ICAI Notes: Bank Reconciliation Statement - 1 | Principles and Practice of Accounting - CA Foundation PDF Download

| Table of contents |

|

| Overview |

|

| Introduction |

|

| Background |

|

| Bank Pass Book |

|

| Bank Reconciliation Statement |

|

| Importance of Bank Reconciliation Statement |

|

Overview

Introduction

Banks are essential institutions in a modern society. With the increase in volume of trade, commerce and business, business entities faced difficulty in transacting in cash for each business activity. They discovered that dealing through bank, on regular basis, would be the better and safer option and finally large business entities switched over to banking transactions instead of dealing in cash. Now-a-days, most of the transactions of the business are done through bank whether it is a receipt or a payment. Rather, it is legally necessary to operate the transactions through bank after a certain limit. A Bank accepts from people, in general, deposits in various forms, and lends funds to those who need; it also invests some funds in profitable investments. Thus, money which would have been otherwise idle is put to use and is made available to those who need it. Those who deposit the money are able to withdraw it according to the settled terms and conditions. Apart from receiving deposits from and handling cash transactions on behalf of its customers, the bank also renders some other useful services as indicated below:

(i) The bank discounts promissory notes or hundies, i.e., it enables a customer to receive the cash before the due date in consideration of a small charge called discount.

(ii) The bank allows overdraft to its good customers so that they can make payments even when they do not have sufficient balance in the bank. Of course, the overdraft facility is generally secured and must be cleared later.

(iii) The bank grants different types of loans (eg. Working capital, term loan) for a specific period say a year or so, to its customers for smooth functioning of their operations in case of lack of self-funding available with customers’. Such financial assistance is of great help for business.

(iv) The bank on behalf of the customer collects the amount of dividend warrants or interest on securities etc.

(v) On instruction of the customer, the bank makes payments of insurance premium, rent etc. on the due dates.

(vi) The bank sells and purchases shares, debentures or government securities on behalf of its customers.

(vii) Money can be remitted to another place or persons through the bank at a low cost.

(viii) The bank in return, for a consideration, furnishes security or guarantee for its customers whose credit is good.

(ix) The bank also issues letter of credit or travellers’ cheque to facilitate commerce or travel.

(x) The bank also provides international banking services such as currency exchange, remittance from abroad, cross country payments, foreign letters of credit, export and import credit, etc.

Background

In the past, many corporate frauds have incurred by the companies through manipulating entries either in bank statements or in cash book. For e.g. –A company’s financial statement may present incorrect bank balance to mislead the stakeholders. Such kind of instances has made reconciliation of bank and cash balances an integral part of internal control maintained by management. Over the period, reconciling the accounts became an important activity for businesses because it gives an opportunity to check for fraudulent activity happening in the organization and helps to prevent the financial statement errors. Reconciliation is typically done at regular intervals, such as monthly or quarterly, as part of normal accounting procedures, however, frequency is largely dependent on the size of organization and the number of transactions that occur.

Bank Pass Book

Bank pass book is merely a copy of the customer’s account in the books of a bank. The bank either sends periodical statements of account or gives a pass book to its customer in which all deposits and withdrawals made by the customer during the particular period is recorded. Both represent almost a copy of the ledger account of the customer in the books of the bank. Thus, it is the bank’s way of keeping the customers informed of the entries made in his account. It is the customer’s duty to check the entries and immediately inform the bank of any error that he may notice. These days, customers can easily access their bank statement online any time as facilitated by Net Banking. The form of the pass book is given below:

Pass Book

Messers.........................................

in account with

Punjab National Bank

Daryaganj, New Delhi-110002

Account number –

Transaction Period - The bank statement of account also has a similar form except that it is on loose sheets or can be in an online format. The bank itself sends the statements to customers but if the customer wants to maintain a pass book then it is their duty to send the pass book to the bank periodically so that it is updated by the bank. These days, many banks’ ATMs have the automated machines where one can get the passbook updated without any manual intervention and without visiting the branch of the bank.

The bank statement of account also has a similar form except that it is on loose sheets or can be in an online format. The bank itself sends the statements to customers but if the customer wants to maintain a pass book then it is their duty to send the pass book to the bank periodically so that it is updated by the bank. These days, many banks’ ATMs have the automated machines where one can get the passbook updated without any manual intervention and without visiting the branch of the bank.

Business houses should also obtain at the end of the year a certificate from the bank duly stamped and signed, showing the balance which, the firm carries with the bank as of date. The bank balance shown in the passbook is known as pass book balance for reconciliation purpose. The credit balance as per pass book at a particular point of time is the deposit made by the customer while debit balance as per pass book is the overdraft balance for the customer (i.e. customer owes to bank). Students may note here that the nature of balance shown by passbook (in the books of bank) and cash book (in the books of customer) is quite different. The debit balance in the pass book represents the credit balance as per the cash book and vice-versa because the business enterprise treats the bank as a debtor/Trade receivable and bank treats the business enterprise as a creditor/Trade payable.

Bank Reconciliation Statement

To reconcile means to identify or find out the difference between two different sources and eliminating that difference. Whenever we deposit or withdraws money from banks, it is always recorded at two places:-

The cash book is maintained by the person having the bank account whereas the bank statement is prepared by the bank. Therefore, the balance in both the books should be equal and opposite in nature. For eg:- if Mr. A deposited ₹ 1,00,000 in his bank account it will be recorded on the Dr. side of his cash book, but for the bank it’s a receipt so it will be recorded as a Cr. Entry in the bank statement or the pass book. But most of the times these two balances do not match. The reasons for difference in balances can be many and are explained later in this chapter. It is possible to eliminate this difference by matching all the facts and figures of the two statements. The process of eliminating this difference and bringing the two statements in line with each other is known as “Reconciliation”, and the statement which reconciles the bank balance as per cash book with the balance as per the pass book by showing all the causes of difference is known as “Bank Reconciliation Statement”.

Importance of Bank Reconciliation Statement

Bank reconciliation statement is a very important tool for internal control of cash flows. It helps in detecting errors, frauds and irregularities occurred, if any, at the time of passing entries in the cash book or in the pass book, whether intentionally or unintentionally. Since frauds can be detected on the preparation of bank reconciliation statement therefore accountants are careful while preparing and maintaining the records of the business enterprise. Hence it works as an important mechanism of internal control. Following are the salient features of bank reconciliation statement:

(i) The reconciliation will bring out any errors that may have been committed either in the cash book or in the pass book;

(ii) Any undue delay in the clearance of cheques will be shown up by the reconciliation;

(iii) A regular reconciliation discourages the accountant of the bank from embezzlement of funds. There have been many cases when the cashiers merely made entries in the cash book but never deposited the cash in the bank; they were able to get away with it only because of lack of reconciliation.

(iv) It helps in finding out the actual or true position of the bank balance by incorporating the effect of any uncleared funds as well.

(v) It will ensure accounting of all the financial transactions incurred by the company during a particular financial year.

Causes of Difference

The difference in the both balances (bank balance as per cash book and pass book) may arise because of the following reasons:-

- Timing: Sometimes a transaction is recorded at two different times in cash book and the pass book. This may happen in the following cases:-

- Mr. A has issued a cheque to PQR ltd., now it will be recorded in his cash book immediately but the bank will recognize this transaction only when the same cheque will be presented to it by PQR ltd.

- Similarly for PQR Ltd , entry in the cash book will be made immediately as the cheque is received from Mr. A but the bank account will be credited when it collects money in respect of that cheque.

- Transactions: There are various transactions which the bank carries out by itself without intimating the customer. For e.g.: interest received on a savings bank account, it will be credited by the bank immediately but the entry in the cash book will be made only when the customer comes to know about it, which is usually at a later stage. Similar is the case with Bank charges (which are debited from the customer account by bank).

- Errors: Mistakes or errors made in preparing the accounts either by the bank or the customer can also result in disagreement of the two statements. For e.g. omission of cheques issued. For this reason rectification of errors is required to be done in both the statements before preparing any Bank Reconciliation Statement.

Some of the Items that Frequently Cause a Difference:

Above each scenario is explained in detail below along with examples:

(i) Cheques issued but not presented for payment: The entry in the cash book is made immediately on issue of cheque but naturally entry will be made by the bank only when the cheque is presented for payment. Thus there will be a gap of some days between the entry in the cash book and in the pass book.

Example 1: The balance as per Cash Book and Pass Book are ₹10,000. Cheque of ₹ 2,000 is issued but not presented for payment. Then the balances as per cash book and pass book will be as follows:

On the issue of aforesaid cheque, the bank account in Cash Book is credited by ₹2,000 and so balance is reduced to ₹ 8,000. Whereas balance in the Pass Book remains ₹10,000 until the cheque is presented for payment.

(ii) Cheques deposited with the bank but not cleared: As soon as cheques are sent to the bank (i.e. deposited with bank), entries are made on the debit side of the bank column of the cash book. But usually banks credit the customer’s account only when they have received the payment from the bank concerned- in other words, when the cheques have been cleared. Again, there will be some time gap between the deposit of the cheques and the credit given by the bank.

Example 2: The balance as per Cash book and Pass Book are ₹ 12,000. Cheque of ₹ 3,000 is deposited but not cleared.

When cheque is deposited into bank, the bank account in Cash Book is increased to ₹ 15,000, but the balance in the Pass Book remains ₹ 12,000 until the cheque is cleared.

(iii) Interest allowed by bank: If the bank has allowed interest to the customer, the entry will normally be made in the customer’s account and later shown in the pass book. The customer usually comes to know the amount of the interest by pursuing the pass book and only then he makes relevant entry in the cash book.

Example 3: The balance as per Cash Book and Pass Book are ₹ 10,000. The bank has allowed ₹ 1,000 interest on saving account to customer.

Because of such interest, balance of Pass Book is increased to ₹11,000. Whereas balance in the Cash Book remains ₹10,000 until information reaches to the customer and he records such transaction.

(iv) Interest and expenses charged by the bank: Like (iii) above, the interest charged by the bank and the amount of the bank charges are entered in the customer account and later in the pass book. The customer makes the required entries only after he sees the pass book or bank statement. These are debited to customer account by bank therefore till such entry is passed in cash book, bank balance as per pass book is less than bank balance as per cash book.

(v) Interest and dividends collected by the bank: Sometimes investments are left with the bank in the safe custody; the bank itself sees to it that the interest or the dividend is collected on the due dates. Entries are made as indicated in (iii) above.

Example 4: The balance as per Cash Book and Pass Book are ₹15,000. The bank has collected dividend of ₹ 2,000.

On collection of dividend bank credits the amount to customer’s account, so balance in Pass Book is increased to ₹ 17,000. Whereas balance in the Cash Book remains ₹ 15,000 until the information of such dividend collection reaches to the customer and he records such transaction.

(vi) Direct payments by the bank: The bank may be given standing instructions for certain payments such as insurance premium, equated monthly installments of loan (EMIs). In these cases also, the customer comes to know of the payment only after viewing the pass book or bank statement. The entries in the pass book and in the cash book may thus be on different dates.

Example 5: The balance as per Cash Book and Pass Book of Mr. X are ₹ 20,000. The bank has instruction to pay insurance premium of ₹ 1,500 directly to insurance company at the end of each month.

On payment of insurance premium bank debits the customer’s account by ₹ 1,500 so balance in Pass Book is decreased to ₹ 18,500. Whereas balance in the Cash Book remains ₹ 20,000 until the information of such payment reaches to the customer and he records such transaction.

(vii) Direct payment into the bank by a customer: If such a payment is received by the bank, it will be entered in the customer’s account and also in the pass book; the account holder may come to know of the amount only when he sees the pass book. (e.g. Customers’ these days prefers using banking facilities like NEFT, RTGS to transfer funds online)

(viii) Dishonour of a bill discounted with the bank: If the bank is not able to receive payment on promissory notes discounted by it, it will debit the customer’s account together with the charges it may have incurred. The customer will naturally make the entry only when he sees the pass book.

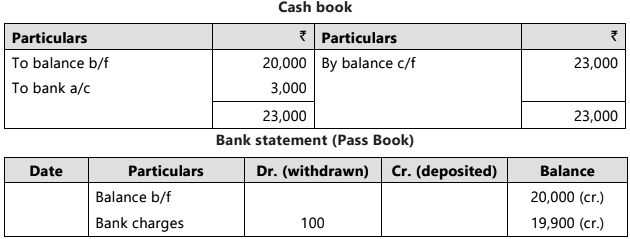

Example 6: The balances as per Cash Book and Pass Book of Mr. X are ₹ 20,000. Mr. X deposited a cheque of ₹ 3,000 and debited to his bank account ₹ 3,000 immediately. But bank will credit X’s account on realization of amount. Now the cheque is dishonoured for nonpayment. Bank charges ₹ 100 in this connection. Thus, balance of Mr. X’s account in Pass Book stands ₹ 19,900 after this transaction while balance as per Cash Book stand ₹ 23,000. So Mr. X should deduct ₹ 3,000 the amount of dishonoured cheque, plus ₹ 100 the amount of bank charges for reconciliation.

Thus, balance of Mr. X’s account in Pass Book stands ₹ 19,900 after this transaction while balance as per Cash Book stand ₹ 23,000. So Mr. X should deduct ₹ 3,000 the amount of dishonoured cheque, plus ₹ 100 the amount of bank charges for reconciliation.

(ix) Bills collected by the bank on behalf of the customer: If goods are sold, the documents may be sent through the bank. If the bank is able to collect the amount, it will credit the customer’s account. The customer may make the entry only on receiving the pass book. All these timing differences will lead to difference in balances as shown by the cash book and the pass book.

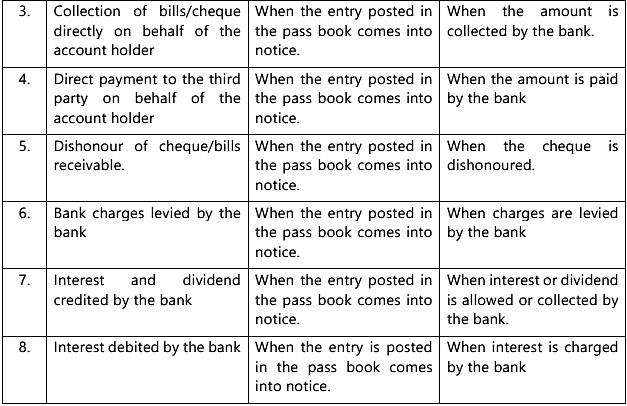

Following is the table summarising in brief the timings of different transactions:

To illustrate this, we give below an extract from a pass book and the bank column of the cash book in Illustration 1:

Illustration 1: Messer’s Tall & Short, Faiz Bazar, New Delhi-110002 in account with Punjab National Bank, Daryaganj, New Delhi-110002

It will be seen that whereas the pass book shows a credit balance of ₹ 2,43,000, the cash-book shows a debit balance of ₹ 2,37,000. We shall compare the two to establish the reasons for the difference. The reconciliation of the two statements can be done in two ways:-

It will be seen that whereas the pass book shows a credit balance of ₹ 2,43,000, the cash-book shows a debit balance of ₹ 2,37,000. We shall compare the two to establish the reasons for the difference. The reconciliation of the two statements can be done in two ways:-

- Arrive at pass book balance from cash book.

- Arrive at cash book balance from pass book.

Let us start with the pass book balance and arrive at the balance as per cash book.

Step: 1. Compare the debit side of cash book with the deposits column of pass book:-

We find that the following cheques are recorded in the cash book but not in the pass book. Therefore if we enter these two cheques in the deposit side of the pass book the balance becomes:- Step: 2. Compare the credit side of the cash book with the withdrawal column of the pass book We find that the following cheques are not recorded. Therefore, if we enter these two cheques on the withdrawal side of the pass book the balance becomes: -

Step: 2. Compare the credit side of the cash book with the withdrawal column of the pass book We find that the following cheques are not recorded. Therefore, if we enter these two cheques on the withdrawal side of the pass book the balance becomes: - There is an item ‘Interest on Government Securities’ which appears on the deposit side of the pass book but not in the debit side of the cash book, so this item should be deducted from pass book balance:-

There is an item ‘Interest on Government Securities’ which appears on the deposit side of the pass book but not in the debit side of the cash book, so this item should be deducted from pass book balance:-

Further, there are two items which appear on the withdrawal side of the pass book i.e. they have been deducted from the bank balance but not on the credit side of the cash book, so these items should be added in order to reconcile the balance:- Therefore, we have arrived at the balance as per the cash book from the pass book.

Therefore, we have arrived at the balance as per the cash book from the pass book.

This process shows that the difference between the two balance arise only because there are some entries made in the cash-book but not in the pass book and some entries which are made in the pass book but not in the cash book. A comparison of the two shows up such entries and then, on that basis, the reconciliation is prepared. To illustrate it again, let us proceed from the cash book balance of ₹ 2,37,000. Since cheques totalling ₹ 1,39,000 have not been entered in the pass book, let us assume that they are also omitted from the cash book, this will reduce the cash book balance to ₹ 98,000. Cheques totalling ₹ 1,51,000 have been entered on the credit side of the cash book but not in the pass book their omission from the cash book will increase the cash book balance to ₹ 2,49,000. Amounts totalling ₹ 26,000 have been entered in the withdrawals column of the pass book but not in the cash book; an entry on the credit side of the cash book for these amounts will reduce the balance to ₹ 2,23,000. The deposits column shows an entry of ₹ 20,000 not found on the debit side of the cash book; the entry made in the cash book will increase balance to ₹ 2,43,000 as shown in the pass book.

(x) Errors: While recording the entries errors can occur both in the cash book and in the pass book. A bank rarely makes an error but if it does, the balance in the pass book will naturally differ from cash book. Similarly if any error is committed in the cash book then it’s balance will be different from that of the pass book. Some of the errors include commission of entry, recording of an incorrect amount, recording of entry on the wrong side of the book, wrong totalling of the account or wrong balancing of the book and recording of transactions of other party.

Example 7: Mr. A’s cash book shows following transactions:

Here there are several errors made by accountant:

Here there are several errors made by accountant:

April 1: Balance should be have bought down in debit side as ₹ 1,00,000

April 13: Also a cheque issued to Vandy Ltd. has been omitted in the books of ₹ 90,000

So, on correcting these entries balance as per Cash Book will be:

|

68 videos|160 docs|83 tests

|

FAQs on ICAI Notes: Bank Reconciliation Statement - 1 - Principles and Practice of Accounting - CA Foundation

| 1. What is a Bank Reconciliation Statement? |  |

| 2. Why is a Bank Reconciliation Statement important? | |

| 3. What are the common reasons for differences between the bank balance and the company's records? | |

| 4. How can outstanding checks be reconciled in a Bank Reconciliation Statement? | |

| 5. What steps should be followed to prepare a Bank Reconciliation Statement? | |

|

4.76/5 Rating |

|

Dec 05, 2024 Last updated |

|

68 videos|160 docs|83 tests

|

|

Explore Courses for CA Foundation exam

|

|

Important questions

,ppt

,study material

,MCQs

,mock tests for examination

,Free

,Viva Questions

,Sample Paper

,Objective type Questions

,Previous Year Questions with Solutions

,ICAI Notes: Bank Reconciliation Statement - 1 | Principles and Practice of Accounting - CA Foundation

,Exam

,practice quizzes

,shortcuts and tricks

,ICAI Notes: Bank Reconciliation Statement - 1 | Principles and Practice of Accounting - CA Foundation

,video lectures

,Semester Notes

,past year papers

,Extra Questions

,ICAI Notes: Bank Reconciliation Statement - 1 | Principles and Practice of Accounting - CA Foundation

,Summary

;

ICAI Notes: Bank Reconciliation Statement - 1 Free PDF Download

Importance of ICAI Notes: Bank Reconciliation Statement - 1

ICAI Notes: Bank Reconciliation Statement - 1

ICAI Notes: Bank Reconciliation Statement - 1 CA Foundation Questions

Study ICAI Notes: Bank Reconciliation Statement - 1 on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|