NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations | Additional Study Material for Commerce PDF Download

PAGE NO. 55

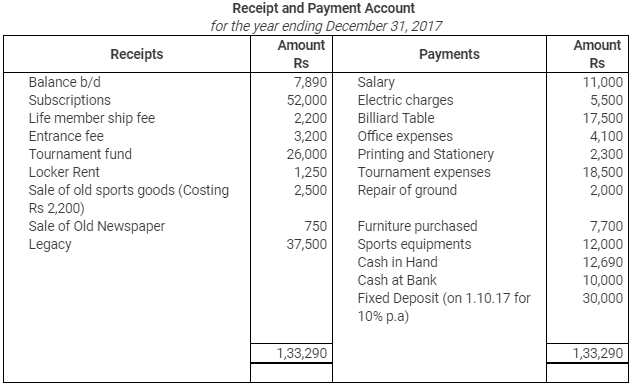

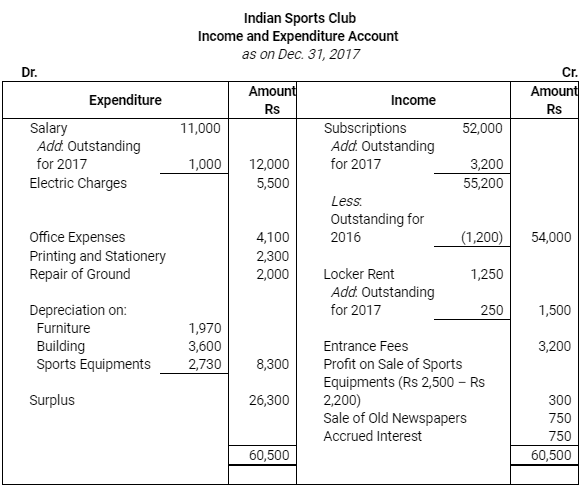

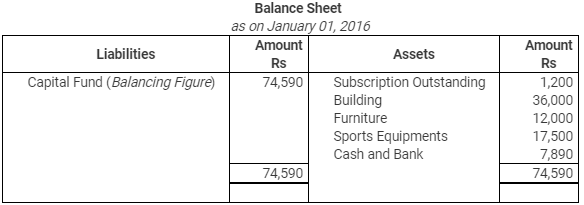

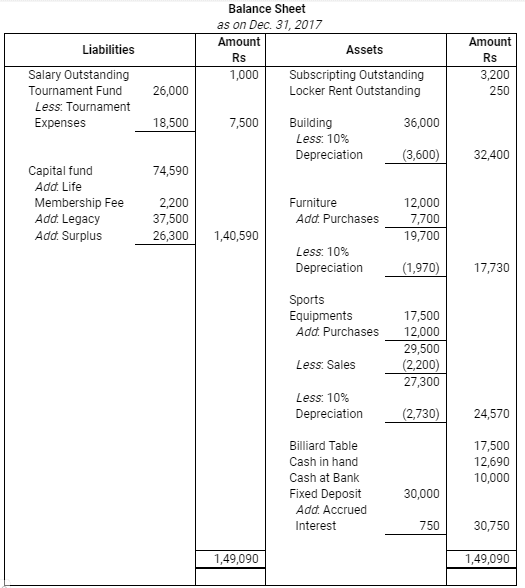

Q.8. Following is the Receipt and Payment Account of Indian Sports Club, prepared Income and Expenditure Account, Balance Sheet as on December 31, 2017:

Other Information:

Subscription outstanding was on December 31, 2016 Rs 1,200 and Rs 3,200 on December 31, 2017. Locker rent outstanding on December 31, 2013 Rs 250. Salary outstanding on December 31, 2013 Rs 1,000.

On January 1, 2017, club has Building Rs 36,000, furniture Rs 12,000, Sports equipments Rs 17,500. Depreciation charged on these items @ 10% (including Purchase).

Ans.

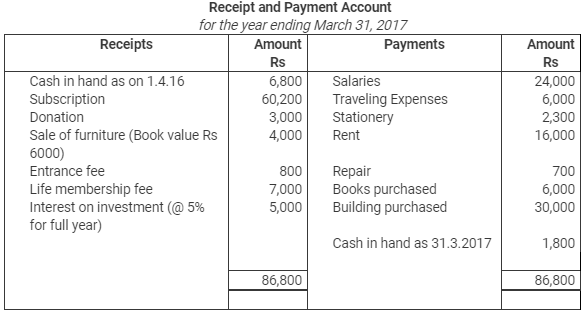

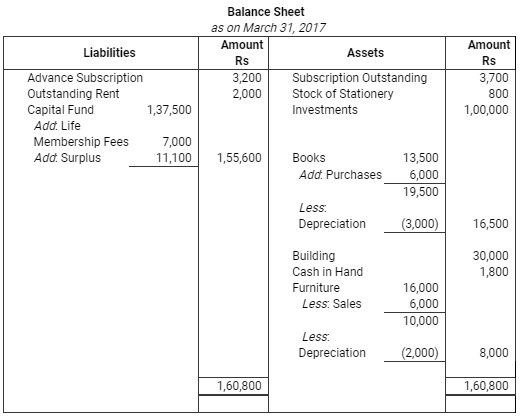

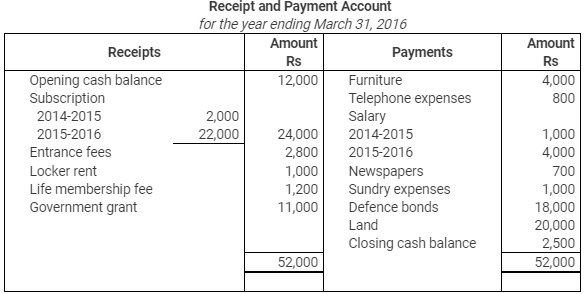

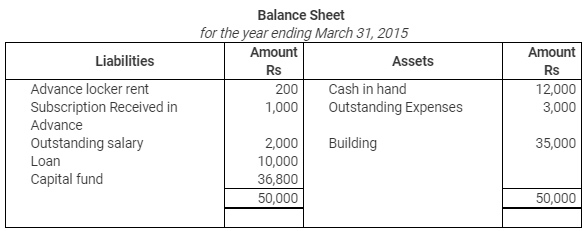

Q.9. From the following Receipt and Payment Account of Jan Kalyan Club, prepare Income and Expenditure Account and Balance Sheet for the year ending March 31, 2017.

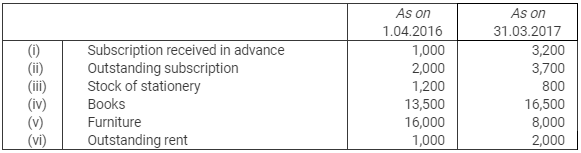

Additional Information:

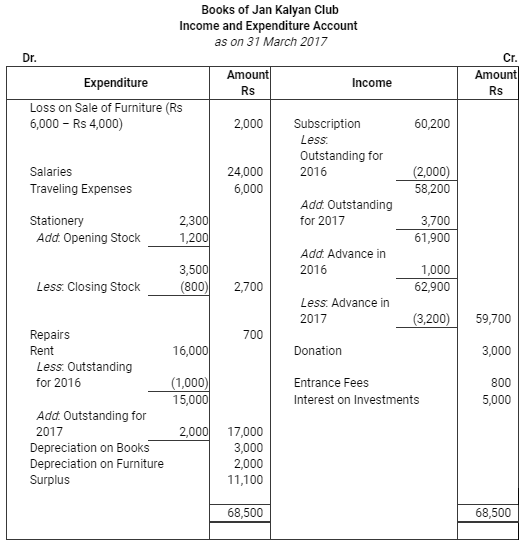

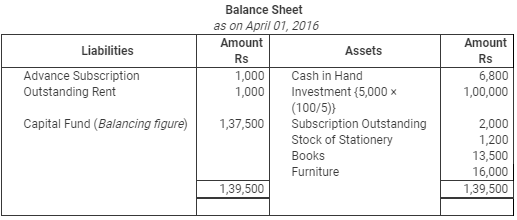

Ans.

PAGE NO. 56

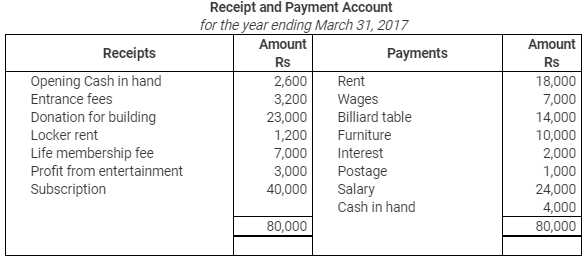

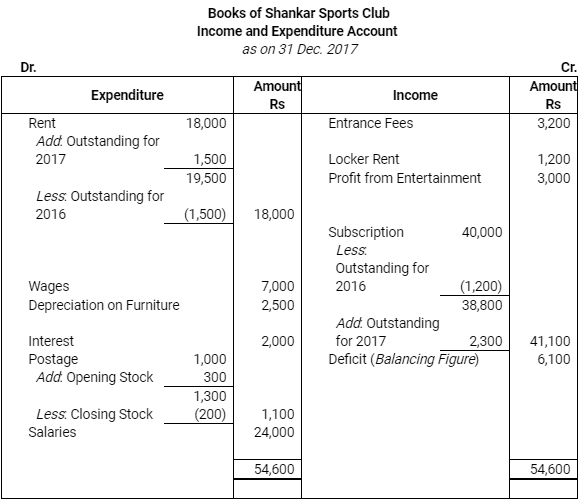

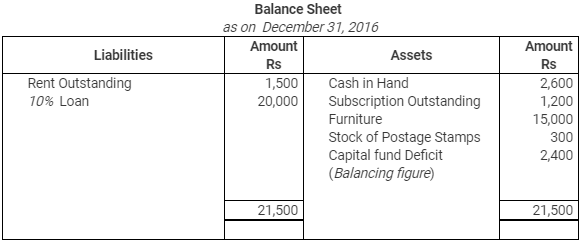

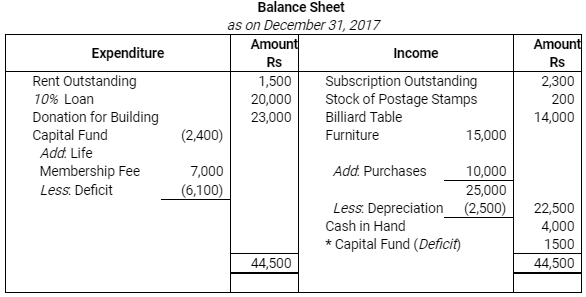

Q.10. Receipt and Payment Account of Shankar Sports club is given below, for the year ended March 31, 2017

Prepare Income and Expenditure Account and Balance Sheet with help of following Information:

Subscription outstanding on March 31, 2016 is Rs 1, 200 and Rs 2,300 on March 31, 2017, opening stock of postage stamps is Rs 300 and closing stock is Rs 200, Rent Rs 1,500 related to 2015 and Rs 1,500 is still unpaid.

On April 01, 2016 the club owned furniture Rs 15,000, Furniture valued at Rs 22,500

On March 31, 2017. The club took a loan of Rs 20,000 (@ 10% p.a.) in 2017*.

Ans.

PAGE NO. 57

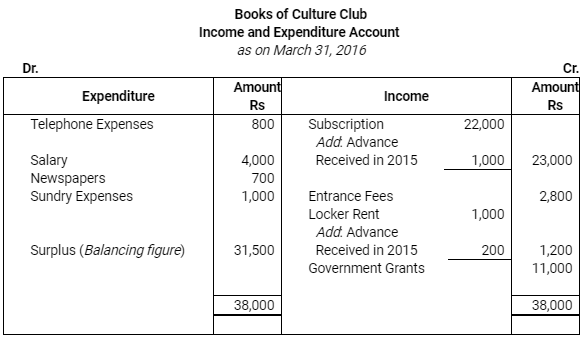

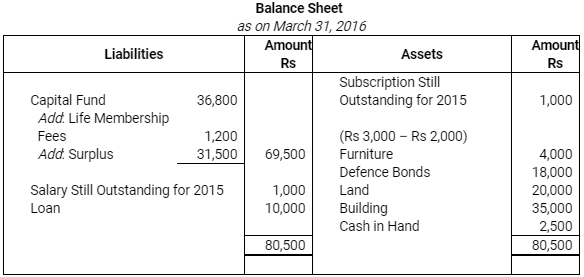

Q.11. Prepare Income and Expenditure Account and Balance Sheet for the year ended December 31, 2006 from the following Receipt and Payment Account and Balance Sheet of culture club:

Ans.

PAGE NO. 58

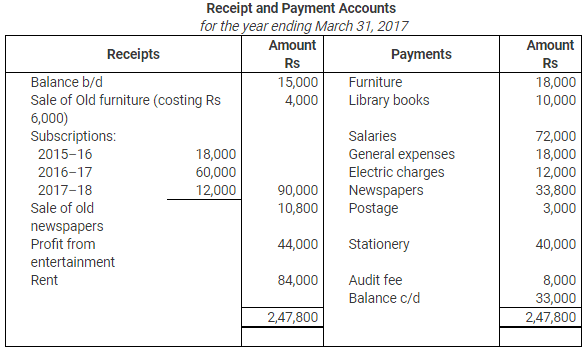

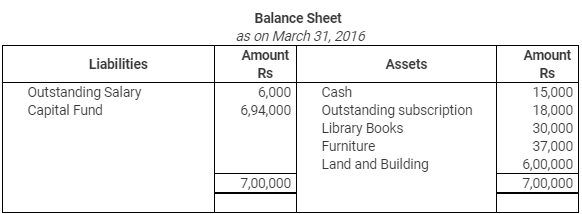

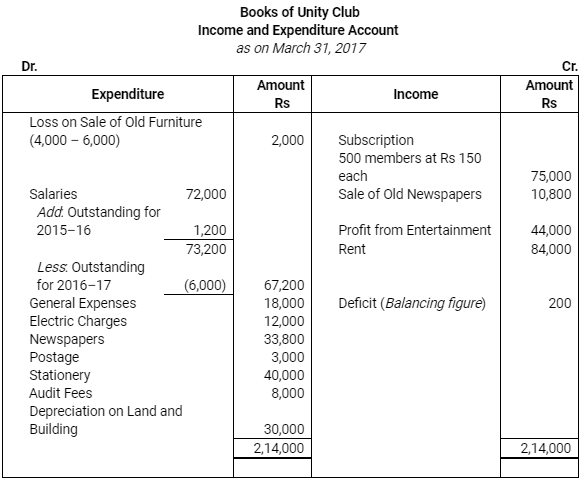

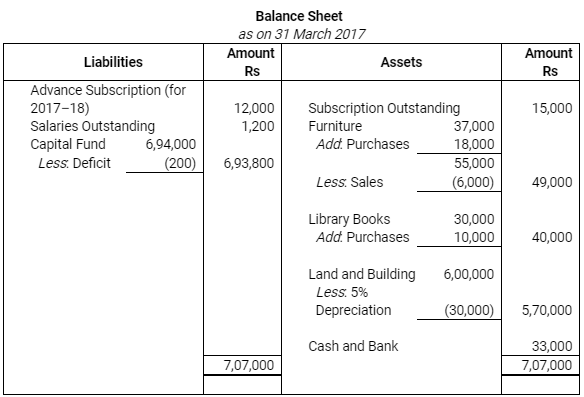

Q.12. From the following Receipt and Payment Account prepare final accounts of a Unity Club for the year ended March 31, 2017.

Additional Information:

1. The Club had 500 members each paying an annual subscription of Rs 150.

2. On 31.3.2016 salaries outstanding amounted to Rs 1,200 and salaries paid included Rs 6,000 for the year 2015–16.

3. Provide 5% depreciation on Land and Building.

Ans.

|

4 videos|168 docs

|

FAQs on NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations - Additional Study Material for Commerce

| 1. What is the meaning of not-for-profit organizations in accounting? |  |

| 2. How are donations and grants accounted for in not-for-profit organizations? | |

| 3. How are expenses allocated in not-for-profit organizations? | |

| 4. How are surplus or deficit calculated in not-for-profit organizations? | |

| 5. Are not-for-profit organizations exempt from paying taxes? | |

study material

,Extra Questions

,MCQs

,NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations | Additional Study Material for Commerce

,Objective type Questions

,past year papers

,NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations | Additional Study Material for Commerce

,practice quizzes

,NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations | Additional Study Material for Commerce

,Summary

,Viva Questions

,Important questions

,Previous Year Questions with Solutions

,shortcuts and tricks

,video lectures

,Exam

,ppt

,mock tests for examination

,Sample Paper

,Semester Notes

,Free

;

NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations Free PDF Download

Importance of NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations

NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations Notes

NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations Commerce Questions

Study NCERT Solution (Part - 3) - Accounting for Not for Profit Organisations on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!