Introduction - Basic Accounting Terms - Commerce PDF Download

Basic Accounting Terms

1. Business transactions:

- It is an economic activity that changes the financial position of the business.

- Every business transactions results in change in the value of some of the assets, liabilities or capital.

Features of business transactions:

- Economic activity

- Transactions are of two types internal and external

- Changes the financial position of the business.

- Must be capable of expressed in terms of money.

2. Event:

Result of the transactions is called as an event. Ex: we purchased goods of Rs.50,000 and sold it for Rs.60,000 then Rs. 10,000 is the profit which is the result of the business.

3. Account: (T shape)

It is record of all the business transactions relating to a particular person, assets, liability, expenses or incomes.

- The place were all transactions are recorded is called as account.

- All accounts have two sides i.e. is debit and credit. (T shape)

4. Debit: (dr.)

The left hand side of an account is called as debit. The word debit is derived from an italian word Debito.

5. Credit : (cr.)

The right hand side of an account is called as credit. The word credit is derived from an italian word credito.

6. Entry:

An event or a transaction when is recorded in the books of the account is called as entry.

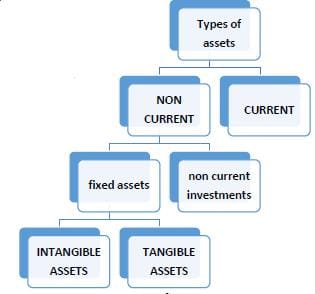

7. Assets :

- The things or resources which are valuable or property of the business is called as an asset.

- It also includes the amount due from others.

Features of assets:

1. Valuable

2. Owned by the business

3. Acquired at a measurable money cost

Types of assets

Non-current assets – examples: land, buildings, plant and machinery and long-term investments

- Held by business for a long period of time

- Not meant for resale

a. Fixed assets:

- Assets which are required for purpose of reuse in the business but not for purpose of resale.

- It increases the earning the capacity of the business

- Benefit is for a long period of time.

- Fixed at their place

i) Tangible Assets: assets which can be physically seen and touched. (Land, Building, Plant and Equipment, Furniture & Fixture, Vehicles, Office Equipments, Others).

ii) Intangible Assets: Assets which are not tangible i.e. which can’t be seen and touch

(a) Goodwill (b) Brand / Trademarks/ copyright .

b Non-Current Investments:

Non-current Investments are investments that are held not with the purpose to resell but to retain them.

Non- current Investments are further classified into ‘ Trade Investments’ and ‘ Other Investments’.

Current Assets/short-lived assets / active assets - examples: cash, stock, debtors, prepaid expenses.

- Assets that are meant for resale.

- Converted into cash within one year.

- Benefit is derived for a period of one year.

Nominal assets/ fictitious assets examples: P & L (dr. balance), advertising expenses (deferred revenue expenditure)

- Assets that cannot be realized in cash or no further benefit can be derived from them.

- Actually, they are the losses which were not written off in the year in which they incurred.

8. Capital/ owners equity/ net worth/net assets

It refers to the amount of money which is invested by the owner/ proprietor in the business.

Capital = assets – liabilities

9. Drawings :

Any cash or the goods withdrawn by the owner for his personal use is called as drawings.

Ex: personal expenses, household expenses, life insurance premium and income tax.

10. Liabilities/ debt Examples – loans , creditors

- It refers to the money which a firm owes (payable) to the outsiders.

- Obligation of the firm towards the outsiders.

- Liability to the owners is an internal liability and towards outsiders (others) are external liabilities.

- Current liabilties are those liabilties which are to be paid in the near future ( normaly within 1 year)

Ex- creditors , short term loan, outstanding expenses

- Non Current liabilties are those liabilties which fall due for payment in a realtively long period ( normaly more

then 1 year)

Ex- long term loans, debentures

11. Receipts:

It is the amount received or receivable by selling goods, services or assets. Two types of receipts are:

a. Revenue receipt:

- Amount received or receivable in the normal course of the basis (day to day business activities).

- Shown in trading and profit and loss account.

- Ex: money obtained from sale of goods, commission received, interest and dividend received.

b. Capital receipt :

- Amount received or receivable from the transactions which are not revenue in nature.

- Shown in balance sheet as increase in liabilities or reduction in assets.

- Ex: amount received by way of loans, selling fixed assets.

12. Expenditure:

- Disbursement of cash or transfer of property or incurring a liability for the purpose of acquiring goods and services

- Amounts spend or liability incurred for the purpose of acquiring goods and services.

- Any type of a payment for a receipt of a benefit is called as expenditure.

Types of expenditure

a. Capital expenditure:

- Any expenditure which is incurred in acquiring (purchasing) assets or increasing the value of fixed assets

- Benefit is received for a long period of time.

- Ex: purchase of fixed assets (machinery)

- It increases the earning capacity of the business.

- Shown in balance sheet assets side.

b. Revenue expenditure :

- Any expenditure whose benefit is derived within the accounting period is called as revenue expenditure.

- Helps in maintaining the earning capacity of the business.

- Shown in Trading and P & L debit side.

- Ex: repair of the machinery, cost of goods sold, rent etc.

c. Deferred revenue expenditure:

- It’s a type of a revenue expenditure whose benefit is derived for more than one accounting year.

- It lasts for 3 to 7 years.

- Ex: a firm spends huge amount on advertising of their newly launched product Rs.2,00,000 and the benefit is to be derived for a period of 4 years. So every year is Rs.50,000 is debited to the P & L account and remaining part is shown in balance sheet assets side 1st yr Rs.1,50,000,2nd yr Rs.1,00,000 and so on.

- As such whole expenditure is not shown in the P & l account only a part (written off portion) is shown and remaining in shown in balance sheet.

13. Expenses

- Cost incurred for generating revenue (producing and selling goods and services).

- Value that had expired during the accounting year.

- Ex: cost of goods sold, rent paid, salary paid etc.

(i) Prepaid expenses/ unexpired amounts: expenses which are paid in advance and there benefit will be derived in accounting year or accounting years is called as prepaid expenses it is treated as an assets.

It’s a Current asset. Ex: prepaid insurance

(ii) Outstanding expenses/ accrued expenses: expenses which are due but not paid by the firm are outstanding expenses i.e. the expenses whose benefit had been received but the amount is yet not paid by the firm.

It’s a current liability. Ex: outstanding wages.

14. Income: income= revenue - expenses

- Surplus of revenue over expenses is called as incomes.

- The money received from the sale of the goods is revenue and cost of goods sold is expense.

- Ex: goods costing Rs.50,000 are sold for Rs.70,000 so Rs. 70,000 is the revenue, Rs.50,000 is the cost and the difference between them is Rs.20,000 is income

15. Profits:

excess of total revenue over total expenses is profit. It’s of two types gross profit and net profit. It increases the total investment of the owner.

16. Gains: it’s a monetary benefit or advantage which is incidental to the business. (irregular)

- EX: winning a court case, sale of fixed assets at a profit(buildings costing Rs.50,000 are sold for Rs.70,000the difference between them is Rs.20,000 is a gain)

17. Loss:

it conveys two meanings :

1. The result of the business (revenues during the year was Rs.10,000 and expenses were Rs.25,000. Rs.5,000 is the loss )

2. Some fact or an activity which the firms receives without any benefit ( loss by fire theft, fire etc.)

- Losses cause a reduction in the capital and they are different from expenses as expenses are incurred revenue but losses are not.

18. Goods/merchandize :

- It includes all those things which are purchased for the purpose of resale or which are used for producing final goods which will be resold.

- A cloth dealer will purchase cloth, a furniture dealer will purchase chairs and tables for resale(for others it’s an assets), a stationery shop will purchase pen, pencil, copies (for others these are expenses)

19. Purchases:

It refers to the purchase of goods in which the business deals .

- For a manufacturing concern raw materials are the goods which will be converted into finished goods.

- For a trading concern it includes all those things which are purchased for the purpose of resale.

- Ex: A cloth dealer will purchases cloth for sale, which is called as goods but if the same cloth dealer purchases furniture for the seating of the customers it is called fixed assets (not meant for resale)

20. Purchase return / return outwards:

When the purchased goods are returned back to the supplier it is called as purchase return.

21. Sales:

- Sale means transfer of ownership of goods or services for a price. It includes only those goods which were meant for resale.

- The term sale is never use of sale of fixed assets its only used for goods.

- EX: A cloth dealer will sell cloth which is called as sales but if the same cloth dealer sells his furniture it is not called as sales.

22. Sales returns / return inwards:

When the sold goods are returned back by the customer is called as sales return.

23. Stock / inventory :

Stock is the value of those goods which are lying unsold at the end of the accounting year which were purchased for reseeling.

Two types are:

Opening stock: Goods lying unsold at the beginning of the accounting year is called as opening sock.

Closing stock: Goods lying unsold at the end of the accounting year is called as closing stock.

24. Inventory

In case of a manufacturer opening and closing inventory can be of four types –

a. Inventory of raw material.

b. Inventory of work in progress.

c. Inventory of finished goods.

d. Inventory of stock in trade

Distinction of stock and inventory

Stock is the value of those goods which are lying unsold at the end of the accounting year which were purchased for reseeling. Whereas the inventory is wider term it includes stock also.

25. Debtors/ book debts:

the customers to whom goods are sold on credit are called as debtors (current assets).

26. Creditors:

the suppliers who had supplied goods on credit to the business is called as creditors.

27. Bills receivables :

a bills of exchange becomes a b/r when the persons who draws it(creditor/drawer) on a debtor(drawee ) accepts it to pay a specified amount to the specified person at the end of a specified period.

28. Trade receivables:

debtors + bills receivables = trade receivables

29. Bills payables:

it refers to the bills of exchange accepted in favor of a creditor.

30. Trade payables :

Creditors+ bills payables = Trade payables

31. Cost: Amount of the resources which are given up in exchange of some goods and services.

Two types are cost are:

a. Actual cost: This involves a cash outlay, ex: raw material purchased, rent of a factory.

b. Notional cost: Which does not involves a cash outlay. Cost of using the owners resources. EX(rent of owned factory)

31. Discount:

Rebate or an allowance given by the seller to the buyer. Two types of discount are:

a. Trade discount: when a discount is given by the seller to the buyer on the list price is called as trade discount.

Not shown in the books of accounts

* Purpose is to increase the sales.

b. Cash discount: when a discount is given to the customer for making a prompt payment it is called as cash discount. Recorded in the books of account * purpose is to collect prompt payment.

32. Vouchers:

It is a document which provides authorization to pay and on the basis of which transaction are recorded in the books of original entry.

- a separate voucher is prepared for every transaction.

- It specifies the accounts to be debited or credited.

33. Bad debts:

the amount which is not recovered from the debtors is called as bad debts. It is a loss for the business.

34. Revenue:

it means any income from any recurring source. It includes the money received from sale of goods, rent receipt

35. Solvent:

a person who is able to pay off his debts(liabilities) is called as solvent person.

36. Insolvent:

a person who is not able to pay off his debts(liabilities) is called as solvent person.

37. GST ( goods and service tax):

All indirect taxes like custom duty , excise duty, sales tax, VAT , service tax etc . have merged into a single tax known as GST.

GST is paid at the time of purchases and colleceted at the time of sales.

38. Stores:

The material held by an entreprise for the purpose of consumption in the business and not ofr resale.

Ex- lubricants, spare parts of machinery , packing materials etc.

39. Revenue from operations:

It is the revenue earned by any enterprise from its operating activities . ex- revenue from sale and goods and services

40. Entity:

It is an economic unit which is formed for earning income by providing goods and services.

Ex- JIO, honda etc

41. Turnover:

Turnover means sales made in a particular period

42. livestock:

Domestic animals, such as horses or catlles are known as live stock

43. Investements:

Deployment of funds in shares and debentures of companies for the purpose earning a return.

You can go through Crash Course of Accountancy Class 11 here.

Cover Basic Accounting terms through this doc.

FAQs on Introduction - Basic Accounting Terms - Commerce

| 1. What are basic accounting terms? |  |

| 2. What is the difference between revenue and profit? | |

| 3. What is the purpose of balance sheets in accounting? | |

| 4. What is the accounting equation? | |

| 5. What is the difference between accounts payable and accounts receivable? | |

Free

,Important questions

,Objective type Questions

,Sample Paper

,study material

,mock tests for examination

,past year papers

,ppt

,Semester Notes

,Previous Year Questions with Solutions

,Introduction - Basic Accounting Terms - Commerce

,Extra Questions

,Viva Questions

,Introduction - Basic Accounting Terms - Commerce

,Exam

,practice quizzes

,video lectures

,shortcuts and tricks

,Introduction - Basic Accounting Terms - Commerce

,MCQs

,Summary

;

Introduction - Basic Accounting Terms Free PDF Download

Importance of Introduction - Basic Accounting Terms

Introduction - Basic Accounting Terms Notes

Introduction - Basic Accounting Terms Commerce Questions

Study Introduction - Basic Accounting Terms on the App

|

© EduRev

|

Education Revolution

|

|