ICAI Notes- Unit 3: Trial Balance | Accounting for CA Foundation PDF Download

Overview

Trial balance contains various ledger balances on a particular date. It forms the basis for preparing the financial statement i.e. profit and loss account and balance sheet. If it tallies, it means that the accounts are arithmetically accurate but certain errors may still remain undetected. Therefore, it is very important to carefully journalise and post the entries, following the rules of accounting.

Introduction

Preparation of trial balance is the third phase in the accounting process. After posting the accounts in the ledger, a statement is prepared to show separately the debit and credit balances. Such a statement is known as the trial balance. It may also be prepared by listing each and every account and entering in separate columns the totals of the debit and credit sides. Whichever way it is prepared, the totals of the two columns should agree. An agreement indicates arithmetic accuracy of the accounting work; if the two sides do not agree, then there is simply an arithmetic error(s).

This follows from the fact that under the Double Entry System, the amount written on the debit sides of various accounts is always equal to the amounts entered on the credit sides of other accounts and vice versa. Hence the totals of the debit sides must be equal to the totals of the credit sides. Also total of the debit balances will be equal to the total of the credit balances. Once this agreement is established, there is reasonable confidence that the accounting work is free from clerical errors, though it is not a proof of cent per cent accuracy, because some errors of principle and compensating errors may still remain. Generally, to check the arithmetic accuracy of accounts, trial balance is prepared at monthly intervals. But because double entry system is followed, one can prepare a trial balance any time. Though a trial balance can be prepared any time but it is preferable to prepare it at the end of the reporting period which may be month end/quarter end/year end to ensure the arithmetic accuracy of all the accounts before the preparation of the financial statements. It may be noted that trial balance is a statement and not an account.

Objectives of Preparing the Trial Balance

The preparation of trial balance has the following objectives:

(i) Trial balance enables one to establish whether the posting and other accounting processes have been carried out without committing arithmetical errors. In other words, the trial balance helps to establish arithmetical accuracy of the books of accounts.

(ii) Financial statements are normally prepared on the basis of agreed trial balance; otherwise the financial statements will not give true and fair picture of the financial transactions.

(iii) The trial balance serves as a summary of what is contained in the ledger; the ledger may have to be seen only when details are required in respect of an account.

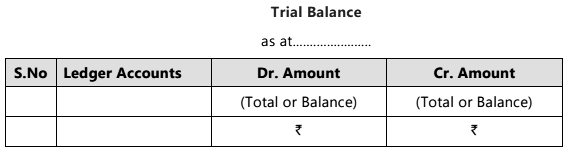

The form of the trial balance is simple as shown below:

The under mentioned points may be noted:

(i) A trial balance is prepared as on a particular date which should be mentioned at the top.

(ii) In the second column the name of the account is written.

(iii) In the third column the total of the debit side of the account concerned or the debit balance, if any is entered.

(iv) In the fourth column, the total of the credit side or the credit balance is written.

(v) The third and fourth columns are totalled at the end.

Limitations of Trial Balance

One should note that the agreement of Trial Balance is not a conclusive proof of accuracy. In other words, in spite of the agreement of the trial balance some errors may remain. These may be of the following types:

(i) Transaction has not been entered at all in the journal.

(ii) A wrong amount has been written in both columns of the journal.

(iii) A wrong account has been mentioned in the journal.

(iv) An entry has not at all been posted in the ledger.

(v) Entry is posted twice in the ledger.

Still, the preparation of the trial balance is very useful; without it, the preparation of financial statements, would be difficult.

Methods of Preparation of Trial Balance

Total Method

Under this method, every ledger account is totalled and that total amount (both of debit side and credit side) is transferred to trial balance. In this method, trial balance can be prepared as soon as ledger account is totalled. Time taken to balance the ledger accounts is saved under this method as balance can be found out in the trial balance itself. The difference of totals of each ledger account is the balance of that particular account. This method is not commonly used as for the preparation of the financial statements, only net balance of the ledger account is required. Therefore, the trial balance compiled under this method cannot be used directly for preparation of the financial statements.

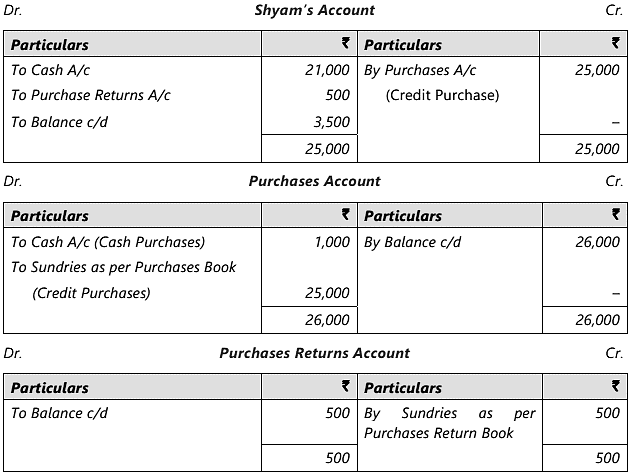

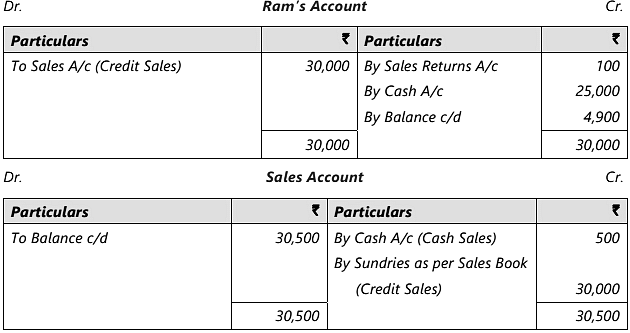

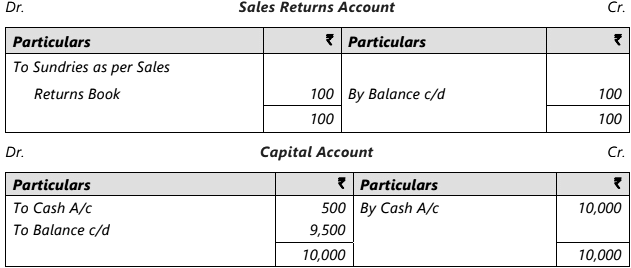

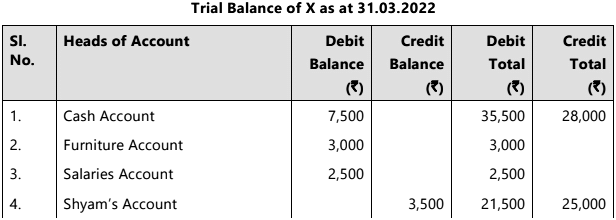

Illustration 1 : Given below is a ledger extract relating to the business of X and Co. as on March, 31, 2022. You are required to prepare the Trial Balance by the Total Amount Method.

Sol:

Sol:

Balance Method

Under this method, every ledger account is balanced and those balances only are carried forward to the trial balance. This method is used commonly by the accountants and helps in the preparation of the financial statements. Financial statements are prepared on the basis of the balances of the ledger accounts.

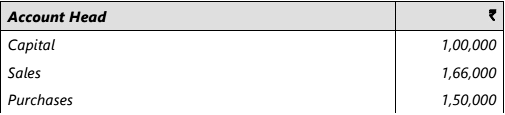

Illustration 2: Taking the same information as given in Illustration 1, prepare the Trial Balance by Balance Method.

Sol:

Total and Balance Method

Under this method, the above two explained methods are combined. This has been explained with the help of the following example:

Adjusted Trial Balance (Through Suspense Account)

If the trial balance does not agree after transferring the balance of all ledger accounts including cash and bank balance and also errors are not located timely, then the trial balance is tallied by transferring the difference of debit and credit side to an account known as suspense account. This is a temporary account opened to proceed further and to prepare the financial statements timely.

Rules of Preparing The Trial Balance

While preparing the trial balance from the given list of ledger balances, following rules should be taken into account:

- The balances of all (i) assets accounts (ii) expenses accounts (iii) losses (iv) drawings are placed in the debit column of the trial balance.

- The balances of all (i) liabilities accounts (ii) income accounts (iii) gains (iv) capital are placed in the credit column of the trial balance.

Illustration 3: From the following ledger balances, prepare a trial balance of Anuradha Traders as on 31st March, 2022:

Sol:

Sol:

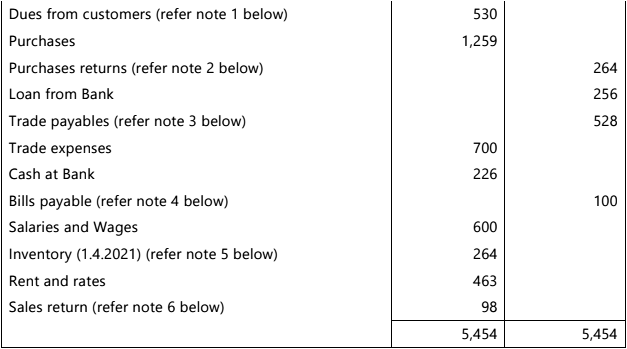

Illustration 4: One of your clients, Mr. Singhania has asked you to finalise his accounts for the year ended 31st March, 2022. Till date, he himself has recorded the transactions in books of accounts. As a basis for audit, Mr. Singhania furnished you with the following statement.

The closing inventory on 31st March, 2022 was valued at ` 574. Mr. Singhania claims that he has recorded every transaction correctly as the trial balance is tallied. Check the accuracy of the above trial balance.

Sol:

Notes:

- Dues from customers is an asset, so its balance will be a debit balance.

- Purchases return account always shows a credit balance because assets go out.

- Balance in Trade payables is a liability, so its balance will be a credit balance.

- Bills payable is a liability, so its balance will be a credit balance.

- Inventory (opening) represents assets, so it will have a debit balance.

- Sales return account always shows a debit balance because assets come.

Illustration 5: The following trail balance as on 31st March, 2022 was drawn from the books of fintech traders:

Even though the debit and credit sides agree, the trial Balance contains certain errors. Check the accuracy of trial balance.

Even though the debit and credit sides agree, the trial Balance contains certain errors. Check the accuracy of trial balance.

Sol:

Summary

- Trial balance contains various ledger balances on a particular date.

- It forms the basis for preparing financial statement i.e. profit and loss account and balance sheet.

- If it tallies, it means that the accounts are arithmetically accurate but certain errors may still remain undetected.

- It is very important to carefully journalize and post the entries, following the rules of accounting.

|

68 videos|160 docs|83 tests

|

FAQs on ICAI Notes- Unit 3: Trial Balance - Accounting for CA Foundation

| 1. What is the purpose of preparing a trial balance? |  |

| 2. What are the limitations of a trial balance? | |

| 3. What are the methods of preparing a trial balance? | |

| 4. What is an adjusted trial balance? How is it prepared? | |

| 5. What are the rules for preparing a trial balance? | |

|

4.78/5 Rating |

|

Dec 05, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

Extra Questions

,Exam

,practice quizzes

,ICAI Notes- Unit 3: Trial Balance | Accounting for CA Foundation

,Semester Notes

,Summary

,past year papers

,Important questions

,Previous Year Questions with Solutions

,Sample Paper

,mock tests for examination

,shortcuts and tricks

,ppt

,MCQs

,ICAI Notes- Unit 3: Trial Balance | Accounting for CA Foundation

,video lectures

,Free

,ICAI Notes- Unit 3: Trial Balance | Accounting for CA Foundation

,Viva Questions

,study material

,Objective type Questions

;

ICAI Notes- Unit 3: Trial Balance Free PDF Download

Importance of ICAI Notes- Unit 3: Trial Balance

ICAI Notes- Unit 3: Trial Balance

ICAI Notes- Unit 3: Trial Balance CA Foundation Questions

Study ICAI Notes- Unit 3: Trial Balance on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|