusive Oligopoly |

|

| Other Forms of Market |

|

| Monopsony |

|

| Oligopsony |

|

| Natural Monopoly |

|

Market

- It refers to an entire area where buyers and sellers of a commodity are in contact with each other and sale/ purchase takes place.

- It doesn’t refer to any particular area or place, and face-to-face contact is not necessary as transactions can be effected through telephone, letter, internet, or TV-shop.

Market on the basis of competition or level of influence of individual sellers on the market:

Perfect competition

It is a market situation where there is a large number of buyers and sellers selling homogenous goods at a single uniform price. The price in this market is set by industry by the free play of demand and supply.

Features

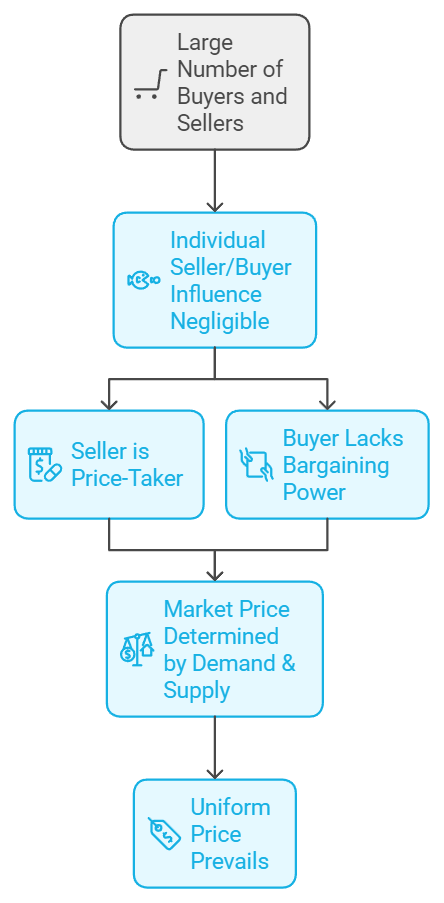

1. Large number of buyers and sellers:

- The “large number” indicates the ineffectiveness of a single seller or buyer in influencing the prevailing market price on its own, as each seller or buyer has an insignificant share of market supply or market demand.

- Implication: The output sold by each firm is very small compared to the total output of all the firms combined.

- Thus by increasing or decreasing the quantity supplied, a seller cannot affect market supply as he sells only a small proportion of the market supply.

- In this way, the firm doesn’t have bargaining power and hence is a price-taker. Similarly, individual buyer share in market demand is insignificant, and hence a single buyer doesn’t have any bargaining power and is unable to influence the price.

- The price of a commodity is determined by the market forces of demand & supply and each buyer and seller has to accept the same price. Hence uniform price prevails.

2. Homogenous products:

- Those goods which are identical with respect to quality, size, design, and colour are called homogenous goods.

- Such products are perfect substitutes or perfect standardized products that buyers do distinguish the product of one firm from that of another.

- This makes their cross-elasticity infinite, i.e. can be readily substituted for each other.

- Implication: A seller cannot afford to charge a high price for a homogenous good as the buyer has the option to purchase the same product from another seller. Uniform price prevails for the products of all the firms in the industry, and those who charge high prices lose their customers.

3. Free entry and exit:

- There are no legal restrictions or barriers to the entry or exit of firms. Firms are free to start producing the commodity or to stop production. A firm seeking profit can enter the market, and any firm suffering losses can exit the market.

- Implication: This ensures that no firm can earn above-normal profits in the long run. Each firm earns just the normal profits, i.e. Minimum necessary to carry on business.

4. Perfect knowledge:

- Buyers and sellers are fully aware of the price and other market conditions.

- Implication: No firm has any cost advantage. Thus all the firms earn uniform profits.

- Buyers also have perfect knowledge about the product market. The buyers will not pay a higher price because they have perfect knowledge. There is no ignorance factor operating in the market. Thus a uniform price prevails in the market.

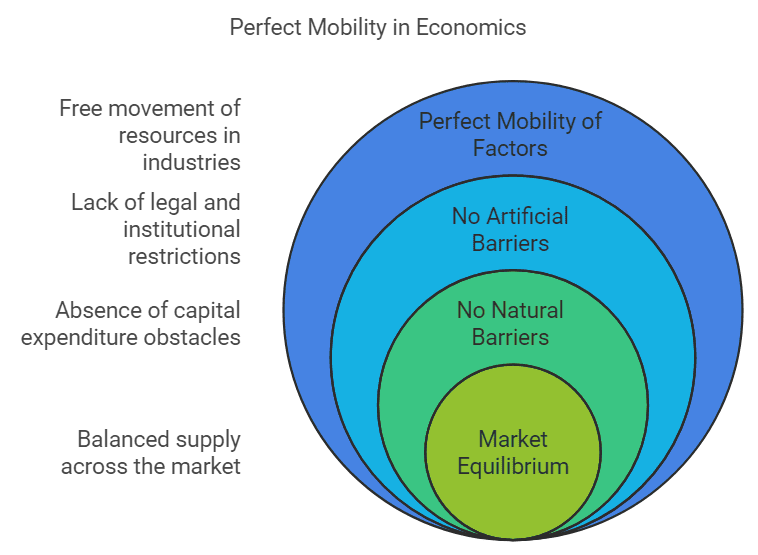

5. Perfect mobility of factors:

- The resources used in the production process like energy, labour, and raw materials can move easily in and out of an industry.

- There are no artificial barriers (trade union, license requirement, patent rights, legal restrictions, etc), and factors can move to the industry that pays the highest remuneration and no natural barrier which may take the form of huge capital expenditure required to start a new firm.

- Implication: The market supply of the commodity and factors of production are equal in all parts of the market. There cannot exist a shortage of the commodity and factors of production in some parts of the market and their excess in other parts of the market.

6. No extra transportation cost:

- It is assumed that different firms work close to each other in such a way that there is no transportation cost and, if any, is part of the cost of production.

7. The demand curve is parallel to the x-axis:

- It means every additional is sold at the prevailing price, and hence AR = MR= perfectly elastic curve. In other words, a firm can sell any quantity at a price determined by the intersection of market demand & market supply by industry.

- Price ‘op’ is determined by industry at the intersection of market demand and market supply. A firm is a price taker who adopts the price and is free to sell any quantity at this price.

Effect of Free Entry and Exit

1. Abnormal profit or super normal profits in the short run: Suppose the market price as given (determined) by the industry is high enough such that the firms are making an abnormal profit this situation will attract new firms to enter the industry.

- On the one hand, more firms will mean more supply leading to falling in the price of the product, and

- On the other, it will lead to more demand for factors like land, and labour which causes factor prices (rent, wages) to rise and consequently higher average cost (AC).

Thus, the fall in the price of the product and rise in ac of production will lead to falling in abnormal profit. This process will continue till abnormal profits are zero. Hence, free entry will push down the long-period price to the level of AC of production, and thus firms will earn only normal profits.

2. Losses in the short run: Suppose the market price as determined by the industry is low enough such that firms are incurring losses. In the short run, a firm can afford to incur losses (equal to fixed costs) but never in the long run. Hence, in the situation of losses (abnormal losses), some existing inefficient firms will quit (leave) the industry. Less number of firms in the industry will mean less supply (output) and consequently a rise in the price of the product. This process of quitting the industry firms will continue till there are no abnormal losses and only normal profits.

Pure and Perfect competition

Pure competition is part and parcel of perfect competition, and it is used in a restricted sense. If only the first three conditions are fulfilled, it is pure competition, and when all conditions prevail, it is a case of perfect competition.

Monopoly

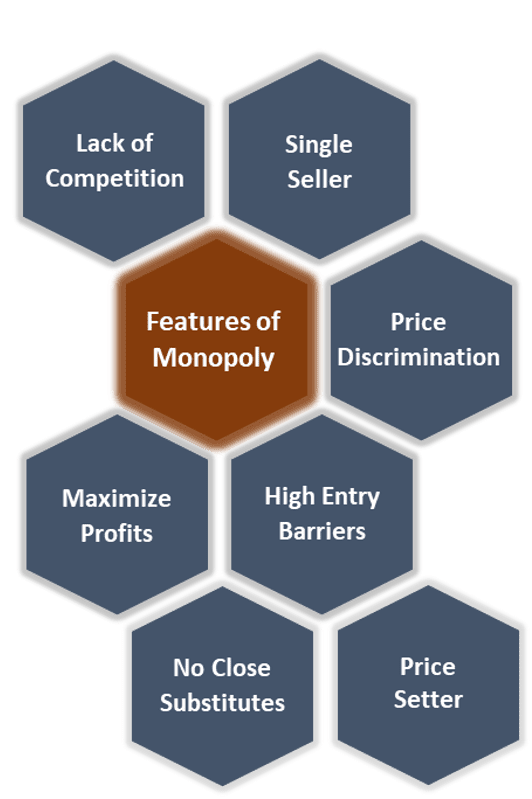

It is a market situation in which there is a single firm selling the commodity, and there is no close substitute for the commodity. It is derived from two Greek words, “monos” meaning single, and “poly” meaning seller.

Features

1. Single seller and large lumber of buyers:

- There is a single seller of a commodity, and it may be in the form of a firm, a group of firms, a joint stock company, or a state corp. or govt. undertaking.

- However, there are a large number of buyers who have weak bargaining power and no influence on the price.

- Implication: Since a monopoly produces the industry’s entire output, there is no distinction between firm and industry. A monopoly firm is also an industry in itself. Having full control over the supply makes a monopoly price-maker. Monopoly firm usually exploits the buyers by charging a higher price for their product. This firm is able to earn supernormal profits in the long run.

2. No close substitute:

- The product sold by monopolists has no perfect substitute.

- Implication: Because cross elasticity is zero, the consumers have to buy the product from a monopolist or go without it.

- The monopoly firm has no fear of competition from new or existing products. This feature helps monopolists to determine the price they like.

3. Barriers to entry:

- There are legal, natural, or technical barriers to the entry of new firms so as to avoid competition and control the supply and hence the price of the commodity.

- Barriers can be in the forms of patent rights, control over technique, or raw material, govt. Laws etc.

- Implication: Thus firm is able to earn supernormal profit in the long run.

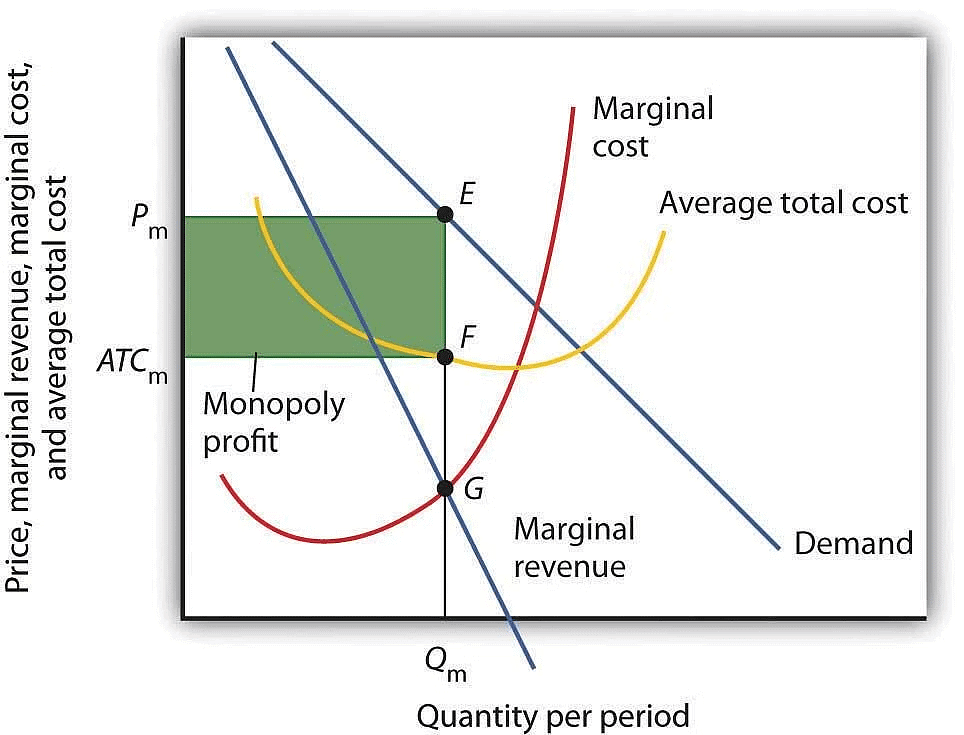

4. Full control over price:

- A monopoly firm is an industry in itself and hence a price maker.

- The above-noted feature makes the firm exert full control over the supply of the product and hence full control over the price of the product.

- As a result, a monopoly firm can earn abnormal profits and losses in the long run.

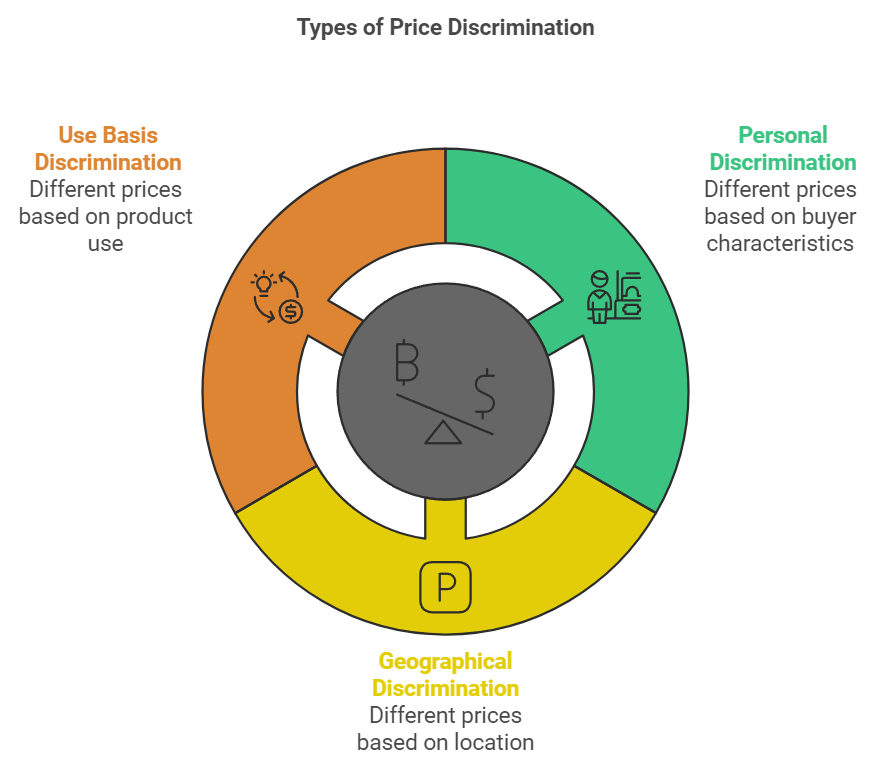

5. Possibility of price discrimination:

- A monopolist often charges different prices to different customers or markets or uses for the same product.

- This price policy is called price discrimination, and the monopolistic practice of this is termed a discriminating monopoly. It can be of three types

(i) Personal price discrimination: In this, the same product is sold at different prices to different kinds of buyers.

For example Railway ticket is cheaper for senior citizens as compared to young citizens, and doctor charges more for a rich person and less for a poor patient for the same service.

(ii) Geographical discrimination: Under this same product is sold at different places.

For example, Electricity charges are lower for rural areas compared to urban areas, the Food Corporation of India (FCI) sells rice at different prices in Jammu and Kashmir, and Himachal Pradesh.

(iii) Use basis discrimination: In this type, the same product is sold at different prices on the basis of different uses. The electricity board charges different rate slabs for electricity being used for commercial, industrial, agricultural, and household purposes. - Implication: A monopolist can increase its profit if it is possible to charge different prices from different markets. So consumers are exploited.

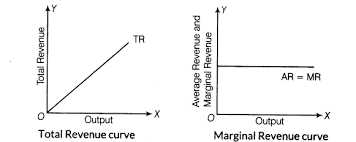

6. The demand curve is downward sloping:

- To sell more quantity, a monopoly firm has to reduce the price of the product in spite of being a price maker.

- Full control over price doesn’t mean that a firm can sell any amount at a fixed price.

- If he fixes a high price, buyers will purchase less. Thus an inverse relationship exists between the price fixed by monopolists and the quantity sold. This makes the demand curve(AR curve) downward sloping, and the MR curve is below the AR curve.

- Implication: The monopolist tries to increase profit by restricting the supply of products and fixing high prices. Accordingly, the greater the monopoly power in any market, the lesser would be the output and the higher would be the price. This form of the market goes in favour of the seller.

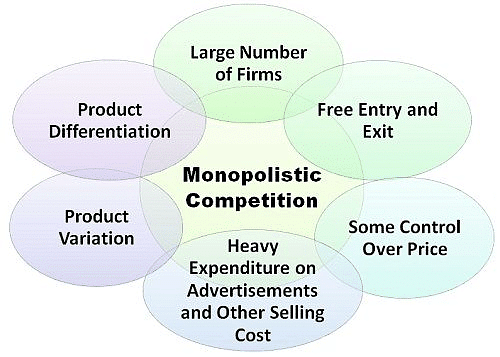

Monopolistic Competition

It is a market situation that has elements of both perfect competition and monopoly.

Markets of products like soap, toothpaste, AC, tea, cycles, etc are examples of monopolistic competition.

Features

1. A large number of sellers and buyers:

- Each firm acts independently, each firm has a limited share of the market, and the size of each firm is small. However, this number is less than the number of sellers in perfect competition.

- Implication: A large number of firms leads to competition in the market. This prevents the firm from having full control over price. However, firms are in the position to influence the price of their own products depending upon the popularity of their brands.

2. Freedom of entry and exit:

- The freedom to enter and exit is there, but firms don’t have absolute freedom to enter into the industry as some firms are legally patented and carry a brand name.

- Implication: There are many sellers, but each producer is the sole producer of its brand or product. Thus it enjoys a “monopoly“ position as far as a particular brand is concerned. However, since the various brands are close substitutes, its monopolistic position is influenced due to stiff “competition” from other firms. All firms earn normal profits in the long run.

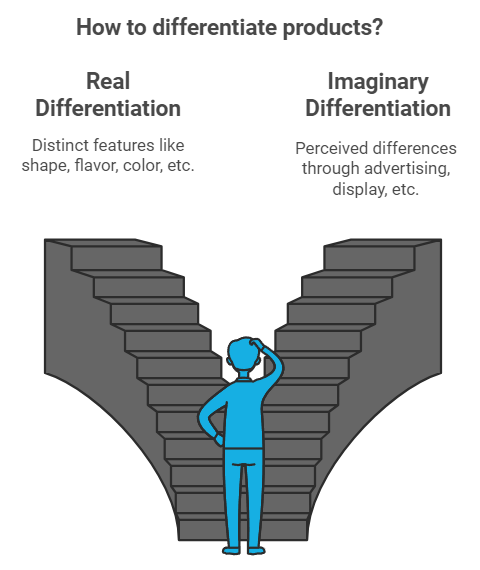

3. Product differentiation:

- Product differentiation refers to differentiating the product on the basis of brand, size, colour, shape, etc. Differentiating can be based on

(a) Real difference: It may be due to differences in shape, flavour, colour, packing, after-sale service, warranty period, design, workmanship, colour, packaging, etc.

(b) Imaginary differences: It means differences that are not really obvious, but buyers are made to believe that such differences exist through selling costs (advertising), display, attractive showrooms, credit facilities, and home delivery systems.

Examples: We have product differentiation in soaps, toothpaste, and cosmetics.

- Implication: A high degree of product differentiation ( better brand image) increases demand for the product and enables the firm to charge a price higher than its competitor's products. Product differentiation creates a monopoly position for a firm i.e., some monopoly power to influence the price. This gives monopolistic partial control over price as if a particular product is preferred by the consumer, he will be ready to pay a higher price.

4. Selling cost:

- Selling costs are the expenses that are incurred for promoting sales or for inducing customers to buy the goods of a particular brand.

- These include the cost of advertisement through newspapers, tv, and radio, free sampling, show windows, salaries of salesmen, and costs of other sales promotion activities. These costs are also called advertisement costs.

- Implication: Selling cost creates artificial superiority in the minds of the consumer. As a result firm’s demand curve shifts to the right. However, it also tends to increase the cost of production.

5. Lack of perfect knowledge:

- Due to a large number of buyers and product differentiation, it is not possible to compare the prices of different products, and thus, buyers are not fully aware of the prevailing prices of all products.

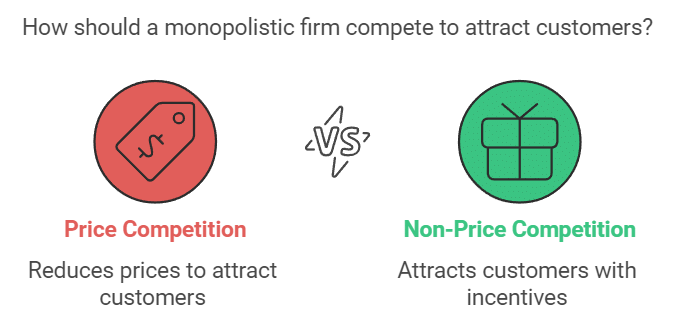

6. Non-price competition:

- Monopolistic firms generally don’t disturb the price of products, and they attract customers by giving free gifts, services, coupons, and other attractive schemes.

- Thus non-price competition refers to competing with other firms by offering free gifts, making favourable credit terms, etc without changing the prices of their own products.

For example: With the purchase of surf, customers get a bucket free or a scratch card to win exotic holidays with every purchase of Samsung product or a 0% finance facility. - Firms under monopolistic competition compete in a number of ways to attract customers. They use both price competition (i.e., competition by reducing the price of the product) and non-price competition to promote their sales.

7. Downward sloping demand curve:

- It means to sell more, a firm has to reduce price, but due to the availability of close substitutes, it is more elastic or flatter than the demand curve of a monopoly firm.

8. Less mobility:

- There is no perfect mobility of factor owners as factors of production are not fully aware of prices being paid by different firms to factor owners for their services.

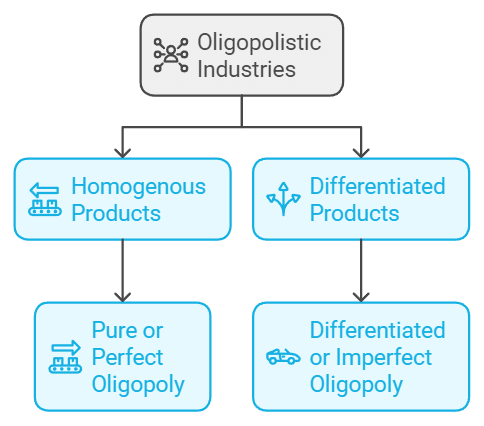

Oligopoly

An oligopoly is a market situation with only a few large sellers. The oligopoly is derived from the Greek words “oligo,” which means few, and poly means “control” or “seller.” Thus, it is a market situation where a few large firms sell either homogenous or differentiated products with a high degree of interdependence among the sellers regarding their price and output policy.

A special case of oligopoly: Duopoly is a special case of oligopoly in which there are exactly two sellers selling almost the same (homogenous product).

Example: Pepsi and Coca-Cola in the soft drink market

Features

1. Few sellers and many buyers:

- An oligopoly is a market structure in which few firms dominate the industry: for example, in India, Maruti, Hyundai, and Tata produce a majority of small cars.

- Implication: Each firm commands a significant share of the market and thus can impact the market price of the product. Also, there exists severe competition among different firms, and every firm keeps a close watch on the activities of rival firms.

2. Homogenous or differentiated products:

- Firms in oligopolistic industries may produce either homogenous or differentiated products. If the firms produce a homogenous product like cement, steel, LPG or aluminium, the industry is called a pure or perfect oligopoly.

- If the firms produce differentiated products like automobiles, the industry is called a differentiated or imperfect oligopoly.

3. Mutual interdependence:

- A very important feature of oligopoly is the mutual interdependence of the firms. Mutual interdependence means that firms are significantly affected by each other’s price and output decisions.

- Since, in an oligopoly, a limited number of firms compete with each other, the sales of one firm depend upon that firm's price and the price charged by other firms.

Implication: It leads to a price war if one firm lowers the price, its own sales will increase, but the sales of other firms in the industry decrease. In such a situation, the other firms will, most likely, lower their prices, too. There are a large number of difficulties faced in price determination. The indeterminate demand curve is the major difficulty faced by each firm.

4. Advertisement:

- An oligopoly firm has to incur a lot of expenditure on advertisement.

- Given the high cross-elasticity of demand for production and price rigidity, the only way open to the oligopolist firm is to promote its sales by advertising its product. The expenditure on advertisement is aimed primarily at shifting the demand in favor of the advertised product.

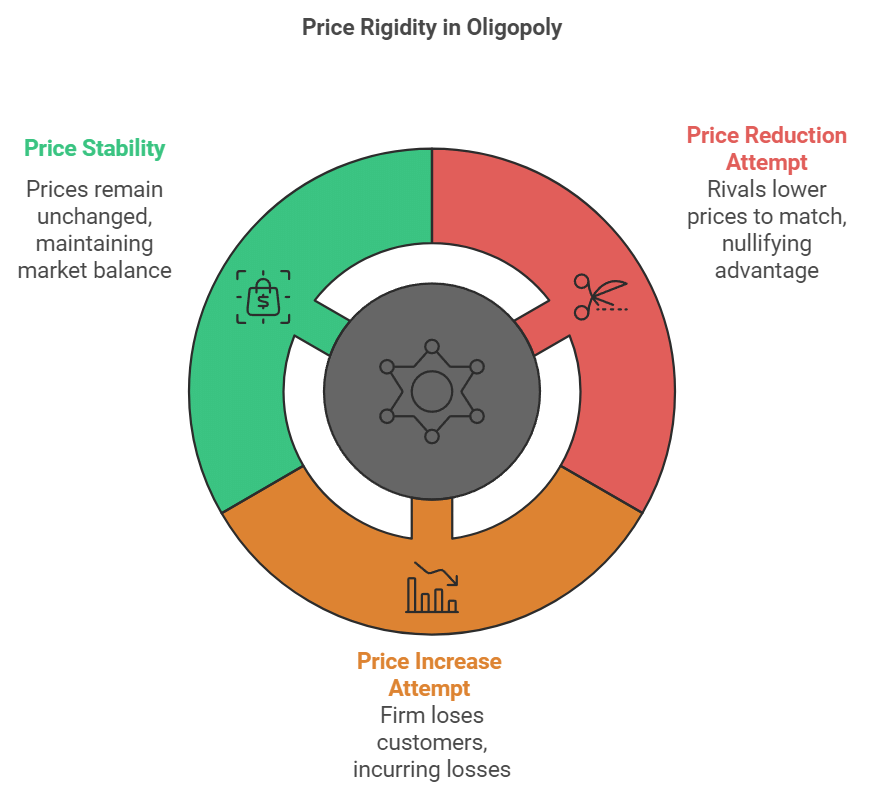

5. Existence of price rigidity:

- The term price rigidity means that firms would not like to change their prices. It will stick to its price.

- If a firm tries to reduce the price, the rivals will also reduce their prices so that it will not be of any advantage to it.

- Likewise, if a firm tries to raise its price, other firms will not do so. As a result, the firm will lose its customers and incur losses. So there is price rigidity in an oligopolistic market.

6. Some barriers to entry:

- Usually, an oligopolistic firm is also characterized by barriers to entry in the industry.

- Some common barriers to entry are the economics of scale, the absolute cost advantage of old firms, patent rights, control over important inputs, preventive price, and prevailing excess capacity, etc.

- Such barriers prevent the entry of new firms.

7. Non-price competition:

- Oligopolistic firms generally don’t disturb the price of products, and they attract customers by giving free gifts, services, coupons, and other attractive schemes.

- Thus non-price competition refers to competing with other firms by offering free gifts, making favorable credit terms, etc without changing the prices of their own products.

Example: In India, both Coca-Cola and Pepsi sell at the same price. However, in order to increase sales and market share, each firm tries to resort to non-price competition:

(a) sponsoring different games and shows

(b) offering many schemes

(c) sponsoring school and college canteen

8. Indeterminate the firm’s demand curve:

- As there is a high degree of interdependence between the firms, the firm's demand curve is indeterminate under an oligopoly.

- The price and output policy of one firm have a significant impact on the rival firm’s price and output policy in the market. It is hard to estimate a change in a firm’s sales caused by a change in price.

Collusive and Non-Collusive Oligopoly

The Emergence of Oligopoly/Monopoly or Why Does Oligopoly/Monopoly Exist

1. Innovations

- Difficulty due to innovations limits the entry of a number of firms in an oligopoly. Oligopoly is often found in industries started by a major invention or innovation. The innovation may have enabled the innovating firms to establish and then maintain their dominance of the industry.

- Example: Companies making operating systems for computers and mobiles

2. Control of an essential resource

- An oligopoly may result because a few firms have control of essential resources.

- Example: DeBeers company of South Africa controls about 80% of the world’s production of diamonds.

3. Successful differentiation

- Some firms are able to establish their brands of differentiated products successfully. The successful differentiation can actually make entry more difficult.

- The new firms who want entry should have to spend a huge amount on advertisements to compete with the established brands. Thus successful differentiation also leads to oligopoly.

4. Large fixed costs

- If huge capital investment is necessary to operate a business, new firms will be discouraged from entering the industry. A new firm cannot enter or quit an industry because of the large fixed costs.

- Example: Operating railways involves huge expenditure on infrastructure.

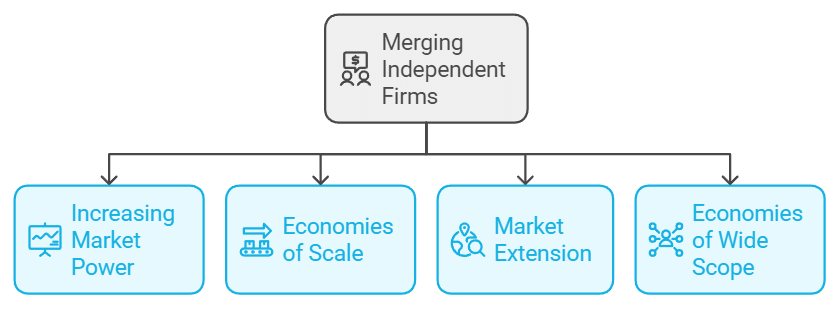

5. Mergers

- Many oligopolies were created by combining two or more previously independent firms. The combination of two or more firms into one firm is called a merger.

- The motives of mergers include

(a) increasing market power

(b) economics of scale

(c) market extension, and economies of wide scope.

6. Patents

- A patent is an exclusive right granted by the government to use some productive technique or to produce a certain product.

- These are granted to the inventor of a technique or product as a reward for risk-taking and investment in r and d. It is a sort of legal right to a monopoly.

7. Government policy

- The government may grant a license to a firm to have the exclusive privilege to produce a given good or service in a particular area. No firm can enter that area without a license provided by the government.

- These licenses are awarded in the case of public utilities like electricity, gas, telephones, and a variety of other situations.

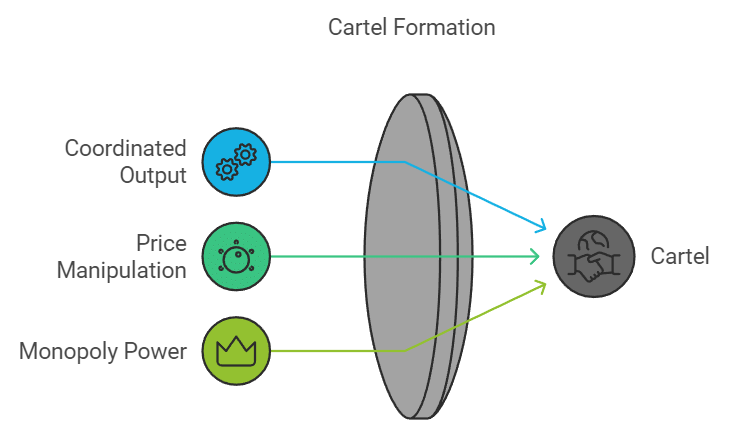

8. Cartel

- It is a business combination under which firms coordinate their output and price to reap the benefits of a monopoly. Thus a cartel is a group of firms that jointly sets the “ output and prices” of its product to exercise monopoly power.

- Example: In 1960, some oil-producing companies formed a cartel by the name of OPEC, which sets production quotas for member states and thereby tries to manipulate the prices of petroleum to derive the highest possible profit.

9. Anti-trust legislation:

- These refer to the laws that prevent big firms from forming trusts or cartels with a view to preventing them from acquiring monopoly control over the market.

- Example: MRTP 1969 Act of India. Now it is replaced by the Competition Act 2002.

Other Forms of Market

Monopsony

- A monopsony refers to a market situation where there is only one buyer, known as the monopsonist. Similar to a monopoly, a monopsony is characterized by an imperfect market condition.

- However, the key distinction lies in the dominant business entity.

- In a monopsony, a single buyer holds control over the market, whereas in a monopoly, a single seller holds control.

- Monopsonies are commonly found in areas where they provide the majority of job opportunities in a specific region.

- For example, a company that employs the entire workforce of a town, such as a sugar factory hires laborers from the entire town to extract sugar from sugarcane.

Oligopsony

- An oligopsony refers to a market situation where a few large buyers have significant influence over the demand for services and products.

- In this scenario, market demand is concentrated among a small number of parties, giving them considerable control over their suppliers and enabling them to effectively keep prices low.

- For instance, the global supermarket industry is evolving into an oligopsony, where a small number of major buyers have substantial power in the market.

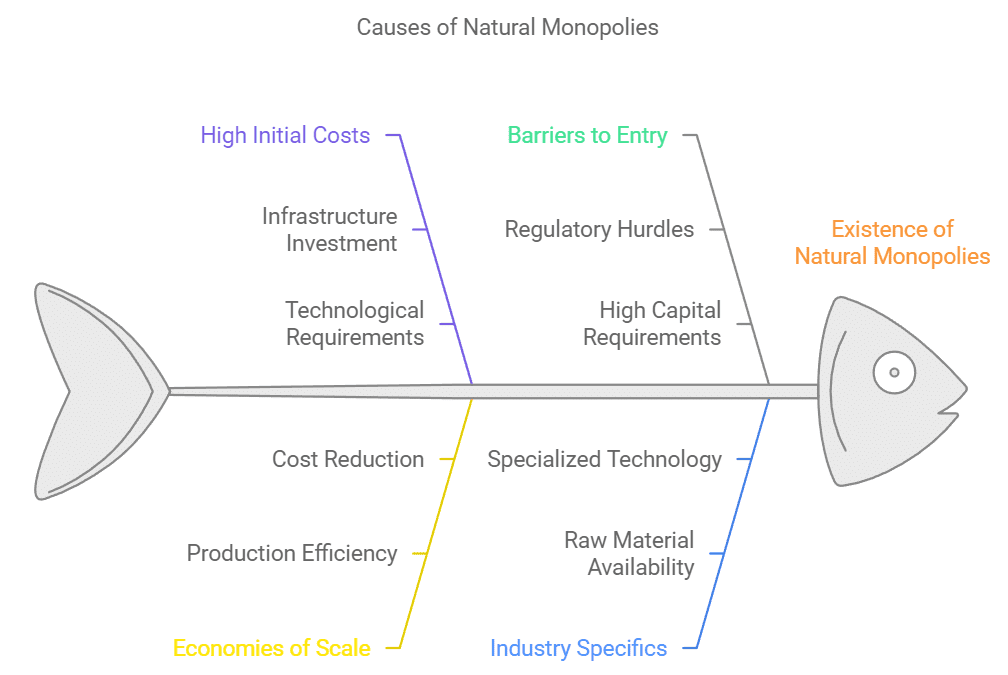

Natural Monopoly

- A natural monopoly is a type of monopoly that occurs naturally due to high initial costs or significant economies of scale in a particular industry.

- This can create substantial barriers for potential competitors to enter or exit the market. In a natural monopoly, a single organization may be the sole provider of a specific service or product within an industry or geographic area.

- Typically, natural monopolies arise in industries that require advanced technology, specific raw materials, or similar factors to operate.

- For instance, the utility service industry, which encompasses the supply of water, electricity, sewer services, and energy distribution to towns and cities nationwide, is an example of a natural monopoly.

|

1335 videos|1436 docs|834 tests

|

FAQs on Forms Of Market Class 12 Economics

| 1. What are the main characteristics of perfect competition? |  |

| 2. How does a monopoly differ from perfect competition? | |

| 3. What are the key features of monopolistic competition? | |

| 4. What distinguishes collusive oligopoly from non-collusive oligopoly? | |

| 5. What is a monopsony and how does it affect the market? | |

Exam

,study material

,Previous Year Questions with Solutions

,MCQs

,Summary

,past year papers

,Sample Paper

,Viva Questions

,Forms Of Market Class 12 Economics

,shortcuts and tricks

,Forms Of Market Class 12 Economics

,Objective type Questions

,Extra Questions

,video lectures

,Free

,ppt

,Semester Notes

,practice quizzes

,mock tests for examination

,Forms Of Market Class 12 Economics

,Important questions

;

Chapter Notes - Forms Of Market Free PDF Download

Importance of Chapter Notes - Forms Of Market

Chapter Notes - Forms Of Market

Chapter Notes - Forms Of Market SSC CGL Questions

Study Chapter Notes - Forms Of Market on the App

|

© EduRev

|

Education Revolution

|

|