Rectification of Errors ( Part - 1) - Commerce PDF Download

Page No 19.39:

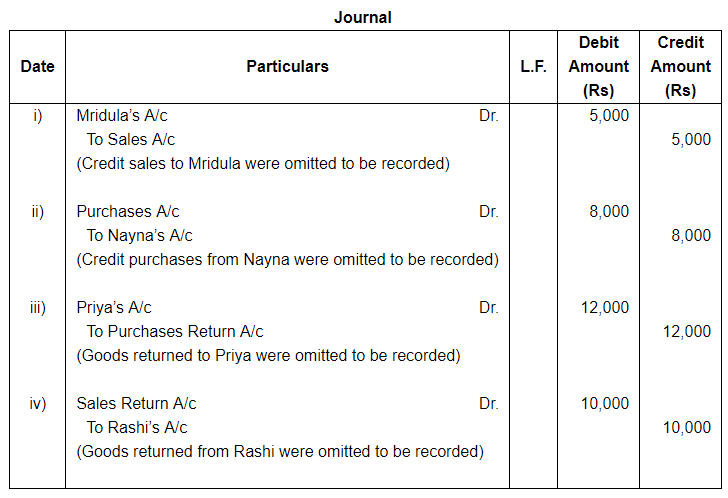

Question 1:

Rectify the following errors:

(i) Credit sales to Mridula ₹ 5,000 were not recorded.

(ii) Credit purchases from Nayna ₹ 8,000 were not recorded.

(iii) Goods returned to Priya ₹ 12,000 were not recorded.

(iv) Goods returned from Rashi ₹ 10,000 were not recorded.

ANSWER:

Two-Sided Errors

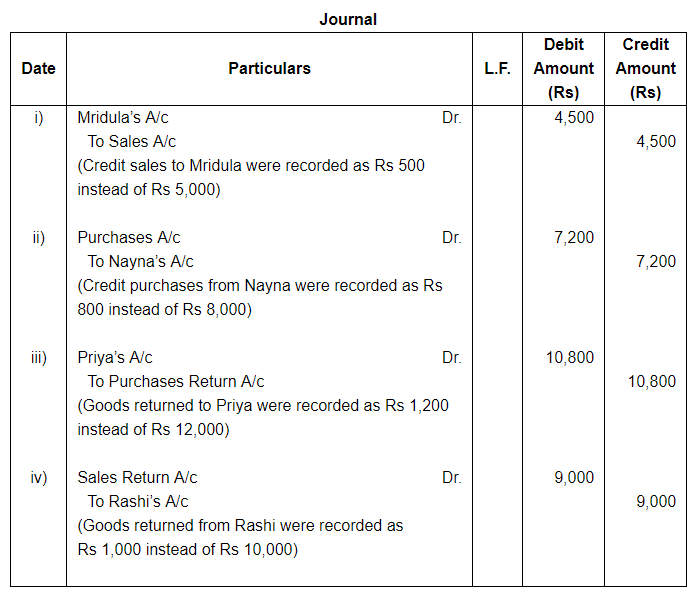

Question 2:

Rectify the following errors:

(i) Credit sales to Mridula ₹ 5,000 were recorded as ₹ 500.

(ii) Credit purchases from Nayna ₹ 8,000 were recorded as ₹ 800.

(iii) Goods returned to Priya ₹ 12,000 were recorded as ₹ 1,200.

(iv) Goods returned from Rashi ₹ 10,000 were recorded as ₹ 1,000.

ANSWER:

Two Sided Errors

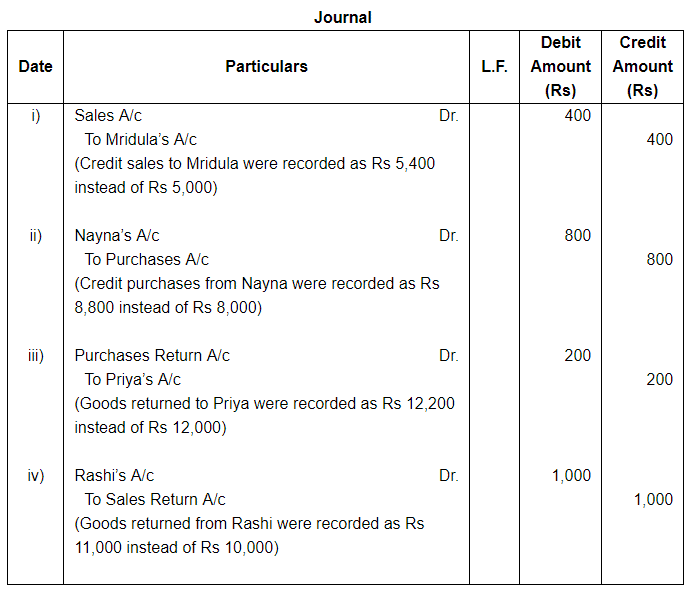

Question 3:

Rectify the following errors:

(i) Credit sales to Mridula ₹ 5,000 were recorded as ₹ 5,400.

(ii) Credit purchases from Nayna ₹ 8,000 were recorded as ₹ 8,800.

(iii) Goods returned to Priya ₹ 12,000 were recorded as ₹ 12,200.

(iv) Goods returned from Rashi ₹ 10,000 were recorded as ₹ 11,000.

ANSWER:

Two Sided Errors

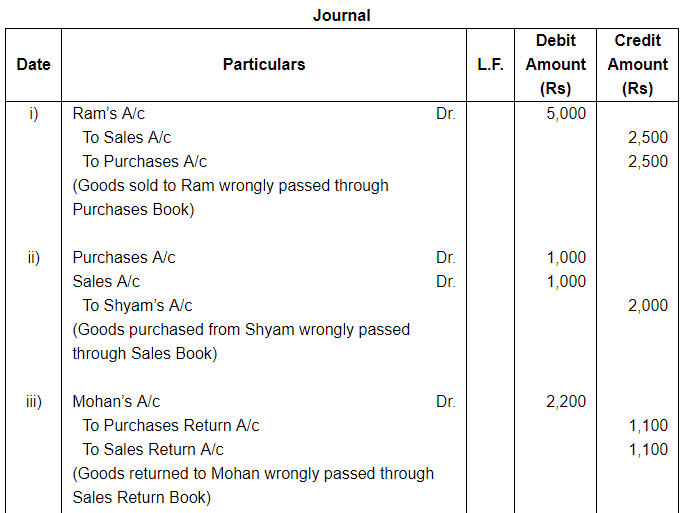

Question 4:

Give rectifying entries for the following:

(i) A credit sales of goods to Ram ₹ 2,500 has been wrongly passed through the 'Purchases Book'.

(ii) A credit purchase of goods from Shyam amounting to ₹ 1,000 has been wrongly passed through the 'Sales Book'.

(iii) A return of goods worth ₹ 1,100 to Mohan was passed through the 'Sales Return Book'.

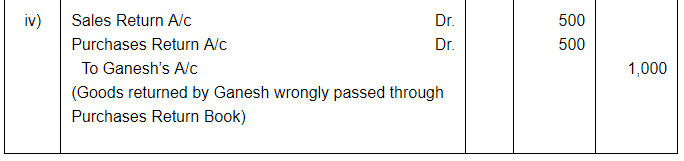

(iv) A return of goods worth ₹ 500 by Ganesh were entered in 'Purchases Return Book'.

ANSWER:

Two Sided Errors

Question 5:

Rectify the following errors:-

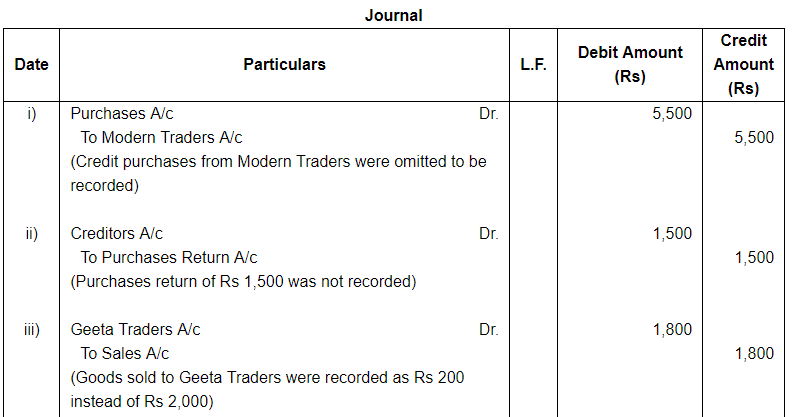

(i) Goods for ₹ 5,500 were purchased from Modern Traders on credit, but no entry has yet been passed.

(ii) Purchase Return for ₹ 1,500 not recorded in the books.

(iii) Goods for ₹ 2,000 sold to 'Geeta Traders' on Credit were entered in the sales book as ₹ 200 only.

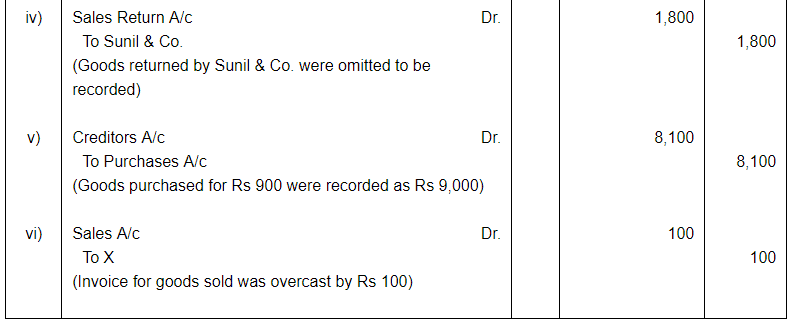

(iv) Goods of the value of ₹ 1,800 returned by Sunil & Co. were included in stock, but no entry was passed in the books.

(v) Goods purchased for ₹ 900, entered in the purchases book as ₹ 9,000.

(vi) An invoice for goods sold to X was overcast by ₹ 100.

ANSWER:

Two Sided Errors

Page No 19.40:

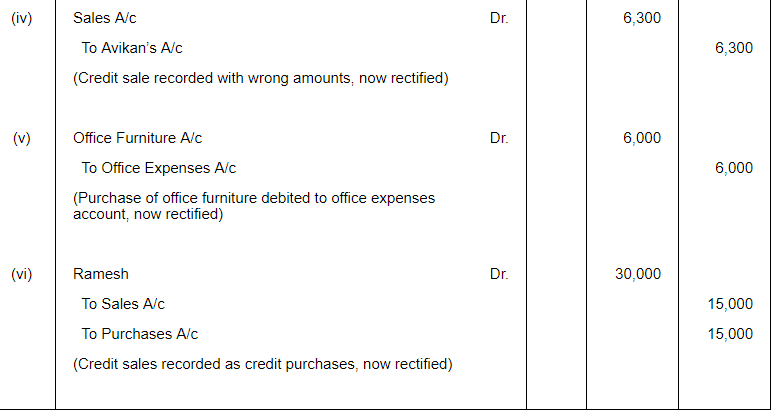

Question 6:

Rectify the following errors:

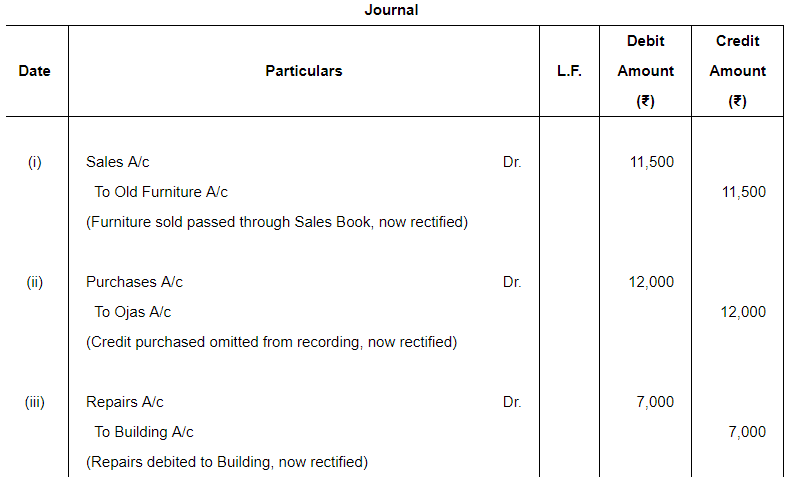

(i) Sold old furniture to A for ₹ 11,500 was passed through the Sales Book.

(ii) Credit purchases of ₹ 12,000 from Ojas omitted to be recorded in the books.

(iii) Repairs made were debited to Building Account ₹ 7,000.

(iv) Credit sale of ₹ 1,800 to Avikan was recorded as ₹ 8,100.

(v) ₹ 6,000 paid for office furniture was debited to office expenses account.

(vi) A credit sale of goods of ₹ 15,000 to Ramesh has been wrongly passed through the purchases Book.

ANSWER:

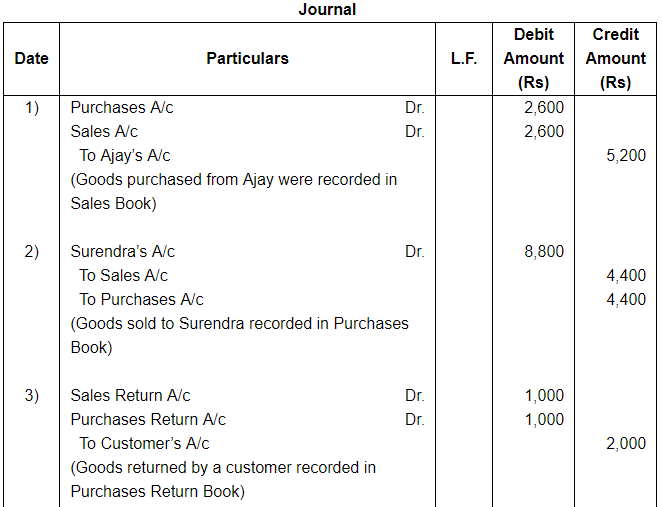

Question 7:

Give Journal Entries to rectify the following errors:-

1. Goods purchased from Ajay for ₹ 2,600 were recorded in Sales Book by mistake.

2. Goods for ₹ 4,400 sold to Surendra was passed through Purchase Book.

3. A customer returned goods worth ₹ 1,000. It was recorded in 'Purchase Return Book'.

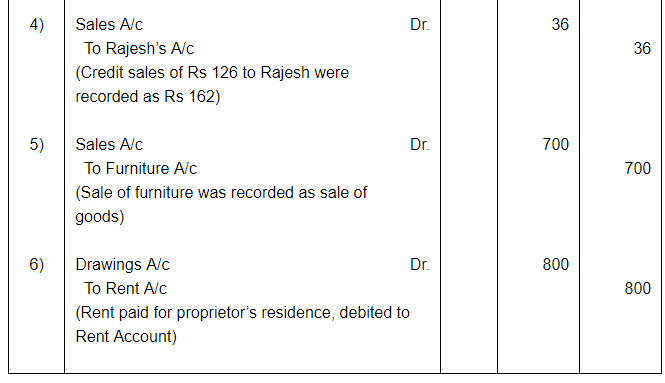

4. A credit sale of ₹ 126 to Rajesh was entered in the books as ₹ 162.

5. Sale of old chairs and Table for ₹ 700 was treated as sale of goods.

6. Rent of proprietor's residence, ₹ 800, debited to Rent A/c.

ANSWER:

Two Sided Errors

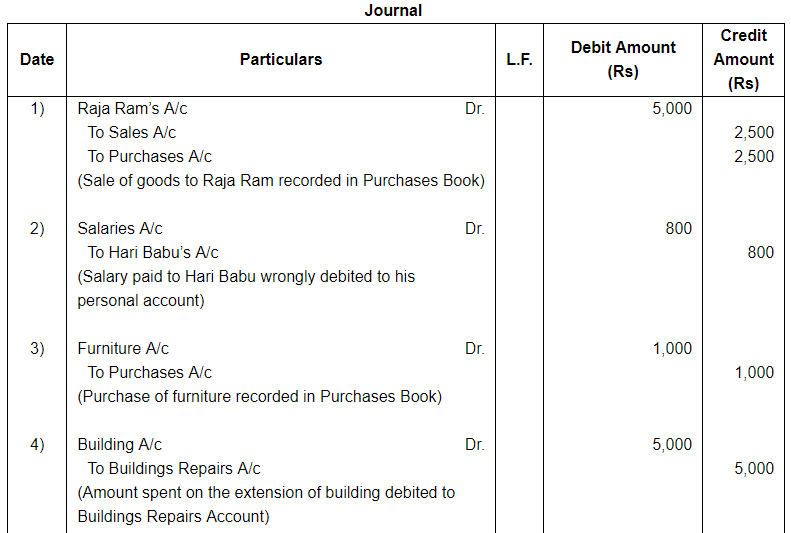

Question 8:

Rectify the following errors:-

1. A sale of goods to Raja Ram for ₹ 2,500 was passed through the Purchases Book.

2. Salary of ₹ 800 paid to Hari Babu was wrongly debited to his personal account.

3. Furniture purchased on credit from Mohan Singh for ₹ 1,000 was entered in the Purchases Book.

4. ₹ 5,000 spent on the extension of buildings was debited to Buildings Repairs Account.

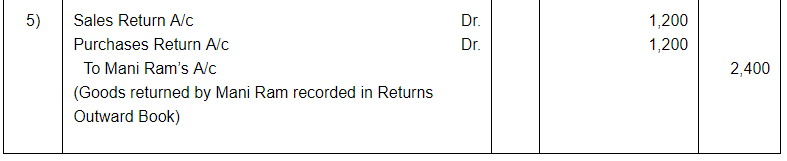

5. Goods returned by Mani Ram ₹ 1,200 were entered in the Returns Outwards Book.

ANSWER:

Two Sided Errors

Question 9:

Rectify the following errors:

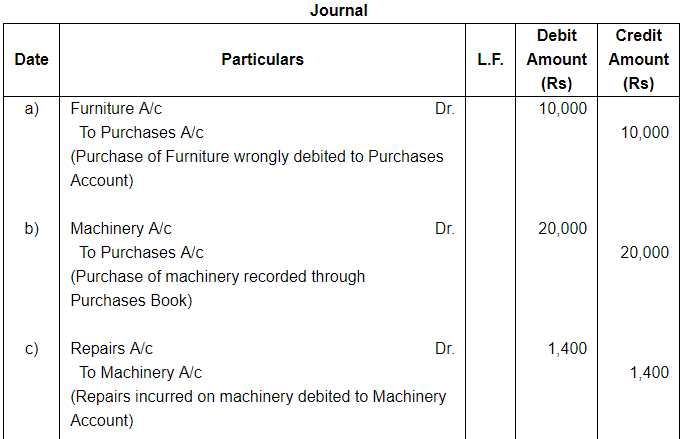

(a) Furniture purchased for ₹ 10,000 wrongly debited to Purchases Account.

(b) Machinery purchased on credit from Raman for ₹ 20,000 was recorded through Purchases Book.

(c) Repairs on machinery ₹ 1,400 debited to Machinery Account.

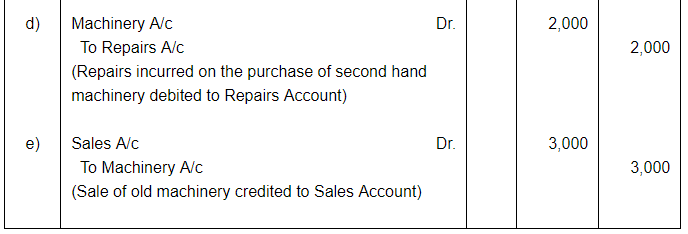

(d) Repairs on overhauling of second hand machinery purchased ₹ 2,000 was debited to Repairs Account.

(e) Sale of old machinery at book value of ₹ 3,000 was credited to Sales Account.

ANSWER:

Two Sided Errors

Page No 19.41:

Question 10:

Pass Journal Entries to rectify the following errors:-

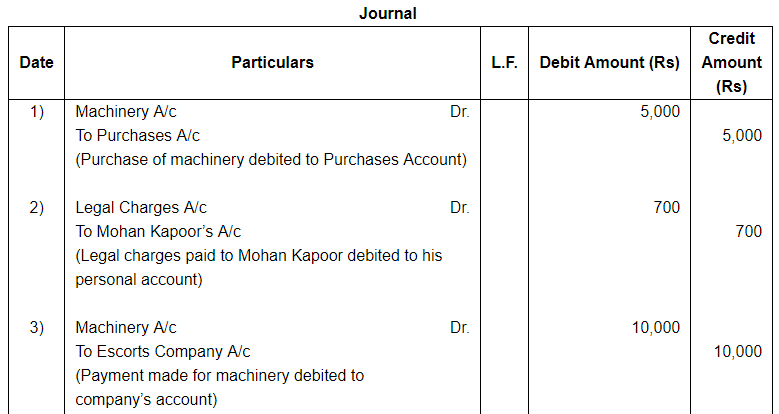

(1) Machinery purchased for ₹ 5,000 has been debited to Purchases A/c.

(2) ₹ 700 paid to Sh. Mohan Kapoor as Legal Charges were debited to his personal account.

(3) ₹ 10,000 paid to Escorts Company for Machinery purchased stand debited to Escorts Company account.

(4) Typewriter purchased for ₹ 6,000 was wrongly passed through purchase book.

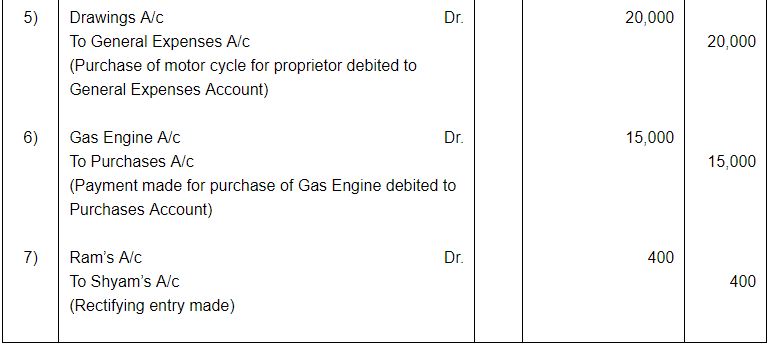

(5) ₹ 20,000 paid for the purchase of a Motor Cycle for proprietor has been charged to 'General Expenses' A/c.

(6) ₹ 15,000 paid for the purchase of 'Gas Engine' were debited to 'Purchases' A/c.

(7) Cash paid to Ram ₹ 400 was debited to the account of Shyam.

ANSWER:

Two Sided Errors

Question 11:

Rectify the following errors:-

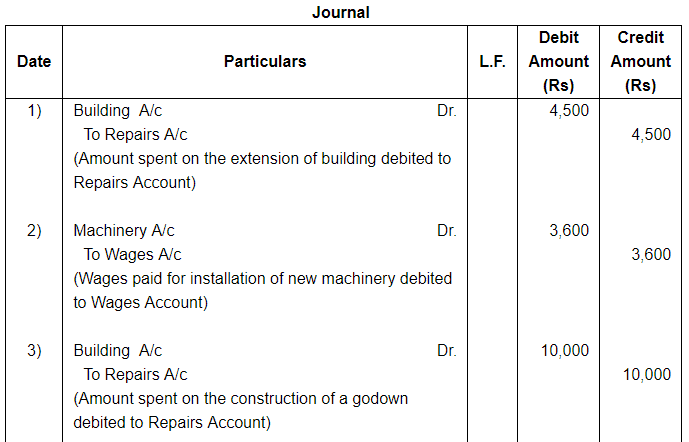

1. ₹ 4,500 spent on the extension of Buildings were debited to Repairs A/c.

2. Wages paid to the firm's own workmen ₹ 3,600 for the installation of a new machinery were posted to Wages Account.

3. Contractor's bill for the construction of a godown at a cost of ₹ 10,000 has been charged to 'Repairs' A/c.

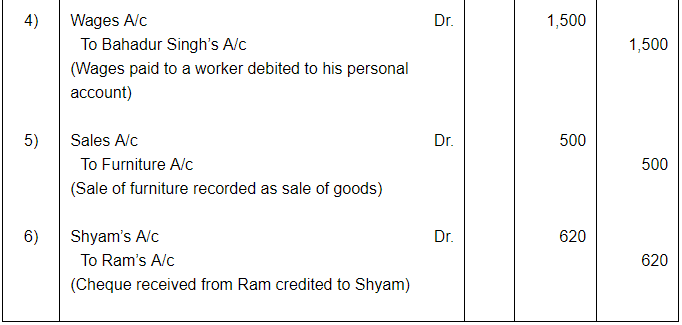

4. ₹ 1,500 paid as Wages to a worker 'Bahadur Singh', has been debited to his personal account.

5. Old furniture sold for ₹ 500 has been credited to Sales Account.

6. A cheque of ₹ 620 received from Ram, has been wrongly credited to Shyam.

ANSWER:

Two Sided Errors

FAQs on Rectification of Errors ( Part - 1) - Commerce

| 1. What is rectification of errors in commerce? |  |

| 2. Why is rectification of errors important in commerce? | |

| 3. What are some common types of errors in commerce that require rectification? | |

| 4. What are the steps involved in the rectification of errors in commerce? | |

| 5. How does rectification of errors affect the financial statements in commerce? | |

Summary

,ppt

,Sample Paper

,video lectures

,Objective type Questions

,Free

,Important questions

,Semester Notes

,Previous Year Questions with Solutions

,Viva Questions

,shortcuts and tricks

,study material

,practice quizzes

,MCQs

,Exam

,past year papers

,Rectification of Errors ( Part - 1) - Commerce

,mock tests for examination

,Rectification of Errors ( Part - 1) - Commerce

,Rectification of Errors ( Part - 1) - Commerce

,Extra Questions

;

Rectification of Errors ( Part - 1) Free PDF Download

Importance of Rectification of Errors ( Part - 1)

Rectification of Errors ( Part - 1) Notes

Rectification of Errors ( Part - 1) Commerce Questions

Study Rectification of Errors ( Part - 1) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!