Worksheet: Market Equilibrium- 1 | Economics Class 11 - Commerce PDF Download

| Table of contents |

|

| Multiple Choice Questions |

|

| Match the Following |

|

| True or False |

|

| Very Short Answers |

|

| Short Answers |

|

Multiple Choice Questions

Q1: What is the primary factor that determines market equilibrium?

(a) Demand only

(b) Supply only

(c) Both Demand and Supply

(d) Government regulations

Q2: Which of the following situations would lead to an increase in market equilibrium price?

(a) Increase in demand and decrease in supply

(b) Decrease in demand and increase in supply

(c) Increase in both demand and supply

(d) Decrease in both demand and supply

Q3: When market price is above the equilibrium price, what is likely to happen in the market?

(a) Surplus

(b) Shortage

(c) Equilibrium

(d) Stability

Q4: What happens to market equilibrium when there is a decrease in consumer preferences for a specific product?

(a) Equilibrium price increases

(b) Equilibrium quantity increases

(c) Equilibrium price and quantity decrease

(d) Equilibrium remains unchanged

Q5: Which of the following is a determinant of market demand?

(a) Production costs

(b) Consumer income

(c) Number of firms in the market

(d) Government policies

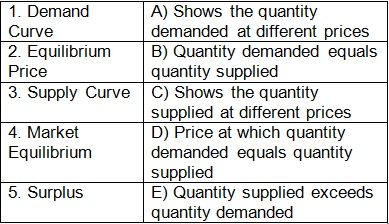

Match the Following

Q1: Match the Following

True or False

Q1: Market equilibrium is always stable.

Q2: Changes in consumer preferences do not affect market equilibrium.

Q3: Surplus occurs when quantity demanded exceeds quantity supplied.

Q4: Demand curve shows the relationship between price and quantity demanded.

Q5: Equilibrium price can be affected by changes in both demand and supply.

Very Short Answers

Q1: Explain the concept of market equilibrium.

Q2: What factors can cause a shift in the demand curve?

Q3: Define surplus and its impact on the market.

Q4: How does market equilibrium change when both demand and supply increase?

Q5: Explain the concept of a supply curve.

Short Answers

Q1: Discuss the factors that can lead to a shift in the supply curve.

Q2: Analyze the impact of government policies on market equilibrium.

Q3: Explain the concept of elasticity of demand and its relevance to market equilibrium.

Q4: Describe the role of consumer preferences in determining market equilibrium.

Q5: Discuss the impact of technological advancements on market equilibrium.

You can access the solutions to this worksheet here.

|

59 videos|222 docs|43 tests

|

FAQs on Worksheet: Market Equilibrium- 1 - Economics Class 11 - Commerce

| 1. What is market equilibrium? |  |

| 2. How does market equilibrium affect prices? | |

| 3. What factors can shift the market equilibrium? | |

| 4. Why is understanding market equilibrium important for businesses? | |

| 5. What happens when there is a surplus or shortage in the market? | |

Exam

,Extra Questions

,Free

,practice quizzes

,ppt

,Sample Paper

,shortcuts and tricks

,Viva Questions

,Worksheet: Market Equilibrium- 1 | Economics Class 11 - Commerce

,Summary

,Worksheet: Market Equilibrium- 1 | Economics Class 11 - Commerce

,study material

,past year papers

,Objective type Questions

,Semester Notes

,video lectures

,Worksheet: Market Equilibrium- 1 | Economics Class 11 - Commerce

,Important questions

,mock tests for examination

,MCQs

,Previous Year Questions with Solutions

;

Worksheet: Market Equilibrium- 1 Free PDF Download

Importance of Worksheet: Market Equilibrium- 1

Worksheet: Market Equilibrium- 1 Notes

Worksheet: Market Equilibrium- 1 Commerce Questions

Study Worksheet: Market Equilibrium- 1 on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!