ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes - CA Foundation PDF Download

(a) When the bill is made payable on a specific date.(a) When the bill is made payable on a specific date.

1.1BILLS OF EXCHANGE

It is general practice that when goods are sold or services are provided, the seller extends a credit period to buyer. In sometimes, the seller may not be in a position to offer credit period and the purchase is not in a position to pay immediately. In such circumstances the seller would like that the purchaser should give a definite promise in writing to pay the amount of the goods on a certain date which he can use to generate immediate funds. Commercial practice has developed to treat these written promises into valuable instruments of credit that when a written promise is made in proper form and is properly stamped, it is expected that the buyer discharges his debt and the seller receives payment. This is because written promises are often accepted by banks and money is advanced against them. Also they can be endorsed, i.e., passed on from person to person. The written promise is either in the form of a Bill of Exchange or in the form of a promissory note.

A Bill of Exchange has been defined as an “instrument in writing containing an unconditional order signed by the maker directing certain person to pay a certain sum of money only to or to the order of a certain person or to the bearer of the instrument”. When such an order is accepted in writing on the face of the order itself, it becomes a valid bill of exchange. Suppose A orders B to pay ₹50,000 for three months after date and B accepts this order by signing his name, then it will be a bill of exchange.

A Bill of Exchange has the following characteristics:

1. It must be in writing.

2. It must be dated.

3. It must contain an order to pay a certain sum of money.

4. The promise to pay must be unconditional.

5. The money must be payable to a definite person or to his order to the bearer.

6. The draft must be accepted for payment by the party to whom the order is made.

7. It should be properly stamped.

8. Payment must be in legal currency of the country.

The party which makes the order is known as the drawer. The party which accepts the order is known as the acceptor and the party to whom the amount has to be paid is known as the payee. The drawer and the payee can be the same.

A Bill of Exchange can be passed on to another person by endorsement. Endorsement on a bill of exchange is made exactly as it is done in the case of a cheque. The primary liability on a bill of exchange is that of the acceptor. If he does not pay, a holder can recover the amount from any of the previous endorsers or the drawee.

Sometimes, it may happen that a bill of exchange is drawn for foreign trade operations. Such a bill is known as “Foreign Bill of Exchange”. A foreign bill of exchange is one which is drawn in one country and is payable in another. It is generally drawn up in triplicate wherein each copy is sent by separate post so that at least one copy reaches the intended party. Payment will be made only on one of the copies and when such payment is made the other copies become useless. Section 12 of the Negotiable Instruments Act provides that all instruments, which are not inland instrument, are foreign.

A specimen of foreign bill of exchange is given below:

The following are examples of foreign bills:

1. A bill drawn in India on a person resident outside India and made payable outside India. 2. A bill drawn outside India on a person resident outside India.

3. A bill drawn outside India and made payable in India.

4. A bill drawn outside India and made payable outside India.

1.2 PROMISSORY NOTES

A promissory note is an instrument in writing, not being a bank note or currency note

containing an unconditional undertaking signed by the maker to pay a certain sum of money only to or to the order of a certain person. Under Section 31(2) of the Reserve Bank of India Act a promissory note cannot be made payable to bearer.

A promissory note has the following characteristics:

1. It must be in writing.

2. It must contain a clear promise to pay. Mere acknowledgement of a debt is not a promissory note.

3. The promise to pay must be unconditional “I promise to pay ₹50,000 as soon as I can” is not an unconditional promise.

4. The promiser or maker must sign the promissory note.

5. The maker must be a certain person.

6. The payee (the person to whom the payment is promised) must also be certain.

7. The sum payable must be certain. “I promise to pay ₹50,000 plus all fine” is not certain.

8. Payment must be in legal currency of the country.

9. It should not be made payable to the bearer.

10. It should be properly stamped.

11. It does not require any acceptance.

Specimen of promissory note :

1.3 DIFFERENCES - BILL OF EXCHANGE AND PROMISSORY NOTE

1.4 RECORD OF BILLS OF EXCHANGE AND PROMISSORY NOTES

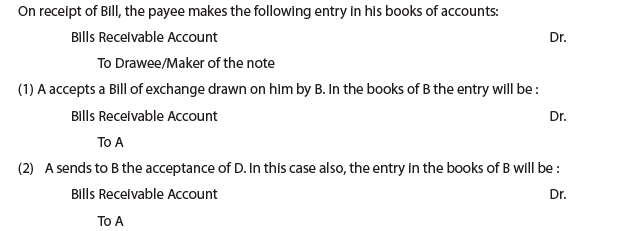

A party which receives a Promissory Note or receives an accepted Bill of Exchange will treat it as a new asset under the name of Bills receivable. A party which issues a Promissory Note or accepts a Bill of Exchange will treat it as new liability under the heading of Bills Payable. We shall first deal with the entries in the books of the party which receives promissory notes or bills. (When we talk of bills, we include promissory notes also).

The person who receives the bill has three options. These are:

(i) He can hold the bill till maturity. (Naturally in this case no further entry is passed until the date of maturity arrives).

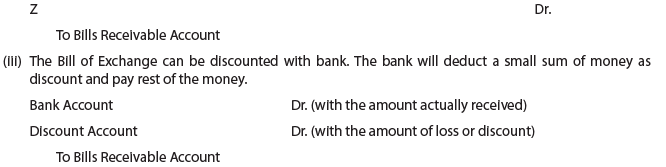

(ii) The bill can be endorsed in favour of another party say Z. In this case, the entry will be to debit the party which now receives the bill and to credit the Bills Receivable Account.

On the date of maturity there will be two possibilities:

(a) The first is that the bill will be paid, that is to say, met or honoured. The entries for this will depend upon what was done to the bill during the period of maturity. If the bill was kept, the cash will be received by the party which originally received the bill. In his books, therefore, the entry will be :

But if he has already endorsed the bill in favour of his creditor or if the bill has been discounted with the bank he will not get the amount; it will be the creditor or the bank which will receive the money. Therefore, in these two cases, no entry will be made in the books of the party which originally received the bill.

(b) The second possibility is that the bill will be dishonoured, that is to say, the bill will not be paid. If the bill is dishonoured, the bill becomes useless and the party from whom the bill was received will be liable to pay the amount (and also the expenses incurred by the party).

Therefore, the following entries will be made :

Thus, it will be seen that in case of dishonour, the party which gave the bill has to be debited (because he has become liable to pay the amount). The credit entry is in Bills Receivable Account (if it was retained) or the Creditor or the bank (if it was endorsed/discounted in their favour).

1.5 TERM OF A BILL

The term of bill of exchange may be of any duration. Usually the term does not exceed 90 days from the date of the bill.

- When a bill is drawn after sight, the term of the bill begins to run from the date of ‘sighting’, i.e., when the bill is accepted.

- When a bill is drawn after date, the term of the bill begins to run from the date of drawing the bill.

1.6 EXPIRY / DUE DATE OF A BILL

The date on which the term of the bill terminates is called as ‘Expiry/Due Date of the bill’.

1.7 DAYS OF GRACE

Every instrument payable otherwise than on demand is entitled to three days of grace.

1.8 DATE OF MATURITY OF BILL

The date which comes after adding three days to the expiry/due date of a bill, is called the date of maturity.

The maturity of a promissory note or bill of exchange is the date at which it falls due. Every promissory note or bill of exchange gets matured on the third day after the day on which it is expressed to be payable, except when it is expressed to be payable:

(i) on demand,

(ii) at sight, or

(iii) on presentment

1.9 BILL AT SIGHT

Bill at Sight means the instruments in which no time for payment is mentioned. A cheque is always payable on demand. A promissory note or bill of exchange is payable on demand–

(a) when no time for payment is specified, or

(b) when it is expressed to be payable on demand, or at sight or on presentment.

Notes:

(i) ‘At sight’ and ‘presentment’ means on demand.

(ii) An instrument payable on demand may be presented for payment at any time.

(iii) Days of grace is not to added to calculate maturity for such types of bill.

1.10 BILL AFTER DATE

Bill after date means the instrument in which time for payment is mentioned. A promissory note or bill of exchange is a time instrument when it is expressed to be payable–

(a) after a specified period.

(b) on a specific day

(c) after sight

(d) on the happening of event which is certain to happen

Notes:

(i) The expression ‘after sight’ means–

(a) in a promissory note, after presentment for sight

(b) in a bill of exchange, after acceptance or noting for non-acceptance or protest for non-acceptance.

(ii) A cheque cannot be a time instrument because the cheque is always payable on demand. Though a cheque can be post dated and which can be presented on or after such date. A cheque has validity of 90 days from its date after that it becomes void, normally termed as ‘Stale Cheque’ as bank will not honour such cheque.

1.11 HOW TO CALCULATE DUE DATE OF A BILL

Note: The term of a Bill after sight commences from the date of acceptance of the bill whereas the term of a Bill after date commences from the date of drawing of bill.

1.12 NOTING CHARGES

It is necessary that the fact of dishonour and the causes of dishonour should be established. If the acceptor can prove that the bill was not properly presented to him for payment, he may escape liability. Therefore, if there is dishonour, or fear of dishonour, the bill will be given to a public official known as “Notary Public”. These officials present the bill for payment and if the money is received, they will hand over the money to the original party. But if the bill is dishonoured they will note the fact of dishonour, with the reasons and give the bill back to their client. For this service they charge a small fee. This fee is known as noting charges. The amount of noting charges is recoverable from the party which is responsible for dishonour.

Suppose X received from Y a bill for ₹1,000. On Maturity the bill is dishonoured and ₹10 is paid as noting charges. The entry in this case will be

1.13 RENEWAL OF BILL

Sometimes the acceptor is unable to pay the amount and he himself moves that he should be given extension of time and in consideration agrees to bear interest for the extended time period (calculated from the date of renewal till the date of expected settlement). In such a case a new bill will be drawn and the old bill will be cancelled. If this happens entries should be passed for cancellation of the old bill. This is done exactly as already explained for dishonour. When the new bill is received entries for the receipt of the bill will be repeated. The amount of the new bill may represent any of the following:

(i) Where the drawee pays nothing: Total of amount of original bill as well as the interest for the extended time period.

(ii) Where the drawee pays the interest amount at the time of renewal: Amount of the Original bill.

(iii) Where the drawee makes part payment of the original bill or interest amount or both: That part of total of amount of original bill as well as the interest for the extended time period on unpaid amount.

1.14 RETIREMENT OF BILLS OF EXCHANGE & REBATE

We have seen that renewal of a bill of exchange is made when a person does not have sufficient fund to pay for the bill of exchange on the due date and he requires a further period of credit. Many a time instances do arise when the acceptor has spare funds much before the maturity date of the bill of exchange accepted by him. In such circumstances he approaches the payee of the bill of exchange and asks him whether the payee is prepared to accept cash before the maturity date. In such cases the acceptor gets a certain rebate or interest or discount for premature payment. The rebate becomes the income of the acceptor and expense of the payee. It is a consideration of premature payment.

ILLUSTRATION 1

Vijay sold goods to Pritam on 1st September, 2016 for ₹1,06,000. Pritam immediately accepted a three months bill. On due date Pritam requested that the bill be renewed for a fresh period of two months. Vijay agrees provided interest at 9% was paid immediately in cash. To this Pritam was agreeable. The second bill was met on due date. Give Journal entries in the books of Vijay and Pritam.

SOLUTION

ILLUSTRATION 2

On 1st January, 2016, Ankita sells goods for ₹5,00,000 to Bhavika and draws a bill at three months for the amount. Bhavika accepts it and returns it to Ankita. On 1st March, 2016, Bhavika retires her acceptance under rebate of 12% per annum. Record these transactions in the journals of Ankita and Bhavika.

SOLUTION

ILLUSTRATION 3

Journalise the following transactions in K. Katrak’s books.

(i) Katrak’s acceptance to Basu for ₹2,500 discharged by a cash payment of ₹1,000 and a new bill for the balance plus ₹50 for interest.

(ii) G. Gupta’s acceptance for ₹4,000 which was endorsed by Katrak to M. Mehta was dishonoured. Mehta paid ₹20 noting charges. Bill withdrawn against cheque.

(iii) D. Dalal retires a bill for ₹2,000 drawn on him by Katrak for ₹10 discount.

(iv) Katrak’s acceptance to Patel for ₹5,000 discharged by Patel. Mody’s acceptance to Katrak for a similar amount.

SOLUTION

ILLUSTRATION 4

On 1st January, 2016, Vilas draws a bill of exchange for ₹10,000 due for payment after 3 months on Eknath. Eknath accepts to this bill of exchange. On 4th March, 2016 Eknath retires the bill of exchange at a discount of 12% p.a. You are asked to show the journal entries in the books of Eknath.

SOLUTION

ILLUSTRATION 5

On 1st January, 2016, Vilas draws a Bill of Exchange for `10,000 due for payment after 3 months on Eknath. Eknath accepts to this bill of exchange. On 4th March, 2016. Eknath retires the bill of exchange at a discount of 12% p.a. You are asked to show the journal entries in the books of Vilas.

SOLUTION

1.15 INSOLVENCY

Insolvency of a person means that he is unable to pay his liabilities. This means that bills accepted by him will be dishonoured. Therefore, when it is known that a person has become insolvent, entry for dishonour of his acceptance must be passed. Later on, something may be received from his estate. When and if an amount is received, cash account will be debited and the personal account of the debtor will be credited. The remaining amount will be irrecoverable and, therefore, should be written off as bad debt. The students should be careful to calculate the amount actually received from an insolvent’s estate and amount to be written off only after preparing his account.

In the books of drawee of the bill, the amount not ultimately paid by him due to insolvency, should be credited to Defciency Account.

ILLUSTRATION 6

Mr. David draws two bills of exchange on 1.1.2016 for ₹6,000 and ₹10,000. The bills of exchange for ₹6,000 is for two months while the bill of exchange for ₹10,000 is for three months. These bills are accepted by Mr. Thomas. On 4.3.2016, Mr. Thomas requests Mr. David to renew the first bill with interest at 18% p.a. for a period of two months. Mr. David agrees to this proposal. On 20.3.2016, Mr. Thomas retires the acceptance for ₹10,000, the interest rebate i.e. discount being ₹100. Before the due date of the renewed bill, Mr. Thomas becomes insolvent and only 50 paise in a rupee could be recovered from his estate.

You are to give the journal entries in the books of Mr. David.

SOLUTION

ILLUSTRATION 7

Rita owed ₹1,00,000 to Siriman. On 1st October, 2016, Rita accepted a bill drawn by Siriman for the amount at 3 months. Siriman got the bill discounted with his bank for ₹99,000 on 3rd October, 2016. Before the due date, Rita approached Siriman for renewal of the bill. Siriman agreed on the conditions that ₹50,000 be paid immediately together with interest on the remaining amount at 12% per annum for 3 months and for the balance, Rita should accept a new bill at three months. These arrangements were carried out. But afterwards, Rita became insolvent and 40% of the amount could be recovered from his estate.

Pass journal entries (with narration) in the books of Siriman.

SOLUTION

1.16 ACCOMMODATION BILLS

Bills of Exchange are usually drawn to facilitate trade transmission, that is, bills are meant to finance actual purchase and sale of goods. But the mechanism of bill can be utilised to raise finance also. Suppose Boss needs finance for three months. In that case he may persuade his friend Kapoor to accept his draft. The bill of exchange may then be taken by Boss to his bank and get it discounted there. Thus, Boss will be able to make use of funds. When the three months period expires, Boss will send the requisite amount to Kapoor and Kapoor will meet the bill. Thus, Boss is able to raise money for his use. If both Boss and Kapoor need money, the same devise can be used. Either Boss accepts a bill of exchange or Kapoor does. In either case, the bill will be discounted with the bank and the proceeds divided between the two parties according to mutual agreement. The discounting charges must also be borne by the two parties in the same ratio in which the proceeds are divided. On the due date the acceptor will receive from the other party his share. The bill will then be met. When bills are used for such a purpose, they are known as accommodation bills.

However, it may so happen that the drawer is not able to remit the proceeds to drawee on the due date. In such a case, the drawee may draw a bill on the drawer, and get it discounted with the bank to honour the first bill. If the new drawer (drawee of the first bill) also remits some proceeds of the new bill to new drawee (drawer of the first bill), then the proportion of discount to be borne by the new drawee will be based upon the proceeds remitted as well as the benefit obtained by him on the first bill (i.e., by not paying the amount due to the original drawee on due date).

Entries are passed in the books of two parties exactly in the way already pointed out for ordinary bills. The only additional entry to be passed is for sending the remittance for one party to the other party and also debiting the other party with the shared amount of discount.

ILLUSTRATION 8

On 1st July, 2016 Gorge drew a bill for ₹1,80,000 for 3 months on Harry for mutual accommodation. Harry accepted the bill of exchange. Gorge had purchased goods worth ₹1,81,000 from Jack on the same date. Gorge endorsed Harry’s acceptance to Jack in full settlement. On 1st September, 2016, Jack purchased goods worth ₹1,90,000 from Harry. Jack endorsed the bill of exchange received from Gorge to Harry and paid ₹ 9,000 in full settlement of the amount due to Harry. On 1st October, 2016, Harry purchased goods worth ₹2,00,000 from Gorge. Harry paid the amount due to Gorge by cheque. Give the necessary Journal Entries in the books of Harry and Gorge.

SOLUTION

ILLUSTRATION 9

For the mutual accommodation of ‘X’ and ‘Y’ on 1st April, 2016, ‘X’ drew a four months’ bill on ‘Y’ for ₹4,000. ‘Y’ returned the bill after acceptance of the same date. ‘X’ discounts the bill from his bankers @ 6% per annum and remit 50% of the proceeds to ‘Y’. On due date ‘X’ is unable to send the amount due and therefore ‘Y’ draws a bill for ₹7,000, which is duly accepted by ‘X’. ‘Y’ discounts the bill for ₹6,600 and sends ₹1,300 to ‘X’. Before the bill is due for payment ‘X’ becomes insolvent. Later 25 paise in a rupee received from his estate.

Record Journal entries in the books of ‘X’.

SOLUTION

ILLUSTRATION 10

Anil draws a bill for ₹9,000 on Sanjay on 5th April, 2016 for 3 months, which Sanjay returns it to Anil afteraccepting the same. Anil gets it discounted with the bank for ₹ 8,820 on 8th April, 2016 and remits one-third amount to Sanjay. On the due date Anil fails to remit the amount due to Sanjay, but he accepts a bill for ₹12,600 for three months, which Sanjay discounts it for ₹ 12,330 and remits ₹ 2,220 to Anil. Before the maturity of the

renewed bill Anil becomes insolvent and only 50% was realized from his estate on 15th October, 2016.

Pass necessary Journal entries for the above transactions in the books of Anil.

SOLUTION ]

]

1.17 BILLS OF COLLECTION

When a person receives a bill of exchange, he may decide to retain the bill till the date of maturity. But inorder to ensure safety, he may send it to bank with instructions that the bill should be retained till maturityand should be realised on that date. This does not mean discounting because the bank will not credit the client until the amount is actually realised. If the bill is sent to the bank with such instructions it is known as

“Bill sent for collection”.

1.18 BILLS RECEIVABLE AND BILLS PAYABLE BOOKS

Bills receivable and bills payable books are journals (Day Books) to record in chronological order the details of bills receivable and bills payable. When large number of bill transactions take place in an organization, it is convenient to maintain these books. Wherein any bill transaction takes place, the same is entered in the Day Books in the first

instance. Postings to individual Debtors or Creditors accounts are made from the Day

Books. Also totals of bills received or accepted are posted periodically to Bills Receivable Account and Bills Payable Account respectively.

Bills receivable book and bills payable book are very useful for following up the status of outstanding bills. When there are large number of bills and these bills fall due on different dates, some of these bills may not be honoured on maturity due to varied reasons. It is possible from these Day Books to trace the details of the outstanding bills and to identify the reasons for not honouring the bills. Given below are forms of Day Books for both bills receivable and bills payable

FAQs on ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes - CA Foundation

| 1. What is a bill of exchange? |  |

| 2. What is a promissory note? | |

| 3. What are the key differences between a bill of exchange and a promissory note? | |

| 4. What are the essential elements of a bill of exchange? | |

| 5. What are the legal requirements for a promissory note to be valid? | |

|

5.2K Views |

|

4.76/5 Rating |

|

Dec 25, 2024 Last updated |

|

Explore Courses for CA Foundation exam

|

|

ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes - CA Foundation

,Previous Year Questions with Solutions

,practice quizzes

,study material

,Summary

,Viva Questions

,Objective type Questions

,Important questions

,Sample Paper

,Exam

,Free

,mock tests for examination

,shortcuts and tricks

,MCQs

,video lectures

,Semester Notes

,ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes - CA Foundation

,past year papers

,ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes - CA Foundation

,ppt

,Extra Questions

;

ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes Free PDF Download

Importance of ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes

ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes

ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes CA Foundation Questions

Study ICAI Notes- Unit 1: Bill Of Exchange and Promissory Notes on the App

|

© EduRev

|

Education Revolution

|

|