Introduction - Issue of Shares | Crash Course of Accountancy - Class 12 - Commerce PDF Download

Definition of a Company:

"A Company is an artificial person created by law, having separate entity with a perpetual succession and a common seal".

Characteristics of a Company:

(1) Separate Legal Entity.

(2) Perpetual Existence.

(3) Limited Liability.

(4) Common Seal.

(5) Transferability of Shares.

(6) Separation of Management from Ownership.

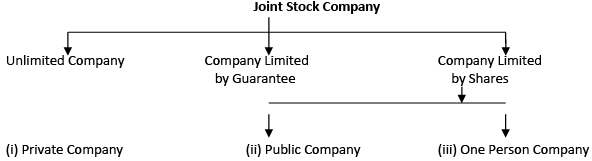

Kinds of a Company:

Companies registered under the Companies Act, 2013, may be classified as below:

Unlimited Company:

• Unlimited Company is a company where there is no limit on the liability of its members.

• It means, when a company suffers loss and the company's property is not sufficient to payoff its debts, the private property of its members will be used to meet the claims of creditors.

Company Limited by Guarantee:

• In case of such a company, the liability of the members is limited to the extent of the guarantee given by them in the event of the winding up of the company.

• The liability of its member will arise only in the event of winding up of the company.

Company Limited by Shares:

• In case of such a company the liability of the members is strictly limited to the extent of the nominal value of shares held by each of them.

• If a member has already paid the full amount of the shares, he will not be liable to pay any amount.

• Such companies may be sub-divided into private, public and one person companies:

Private Company:

• As per Section 2 (68) of Companies Act, 2013, a private company is one which has a minimum paid-up share capital of Rs 1,00,000 or such higher paid-up capital as may be prescribed by Companies Act, and by its Articles of Association.

• The name of every private company must end with the words private limited.

Public Company:

• As per Section 2 (71) of Companies Act, 2013, a public company means a company which is not a private company and has a minimum paid-up share capital of Rs.5,00,000 or such higher paid-up share capital as may be prescribed by the Companies Act.

| s.no. | Basis | Private co. | Public co. |

| 1 | Number of members | Minimum number of members is 2, and the maximum, exclusive of past and present employees is 200. | Minimum number of members is 7 and there is no limit to, maximum number. |

| 2 | Paid-up Capital | It should have minimum paid-up capital as prescribed by the Companies Act, which is Rs. 1,00,000 at present. | It should also have minimum paid-up capital as prescribed by the Companies Act, which is Rs.5,00,000 at present. |

| 3 | Invitation to the public | It cannot invite the public to subscribe to its shares. | It can invite the public to subscribe to its shares. |

| 4 | Transfer of Shares | There is restriction on the transfer of its shares. | There is no restriction on transfer of its shares. |

One Person Company OR OPC:

Meaning: Companies Act 2013 introduces a new type of entity to the existing list i.e., apart from forming a public or private limited company, the Act enables the formation of a new entity ‘One Person Company’ (OPC). An OPC means a private limited company with only one person as its member [Section 2 (62)].

Member of OPC:

Only natural person who is citizen of India can be a member of OPC.

Minimum Paid-up Capital:

Its minimum paid-up Capital should be Rs.1,00,000.

Purpose:

It can be formed for business as well as charitable purpose.

Number of Directors:

An OPC can have minimum one and maximum fifteen directors.

Conversion:

An OPC cannot convert itself into public or private company unless a period of 2 years has expired from the date of its incorporation and conversion is mandatory when the paid-up share capital is increased beyond Rs.50 Lakh or its average annual turnover during the relevant period exceeds Rs.2 Crore.

Benefits:

(i) OPC is not required to include Cash Flow Statement in its financial statements.

(ii) The provisions relating to calling of AGM, Notice for General Meeting, Quorum for meetings, Proxies etc. shall not apply to OPC.

|

79 docs|43 tests

|

FAQs on Introduction - Issue of Shares - Crash Course of Accountancy - Class 12 - Commerce

| 1. What is the process of issuing shares in commerce? |  |

| 2. What are the benefits of issuing shares in commerce? | |

| 3. What are the different types of shares that can be issued in commerce? | |

| 4. How does issuing shares affect the ownership and control of a company in commerce? | |

| 5. What are the regulatory requirements for issuing shares in commerce? | |

Exam

,Summary

,Viva Questions

,MCQs

,past year papers

,shortcuts and tricks

,video lectures

,Semester Notes

,Previous Year Questions with Solutions

,Introduction - Issue of Shares | Crash Course of Accountancy - Class 12 - Commerce

,practice quizzes

,Extra Questions

,Important questions

,Objective type Questions

,ppt

,Sample Paper

,Free

,study material

,Introduction - Issue of Shares | Crash Course of Accountancy - Class 12 - Commerce

,Introduction - Issue of Shares | Crash Course of Accountancy - Class 12 - Commerce

,mock tests for examination

;

Introduction - Issue of Shares Free PDF Download

Importance of Introduction - Issue of Shares

Introduction - Issue of Shares Notes

Introduction - Issue of Shares Commerce Questions

Study Introduction - Issue of Shares on the App

|

© EduRev

|

Education Revolution

|

|