Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies | Accountancy Class 12 - Commerce PDF Download

Sure Short 20-20 Questions

Q1. A and B are partners. The net divisible profit as per Profit and Loss Appropriation A/c is 2,50,000. The total interest on partner’s drawing is 4,000. A’s salary is 4,000 per quarter and B’s salary is 40,000 per annum. Calculate the net profit/loss earned during the year.

(1)

Sol.

Net Profit during the year = Divisible profits + Salary to partners – Interest on Drawings

= 2,50,000 + 16,000 + 40,000 – 4000 =

3,02,000

Q2. A group of 60 persons want to form a partnership business in India. Can they do so? Give reason in support of your answer.

(1)

Sol.

No, Maximum no. of partners as per The Companies Misc. Rule, 2014 is 50 persons

Q3. Kapoor, Meenakshi and Gauri are partners doing a paper business in Ludhiana. After the accounts of partnership have been drawn up and closed, it was discovered that for the years ending 31st March 2013 and 2014, Interest on capital has been allowed to partners @ 6% p. a. although there is no provision for interest on capital in the partnership deed. Their fixed capitals were 2,00,000; 1,60,000 and 1,20,000

respectively. During the last two years they had shared the profits as under:

Year Ratio

31 March 2013 3 : 2 : 1

31 March 2014 5 : 3 : 2

You are required to give necessary adjusting entry on April 1, 2014. (4)

Sol.

Table Showing Adjustment

20 IMPORTANT QUESTIONS FOR A QUICK REVISION

Q1. Xand Yare partners in a firm. X is to get a commission of 10% of Net Profit before charging any commission. Yis to get a commission of 10% on Net Profit after charging all commissions. Net Profit before charging any commission was Rs. 55,000. Find out the commission of Y.

( Rs 4500)

Q2. At what rate will partners be entitled for remuneration in absence of partnership deed?

(no remuneration will be paid)

3. If the amount of super profit is negative, what does it indicate?

(firm is earning less then the normal profits, hence no goodwill account will be raised)

Q 4. List anyone difference between Profit & Loss Appropriation Account and Profit & Loss Adjustment Account.

( Profit & Loss Appropriation Account records all the expenses and incomes related to the

partners and Profit & Loss Adjustment Account is the revaluation a/c which records the profits

and losses at the time of reconstitution of a partnership firm)

Q5. X, Y and Z who are presently sharing profits & losses in the ratio of 5 : 3 : 2, decide to share future profits & losses in the ratio of 2 : 3 : 5. Give the journal entry to distribute 'Investment Fluctuation Reserve' of Rs.8,000 at the time of change in profit sharing ratio, when Investments (market value 30,000) appear at Rs.40,000.

( IFF a/c dr. 8,000

Revaluation a/c dr. 2,000

To Investments a/c 10,000)

Q6. Ram and Manohar are partners in a firm sharing profits and losses in the ratio of 7 : 3. On 1 st Oct. 2013, Ram granted a loan of Rs.1 ,00,000. According to the partnership deed, Ram was entitled to a rent of Rs. 3,000 per month for the use of his premises by the firm. It is paid to him by cheque at the end of every month. Ram was to be paid salary of Rs. 5,000 per month and Manohar was to get a bonus of Rs. 30,000 per annum.

Interest on capital was to be allowed @ 10% per annum and interest on drawings was to be charged @ 8% per annum. Ram's drawings were Rs. 75,000 and Manohar's drawings were Rs. 50,000. Their fixe capitals were Rs. 4,00,000 and Rs. 1,50,000 respectively. The firm earned a profit of Rs. 2,89,000 before charging any interest for the year ended 31.3.2014. Prepare Profit & Loss Appropriation A/c.

(Divisible profits Rs.1,00,00)

Q7. A, Band C were partners in a firm. On 1.4.2013 their capitals stood at Rs. 50,000, Rs. 25,000 and Rs. 25,000 respectively. As per the provisions of the partnership deed:

(a) C was entitled for a salary of Rs. 1,500 p.m.

(b) Partners were entitled to interest on capital at 5% p.a.

The net profit for the year 2013-2014 of Rs. 45,000 was divided equally without providing for the above terms. Pass an adjusting entry to rectify the above error.

( A’s capital a/c Dr. 1,500

B’s capital a/c Dr. 8,250

To C’s capital a/c 9,750 )

Q8. A and B share profits and losses in the ratio of 2:1. They admit C as partner with 1/4 share in profits with a guarantee that his share of profit shall be at least Rs. 1,00,000. The net loss of the firm for the year ending March 31, 2006 was Rs. 3,20,000. Pass an entry for distribution of profits and guarantee?

Q9 X and Yentered into a partnership business on 1 st April, 2013 and contributed Rs. 80,000 and Rs. 60,000 respectively as their capitals. On 1 st Oct., X granted a loan of Rs. 20,000. The terms of the partnership agreement are as follows:

(a) 20% of Profits before charging Interest on Drawings but after making appropriations to be transferred to General Reserve.

(b) Interest on Capital @ 12% p.a. and Interest on Drawings @ 10% p.a.

(c) X to get a monthly salary of Rs. 2,000 and Y to get salary of Rs. 9,000 per quarter.

(d) X is entitled to a commission of 2% on Sales. Sales for the year were Rs. 3,50,000.

(e) Profits & Losses to beshared in the ratio of their Capital Contribution up to Rs. 70,000 and above Rs 70,000 equally.

The profit for the year ended 31st March, 2014, before providing for any Interest was Rs. 1,84,400. The drawings of X and Y were Rs. 40,000 and Rs. 50,000 respectively.

Pass the journal entries and prepare P & L appropriation a/c

( divisible profits X= 40,000+7250 Y=30,000+4250)

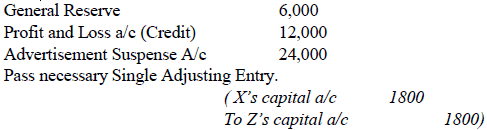

Q10. X and Yare partners in a firm. Their capital accounts as on March 31 , 2015 showed balances of Rs.70,000 and Rs.60,000 respectively .The drawings of X and Y during the year 2014-2015 were Rs.8,000 and Rs.6,000 respectively. After distributing the profits of the year 2014-2015 which amounted to Rs.40,000, it was subsequently found that the following items have been left out while preparing the final accounts of the year ended 31 st March, 2014.

(i) The partners were entitled to Interest on capitals @ 6% p.a.

(ii) The interest on drawings was also to be charged @ 5% p.a.

(ii) X was entitled to salary of Rs.10,000 and Y commission of, Rs. 4,000 for the whole year.

Pass the necessary single Adjusting Entry.

Q11. X, Yand Z are sharing profits and losses in the ratio of 5 : 3 : 2. They decide to share future profits and losses in the ratio of 2 : 3 : 5 with effect from 1st April, 2014. They also decide to record the effect of the following accumulated profits, losses and reserves without affecting their book figures by passing a single entry

Q12. On March 31st, 2014, the balances in the capital accounts of Esha, Manav and Daman after making adjustments for profits and drawings wereRs.3,20,000,Rs.2,40,000 andRs.1,60,000 respectively.

Subsequently, it was discovered that the interest on capital and drawings had been omitted.

• The profit for the year ended on 31st March, 2014 wasRs.90,000.

• During the year, Esha and Manav each withdrew a sum ofRs.48,000 in equal instalments in the middle of every month and Daman withdrewRs.60,000.

• The interest on drawings was to be charged @ 5% p.a. and interest on capital was to be allowed @ 10% p.a.

• The profit sharing ratio of the partners was 3 : 2 : 1.

Showing your workings clearly pass the necessary rectifying entry.

Q13. The average profit earned by a firm is Rs. 95,000 which includes undervaluation of stock of Rs. 10,000 on an average basis. The capital invested in the business is Rs. 9,00,000 and the normal rate of return is 9%. Calculate goodwill of the firm on the basis of 8 times the super profit.

Q14. Kanika and Gautam are partners doing a dry cleaning business in Lucknow, sharing profits in the ratio 2:1 with capitals `5,00,000 and `4,00,000 respectively. Kanika withdrew the following amounts during the year to pay the hostel expenses of her son.

Rs.

1st April 10,000

1st June 9,000

1st Nov. 14,000

1st Dec. 5,000

Gautam withdrew `15,000 on the first day of April, July, October and January to pay rent for the accommodation of his family. He also paid Rs. 20,000 per month as rent for the office of partnership which was in a nearby shopping complex. Calculate interest on Drawings @6% p.a.

Q15. Amit, Babita and Sona form a partnership firm, sharing profits in the ratio of 3 : 2 : 1, subject to the following

(i) Sona’s share in the profits, guaranteed to be not less than Rs. 15,000 in any year.

(ii) Babita gives guarantee to the effect that gross fee earned by her for the firm shall be equal to her average gross fee of the proceeding five years, when she was carrying on profession alone (which is Rs. 25,000). The net profit for the year ended March 31, 2007 is Rs. 75,000. The gross fee earned by Babita for the firm was Rs. 16,000. You are required to show Profit and Loss Appropriation Account.

(Ans : Profit transferred to Capital Accounts of; Amit, Rs. 41,400, Babita,Rs.27,600 and Sona, Rs.15,000)

Q16. Kapoor and Mayank are partners, sharing profits in the ratio of 3 : 2. They employed Anurag as their manager, to whom they paid a salary of Rs. 1500 p.m. Anurag deposited Rs. 40,000 on which interest is payable @ 18% p.a. At the end of 2014 (after the division of profit), it was decided that Anurag should be treated as partner w.e.f. Jan. 1., 2011 with 1/5 th share in profits. His deposit being considered as capital carrying interest @ 12% p.a. like capital of other partners. Firm’s profits after allowing interest on capital were as follows:

(Rs.)

2011 Profit 1,18,000

2012 Profit 1,24,000

2013 Loss (8,000)

2014 Profit 1,56,000

Record the necessary journal entries to give effect to the above.

( Kapoor[dr.] 3312 , mayank [dr.]2208 and Anurag [cr] 5520)

Q17. Ali, Bishnu and Donald are partners in a firm. On 1 st April, 2011 the b in their capital accounts stood at Rs. 8,00,000, Rs. 6,00,000 and Rs.4,00,000 respectively They shared profits in the proportion of 5 : 3 : 2 respectively. Partners are entitled interest on capital @ 5% per annum and salary to Bishnu @ 3,000 per month commission of Rs.12,000 to Donald as per the provisions of the partnership deed.

Ali's share of profit, excluding interest on capital, is guaranteed at no than Rs.25,000 p.a. Bishnu's share of profit, including interest on capital but excluding salary, is guaranteed at not less than Rs. 55,000 p.a. Any deficiency arising on account shall be met by Donald. The profits of the firm for the year ended 31st 2012 amounted to Rs. 2,16,000. Prepare 'Profit and Loss Appropriation Account' for year ended 31 st March 2012 and also highlight the values reftlected here.

(divisible profits ali- 39,000 bishnu- 25000 and Donald 14,000)

Q18. X; Y and Z were in partnership. X and Y sharing profits in the ratio of 2 : 1 and Z receiving a salary of Rs. 1,790 per month plus 5% of the profit a his salary and commission or 1/5 of the profit of the firm whichever is excess of the latter over the former received by Z is, under the partnership borne by X The profit for the year ended 31 st March, 2014 amounted to Rs.1,28,520 after charging Z's salary.

Prepare the Profit and Loss Appropriation Account showing the di profit of the year.

(profit – X 79,200 ; Y – 40,800 ; Z – 30,000)

19. A & B are partners sharing profits and losses in the ratio of 5:3. On 1.4.10 they decided to share profits and losses equally. Pass entries and prepare revaluation a/c from the following considering that the firm do not wants to record the revised values :

a. Value of land & buildings is increased by Rs.50000.

b. Value of furniture is reduced by Rs.12,100

c. Rs.1000 included in creditors are not likely to be claimed and hence should be written back.

d. Unrecorded investments worth Rs.2,000 are to be recorded.

e. There is claim of Rs.900 against the firm which is disputed and needs a provision for the same.

Q20. Calculate the value of goodwill at 3 years' purchase of average profits for past four years. The profits are:

On 1st September 2010, major repair of plant was charged to revenue as Rs.6,000. It is agreed to capitalise it subject to depreciation of 10% p.a. on reducing instalment. The closing stock of 2009 was over-valued by Rs.2,400. To cover partner's remuneration a sum of Rs.4,800 p.a. shall have to be incurred.

(goodwill 60,000)

|

42 videos|168 docs|43 tests

|

FAQs on Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies - Accountancy Class 12 - Commerce

| 1. How are profits and losses distributed among partners in a partnership firm? |  |

| 2. How are profits and losses distributed among shareholders in a company? | |

| 3. How are partnership firms and companies different in terms of ownership? | |

| 4. What are the accounting requirements for partnership firms and companies? | |

| 5. How are partnership firms and companies taxed differently? | |

Semester Notes

,Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies | Accountancy Class 12 - Commerce

,mock tests for examination

,Extra Questions

,Viva Questions

,study material

,Previous Year Questions with Solutions

,Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies | Accountancy Class 12 - Commerce

,Sample Paper

,Important questions

,Exam

,MCQs

,Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies | Accountancy Class 12 - Commerce

,practice quizzes

,shortcuts and tricks

,Objective type Questions

,video lectures

,past year papers

,Summary

,ppt

,Free

;

Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies Free PDF Download

Importance of Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies

Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies Notes

Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies Commerce

Study Sure Short 20-20 Questions - Accounting for Partnership Firms and Companies on the App

|

© EduRev

|

Education Revolution

|

|