ICAI Notes 4: Inventories- 1 - CA Foundation PDF Download

Inventory can be defined as tangible property held for sale in the ordinary course of business, or in the process of production for such sale, or for consumption in the production of goods or services for sale, including maintenance supplies and consumables other than machinery spares. Inventories are assets:

(a) held for sale in the ordinary course of business;

(b) in the process of production for such sale;

(c) in the form of materials or supplies to be consumed in the production process or in the rendering of services. Inventories encompass goods purchased and held for resale, for example merchandise (goods) purchased by a retailer and held for resale, or land and other property held for resale. Inventories also include finished goods produced, or work in progress being produced, by the enterprise and include materials, maintenance supplies, consumables and loose tools awaiting use in the production process. However, inventories do not include machinery spares which can be used only in connection with an item of fixed asset and whose use is expected to be irregular; such machinery spares are generally accounted for as fixed assets.

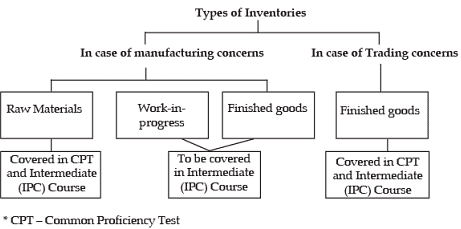

The types of inventories are related to the nature of business. The inventories of a trading concern consist primarily of products purchased for resale in their existing form. It may also have an inventory of supplies such as wrapping paper, cartons, and stationery. The inventories of manufacturing concern consist of several types of inventories: raw material (which will become part of the goods to be produced), parts and factory supplies, work-in-process (partially completed products in the factory) and, of course, finished products.

At the year end every business entity needs to ascertain the closing balance of Inventory which comprise of Inventory of raw material, work-in-progress, finished goods and miscellaneous items. Value of closing Inventory is put at the credit side of the Trading Account and asset side of the Balance Sheet. So before preparation of final accounts, the accountant should know the value of Inventory of the business entity. However, we shall restrict our discussion on inventory valuation for raw materials of a manufacturing concern and goods of a trading concern. The valuation of other types of inventories will be covered in Accounting and Cost Accounting subject at Intermediate (IPC) Course.

2. INVENTORY VALUATION

A primary issue in accounting for inventories is the determination of the value at which inventories are carried in the financial statements until the related revenues are recognized. Inventory is generally the most significant component of the current assets held by a trading or manufacturing enterprise. It is widely recognised that the major asset that affects efficiency of operations is inventory. Both excess of inventory and its shortage affects the production activity, and the profitability of the enterprise whether it is a manufacturing or a trading business. Proper valuation of inventory has a very significant bearing on the authenticity of the financial statements. The significance of inventory valuation arises due to various reasons as explained in the following points:

(i) Determination of income

The valuation of inventory is necessary for determining the true income earned by a business entity during a particular period. To determine gross profit, cost of goods sold is matched with revenue of the accounting period.

Cost of goods sold is calculated as follows: Cost of goods sold = Opening Inventory + Purchases + Direct expenses - Closing Inventory.

Inventory valuation will have a major impact on the income determination if merchandise cost is large fraction of sales price. The effect of any over or understatement of inventory may be explained as:

(a) When closing inventory is overstated, net income for the accounting period will be overstated.

(b) When opening inventory is overstated, net income for the accounting period will be understated.

(c) When closing inventory is understated, net income for the accounting period will be understated.

(d) When opening inventory is understated, net income for the accounting period will be overstated.

The effect of misstatement of inventory figure on the net income is always through cost of goods sold. Thus, proper calculation of cost of goods sold and for that matter, proper valuation of inventory is necessary for determination of correct income.

(ii) ascertainment of Financial Position

Inventories are classified as current assets. The value of inventory on the date of balance sheet is needed to determine the financial position of the business. In case the inventory is not properly valued, the balance sheet will not disclose the truthful financial position of the business.

(iii) Liquidity analysis

Inventory is classified as a current asset, it is one of the components of net working capital which reveals the liquidity position of the business. Current ratio which studies the relationship between current assets and current liabilities is significantly affected by the value of inventory.

(iv) Statutory Compliance

Schedule III to the Companies Act, 2013 requires valuation of each class of goods i.e. raw material, work-in-progress and finished goods under broad head to be disclosed in the financial statements. As per the requirements of the Accounting Standards, the financial statements should disclose (a) the accounting policies adopted in measuring inventories, including the cost formula used, and (b) the total carrying amount of inventories and its classification appropriate to the enterprise. The common classification of inventories are raw materials; work-in-progress; finished goods; stores and spares and loose tools.

3. BASIS OF INVENTORY VALUATION

Inventories should be generally valued at the lower of cost or net realizable value. Pricing of inventory assumes significance when different lots are purchased at varying prices at different timings. In case of no change in price level, determination of historical cost of inventory shall not pose any major problem.

The amount of expenditure incurred on acquisition of goods.

The amount of expenditure incurred on acquisition of goods.

This is the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale. An assessment is made of net realisable value as at each balance sheet date. Inventories are usually written down to net realisable value on an item-by-item basis. In some circumstances, however, it may be approximate to group similar or related items.

This is the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale. An assessment is made of net realisable value as at each balance sheet date. Inventories are usually written down to net realisable value on an item-by-item basis. In some circumstances, however, it may be approximate to group similar or related items.

FAQs on ICAI Notes 4: Inventories- 1 - CA Foundation

| 1. What is the objective of the ICAI Notes 4: Inventories article? |  |

| 2. How are inventories classified under the ICAI Notes 4: Inventories article? | |

| 3. What is the significance of inventory valuation in the context of the ICAI Notes 4: Inventories article? | |

| 4. What are the key accounting principles related to inventories discussed in the ICAI Notes 4: Inventories article? | |

| 5. How does the ICAI Notes 4: Inventories article relate to the CA Foundation exam? | |

|

6.4K Views |

|

4.92/5 Rating |

|

Nov 16, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

Objective type Questions

,shortcuts and tricks

,MCQs

,Semester Notes

,Previous Year Questions with Solutions

,practice quizzes

,study material

,Extra Questions

,ICAI Notes 4: Inventories- 1 - CA Foundation

,ICAI Notes 4: Inventories- 1 - CA Foundation

,video lectures

,Free

,past year papers

,Summary

,Sample Paper

,ICAI Notes 4: Inventories- 1 - CA Foundation

,Viva Questions

,mock tests for examination

,ppt

,Exam

,Important questions

;

ICAI Notes 4: Inventories- 1 Free PDF Download

Importance of ICAI Notes 4: Inventories- 1

ICAI Notes 4: Inventories- 1

ICAI Notes 4: Inventories- 1 CA Foundation Questions

Study ICAI Notes 4: Inventories- 1 on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|