SUMMARY:-

- Non-manufacturing entities are the trading entities, which are engaged in the purchase and sale of goods at profit without changing the form of the goods.

- For accounting, profit is measured at two levels: (a) Gross Profit (b) Net Profit

- The principal function of final statements of account (Trading Account, Profit and Loss Account and the Balance Sheet) is to exhibit truly and fairly the profitability and the financial position of the business to which they relate. In order that these may be properly drawn up, it is essential that a proper record of transactions entered into by the business during a particular accounting period should be maintained.

- At the end of the year, it is necessary to ascertain the net profit or the net loss. For this purpose, it is first necessary to know the gross profit or gross loss. Gross Profit is the difference between the selling price and the cost of the goods sold. For a trading firm, the cost of goods sold can be ascertained by adjusting the cost of goods still on hand at the end of the year against the purchases.

TEST YOUR KNOWLEDGE:-

Multiple Choice Questions:-

Ques 1: A debit to an account may

(a) increase expense

(b) decrease an asset.

(c) increase a liability.

(d) increase income.

Ans: (a)

Ques 2: Prepayment of insurance premium will appear in the Balance Sheet and in the Insurance Account respectively as:

(a) a liability and a debit balance.

(b) an asset and a debit balance.

(c) an asset and a credit balance.

(d) a liability and a credit balance.

Ans: (c)

Ques 3: Gross profit is the difference between:

(a) sales and purchases

(b) sales and cost of sales.

(c) sales and total expenses.

(d) Sales and total liabilities.

Ans: (b)

Ques 4: Payment made to a creditor subject to cash discount will :

(a) reduce a liability, reduce an asset and add to expenses.

(b) reduce a liability, add to an asset, and add to revenue.

(c) reduce an asset, reduce a liability, and add to revenue.

(d) reduce a liability, reduce an asset and decrease expenses.

Ans: (c)

Ques 5: A customer returns goods already charged to him. We should:

(a) debit his account.

(b) credit his account.

(c) make no entry on his account.

(d) None of the above.

Ans: (b)

Ques 6: Capital is the difference between

(a) Income and expenses

(b) Sales and Cost of goods sold

(c) Assets and liabilities

(d) None of the above.

Ans: (c)

Ques 7: The capital of a sole trader would change as a result of:

(a) A creditor being paid his account by cheque.

(b) Raw materials being purchased on credit.

(c) Fixed assets being purchased on credit.

(d) Wages being paid in cash.

Ans: (d)

Ques 8: A decrease in the provision for doubtful debts would result in:

(a) An increase in liabilities.

(b) A decrease in working capital.

(c) An increase in net profit.

(d) None of the three.

Ans: (c)

Ques 9: A Company wishes to earn a 20% profit margin on selling price. Which of the following is the profit mark up on cost, which will achieve the required profit margin?

(a) 33%

(b) 25%

(c) 20%

(d) 30%

Ans: (b)

Ques 10: If sales is ₹2,000 and the rate of gross profit on cost of goods sold is 25%, then the cost of goods sold will be

(a) ₹2,000.

(b) ₹1,500.

(c) ₹1,600.

(d) ₹1,000.

Ans: (c)

Ques 11: Sales for the year ended 31st March, 2016 amounted to ₹10,00,000. Sales included goods sold to Mr. A for ₹50,000 at a profit of 20% on cost. Such goods are still lying in the godown at the buyer’s risk. Therefore, such goods should be treated as part of

(a) Sales.

(b) Closing Inventory.

(c) Goods in transit.

(d) None of the above.

Ans: (a)

Ques 12: If sales revenues are ₹4,00,000; cost of goods sold is ₹3,10,000 and expenses are ₹60,000, the gross profit is

(a) ₹30,000.

(b) ₹90,000.

(c) ₹3,40,000.

(d) ₹4,00,000.

Ans: (b)

Theory questions:-

Ques 1: Write shorts notes on:

(a) Balance sheet.

(b) Trading account

(c) Closing entries

Ans: (a) The balance sheet may be defined as “a statement which sets out the assets and liabilities of a firm or an institution as at a certain date.” Since even a single transaction will make a difierence to some of the assets or liabilities, the balance sheet is true only at a particular point of time. That is the significance of the word “as at.”

(b) At the end of the year, it is necessary to ascertain the net profit or the net loss. For this purpose, it is first necessary to know the gross profit or gross loss with the helps to Trading A/c. Gross Profit is the difference between the selling price and the cost of the goods sold.

(c) Closing entries: The entries that have to be made in the journal for preparing the Trading and the Profit and Loss Account that is for transferring the various accounts to these two accounts are known as closing entries.

Ques 2: Distinguish between Provision and reserve fund.

Ans: Provision means “any amount written off or retained by way of providing for depreciation, renewal or diminution in the value of assets or retained by way of providing for any known liability of which the amount cannot be determined with substantial accuracy”.

Reserve Fund: It signifies the amount standing to the credit of the reserve that is invested outside the business in securities which are readily realisable e.g., when the amounts set apart for replacement of an asset are invested periodically, in government securities or shares. The account to which these amounts are annually credited is described as the Reserve Fund.

Practical questions:-

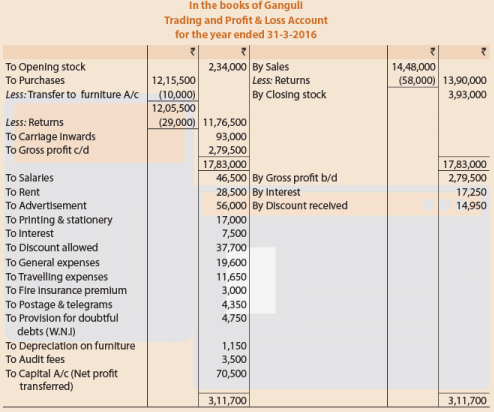

Ques 1: From the following particulars extracted from the books of Ganguli, prepare trading and profit and loss account and balance sheet as at 31st March, 2016 after making the necessary adjustments:

Adjustments:

(1) Value of stock as on 31st March, 2016 is ₹3,93,000. This includes goods returned by customers on 31st March, 2016 to the value of ₹15,000 for which no entry has been passed in the books.

(2) Purchases include furniture purchased on 1st January, 2016 for ₹10,000.

(3) Depreciation should be provided on furniture at 10% per annum.

(4) The loan account from Dena bank in the books of Ganguli appears as follows:

(5) Sundry debtors include ₹20,000 due from Robert and sundry creditors include ₹10,000 due to him.

(6) Interest paid include ₹3,000 paid to Dena bank.

(7) Interest received represents ₹1,000 from the sundry debtors and the balance on investments and deposits.

(8) Provide for interest payable to Dena bank and for interest receivable on investments and deposits.

(9) Make provision for doubtful debts at 5% on the balance under sundry debtors. No such provision need to be made for the deposits.

Ans:

Ques 2: Sengupta & Co. employs a team of eight workers who were paid ₹30,000 per month each in the year ending 31st December, 2015. At the start of 2016, the company raised salaries by 10% to ₹33,000 per month each.

On July 1, 2016 the company hired two trainees at salary of ₹21,000 per month each. The work force are paid salary on the first working day of every month, one month in arrears, so that the employees receive their salary for January on the first working day of February etc.

You are required to calculate:

(i) Amount of salaries which would be charged to the profit and loss for the year ended 31st December, 2016.

(ii) Amount actually paid as salaries during 2016

(iii) Outstanding Salaries as on 31st December, 2016.

Ans:

Ques 3: You are required, prepare a Trading and Profit and Loss Account for the year ending 31st March, 2016 and a Balance Sheet as on that date from the Trial Balance given below:

On 31st March, 2016 the Inventory was valued at ₹10,00,000.

Ans:

Ques 4: Mr. Kotriwal is engaged in business of selling magazines. Several of his customers pay money in advance for subscribing his magazines. Information related to year ended 31st March 2017 has been given below:

On 1.4.2016 he had a balance of ₹2,00,000 advance from customers of which ₹1,50,000 is related to year 2016-17 while remaining pertains to year 2017-18. During the year 2016-17 he made cash sales of ₹5,00,000. You are required to compute:

i) Total income for the year 2016-17.

ii) Total money received during the year if the closing balance in advance from customers account is ₹,70,000.

Ans:

Ques 5: Mr. Birla is a proprietor engaged in business of trading electronics. An excerpt from his Trading & P&L account is as follows:

Commission is charged at the rate of 10%.

Selling Expenses amount to 1% of total sales.

You are required to compute the missing figures.

Ans:

Commission is charged at the rate of 10%.

Commission is charged at the rate of 10%.