Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner | Accountancy Class 12 - Commerce PDF Download

MCQ Questions

Q1: A, B, C, and D are partners. A and B share 2/3rd of profits equally and C and D share remaining profits in the ratio of 3:2. Find the profit sharing ratio of A/ B, C and D.

(a) 5:5:3:2

(b) 7:7:6:4

(c) 2.5:2.5:8:6

(d) 3:9:8:3

Ans: (a)

Q2: X and Y are partners in a firm with capital of Rs.180000 and Rs.200000. Z was admitted for 1/3rd share in profits and brings Rs.340000 as capital. Calculate the amount of goodwill

(a) 240000

(b) 100000

(c) 150000

(d) 300000

Ans: (d)

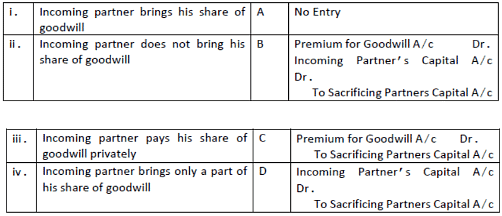

Q3: Match the following with respect to journal entries for treatment of goodwill.

(a) i- B, ii-C, iii-A, iv-D

(b) i- C, ii-D, iii-A, iv-B

(c) i- D, ii-C, iii-A, iv-B

(d) i- D, ii-C, iii-B, iv-A

Ans: (b)

Q4: General reserve at the time of admission of a partner is transferred to:

(a) Revaluation a/c

(b) Partners’ capital a/c

(c) Neither of two

(d) Profit and loss a/c

Ans: (b)

Q5: A and B are partners sharing profits and losses in the ratio of 5:3. On admission, C brings Rs.70000 as capital and Rs.43000 against goodwill. New profit ratio between A, B and C is 7:5:4. The sacrificing ratio of A and B is:

(a) 3:1

(b) 1:3

(c) 4:5

(d) 5:9

Ans: (a)

Q6: At the time of admission of a new partner, the balance of Workmen Compensation Reserve will be transferred to:

(a) Old partners in the old profit sharing ratio

(b) Sacrificing partners in the sacrificing ratio

(c) Revaluation Account

(d) All partners in the new profit sharing ratio

Ans: (a)

Q7: On the admission of a new partner:

(a) Old partnership is dissolved

(b) Both old partnership and firm are dissolved

(c) Old firm is dissolved

(d) None of the above

Ans: (a)

Q8: If at the of admission, some balance of profit and loss account appears in the books, it will be transferred to :

(a) Profit and loss adjustment account

(b) All partners’ capital account

(c) Old partners’ capital account

(d) Revaluation account

Ans: (c)

Q9: Premium brought by newly admitted partner should be:

(a) Credited to sacrificing partners

(b) Credited to all partners in the new profit sharing ratio

(c) Credited to old partners in the old profit sharing ratio

(d) Credited to only gaining partners

Ans: (a)

Q10: When a new partner brings his share of goodwill in cash, the amount is debited to:

(a) Cash account

(b) Capital accounts of the new partner

(c) Goodwill account

(d) Capital accounts of the old partner

Ans: (a)

Q11: The balance in the investment fluctuation fund after meeting the fall in book value of investment, at the time of admission of partner will be transferred to:

(a) Revaluation account

(b) Capital accounts of old partners

(c) General reserve

(d) Capital account of all partners

Ans: (b)

Q12: The proportion in which old partners make a sacrifice:

(a) Ratio of capital

(b) Ratio of sacrifice

(c) Gaining ratio

(d) Profit sharing ratio

Ans: (b)

Q13: If the new partner brings his share of goodwill in cash, it will be shared by old partners in:

(a) Sacrificing ratio

(b) Old profit sharing ratio

(c) New ratio

(d) Capital ratio

Ans: (a)

Q14: Which of the following is not the reconstitution of partnership?

(a) Admission of a partner

(b) Dissolution of Partnership

(c) Change in Profit Sharing Ratio

(d) Retirement of a partner

Ans: (b)

Q15: New partner may be admitted to partnership:

(a) With the consent of all the old partners

(b) With the consent of any one partner

(c) With the consent of 2/3rd of the old partners

(d) With the consent of 3/4th of the old partners

Ans: (a)

Q16: A, and B are partners sharing profits in the ratio of 2:3. Their balance sheet shows machinery at ₹2,00,000; stock ₹80,000, and debtors at ₹1,60,000. C is admitted and the new profit sharing ratio is 6:9:5. Machinery is revalued at ₹1,40,000 and a provision is made for doubtful debts @5%. A’s share in loss on revaluation amount to ₹20,000. Revalued value of stock will be:

(a) ₹62,000

(b) ₹1,00,000

(c) ₹60,000

(d) ₹98,000

Ans: (c)

Q17: Yash and Manan are partners sharing profits in the ratio of2:1. They admit Kushagra into partnership for 25% share of profit. Kushagra acquired the share from old partners in the ratio of 3:2. The new profit sharing ratio will be:

(a) 14:31:15

(b) 3:2:1

(c) 31:14:15

(d) 2:3:1

Ans: (c)

Q18: When goodwill is not recorded in the books at all on admission of a partner:

(a) If paid privately

(b) If brought in cash

(c) If not brought in cash

(d) If brought in kind

Ans: (a)

Q19: At the time of admission of a new partner, the entry for unrecorded investment will be:

(a) Dr. Investment A/c and Cr. Revaluation A/c

(b) Dr. Partners’ Capital A/c and Cr. Investment A/c

(c) Dr. Revaluation A/c and Cr. Investment A/c

(d) None of the above

Ans: (a)

Q20: Heena and Sudha share Profit & Loss equally. Their capitals were Rs.1,20,000 and Rs. 80,000 respectively. There was also a balance of Rs. 60,000 in General reserve and revaluation gain amounted to Rs. 15,000. They admit friend Teena with 1/5 share. Teena brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm.

(a) Rs.85,000

(b) Rs.1,00,000

(c) Rs.20,000

(d) None of the above

Ans: (a)

True Or False

Q1: “Unless agreed otherwise, Sacrificing Ratio of the old partners will be the same as their Old Profit Sharing Ratio”.

Ans: True

Q2: Hidden goodwill arises when total capital is computed based on the new partner’s capital is less than total capitals of remaining partners after all adjustments.

Ans: False

Q3: New partner may or may not contribute capital at the time of admission.

Ans: True

Q4: New partner may bring his share of goodwill premium in kind.

Ans: True

Q5: Employee Provident Fund is a part of Accumulated profits and reserves.

Ans: False

Q6: The need for valuation of goodwill also arises when the firm is dissolved involving sale of business as a going concern.

Ans: True

Q7: New partner brings goodwill in the firm to get share in the past profits.

Ans: False

Q8: At the time of admission, reserves may be carried forwarded by the partners.

Ans: True

Q9: “As per Section 26 of the Indian Partnership Act, 1932, a person can be admitted as a new partner if it is agreed in the Partnership Deed”.

Ans: False

Q10: Claim of workmen compensation if more than workmen compensation reserve, is debited to revaluation account.

Ans: True

Fill in the blanks

Q1: In case of upward revaluation of a liability, revaluation account is____

Ans: Debited

Q2: A and B are partners sharing profits equally. They admit C for 1/3 share in profits. A debtor whose dues of Rs.5000 were written off as bad debts, paid Rs.4000 in full settlement. Bad debts recovered Rs.4000 will be debited to ____ and credited to ____

Ans: Cash account, revaluation account

Q3: On the admission of a new partner, after revaluation has been done, the value of assets and liabilities appear in the books of the firm at ____

Ans: their current value

Q4: At the time of admission of a partner, new profit sharing is used for sharing future ____

Ans: Profit

Q5: when the value of goodwill of the firm is not given but has to be inferred on the basis of net worth of the firm, it is called ____

Ans: Hidden goodwill

Q6: At the time of admission, it the book value and the market value of investment is same then investment fluctuation reserved is transferred to ____ account of the old partners in their ____ ratio.

Ans: Capital accounts of old partners, old profit sharing ratio

Q7: At the time of admission, the assets are revalued and liabilities are reassessed. The increase or decrease in the values is debited or credited in ____

Ans: Revaluation account

Q8: Revaluation account is a ____

Ans: Nominal account

Q9: The newly admitted partner brings his/ her share of capital for which he/she will get ____ in firm.

Ans: Profit share

Q10: Goodwill appearing in the books oat the time of admission of a new partner is written off by debiting ____ and crediting ____

Ans: Old partners'capital accounts, goodwill account

Q11: Why is it necessary to revalue assets and reassess liabilities of a firm in case of admission of a new partner?

Ans: The assets are revalued and liabilities of a firm are reassess, at the time of admission of a partner because the new partner should; neither benefit nor suffer because change in the value of assets and liabilities as on the date of admission.

Q12: What are the accumulated profit and accumulated losses?

Ans: The profit accumulated over the years and have not been credited to partners’ capital A/c are known as accumulated Profit or undistributed profit, e.g. the General Reserve, Profit and Loss A/c (credit balance). The losses which have not yet been written off to the debit of Partners’ Capital A/c are known as accumulated Losses, e.g. the Profit and Loss A/c appearing on the assets side of Balance Sheet, etc.

Q13: Explain the treatment of goodwill in the books of a firm on the admission of a new Partner when goodwill already appears in the Balance sheet at its full value and the new partner brings his share of good will in cash.

Ans: By following accounting standard - 10, the existing goodwill (i.e. goodwill appearing in the Balance Sheet) is written off to the old partners’ Capital a/c in their old profit sharing ratio.

Old partners’ capital A/c Dr.

To Goodwill A/c

[Being the existing g/w written off in the old ratio.]

Q14: Under what circumstances the premium for goodwill paid by the incoming Partner will not recorded in the books of Accounts?

Ans: When the premium for goodwill is paid by the incoming partner privately, it is not recorded in the books of A/c as it is as a matter outside the business.

|

42 videos|199 docs|43 tests

|

FAQs on Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner - Accountancy Class 12 - Commerce

| 1. What is the process of reconstitution of a partnership firm? |  |

| 2. How is a new partner admitted into a partnership firm? | |

| 3. What are the reasons for admitting a new partner into a partnership firm? | |

| 4. Can a partnership firm be reconstituted without the consent of all partners? | |

| 5. Can a partner be expelled from a partnership firm? | |

Extra Questions

,Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner | Accountancy Class 12 - Commerce

,past year papers

,Viva Questions

,shortcuts and tricks

,mock tests for examination

,Free

,ppt

,Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner | Accountancy Class 12 - Commerce

,Important questions

,Exam

,study material

,practice quizzes

,video lectures

,Objective type Questions

,Summary

,Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner | Accountancy Class 12 - Commerce

,MCQs

,Sample Paper

,Previous Year Questions with Solutions

,Semester Notes

;

Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner Free PDF Download

Importance of Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner

Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner Notes

Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner Commerce Questions

Study Worksheet Solutions: Reconstitution of a Partnership Firm : Admission of a Partner on the App

|

© EduRev

|

Education Revolution

|

|