NCERT Solution - Financial Statements of a Company | Accountancy Class 12 - Commerce PDF Download

Short Answer Questions

Q1: State the meaning of financial statements?

Ans: The preparation of the Financial Statements is done from the Trial Balance. They are responsible for depicting the true financial position of the business and they may further provide the valuable financial information to the users. The Financial statements include the following:

- Trading and Profit & Loss A/c or Income statement: This shows the financial performance by determining the profit or loss made by the business during an accounting year.

- Balance sheet: This showcases the financial position of the business by telling about the assets, liabilities and The capital as on a particular date.

- Cash flow statement: This is responsible for showcasing the inflow and outflow of cash during a particular accounting period.

Financial statements are prepared from Trial Balance. They should present a true and fair view of the financial performance and financial position of a business. They provide valuable information to the users/stakeholders and aid them in decision-making.

Q2: What are limitations of financial statements?

Ans: Limitations of financial statements are given below.

- Ignores Changes in the Price level:

The financial analysis fails to capture the change in price level. The figures of different years are taken on nominal values and not in real terms (i.e. not taking price change into consideration). - Misleading and Wrong Information:

The financial analysis fails to reveal the change in the accounting procedures and practices. Consequently, they may provide wrong and misleading information. - Interim and Final Picture:

The financial analysis presents only the interim report and thereby provides incomplete information. They fail to provide the final and holistic picture. - Ignores Qualitative and Non-monetary Aspects:

The financial analysis reveals only the monetary aspects. In other words, these analyses consider only that information that can be expressed only in monetary terms. These analyses fail to disclose managerial efficiency, growth prospects, and other non-operational efficiency of a business.

Q3: List any three objectives of financial statements?

Ans: Objectives of Financial Statements

The following are the various objectives for preparing financial statements.

- It enables the conduct of meaningful comparisons of financial data. It provides better and easy understanding of the changes in the financial data overtime.

- It helps in designing effective plans and better execution of plans by enabling control and checks over the use of the financial resources.

- Analysis of Financial Statements helps to know the earning capacity and profitability of a business firm. It also measures the efficiency of the business operations.

Q4: State the importance of financial statements to:

(i) shareholders

(ii) creditors

(iii) government

(iv) investors

Ans: Importance of financial statements to its various users is given below.

(i) Shareholders: They are interested in assessing the profitability and viability of the capital invested by them in the business. The financial statements prepared by the business concerns enable them to have sufficient information to assess the financial performance and financial health of the business.

(ii) Creditors: These are those individuals and organisations to whom a business owes money on account of credit purchases of goods and services. Hence, the creditors require information about the credit worthiness and liquidity position of the business.

(iii) Government: It needs information to determine various macroeconomic variables such as national income, GDP, industrial growth, etc. The accounting information assist the government in the formulation of various policies measures and to address various economic problems such as unemployment, poverty, etc

(iv) Investors: These are the parties who have invested or are planning to invest in the business of an enterprise. Hence, in order to assess the viability and prospects of their investments, they need information about the profitability and solvency position of the business.

Q5: How will you disclose the following items in the Balance Sheet of a company;

(i) Current assets, inventory

(ii) Contigent liabilities in notes to accounts

(iii) Shareholders Funds, Reserve and Surplus

(iv) Fixed Assets, Intangible Assets

(v) Proposed Dividend for the current year

(vi) Non Current Liabilities

(vii) Arrears of Dividend on Commulative Preference Shares.

Ans: Disclosure of various items in the Balance Sheet of a company is given below.

Long Answer Questions

Q1: Explain the nature of the financial statements.

Ans: The financial statements are the end-products of the accounting process. The financial statements not only reveal the true financial position of the company but also help various accounting users in decision-making and policy-designing process. The nature of the financial statements depends upon the following aspects like recorded facts, conventions, concepts, and personal judgment

1. Recorded facts- The items recorded in the financial statements reflect their original cost i.e. the cost at which they were acquired. Consequently, financial statements do not reveal the current market price of the items. Further, financial statements fail to capture the inflation effects.

2. Conventions- Prudence Convention, Materiality Convention, Matching Concept, etc. The adherence to such accounting conventions makes financial statements easy to understand, and comparable and reflects the true and fair financial position of the company.

3. Accounting Assumptions − These basic accounting assumptions like Going Concern Concept, Money Measurement Concept, Realisation Concept, etc are called as postulates. While preparing financial statements, certain postulates are adhered to. The nature of these postulates is reflected in the nature of the financial statements.

4. Personal Judgments- Personal value judgments play an important role in deciding the nature of the financial statements. Different judgments are attached to different practices of recording transactions in the financial statements. For example, recording stock either at market value or at the cost requires value judgment. Similarly, provision on various assets, method of charging depreciation, period related to writing off intangible assets depends on personal judgment. Thus, personal judgments determine the nature of the financial statements to a great extent.

Q2: Explain in detail about the significance of the financial statements.

Ans: The importance of financial statements is mentioned below.

- Provides Information- Financial statements provide information to various accounting users both internal as well as external users. It acts as a basic platform for different accounting users to derive information according to varying needs. For example, the financial statements on one hand help the shareholders and investors in assessing the viability and return on their investments, while on the other hand, the financial statements help the tax authorities in calculating the amount of tax liability of the company.

- Cash Flow- Financial statements provide information about the cash flows of the company. The financial statements help the creditors and other investors in determining the solvency of a company.

- Effectiveness of Management- The comparability feature of the financial statements enables management to undertake comparisons like inter-firm and intra-firm comparisons. This not only helps in assessing the viability and performance of the business but also helps in designing policies and drafting policies. The financial statements enhance the effectiveness and efficacy of the management.

- Disclosure of Accounting Policies- Financial statements provide information about the various policies, important changes in the methods, practices and process of accounting by the company. The disclosure of the accounting policies makes financial statements simple, true and enables different accounting users to understand without any ambiguity.

- Policy Formation by Government- It needs information to determine national income, GDP, industrial growth, etc. The accounting information assists the government in the formulation of various policy measures and to address various economic problems like employment, poverty etc.

- Attracts Investors and Potential Investors- They invest or plan to invest in the business. Hence, in order to assess the viability and prospectus of their investment, creditors need information about the profitability and solvency of the business.

Q3: Explain the limitations of financial statements.

Ans: The following are the limitations of financial statements.

- Historical Data: The items recorded in the financial statements reflect their original cost i.e. the cost at which they were acquired. Consequently, financial statements do not reveal the current market price of the items. Further, financial statements fail to capture the inflation effects.

- Ignorance of Qualitative Aspect: Financial statements do not reveal the qualitative aspects of a transaction. The qualitative aspects like colour, size and brand position in the market, employee qualities and capabilities are not disclosed by the financial statements.

- Biased: Financial statements are based on personal judgments regarding the use of methods of recording. For example, the choice of practice in the valuation of inventory, method of depreciation, amount of provisions, etc. are based on personal value judgments and may differ from person to person. Thus, the financial statements reflect the personal value judgments of the concerned accountants and clerks.

- Inter-firm Comparisons: Usually, it is difficult to compare the financial statements of two companies because of the difference in the methods and practices followed by their respective accountants.

- Window dressing: The possibility of window dressing is probable. This might be because of the motive of the company to overstate or understate the assets and liabilities to attract more investors or to reduce taxable profit. For example, Satyam showed high fixed deposits on the Assets side of its Balance Sheet for better liquidity and gave false and misleading signals to the investors.

- Difficulty in Forecasting: Since the financial statements are based on historical data, they fail to reflect the effect of inflation. This drawback makes forecasting difficult.

Q4: Prepare the format of statement of profit and loss and explain its items upto the as certainment of profit before tax.

Ans: Format of Statement of Profit and Loss- As per the REVISED SCHEDULE VI

I. Revenue from Operations- It refers to the revenue earned from the basic operating business activities of an organization. For Non-financing companies, it consists of the following.

- Sale of Products

- Sale of Services

- Other Operating Revenues

For financing companies, revenue from operations includes the following.

- Interest

- Dividends

- Other Financial Services

II. Other Incomes- This income includes the income earned other than from the operating activities of a business. It comprised of the following incomes.

- Interest Income (in the case of a Non-Financing Company)

- Dividend Income (in the case of a Non-Financing Company)

- Net Gain or Loss on Sale of Investments

- Other Non-Operating Incomes (i.e. after deducting expenses directly related to such income)

III. Expenses- These can be bifurcated in the following given below types.

- Cost of Materials Consumed- It includes all the materials consumed during the process of manufacturing. It can also be calculated with the help of the given below formula.

- Material Consumed = Opening Stock of Raw Material + Purchase of Raw Material – Closing Stock of Raw Material

- Purchase of Stock-in-Trade- It includes all the goods purchased by a trading concern with the intention of reselling.

- Change in Inventories, Work-in-Progress and Stock-in-Trade- It is the difference of the opening and closing balance of inventories (stock), work-in-progress and stock-in-trade.

Q5: Prepare the format of balance sheet and explain the various elements of balance sheet.

Ans: COMPANY'S BALANCE SHEET- As per REVISED SCHEDULE VI

Items under the head Equity and Liabilities

1. Shareholders’ Funds

a. Share Capital:

- Authorised Capital-

- Issued Share Capital-

- Subscribed Share Capital-

- Called-up Share Capital-

- Paid-up Share Capital-

- Share Forfeiture Amount

b. Reserves and Surplus: It consists of the following items to be shown separately.

- Capital Reserve

- Capital Redemption Reserve

- Securities Premium

- Debenture Redemption Reserve

- Revaluation Reserve

- Other Reserves (such as General Reserve, Tax Reserve, etc.)

- Proposed Additions to Reserves

- Sinking Fund

- Share Option Outstanding Amount

- Surplus i.e. credit balance in Statement of Profit and Loss. However, in the case of debit balance in Statement of Profit and Loss, it is deducted from the total reserves.

c. Money received against warrants: A financial instrument that allows its holder to acquire equity shares is known as Share Warrant. Any amount received by the company on such share warrants is required to be disclosed under this head.

2. Share Application Money Pending Allotment

The amount received by the company on the application of shares issued and the allotment on which is to be received after the date of balance sheet is shown under this head separately.

3. Non-Current Liabilities

These are comprised of the following items.

a. Long-Term Borrowings- It is further consists of the given below items.

- Debentures

- Bonds

- Term Loans from bank as well as from other parties

- Deposits

- Other Loans and Advances

b. Deferred Tax Liabilities (Net)

c. Other Long-Term Liabilities

d. Long-Term Provisions

4. Current Liabilities

Under this head, the following items are disclosed.

a. Short-term Liabilities- It is further comprised of the given below items.

- Loan repayable on demands from bank as well as from other parties

- Deposits

- Other Loans and Advances

b. Trade Payables

c. Other Current Liabilities- It includes all those liabilities that are not covered in any of the mentioned above heads. Some examples are-

- Income received in advance

- Interest accrued but not due on borrowings

- Interest accrued and due on borrowings

- Unpaid Dividends

- Calls-in-Advance and interest thereon

- Other Payables etc.

d. Short-term Provisions- These are categorised as follows.

- Provision for Doubtful Debts

- Proposed Dividend

- Provision for Tax

- Provision for Employees Benefits

- Others

Items under the head Assets

Non-Current Assets and Current Assets are two titles that come under the heading of Assets.

1. Non-Current Assets

a. Fixed Assets- These are further classified s follows.

- Tangible Assets (such as, Building, Machinery, Furniture, etc.)

- Intangible Assets (such as Goodwill, Trademark, Copyrights, Mining Rights, etc.)

- Capital Work-in-Progress

- Intangible Assets under development

b. Non-current Investments- These are the investments that are not held for the purpose of resale.

c. Deferred Tax Assets

d. Long-term Loans and Advances

e. Other Non-Current Assets

2. Current Assets

Under this head the following items are shown.

a. Current Investments- Investments that are held for conversion into cash within a period of 12 months. These are further classified as follows.

- Investment in Equity Shares

- Investment in Preference Shares

- Investment in Government or Trust Securities

- Investment in Debentures or Bonds

- Investment in Mutual Funds

- Investment in Partnership Firms

- Other Investments

b. Inventories- It comprised of the given items.

- Raw Materials

- Work-in-Progress

- Finished Goods

- Stock-in-Trade (goods acquired for trading)

- Stores and Spares

- Loose Tools

c. Trade Receivables

d. Cash and Cash Equivalents- These are classified as follows.

- Cash on Hand

- Balances with Banks

- Cheques, Drafts on Hand

- Others

e. Short-term Loans and Advances

f. Other Current Assets (such as prepaid expenses, advance taxes, etc.)

Q6: Explain how financial statements are useful to the various parties who are interested in the affairs of an undertaking?

Ans: The various parties that are directly or indirectly interested in the financial statements of a company can be categorized into the following two categories:

1. Internal parties

2. External parties

Internal Parties

The following are the various internal accounting users who are directly related to the company.

- Owner: The owner/s is/are interested in the profit earned or loss incurred during an accounting period. They are interested in assessing the profitability and viability of the capital invested by them in the business.

- Management: The financial statements help the management in drafting various policies and measures, facilitating planning and decision-making processes. The financial statements also enable management to exercise various cost-controlling measures and to remove inefficiencies.

- Employees and workers: They are interested in the timely payment of wages and salaries, bonuses and appropriate increments in their wages and salaries. With the help of the financial statements, they can know the amount of profit earned by the company and can demand reasonable hike in their wages and salaries.

External Parties

There are various external users of accounting who need accounting information for decision making, investment planning and to assess the financial position of the business. The various external users are given below.

- Banks and other financial institutions: Banks provide finance in the form of loans and advances to various businesses. Thus, they need information regarding liquidity, creditworthiness, solvency and profitability to advance loans.

- Creditors: These are those individuals and organisations to whom a business owes money on account of credit purchases of goods and receiving services; hence, the creditors require information about credit worthiness of the business.

- Investors and potential investors: They invest or plan to invest in the business. Hence, in order to assess the viability and prospectus of their investment, creditors need information about the profitability and solvency of the business.

- Tax authorities: They need information about sales, revenues, profit and taxable income in order to determine the levy of various types of tax on the business.

- Government: It needs information to determine national income, GDP, industrial growth, etc. The accounting information assists the government in the formulation of various policy measures and in addressing various economic problems like employment, poverty etc.

- Researchers: Various research institutes like NGOs and other independent research institutions like CRISIL, stock exchanges, etc. undertake various research projects and the accounting information facilitates their research work.

- Consumers: Every business tries to build up a reputation in the eyes of consumers, which can be created by the supply of better quality products and post-sale services at reasonable and affordable prices. A business that has transparent financial records, assists the customers in knowing the correct cost of production and accordingly assesses the degree of reasonability of the price charged by the business for its products and, thus, helps in repo building of the business.

- Public: The public is keenly interested in knowing the proportion of the profit that the business spends on various public welfare schemes; for example, charitable hospitals, funding schools, etc. This information is also revealed by the profit and loss account and balance sheet of the business.

Q7: `Financial statements reflect a combination of recorded facts, accounting conventions and personal judgments’ discuss.

Ans: The financial statements are the end-products of the accounting process. The financial statements not only reveal the true financial position of the company but also help various accounting users in the decision-making and policy-designing process. The nature of the financial statements depends upon the following aspects recorded facts, conventions, concepts, and personal judgment

- Recorded facts- The items recorded in the financial statements reflect their original cost i.e. the cost at which they were acquired. Consequently, financial statements do not reveal the current market price of the items. Further, financial statements fail to capture the inflation effects.

- Conventions- The preparation of financial statements is based on some accounting conventions like Prudence Convention, Materiality Convention, Matching Concept, etc. The adherence to such accounting conventions makes financial statements easy to understand, and comparable and reflects the true and fair financial position of the company.

- Accounting Assumptions − These basic accounting assumptions like the Going Concern Concept, Money Measurement Concept, Realisation Concept, etc are called as postulates. While preparing financial statements, certain postulates are adhered to. The nature of these postulates is reflected in the nature of the financial statements.

- Personal Judgments- Personal value judgments play an important role in deciding the nature of the financial statements. Different judgments are attached to different practices of recording transactions in the financial statements. For example, recording stock either at market value or at the cost requires value judgment. Similarly, provision on various assets, method of charging depreciation, period related to writing off intangible assets depend on personal judgment. Thus, personal judgments determine the nature of the financial statements to a great extent.

Q8: Explain the process of preparing income statement and balance sheet.

Ans: The process of preparing an Income Statement (now a Statement of Profit and Loss) as per Revised Schedule VI is explained below in chronological order.

- Prepare a Trial Balance on the basis of the balances of various accounts in the ledger.

- Record Revenue from Operations i.e. Sales less Sales Return.

- Add Other Incomes to Revenue from Operations (such as profit on sale of assets, cash discount received etc.) to ascertain Total Revenue.

- Deduct all the expenses incurred by the company from Total Revenue (such as cost of material consumed, finance cost, depreciation and amortisation etc.) to ascertain Profit before Tax.

- Deduct Tax paid by the company from Profit before Tax to ascertain the Profit or loss for the period.

The process of preparing the Balance Sheet as per the Revised Schedule VI is explained below in a chronological order.

As per this schedule, the Balance Sheet is prepared in vertical format and divided into two parts i.e.

(i) Equity and Liabilities and

(ii) Assets - Under the head Equity and Liabilities: Shareholders' Funds, Share Application Money Pending Allotment, Non-Current Liabilities and Current Liabilities are recorded.

- After recording Equity and Liabilities, Assets are recorded. Under this head, all the Non-Current Assets (such as Tangible and Intangible Assets, Capital Work-in-Progress etc.) and Current Assets (such as Inventories, Trade Receivables, Current Investment etc.) are recorded.

- At the end, a total of two heads is ascertained, which must be equal.

Numerical Questions

Q1: Show the following items in the balance sheet as per the provisions of the Companies Act, 2013 in Schedule III:

Ans:

Notes to Accounts

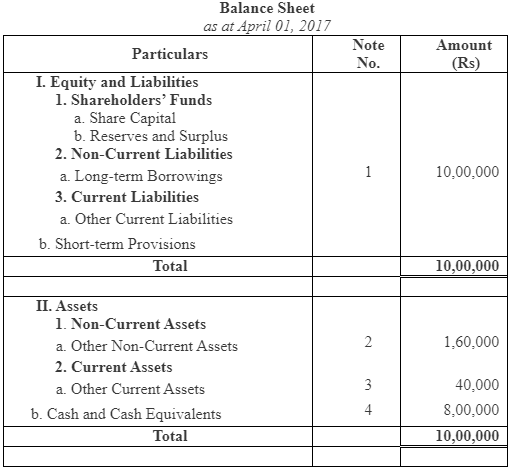

Q2: On April 1 , 2017, Jumbo Ltd., issued 10,000; 12% debentures of Rs. 100 each a discount of 20%, redeemable after 5 years. The company decided to write-off discount on issue of such debentures on March 31, 2018.

Show the items in the balance sheet of the company immediately after the issue of these debentures.

Ans:

Notes to Accounts

Notes to Accounts

Q3: From the following information prepare the balance sheet of Gitanjali Ltd., as per the (Revised) Schedule VI:

Inventories Rs. 14,00,000; Equity Share Capital Rs. 20,00,000; Plant and Machinery Rs. 10,00,000; Preference Share Capital Rs. 12,00,000; Debenture Redemption Reserve Rs. 6,00,000; Outstanding Expenses Rs. 3,00,000; Proposed Dividend Rs. 5,00,000; Land and Building Rs. 20,00,000; Current Investments Rs. 8,00,000; Cash Equivalent Rs. 10,00,000; Short term loan from Zaveri Ltd. (A Subsidiary Company of Twilight Ltd.) Rs. 4,00,000; Public Deposits Rs. 12,00,000.

Ans:

Q4: From the following information prepare the balance sheet of Jam Ltd. as per the (revised) Schedule VI:

Inventories Rs. 7,00,000; Equity Share Capital Rs. 16,00,000; Plant and Machinery Rs. 8,00,000; Preference Share Capital Rs. 6,00,000; General Reserves Rs. 6,00,000; Bills payable Rs. 1,50,000; Provision for taxation Rs. 2,50,000; Land and Building Rs. 16,00,000; Noncurrent Investments Rs. 10,00,000; Cash at Bank Rs. 5,00,000;Creditors Rs. 2,00,000; 12% Debentures Rs. 12,00,000.

Ans:

Q5: Prepare the balance sheet of Jyoti Ltd. as at March 31, 2017 from the following information:

Building Rs. 10,00,000; Investments in the shares of Metro Tyers Rs. 3,00,000; Stores & Spares Rs. 1,00,000; Discount on issue of 10% debentures Rs. 10,000; Statement of Profit and Loss (Dr.) Rs. 90,000; 5,00,000 Equity Shares of Rs. 20 each fully paid-up; Capital Redemption Reserve Rs. 1,00,000; 10% Debentures Rs. 3,00,000; Unpaid dividends Rs. 90,000; Share options outstanding account Rs. 10,000.

Ans:

*Note: There is a misprint in the book. The number of equity shares issued must be 50,000 so that both sides of the Balance Sheet stand equal.

Q6: Brinda Ltd. has furnished the following information:

(a) 25,000, 10% debentures of Rs. 100 each;

(b) Bank Loan of Rs. 10,00,000 repayable after 5 years;

(c) Interest on debentures is yet to be paid.

Show the above items in the balance sheet of the company as at March 31, 2017.

Ans:

Question 7: Prepare a balance sheet of Black Swan Ltd., as at March 31, 2017 from the following information:

Ans:

|

42 videos|199 docs|43 tests

|

FAQs on NCERT Solution - Financial Statements of a Company - Accountancy Class 12 - Commerce

| 1. What are the key components of a financial statement for a company? |  |

| 2. How do financial statements help in analyzing a company's performance? | |

| 3. What is the difference between cash flow and profit in financial statements? | |

| 4. Why is it important for companies to prepare financial statements regularly? | |

| 5. What role do auditors play in the financial statement process? | |

NCERT Solution - Financial Statements of a Company | Accountancy Class 12 - Commerce

,Important questions

,past year papers

,shortcuts and tricks

,NCERT Solution - Financial Statements of a Company | Accountancy Class 12 - Commerce

,Previous Year Questions with Solutions

,video lectures

,practice quizzes

,Semester Notes

,Extra Questions

,mock tests for examination

,NCERT Solution - Financial Statements of a Company | Accountancy Class 12 - Commerce

,MCQs

,Exam

,study material

,Viva Questions

,Sample Paper

,Summary

,Objective type Questions

,Free

,ppt

;

NCERT Solution - Financial Statements of a Company Free PDF Download

Importance of NCERT Solution - Financial Statements of a Company

NCERT Solution - Financial Statements of a Company Notes

NCERT Solution - Financial Statements of a Company Commerce Questions

Study NCERT Solution - Financial Statements of a Company on the App

|

© EduRev

|

Education Revolution

|

|