Question Paper 2016 (Set 3) | Additional Study Material for Commerce PDF Download

Annual Examination – (2015-16)

Accountancy (Set 3)

Class – XI

Time: 3 Hrs. M.M. 90

General Instructions:

(i) All the questions are compulsory.

(ii) Question no. 1 to 4 and 16 to 17 are very short answer type question carrying 1 mark each.

(iii) Question no. 5 to 8 and 18 to 19 are short answer type question carrying 3 marks each.

(iv) Question no. 9 to 12 and 20 are also short answer type question carrying 4 marks each.

(v) Question no. 13 to 15 and 21 to 22 are long answer type question carrying 6 marks each.

(vi) Question no. 23 and are very long answer type question carrying 8 marks each.

(vii) All parts of the question must be attempted at one place.

(viii) Show working notes wherever necessary.

Section-A

1. Is cash memo a source document or an accounting voucher?

2. Rent is paid for the month of April, 2013 in March, 2013. The accounting year ended on 31st March, 2013. The accountant has shown it on the assets side of balance sheet. Is he correct? Identify the value followed by the accountant.

3. Name the column in the journal which is not filled at the time of journalising?

4. Should a transaction be first recorded in a journal or a ledger. Why?

5. State the nature of accounting information required by (a) management (b) Owners

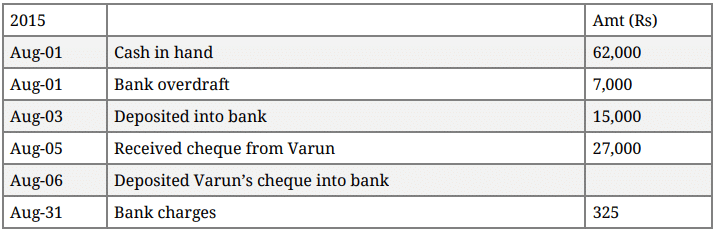

6. From the following particulars, prepare a bank reconciliation statement showing the balance as per cash book on 31st December, 2015.

(i) The following cheques were paid into bank in December, but were credited in January. X Rs. 35,000, Y Rs 25,000 and Z Rs 20,000.

(ii) The following cheques were issued by the firm in December, but were presented in January P Rs 40,000, Q Rs 45,000.

(iii) A cheque for Rs 10,000 which was received from a customer was entered in the bank column of the cash book in December, but was omitted to be banked in December. (iv) The pass book shows a debit entry of Rs 10,000 for bank charges and credit entry of Rs 20,000 for interest.

(v) Interest on investments Rs 25,000 collected by bank appeared in the pass book.

(iv) The bank balance as per pass book was Rs 6,20,000 on 31st December, 2013.

7. Briefly discuss the three branches of accounting?

8. Explain briefly any three advantages of double entry system of accounting?

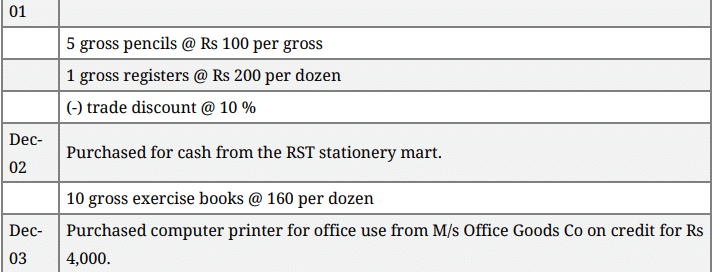

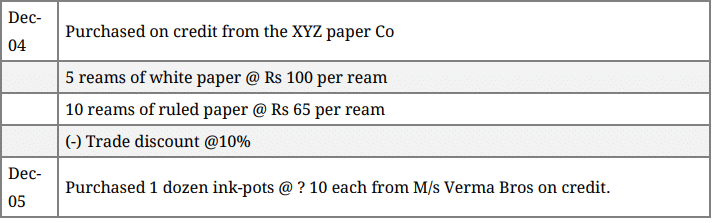

9. Record the following in the appropriate book of original entry.

10. Rectify the following errors

(i) Wages paid for installation of machinery Rs 500 was posted to wages account as Rs 50.

(ii) Machinery purchased from Ram & Co for Rs 10,000 on credit was entered in purchase book as Rs 6,000 and posted there from to Ram & Co as Rs 1,000.

(iii) Credit sales to Vishal Rs 5,000 were recorded in purchase book.

(iv) Credit purchases from Sohan & Co for Rs 6,000 were recorded in sales book. However, Sohan & Co was correctly credited.

11. The rough book of M/s MNO & Co contains the following

Prepare the purchase book of M/s MNO & Co

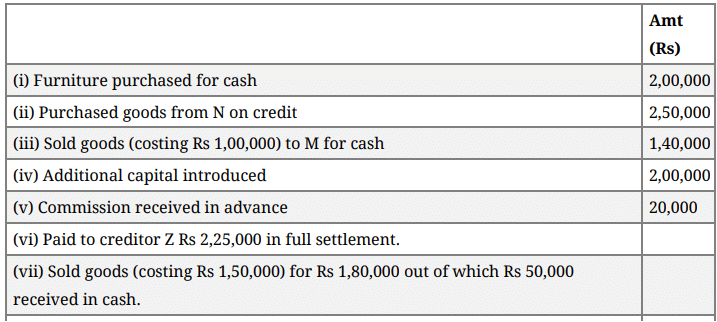

12. Mr Nanda started business as on 1st April, 2013 with a capital of 15,00,000. During the year, the following transactions took place.

13. On 1st October, 2011 the MNP transport company purchased a truck for Rs 40,00,000. On 1st April, 2013 this truck was involved in an accident and was completely destroyed and Rs 30,00,000 were received from the insurance company in full settlement. On the same date another truck was purchased by the company for Rs 50,00,000. The company writes-off 20% depreciation per annum on written down value method. Give the truck account from 2011 to 2013.

14. A sell goods to B for Rs 10,000 and draws a bill on him for the same amount for 3 months. Before the due date, B requests A to cancel the bill, to accept Rs 3,000 as part payment and to draw a fresh bill on him for Rs 7,200 for a further period of 2 months Rs 200 being the interest for the extended period. A agrees to the proposal. The new bill is duly honoured. Pass the necessary journal entries and other party's account in the books of both the parties.

15. (i) Briefly explain the concept based on the premise 'do not anticipate profits but provide for all losses'.

(ii) Explain briefly 'full disclosure' principle of accounting?

Section – B

Financial Accounting – II

16. Adjustments for outstanding expenses, prepaid expenses or depreciation are not made in receipts and payments account. Why?

17. Name the accounting software appropriate for small business organisations, having one user and single office location.

18. Accounting software is an integral part of the computerised accounting system. An important factor to be considered before acquiring accounting software is the accounting expertise of people responsible in organisation for accounting work. In the light of this statement, briefly discuss various types of accounting software.

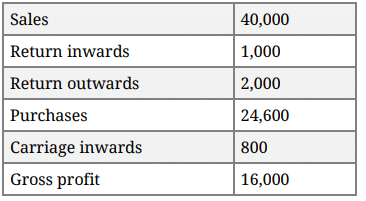

19. Calculate closing stock from the following:

(i)

(ii) Is it correct that debit balance in the profit and loss account is profit?

20. Shyam, who keeps his books on single entry system, tells you that his capital on 31st March, 2013 is Rs 11,22,000 and his capital on 1st April, 2012 was Rs 11,52,000. He further informs you that during the year, he withdrew for his household purpose Rs 5,05,200. He sold his personal investment of Rs 1,20,000 at 2% premium and brought that money into the business. You are required to prepare statement of profit or loss, also identify the value being conveyed in the question.

21. An accounting report is an essential report, which must be able to fulfill certain basic criterion. In the context of this statement, explain various types of accounting reports.

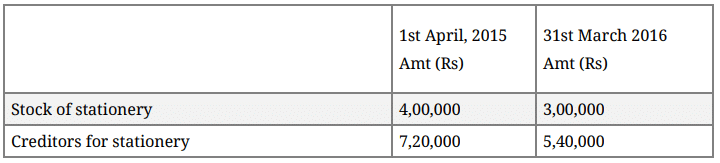

22. How will you deal with the following items while preparing the final accounts of a club

Amount paid for stationery during the year 2012-13 Rs 25,00,000.

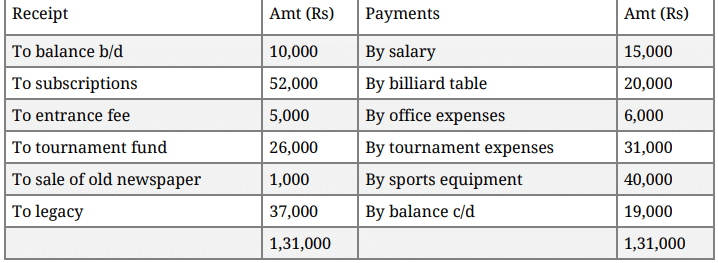

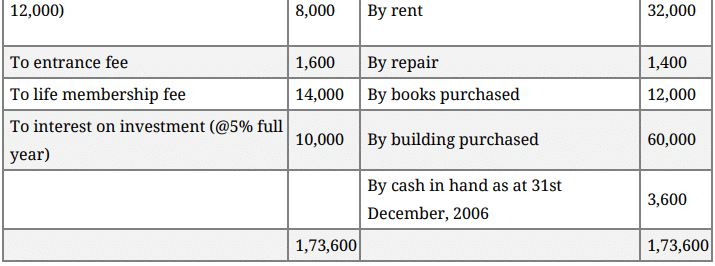

23. Following is the receipt and payment account of Indian Sports Club for the year ended 31st December, 2015

Receipt and Payment Account

For the year ended 31st December, 2013

Additional Information: On 31st December, 2013 subscription outstanding was Rs 2,000 and on 31st December, 2012 subscription outstanding was Rs 3,000. Salary outstanding on 31st December, 2013 was Rs 1,500.

On 1st January, 2013 the club had building Rs 75,000, furniture Rs 18,000, 12% investment Rs 30,000 and sports equipment Rs 30,000. Depreciation charged on these items including purchases was 10%.

Prepare income and expenditure account of the club for the year ended 31st December, 2013 and ascertain the capital fund on 31st December, 2012.

Or

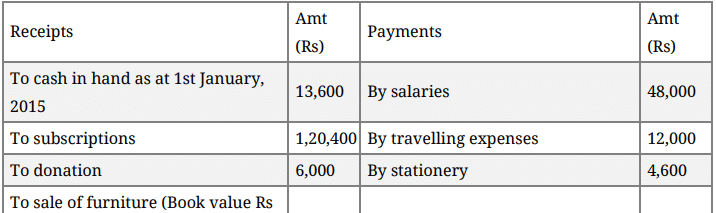

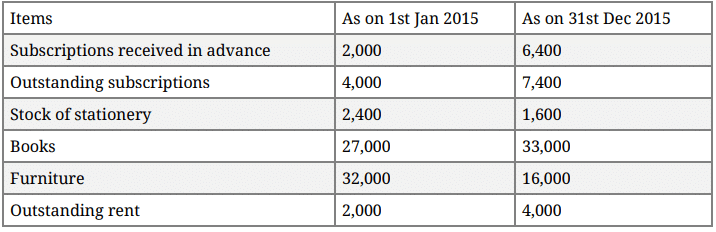

From the following receipts and payments account of Aakash Club, prepare income and expenditure account and balance sheet for the year ending 31st December, 2015.

Receipts and Payments Account

For the year ending 31st December, 2015

Additional Information:

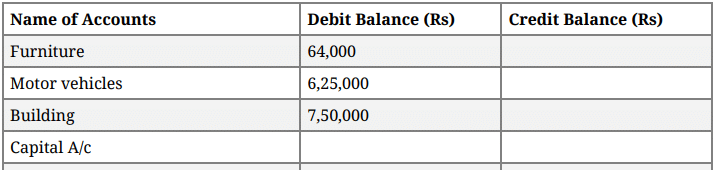

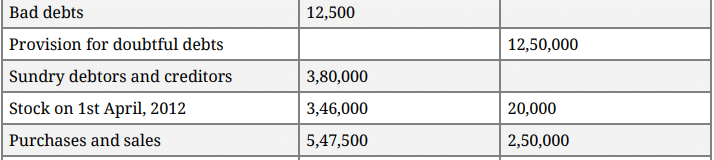

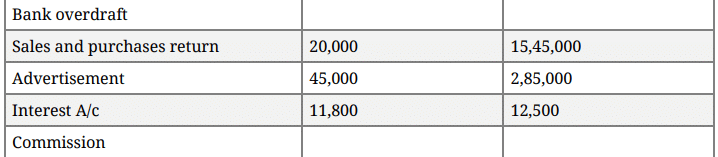

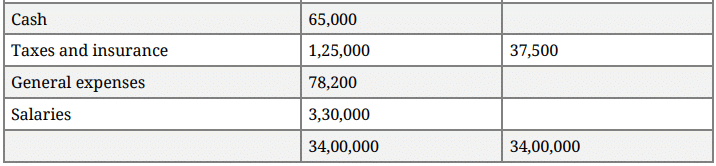

24. Following trial balance is extracted from the books of a merchant on 31st March, 2013

The following adjustments are to be made

(i) Stock in hand on 31st March, 2013 was Rs 3,25,000.

(ii) Depreciate building @ 5%, furniture @ 10% and motor vehicles @ 20%.

(iii) Rs 8,500 are due for interest on bank overdraft.

(iv) Salaries Rs 30,000 and taxes Rs 12,000 are outstanding.

(v) Insurance amounted to Rs 10,000 is prepaid.

(vi) 0ne-third of the commission received is in respect of work to be done next year.

(vii) Write off further Rs 10,000 as doubtful debts and provision for doubtful debts is to be made equal to 5% on sundry debtors.

Prepare the trading and profit and loss account for the year ended 31st March, 2013 and the balance sheet as at that date.

Or

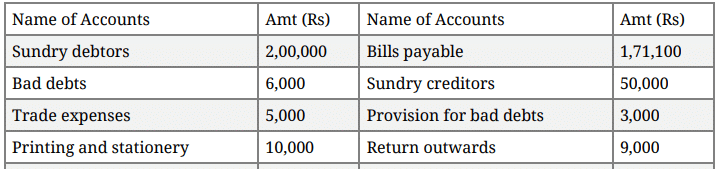

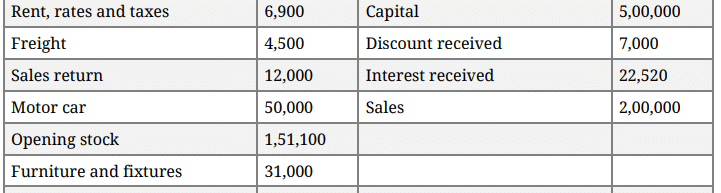

Prepare the trading and profit and loss account and a balance sheet of M/s Shine Ltd from the following particulars.

Additional Information:

(i) Closing stock was valued Rs 70,000.

(ii) Depreciation charged on furniture and fixtures @ 5%.

(iii) Further bad debts Rs 2,000. Make a provision for bad debts @ 5% on sundry debtors.

(iv) Depreciation charged on motor car @ 10%.

(v) Interest on drawings @ 6%.

(vi) Rent, rates and taxes was outstanding Rs 400.

(vii) Discount on debtors 2%.

|

4 videos|168 docs

|

FAQs on Question Paper 2016 (Set 3) - Additional Study Material for Commerce

| 1. What are the career options for commerce students? |  |

| 2. How can I prepare for commerce exams effectively? | |

| 3. What are the major subjects included in commerce stream? | |

| 4. What are the benefits of pursuing a career in commerce? | |

| 5. What skills are essential for commerce students? | |

Extra Questions

,Important questions

,Semester Notes

,Exam

,Free

,Summary

,ppt

,Viva Questions

,video lectures

,practice quizzes

,Objective type Questions

,mock tests for examination

,study material

,Question Paper 2016 (Set 3) | Additional Study Material for Commerce

,shortcuts and tricks

,Sample Paper

,past year papers

,Question Paper 2016 (Set 3) | Additional Study Material for Commerce

,MCQs

,Previous Year Questions with Solutions

,Question Paper 2016 (Set 3) | Additional Study Material for Commerce

;

Question Paper 2016 (Set 3) Free PDF Download

Importance of Question Paper 2016 (Set 3)

Question Paper 2016 (Set 3) Notes

Question Paper 2016 (Set 3) Commerce Questions

Study Question Paper 2016 (Set 3) on the App

|

© EduRev

|

Education Revolution

|

|