Introduction to Budgetary Control - Budgetary Control, Cost Management | Crash Course for UGC NET Commerce PDF Download

Meaning:

Budgetary control is the process of determining various actual results with budgeted figures for the enterprise for the future period and standards set then comparing the budgeted figures with the actual performance for calculating variances, if any. First of all, budgets are prepared and then actual results are recorded.

The comparison of budgeted and actual figures will enable the management to find out discrepancies and take remedial measures at a proper time. The budgetary control is a continuous process which helps in planning and co-ordination. It provides a method of control too. A budget is a means and budgetary control is the end-result.

Definitions:

“According to Brown and Howard, “Budgetary control is a system of controlling costs which includes the preparation of budgets, coordinating the departments and establishing responsibilities, comparing actual performance with the budgeted and acting upon results to achieve maximum profitability.” Weldon characterizes budgetary control as planning in advance of the various functions of a business so that the business as a whole is controlled.

J. Batty defines it as, “A system which uses budgets as a means of planning and controlling all aspects of producing and/or selling commodities and services. Welsch relates budgetary control with day-to-day control process.” According to him, “Budgetary control involves the use of budget and budgetary reports, throughout the period to co-ordinate, evaluate and control day-to-day operations in accordance with the goals specified by the budget.”

From the above given definitions it is clear that budgetary control involves the follows:

(a) The objects are set by preparing budgets.

(b) The business is divided into various responsibility centres for preparing various budgets.

(c) The actual figures are recorded.

(d) The budgeted and actual figures are compared for studying the performance of different cost centres.

(e) If actual performance is less than the budgeted norms, a remedial action is taken immediately.

Objectives of Budgetary Control:

Budgetary control is essential for policy planning and control. It also acts an instrument of co-ordination.

The main objectives of budgetary control are the follows:

1. To ensure planning for future by setting up various budgets, the requirements and expected performance of the enterprise are anticipated.

3. To operate various cost centres and departments with efficiency and economy.

4. Elimination of wastes and increase in profitability.

5. To anticipate capital expenditure for future.

6. To centralise the control system.

7. Correction of deviations from the established standards.

8. Fixation of responsibility of various individuals in the organization.

Essentials of Budgetary Control:

There are certain steps which are necessary for the successful implementation budgetary control system.

These are as follows:

1. Organisation for Budgetary Control

2. Budget Centres

3. Budget Mammal

4. Budget Officer

5. Budget Committee

6. Budget Period

7. Determination of Key Factor.

1. Organization for Budgetary Control:

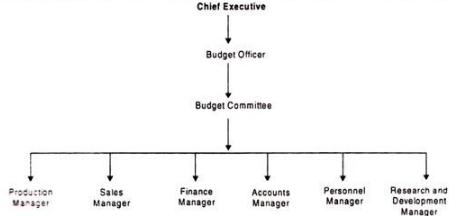

The proper organization is essential for the successful preparation, maintenance and administration of budgets. A Budgetary Committee is formed, which comprises the departmental heads of various departments. All the functional heads are entrusted with the responsibility of ensuring proper implementation of their respective departmental budgets.

The Chief Executive is the overall in-charge of budgetary system. He constitutes a budget committee for preparing realistic budgets A budget officer is the convener of the budget committee who co-ordinates the budgets of different departments. The managers of different departments are made responsible for their departmental budgets.

2. Budget Centres:

A budget centre is that part of the organization for which the budget is prepared. A budget centre may be a department, section of a department or any other part of the department. The establishment of budget centres is essential for covering all parts of the organization. The budget centres are also necessary for cost control purposes. The appraisal performance of different parts of the organization becomes easy when different centres are established.

3. Budget Manual:

A budget manual is a document which spells out the duties and also the responsibilities of various executives concerned with the budgets. It specifies the relations amongst various functionaries.

4. Budget Officer:

The Chief Executive, who is at the top of the organization, appoints some person as Budget Officer. The budget officer is empowered to scrutinize the budgets prepared by different functional heads and to make changes in them, if the situations so demand. The actual performance of different departments is communicated to the Budget Officer. He determines the deviations in the budgets and the actual performance and takes necessary steps to rectify the deficiencies, if any.

He works as a coordinator among different departments and monitors the relevant information. He also informs the top management about the performance of different departments. The budget officer will be able to carry out his work fully well only if he is conversant with the working of all the departments.

5. Budget Committee:

In small-scale concerns the accountant is made responsible for preparation and implementation of budgets. In large-scale concerns a committee known as Budget Committee is formed. The heads of all the important departments are made members of this committee. The Committee is responsible for preparation and execution of budgets. The members of this committee put up the case of their respective departments and help the committee to take collective decisions if necessary. The Budget Officer acts as convener of this committee.

6. Budget Period:

A budget period is the length of time for which a budget is prepared and employed. The budget period depends upon a number of factors. It may be different for different industries or even it may be different in the same industry or business.

The budget period depends upon the following considerations:

(a) The type of budget i.e., sales budget, production budget, raw materials purchase budget, capital expenditure budget. A capital expenditure budget may be for a longer period i.e. 3 to 5 years purchase, sale budgets may be for one year.

(b) The nature of demand for the products.

(c) The timings for the availability of the finances.

(d) The economic situation of the country.

(e) The length of trade cycles.

All the above-mentioned factors are taken into account while fixing period of budgets

7. Determination of Key Factor:

The budgets are prepared for all functional areas. These budgets are interdependent and inter-related. A proper co-ordination among different budgets is necessary for making the budgetary control a success. The constraints on some budgets may have an effect on other budgets too. A factor which influences all other budgets is known as Key Factor or Principal Factor.

There may be a limitation on the quantity of goods a concern may sell. In this case, sales will be a key factor and all other budgets will be prepared by keeping in view the amount of goods the concern will be able to sell. The raw material supply may be limited, so production, sales and cash budgets will be decided according to raw materials budget. Similarly, plant capacity may be a key factor if the supply of other factors is easily available.

The key factor may not necessarily remain the same. The raw materials supply may be limited at one time but it may be easily available at another time. The sales may be increased by adding more sales staff, etc. Similarly, other factors may also improve at different times. The key factor also highlights the limitations of the enterprise. This will enable the management to improve the working of those departments where scope for improvement exists.

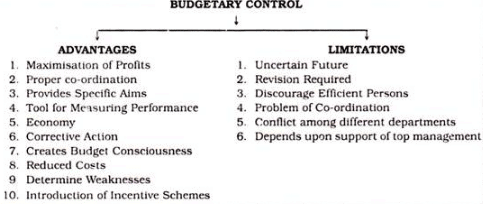

Advantages of Budgetary Control:

The budgetary control system help in fixing the goals for the organization as whole and concerted efforts are made for its achievements. It enables ‘economies in the enterprise.

Some of the advantages of budgetary control are:

1. Maximization of Profits:

The budgetary control aims at the maximization of profits of the enterprise. To achieve this aim, a proper planning and co ordination of different functions is undertaken. There is a proper control over various capital and revenue expenditures. The resources are put to the best possible use.

2. Co-ordination:

The working of different departments and sectors is properly coordinated. The budgets of different departments have a bearing on one another. The co-ordination of various executives and subordinates is necessary for achieving budgeted targets.

3. Specific Aims:

The plans, policies and goals are decided by the top management. All efforts are put together to reach the common goal, of the organization. Every department is given a target to be achieved. The efforts are directed towards achieving some specific aims. If there is no definite aim then the efforts will be wasted in pursuing different aims.

4. Tool for Measuring Performance:

By providing targets to various departments, budgetary control provides a tool for measuring managerial performance. The budgeted targets are compared to actual results and deviations are determined. The performance of each department is reported to the top management. This system enables the introduction of management by exception.

5. Economy:

The planning of expenditure will be systematic and there will be economy in spending. The finances will be put to optimum use. The benefits derived for the concern will ultimately extend to industry and then to national economy. The national resources will be used economically and wastage will be eliminated.

6. Determining Weaknesses:

The deviations in budgeted and actual performance will enable the determination of weak spots. Efforts are concentrated on those aspects where performance is less than the stipulated.

7. Corrective Action:

The management will be able to take corrective measures whenever there is a discrepancy in performance. The deviations will be regularly reported so that necessary action is taken at the earliest. In the absence of a budgetary control system the deviations can be determined only at the end of the financial period.

8. Consciousness:

It creates budget consciousness among the employees. By fixing targets for the employees, they are made conscious of their responsibility. Everybody knows what he is expected to do and he continues with his work uninterrupted.

9. Reduces Costs:

In the present day competitive world budgetary control has a significant role to play. Every businessman tries to reduce the cost of production for increasing sales. He tries to have those combinations of products where profitability is more.

10. Introduction of Incentive Schemes:

Budgetary control system also enables the introduction of incentive schemes of remuneration. The comparison of budgeted and actual performance will enable the use of such schemes.

Limitations of Budgetary Control:

Despite of many good points of budgetary control there are some limitations of this system.

Some of the limitations are discussed as follows:

1. Uncertain Future:

The budgets are prepared for the future period. Despite best estimates made for the future, the predictions may not always come true. The future is always uncertain and the situation which is presumed to prevail in future may change. The change in future conditions upsets the budgets which have to be prepared on the basis of certain assumptions. The future uncertainties reduce the utility of budgetary control system.

2. Budgetary Revision Required:

Budgets arc prepared on the assumptions that certain conditions will prevail. Because of future uncertainties, assumed conditions may not prevail necessitating the revision of budgetary targets. The frequent revision of targets will reduce the value of budgets and revisions involve huge expenditures too.

3. Discourage Efficient Persons:

Under budgetary control system the targets are given to every person in the organization. The common tendency of people is to achieve the targets only. There may be some efficient persons who can exceed the targets but they will also feel contented by reaching the targets. So budgets may serve as constraints on managerial initiatives.

4. Problem of Co-ordination:

The success of budgetary control depends upon the co-ordination among different departments. The performance of one department affects the results of other departments. To overcome the problem of coordination a Budgetary Officer is needed. Every concern cannot afford to appoint a Budgetary Officer. The lack of co-ordination among different departments results in poor performance.

5. Conflict Among Different Departments:

Budgetary control may lead to conflicts among functional departments. Every departmental head worries for his department goals without thinking of business goal. Every department tries to get maximum allocation of funds and this raises a conflict among different departments.

6. Depends Upon Support of Top Management:

Budgetary control system depends upon the support of top management. The management should be enthusiastic for the success of this system and should give full support for it. If at any time there is a lack of support from top management then this system will collapse.

|

237 videos|236 docs|166 tests

|

FAQs on Introduction to Budgetary Control - Budgetary Control, Cost Management - Crash Course for UGC NET Commerce

| 1. What is budgetary control? |  |

| 2. How does budgetary control help in cost management? | |

| 3. What are the benefits of implementing budgetary control? | |

| 4. What are the key components of budgetary control? | |

| 5. How can organizations ensure the success of budgetary control? | |

past year papers

,Cost Management | Crash Course for UGC NET Commerce

,Cost Management | Crash Course for UGC NET Commerce

,practice quizzes

,video lectures

,Viva Questions

,mock tests for examination

,MCQs

,shortcuts and tricks

,Cost Management | Crash Course for UGC NET Commerce

,Introduction to Budgetary Control - Budgetary Control

,Introduction to Budgetary Control - Budgetary Control

,study material

,Summary

,ppt

,Exam

,Extra Questions

,Previous Year Questions with Solutions

,Objective type Questions

,Important questions

,Free

,Semester Notes

,Sample Paper

,Introduction to Budgetary Control - Budgetary Control

;

Introduction to Budgetary Control - Budgetary Control, Cost Management Free PDF Download

Importance of Introduction to Budgetary Control - Budgetary Control, Cost Management

Introduction to Budgetary Control - Budgetary Control, Cost Management Notes

Introduction to Budgetary Control - Budgetary Control, Cost Management UGC NET Questions

Study Introduction to Budgetary Control - Budgetary Control, Cost Management on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!