Chapter Notes - Financial Statements - II

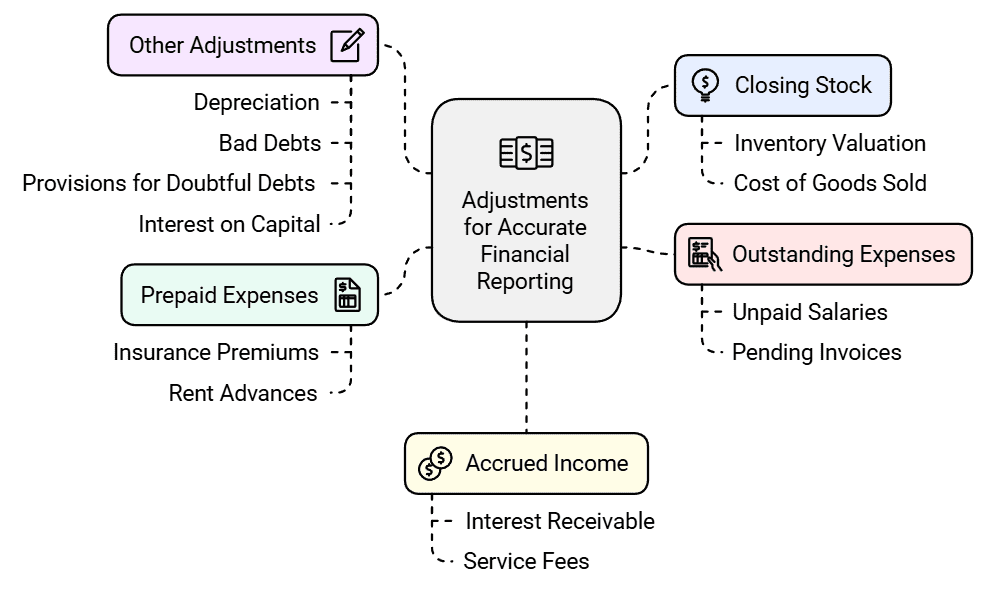

Need for Adjustments

- According to the accrual concept of accounting, profit or loss for an accounting year is determined by incomes earned and expenses incurred during that year, not merely by cash received and paid.

- Business transactions often affect two or more accounting periods. To show a fair and true view of profit and the financial position, certain adjustments are required in the final accounts.

- Common adjustments include closing stock, outstanding expenses, prepaid expenses, accrued income, income received in advance, depreciation, bad debts, provision for doubtful debts, provision for discount on debtors, manager's commission, and interest on capital.

- For example, if an insurance premium covers several years, only the part relating to the current accounting year should be charged as expense. Outstanding salaries unpaid at year-end must be included as expenses for the year to determine the correct profit.

- The journal entries made to record these adjustments are called adjusting entries. Each adjustment affects two places in the final accounts (double entry): the trading/profit and loss account and the balance sheet.

Adjustments in Financial Statements

- Closing Stock: Adjust the figure to reflect inventory on hand at the end of the accounting period.

- Outstanding Expenses: Record expenses incurred but not yet paid in the correct accounting period.

- Prepaid/Unexpired Expenses: Recognise expenses paid in advance that relate to future periods as assets.

- Accrued Income: Include income earned but not yet received in the current period.

- Income Received in Advance: Treat income received but not earned in the current period as a liability.

- Depreciation: Charge depreciation on fixed assets to reflect wear and tear and obsolescence.

- Bad Debts: Write off receivables that are irrecoverable.

- Provision for Doubtful Debts: Create a provision to cover receivables that may become bad in future.

- Provision for Discount on Debtors: Estimate discounts likely to be allowed to debtors for early payment.

- Manager's Commission: Account for commission payable to the manager as per the agreement, either before or after charging the commission itself.

- Interest on Capital: Account for interest due to the proprietor on his capital, where applicable.

When preparing final accounts, we normally start with a trial balance and are given additional information for adjustments. Each adjustment is reflected in the final accounts in two places to complete the double entry. Consider the following illustrative account and adjustments:

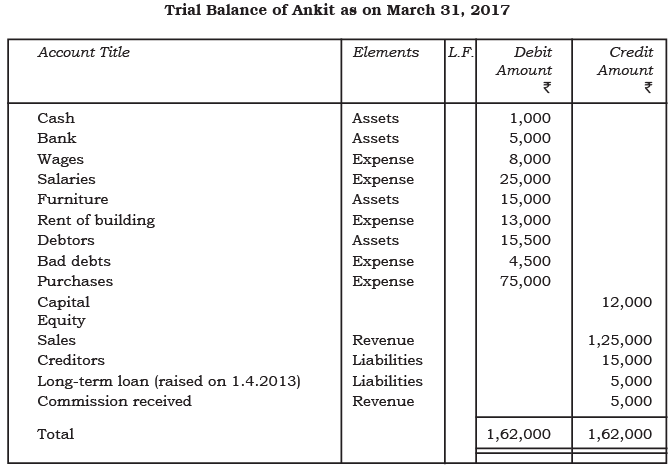

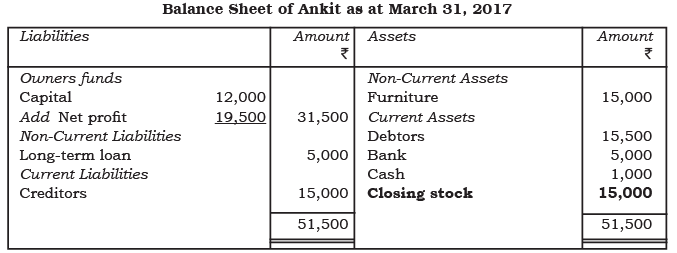

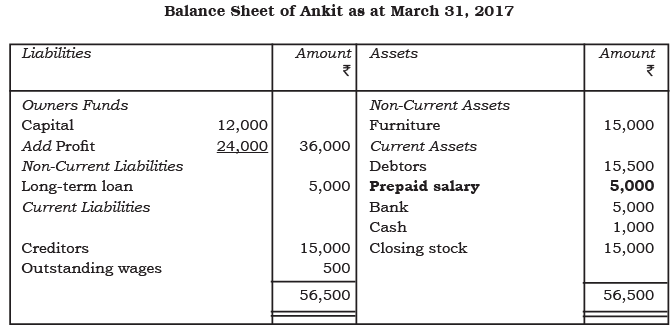

Showing the trial balance of Ankit

Showing the trial balance of AnkitAdditional information: The stock on March 31, 2017 was ₹ 15,000.

Closing Stock

- Closing stock is the value of goods unsold and remaining in inventory at the end of the accounting period.

- It is a necessary component in calculating the cost of goods sold (COGS) and hence affects gross profit and net profit.

Adjustment of Closing Stock

- Closing stock is adjusted in the Trading and Profit & Loss Account by crediting the Trading Account with the closing stock figure.

- Closing stock is also shown on the asset side of the Balance Sheet.

Accounting Entry for Closing Stock

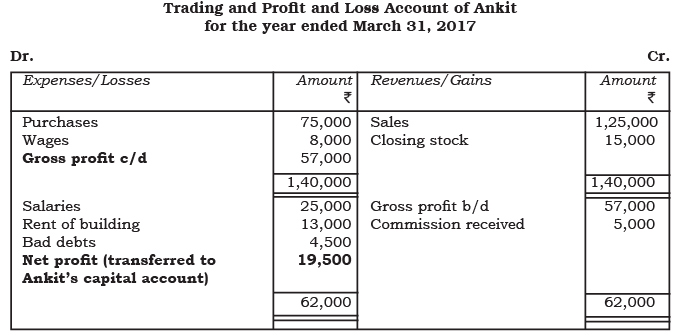

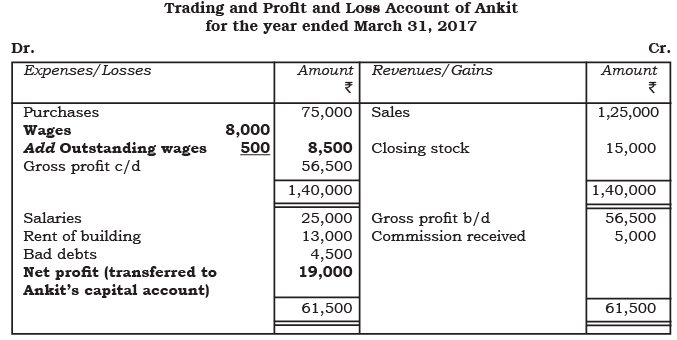

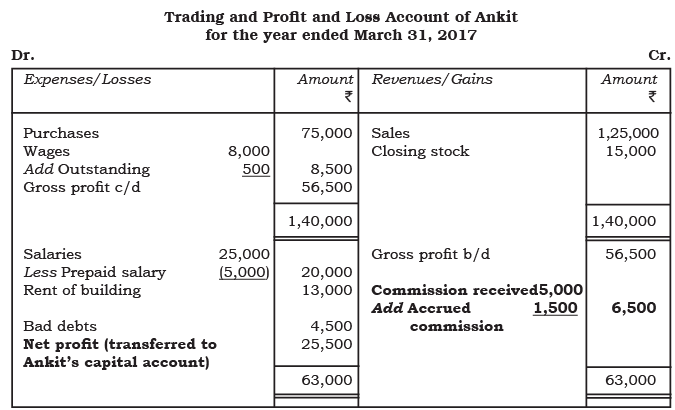

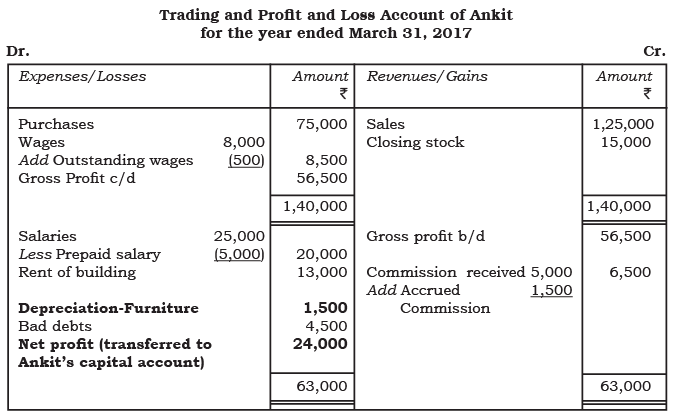

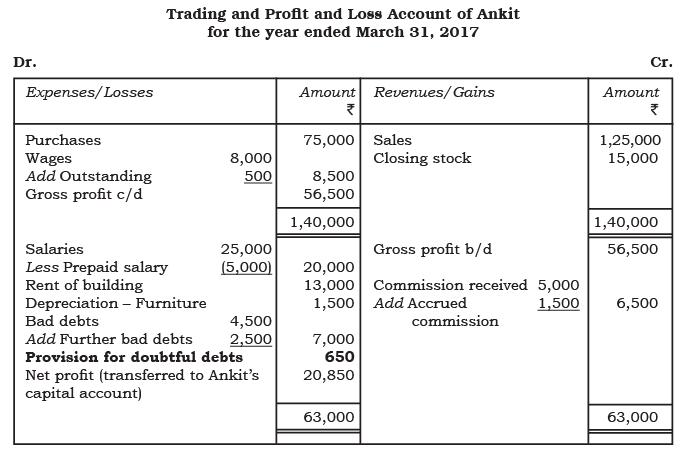

The closing stock of the year becomes the opening stock of the next year and will appear in next year's trial balance. For example, the Trading and Profit & Loss Account and Balance Sheet of Ankit for the year ended 31 March 2017 will appear as follows:

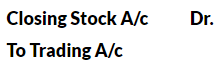

Sometimes, opening and closing stocks are adjusted through the Purchases Account. The journal entry used in that case is:

When this entry is made, the Purchases figure recorded in the Trading Account becomes adjusted purchases. The adjusted purchases are shown on the debit side of the Trading Account, and closing stock is not separately displayed on the credit side of the Trading Account because it has already been accounted for via the purchases adjustment. Similarly, opening stock is not separately shown when it is included in purchase adjustments:

When opening and closing stocks are adjusted through Purchases, the trial balance will not show opening stock; the closing stock will be included directly in the trial balance (not as supplementary information). In that case, adjusted purchases should be debited in the Trading Account. The closing stock shall be shown on the assets side of the Balance Sheet as follows:

Outstanding Expenses

At the end of an accounting year, certain expenses may have been incurred but remain unpaid (for example, wages, salaries, interest). Such items are called outstanding expenses and must be recognised in the accounting period in which they are incurred.

The journal entry to record an outstanding expense is:

The entry creates a new account called Outstanding Expenses, categorized as a liability on the balance sheet. The amount for outstanding expenses is included in the total expenses under a specific category for preparing the trading and profit and loss account. For instance, in Ankit's trial balance, wages are recorded at ₹8,000. If Ankit owes ₹500 in wages for the year 2016-17 to an employee, the actual wage expense should be ₹8,500 instead of ₹8,000. Ankit must report ₹8,500 as the wage expense in the trading and profit and loss account and recognize a current liability of ₹500 for the outstanding wages. This amount will be labeled as wages outstanding and will be adjusted in the wages account through the following journal entry:

The wages account for the preparation of the Trading and Profit & Loss Account will appear as follows:

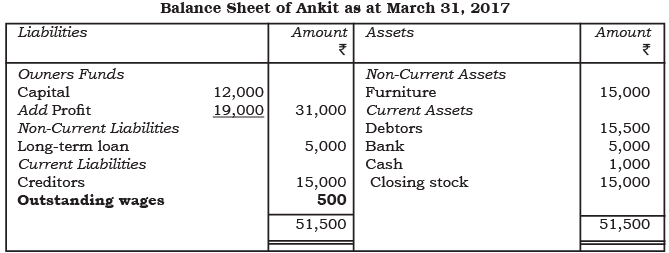

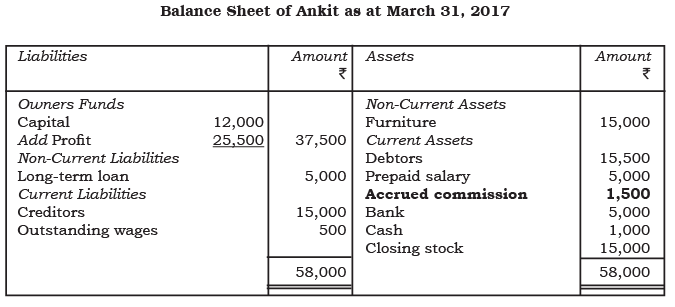

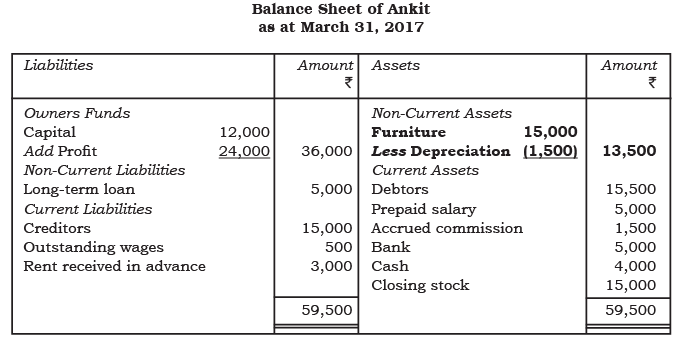

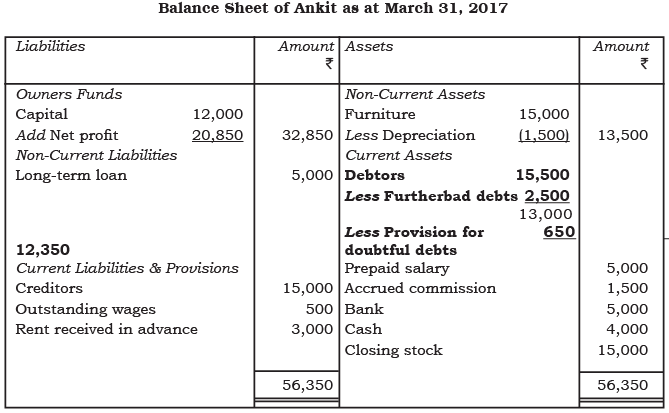

Due to outstanding wages the net profit of Ankit decreases to ₹ 19,000. The Balance Sheet will show the outstanding wages as follows:

Prepaid (Unexpired) Expenses

Some expenses are paid in advance and their benefit extends to future periods. The portion of such payment that relates to the next accounting period is called prepaid expense and should be carried forward as an asset.

The adjusting journal entry for prepaid expense is:

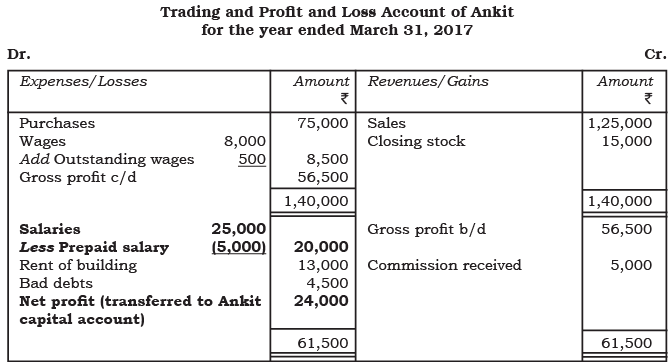

The adjustment entry reduces the prepaid amount from the total expense, and the new prepaid expense account appears on the asset side of the balance sheet. For instance, in Ankit's trial balance, if he has paid a total salary of ₹25,000, which includes an advance payment of ₹5,000 to an employee, he has effectively overpaid by ₹5,000. Therefore, the correct salary expense for the period should be ₹20,000. Ankit must report ₹20,000 as salary expense in the profit and loss account and recognise ₹5,000 as a current asset for the prepaid salary. This will be recorded as a prepaid salary account through the following journal entry:

Observe how the prepaid salary has resulted in an increase in net profit by ₹ 5,000, making it ₹ 24,000. Further, the item relating to prepaid salary will be shown in the balance sheet on the assets side as follows:

Try yourself: Which of the following adjustments is made for outstanding expenses in the accounting records?

Accrued Income

Accrued income (or outstanding income) is income earned during the accounting period but not yet received by the end of that period. Examples include interest receivable, commission receivable, rent receivable, etc. The adjusting entry is:

The accrued income will be included in the corresponding income on the profit and loss account, and a new accrued income account will be listed on the asset side of the balance sheet. For example, if Ankit assisted a fellow businessman by introducing parties for a commission, the trial balance will show a commission received of ₹5,000. If an additional ₹1,500 is still owed by the businessman, the total commission income for 2016-17 would be ₹6,500 (₹5,000 + ₹1,500). Ankit must record an adjustment entry to reflect the accrued commission as follows:

The Accrued Income account will be shown in the Trading and Profit & Loss Account as follows:

Accrued commission increases Ankit's net profit by ₹ 1,500 to ₹ 25,500. This ₹ 1,500 will be shown under current assets on the Balance Sheet.

Income Received in Advance

Income received before it is earned in the current accounting period is income received in advance (unearned income). It is a liability because the business owes either services or the return of money if services are not provided.

The adjusting entry is:

This ensures the Profit & Loss Account shows only income earned in the period, while Income Received in Advance appears as a liability in the Balance Sheet.

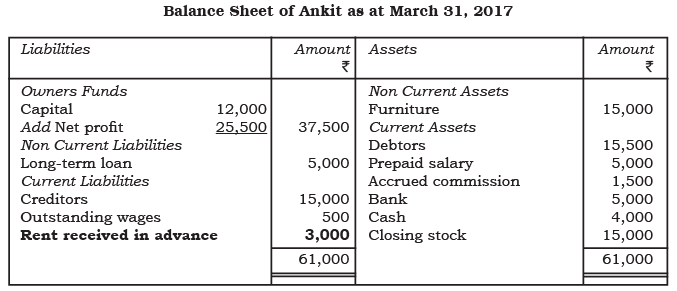

For instance, if Ankit agrees on March 31, 2017, to sublet part of his building to a fellow shopkeeper for ₹1,000 per month, and the shopkeeper pays rent in advance for April, May, and June, totalling ₹3,000, this amount initially credited to the profit and loss account is incorrect. Since this income does not pertain to the current year, it should not be credited to the profit and loss account. Instead, it is classified as income received in advance and recorded as a liability of ₹3,000. Ankit must make an adjustment entry to reflect the income received in advance through the following journal entry:

The Rent Received in Advance account will appear as follows:

Depreciation

Depreciation is the systematic allocation of the cost of a fixed asset over its useful life. It represents the decrease in the value of an asset due to wear and tear, obsolescence and passage of time. Depreciation is treated as an expense of the business and debited to the Profit & Loss Account.

The journal entry for recording depreciation is:

- Depreciation A/c Dr.

To Concerned Asset A/c

On the Balance Sheet, the asset is shown at its cost less accumulated depreciation (or by showing the asset at cost and a separate provision/accumulated depreciation figure as a deduction).

For example, if Ankit has Furniture shown at ₹ 15,000 and depreciation is charged at 10% per annum, depreciation for the year is ₹ 1,500 (₹ 15,000 × 10%). The adjusting entry is:

- Depreciation A/c Dr. ₹ 1,500

To Furniture A/c ₹ 1,500

Depreciation will reduce net profit and be shown in the Profit & Loss Account. The Balance Sheet will reflect the asset at its written-down value after depreciation.

Depreciation as an expense reduces net profit.

Bad Debts

Bad debts are amounts due from debtors which are considered irrecoverable and must be written off as an expense.

The journal entry for writing off bad debts is:

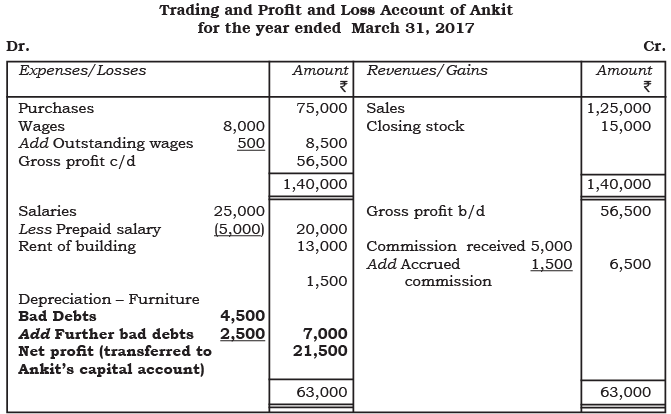

In the example of Ankit, the trial balance shows Bad Debts ₹ 4,500 and Sundry Debtors ₹ 15,500. If a particular debtor owing ₹ 2,500 becomes insolvent, that amount is additional bad debts for the year. The adjusting entry is:

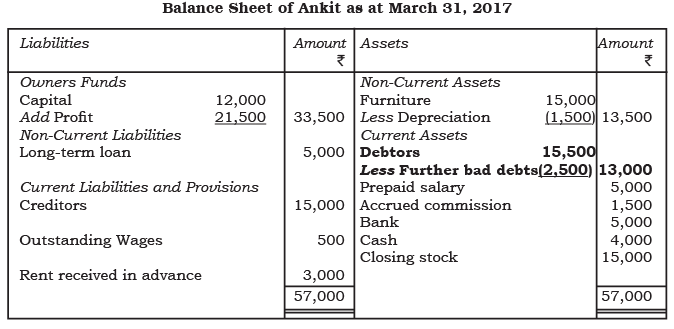

After this, debtors reduce to ₹ 13,000 (₹ 15,500 - ₹ 2,500) and total bad debts increase to ₹ 7,000 (₹ 4,500 + ₹ 2,500). The treatment in the Profit & Loss Account and Balance Sheet is shown below:

Provision for Bad and Doubtful Debts

To provide for debts that may become irrecoverable in future, businesses create a provision for bad and doubtful debts. This is a prudent estimate deducted from debtors to report a realistic realisable value.

The provision is created by debiting the Profit & Loss Account and crediting the Provision for Doubtful Debts (or Reserve for Bad Debts) account.

In the Balance Sheet, the provision is shown as a deduction from Sundry Debtors.

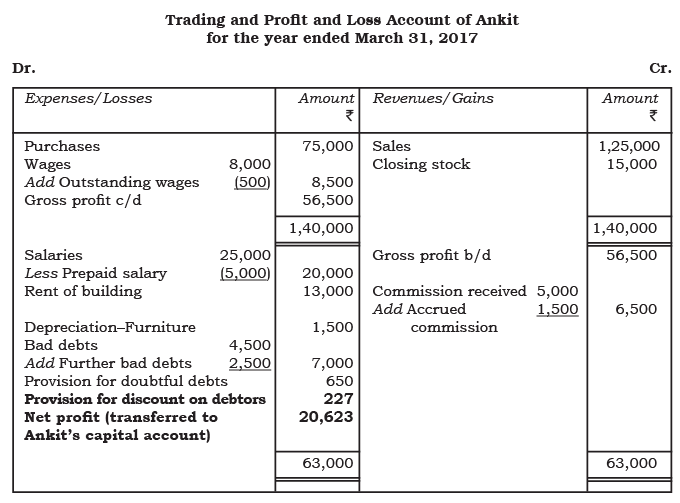

For example, if Ankit estimates that 5% of the Debtors of ₹ 13,000 may default, the provision required is ₹ 650 (₹ 13,000 × 5%). The adjusting entry is:

This entry reduces the current year's profit by ₹ 650 and is shown as a deduction from Sundry Debtors in the Balance Sheet:

The opening provision (provision brought forward) is adjusted against current year bad debts, and the required closing provision is computed accordingly when an old provision exists.

Provision for Discount on Debtors

Businesses often allow discounts to debtors to encourage prompt payment. To anticipate such discounts, a provision for discount on debtors is created. This provision is made on the amount of good debtors, i.e., after deducting bad debts and provision for doubtful debts from the total debtors.

The journal entry for creating a provision for discount on debtors is:

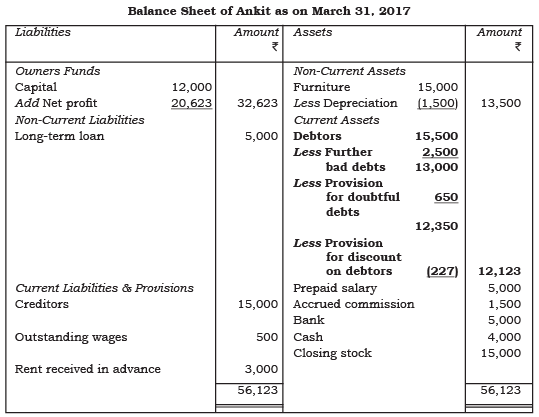

For example, after deducting doubtful debts, the good debtors are ₹ 12,350 (₹ 13,000 - ₹ 650). If the provision required works out to ₹ 227, the adjustment entry will be:

This reduces current year profit by ₹ 227, and the Balance Sheet shows debtors at the expected realisable value, i.e., ₹ 12,123 after deducting both provisions.

Next year when discounts are actually allowed, the Provision for Discount on Debtors account is used to meet those discounts; the account is handled similar to the provision for doubtful debts.

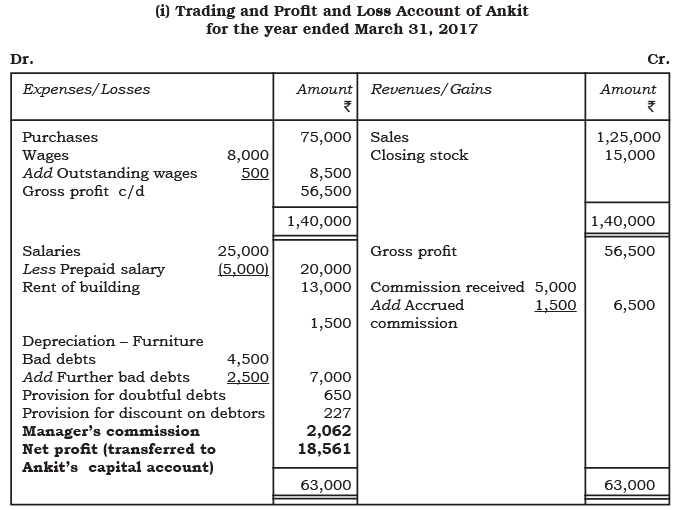

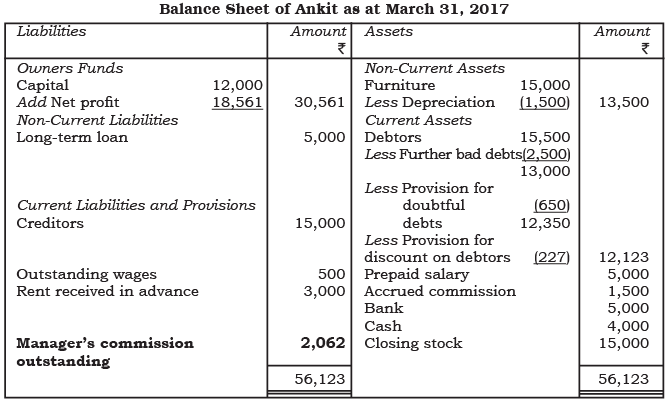

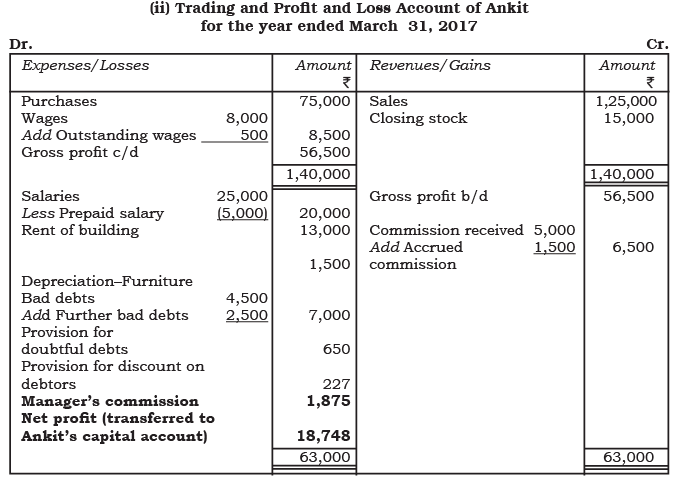

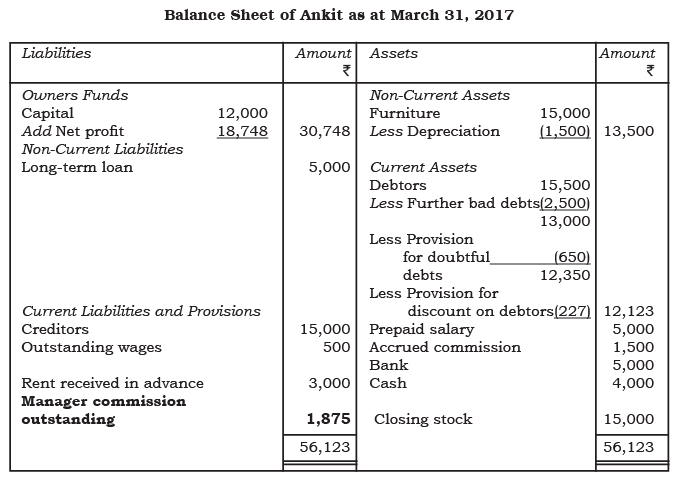

Manager's Commission

The manager of a business may be entitled to commission based on the company's net profit. Commission may be calculated either:

- as a percentage of net profit before charging such commission, or

- as a percentage of net profit after charging such commission.

If no specification is given, it is generally assumed commission is on net profit before charging such commission.

Example: If net profit before commission is ₹ 110 and commission is 10% on profit before commission, commission = ₹ 110 × 10% = ₹ 11.

If the commission is 10% on profit after charging the commission, it is computed using the formula:

- Commission = Profit before commission × Rate of commission / (100 + Rate of commission)

So Commission = 110 × 10 / 110 = ₹ 10 in that case.

The manager's commission is recorded by debiting the Profit & Loss Account and crediting the Manager's Commission Payable account as follows:

Example presentations where the manager's commission is calculated on profit before and after charging such commission are shown below for Ankit:

Interest on Capital

When interest is allowed to the proprietor on capital, such interest is treated as an expense for the business. Interest on capital is usually calculated on the opening capital for the year. If additional capital is introduced during the year, interest can be provided on that portion from the date of introduction.

The journal entry for interest on capital is:

In the final accounts, interest on capital appears as an expense in the Profit & Loss Account and is added to the proprietor's capital in the Balance Sheet.

For example, if interest on capital is 5% and the amount comes to ₹ 600, the entry will be:

This decreases net profit by ₹ 600. Adding the reduced profit to capital and then adding interest on capital back to capital neutralises the effect on capital overall (i.e., the net effect on capital depends on both adjustments).

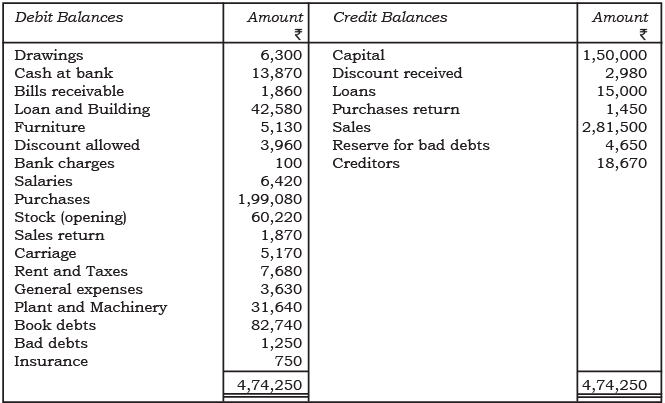

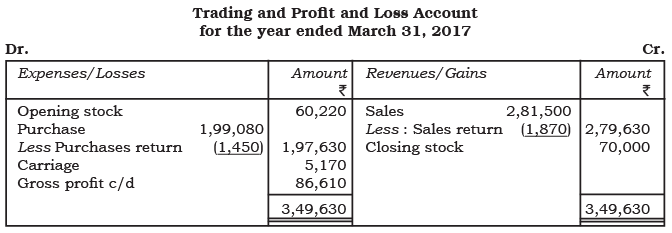

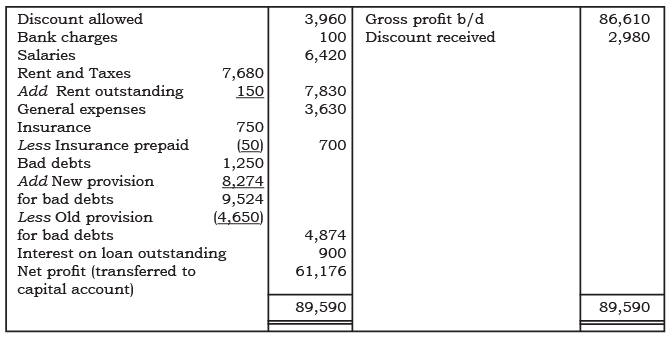

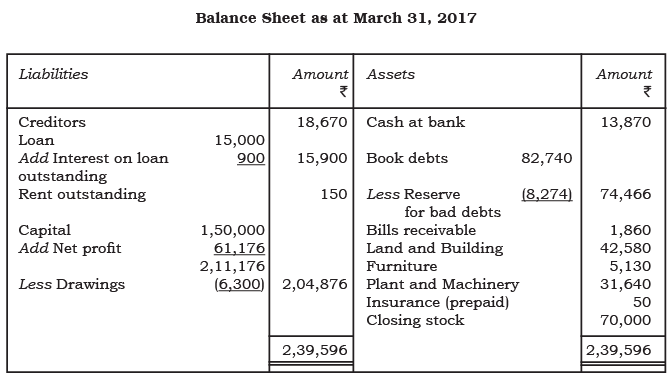

Illustration 1:

From the following balances, prepare the Trading and Profit & Loss Account and Balance Sheet as on 31 March 2017.

Adjustments

- Closing stock ₹ 70,000

- Create a reserve for bad and doubtful debts @ 10% on book debts

- Insurance prepaid ₹ 50

- Rent outstanding ₹ 150

- Interest on loan due @ 6% p.a.

Solution:

Illustration 2:

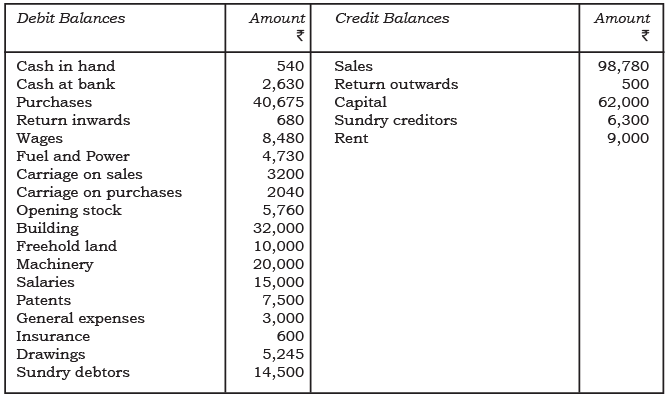

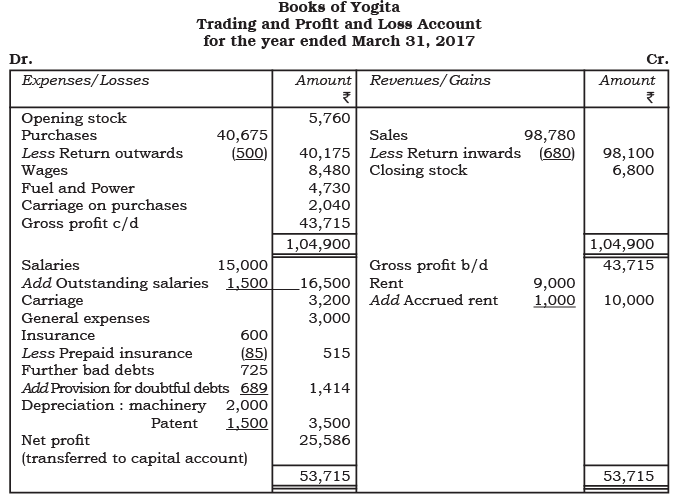

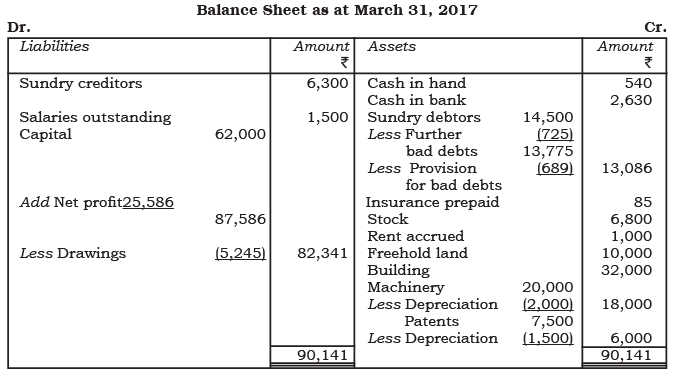

The following were the balances extracted from the books of Yogita as on 31 March 2017:

Taking into account the following adjustments, prepare Trading and Profit & Loss Account and Balance Sheet as on 31 March 2017:

- Stock in hand on 31 March 2017 was ₹ 6,800

- Machinery is to be depreciated at 10% and Patents at 20%

- Salaries for March 201,7, amounting to ₹ 1,500 were outstanding

- Insurance includes a premium of ₹ 170 on a policy expiring on 30 September 2017

- Further bad debts ₹ 725; create a provision @ 5% on debtors

- Rent receivable ₹ 1,000

Solution:

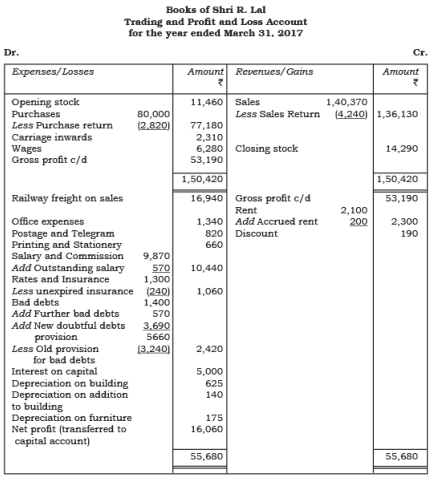

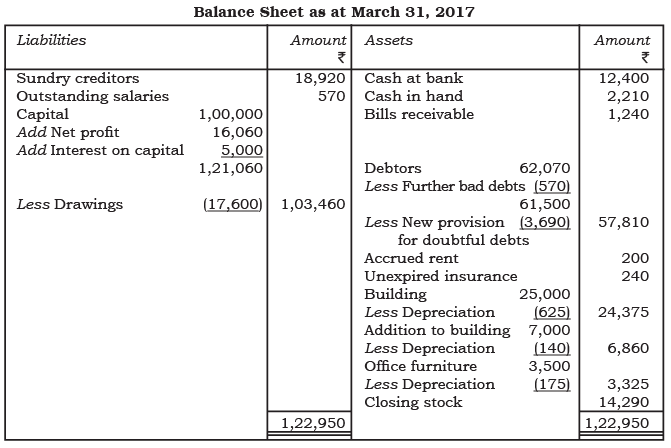

Illustration 3:

The following balances were extracted from the books of Shri R. Lal on 31 March 2017:

Prepare Trading and Profit & Loss Account and Balance Sheet as on 31 March 2017 after the following adjustments:

- Depreciate old building by ₹ 625; add to building at 2% and office furniture at 5%

- Write off further bad debts ₹ 570

- Increase the bad debts reserve to 6% of debtors

- Outstanding salary ₹ 570 as on 31 March 2017

- Rent receivable ₹ 200 on 31 March 2017

- Interest on capital at 5% to be charged

- Unexpired insurance ₹ 240

- Stock valued at ₹ 14,290 on 31 March 2017

Solutions:

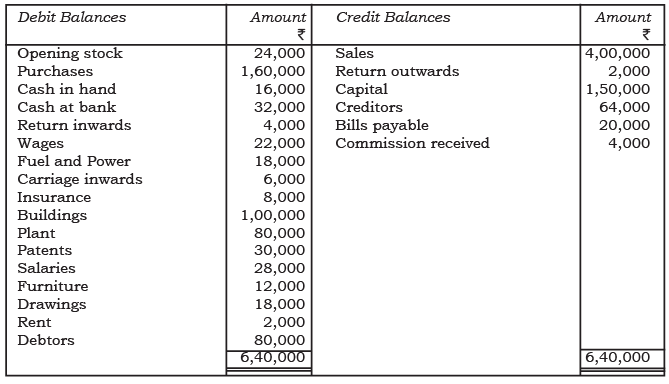

Illustration 4:

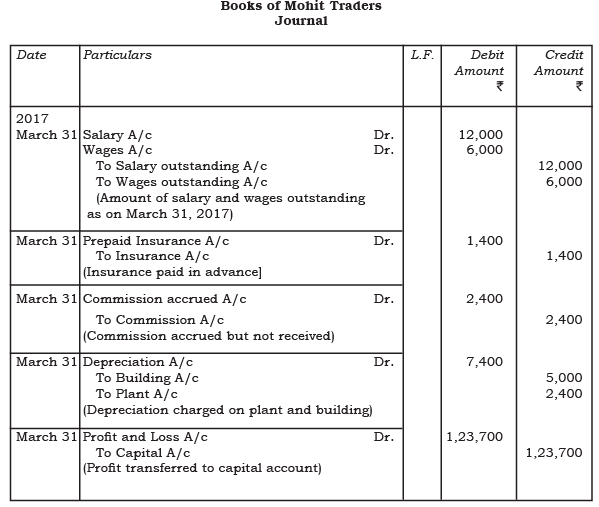

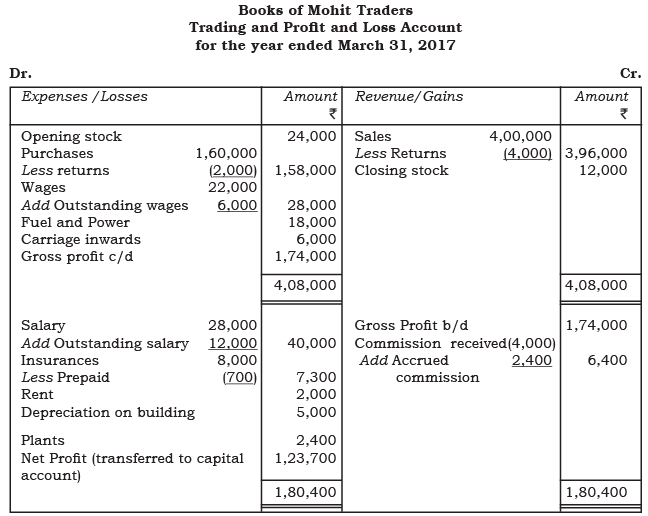

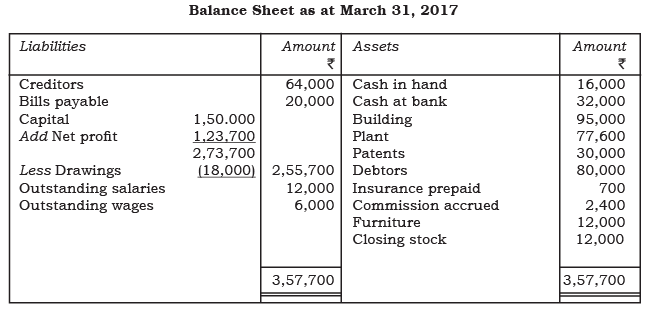

Prepare the Trading and Profit & Loss Account of M/s Mohit Traders as on 31 March 2017; draw necessary Journal entries and Balance Sheet as on that date.

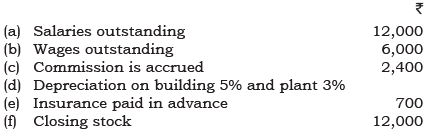

Adjustments

Solution:

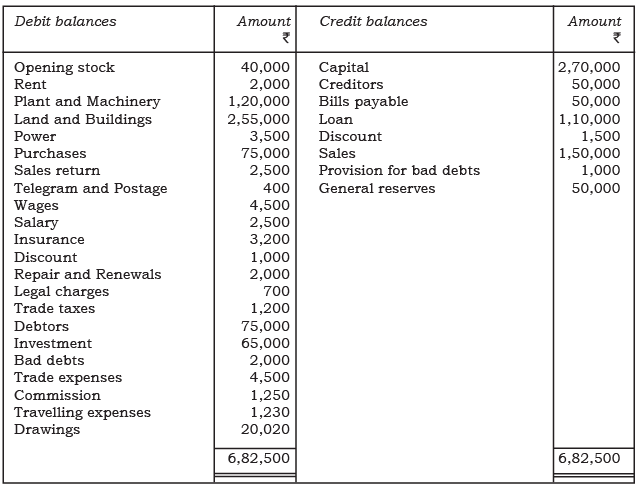

Illustration 5:

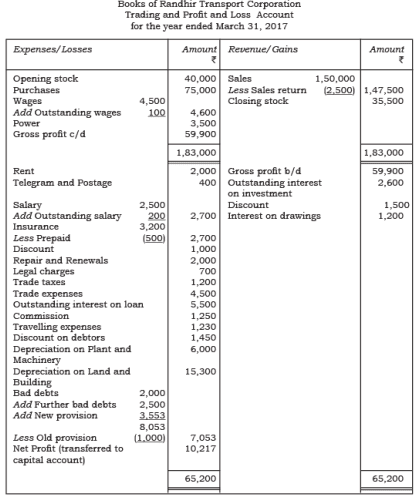

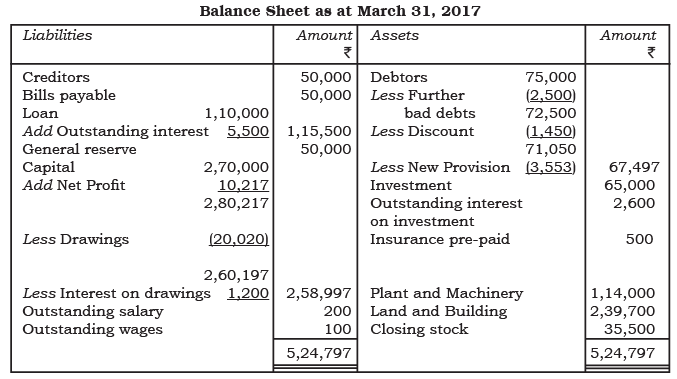

The following information has been extracted from the trial balance of M/s Randhir Transport Corporation.

Adjustments

- Closing stock ₹ 35,500

- Depreciation charged on plant & machinery 5% and land & building 6%

- Interest on drawings @ 6% and interest on loan @ 5%

- Interest on investments @ 4%

- Further bad debts ₹ 2,500 and provision for doubtful debts on debtors 5%

- Discount on debtors @ 2%

- Salary outstanding ₹ 200

- Wages outstanding ₹ 100

- Insurance prepaid ₹ 500

You are required to prepare the Trading and Profit & Loss Account and the Balance Sheet on 31 March 2017.

Solution:

Illustration 6:

From the following balances of M/s Keshav Bros., prepare Trading and Profit & Loss Account and Balance Sheet as on 31 March 2017.

Adjustments

- Provision for bad debts @ 5% and further bad debts ₹ 2,000

- Rent received in advance ₹ 6,000

- Prepaid insurance ₹ 200

- Depreciation on furniture @ 5%, plant & machinery @ 6%, building @ 7%

Solution:

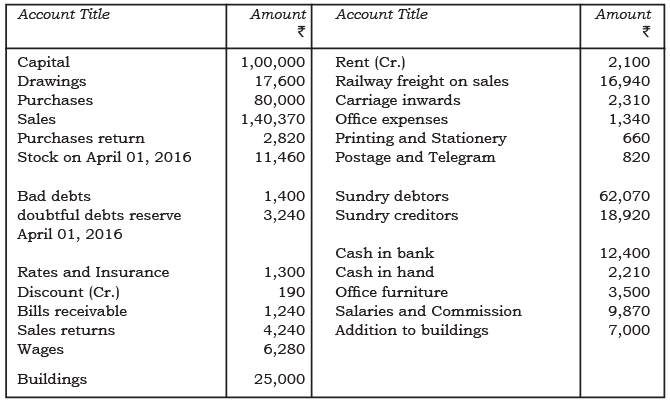

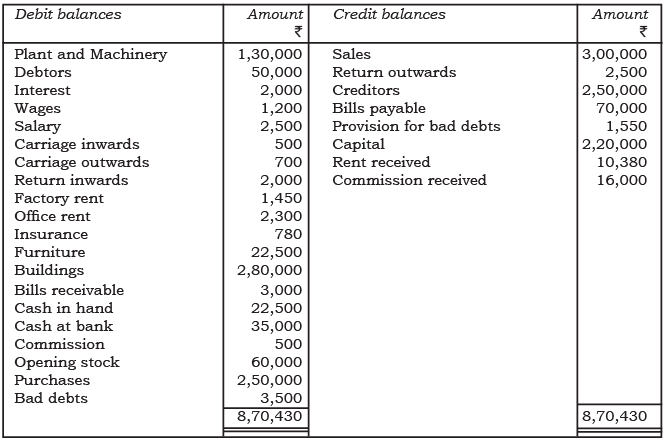

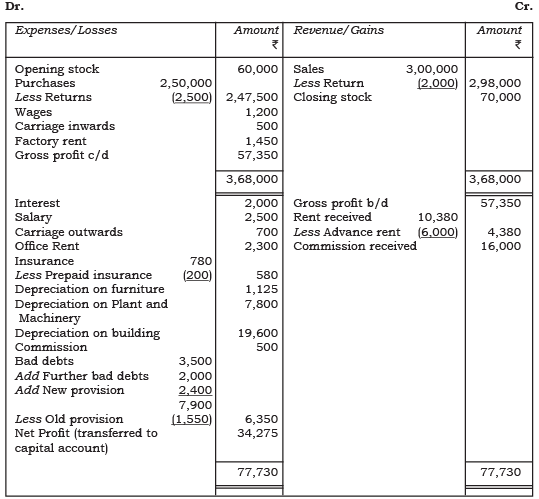

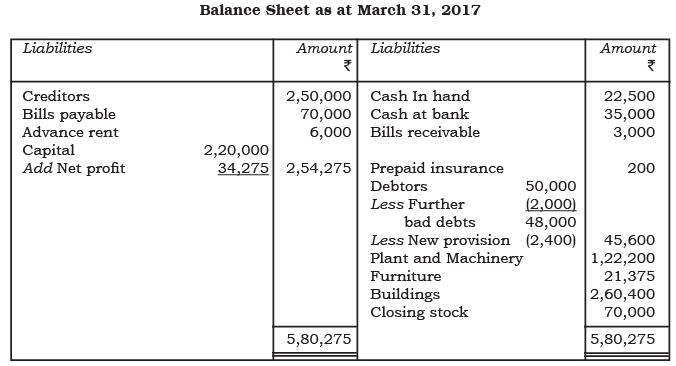

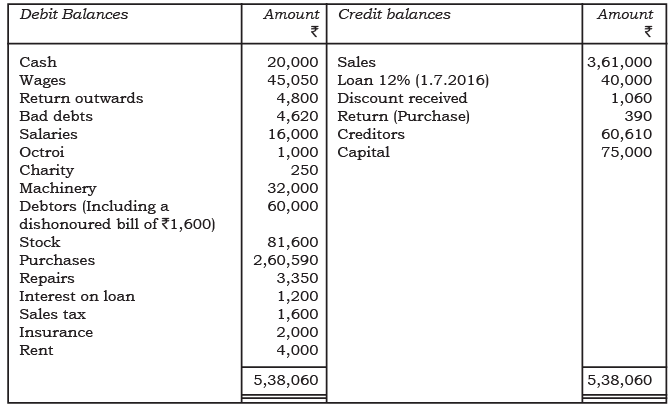

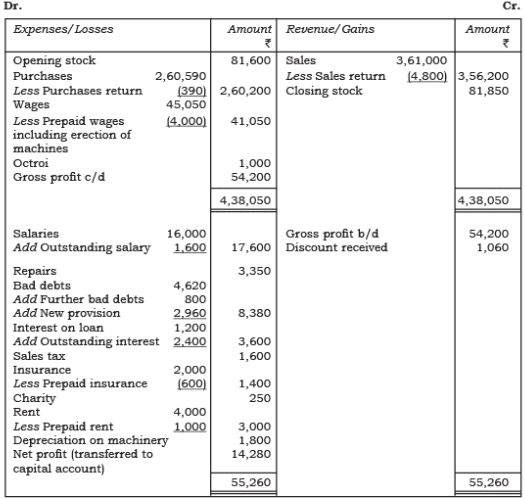

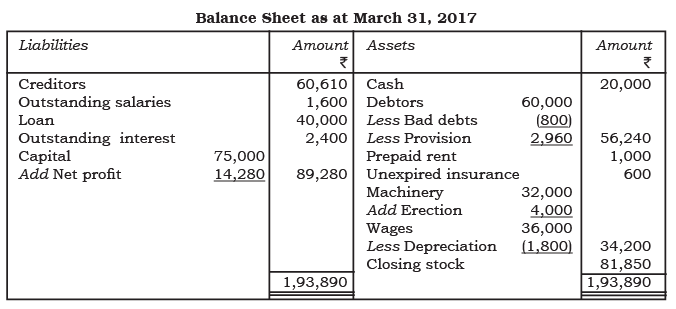

Illustration 7:

The following information has been taken from the trial balance of M/s Fair Brothers Ltd. Prepare Trading and Profit & Loss Account and Balance Sheet as at 31 March 2017.

Adjustments

- Wages include ₹ 4,000 for the erection of new machinery on 1 April 2016

- Provide 5% depreciation on furniture

- Salaries unpaid ₹ 1,600

- Closing stock ₹ 81,850

- Create a provision of 5% on debtors

- Half the amount of a bill is recoverable

- Rent is paid up to 30 July 2017

- Insurance unexpired ₹ 600

Solution:

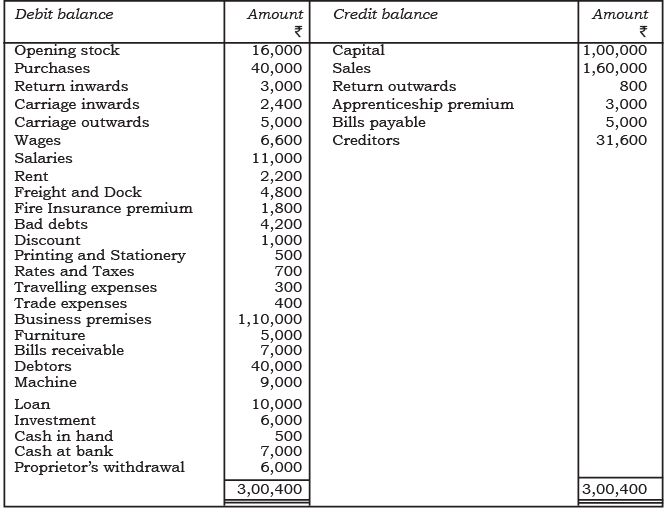

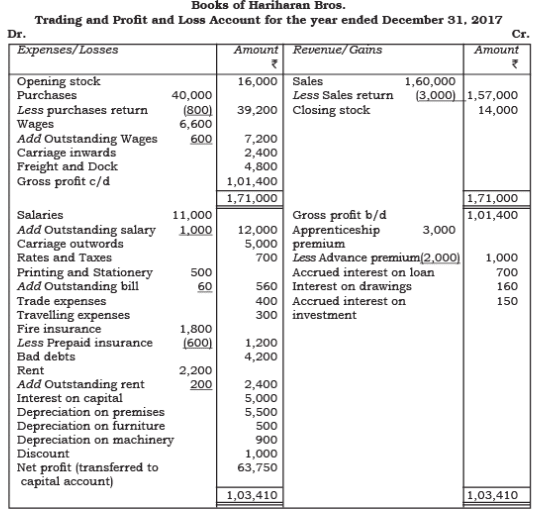

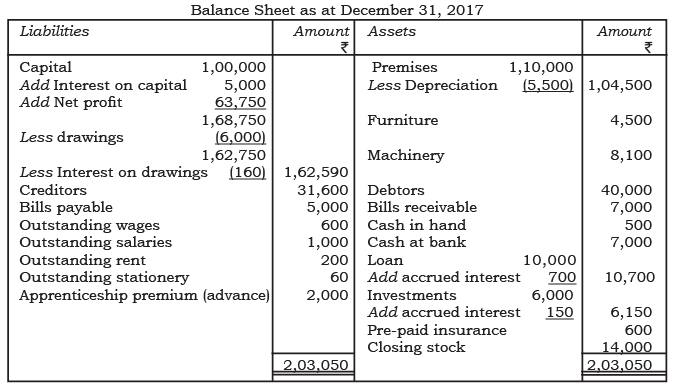

Illustration 8:

From the following balances extracted from the books of M/s Hariharan Brothers, prepare Trading and Profit & Loss Account and Balance Sheet as on 31 December 2017.

Adjustments

- Closing stock ₹ 14,000

- Wages outstanding ₹ 600, Salaries outstanding ₹ 1,000, Rent outstanding ₹ 200

- Fire insurance premium includes ₹ 1,200 paid on 1 July 2016 for one year (1 July 2016 - 30 June 2017)

- Apprenticeship premium paid on 1 January 2016 for three years in advance

- Stationery bill unpaid ₹ 60

- Depreciation on Premises @ 5%, Furniture @ 10%, Machinery @ 10%

- Interest on the loan given accrued for one year @ 7%

- Interest on investment @ 5% for half a year to 31 December 2016 has accrued

- Interest on capital to be allowed at 5% for one year

- Interest on drawings to be charged at ₹ 160 for the year

Solution:

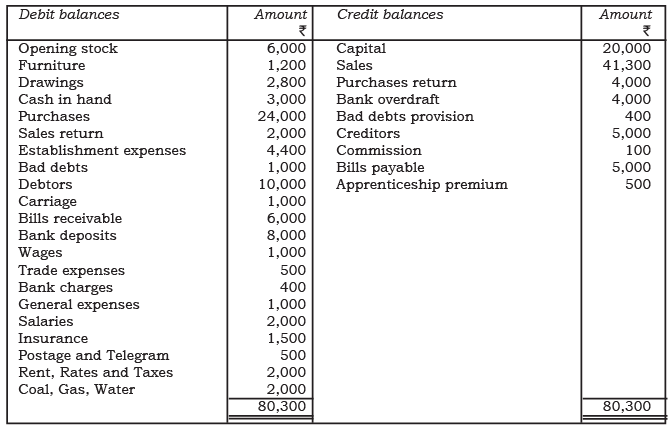

Illustration 9:

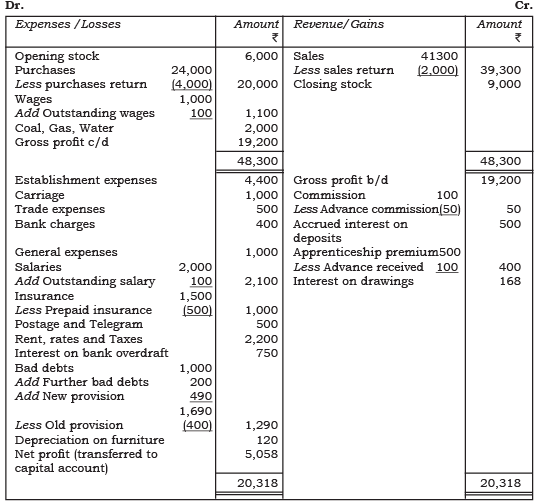

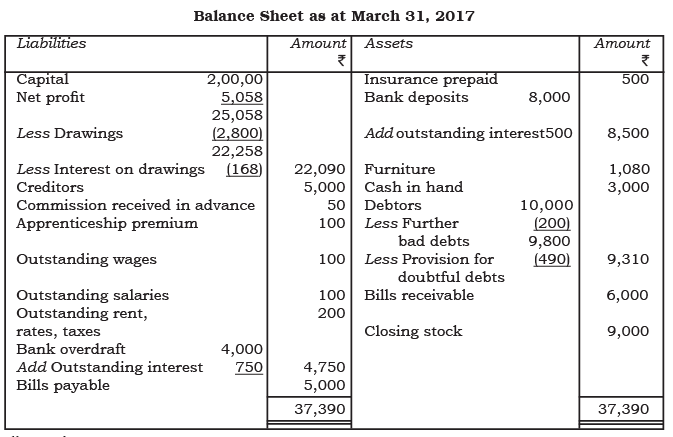

The following balances have been extracted from the trial balance of M/s Kolkata Ltd. Prepare Trading and Profit & Loss Account and Balance Sheet as at 31 March 2017.

Adjustments

- Outstanding salaries ₹ 100, Rent & Taxes ₹ 200, Wages ₹ 100

- Unexpired insurance ₹ 500

- Commission received in advance ₹ 50

- Interest of ₹500 is to be received on bank deposits

- Interest on bank overdraft ₹ 750

- Depreciation on furniture @ 10%

- Closing stock ₹ 9,000

- Further bad debts ₹ 200; new provision @ 5% on debtors

- Apprenticeship premium received in advance ₹ 100

- Interest on drawings @ 6%

Solution:

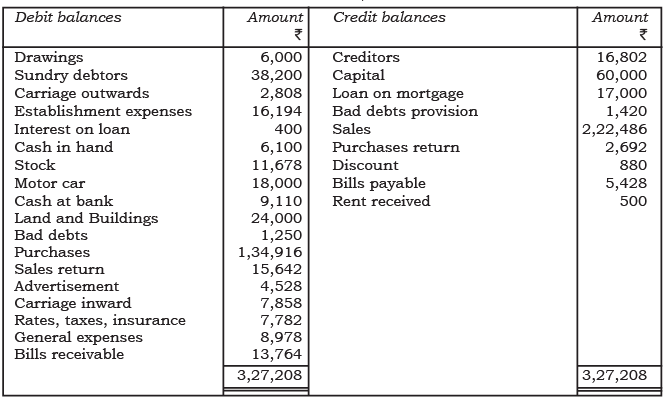

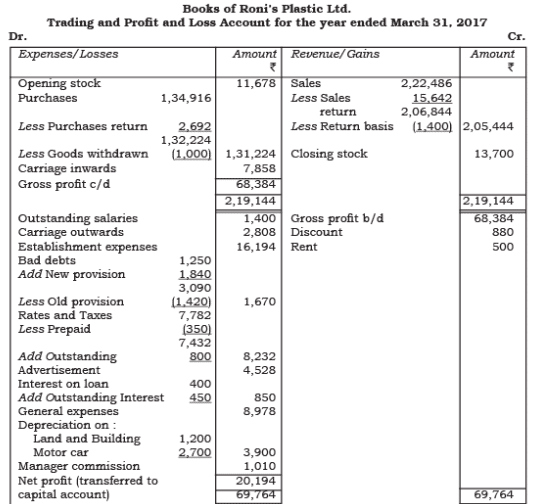

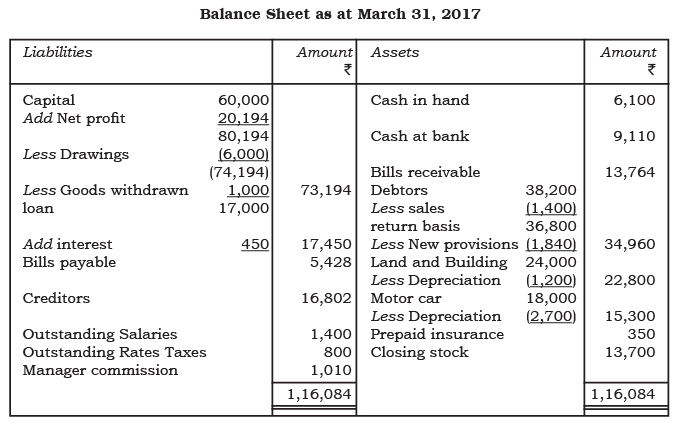

Illustration 10:

Prepare Trading and Profit & Loss Account of M/s Roni Plastic Ltd. from the following trial balance and a Balance Sheet as at 31 March 2017.

Adjustments

- Depreciation on land & building @ 5% and Motor Vehicle @ 15%

- Interest on loan @ 5% taken on 1 April 2016

- Goods costing ₹ 1,200 were sent to a customer on a sale or return basis for ₹ 1,400 on 30 March 2017 and recorded as actual sales

- Salaries ₹ 1,400 and Rates ₹ 800 are due

- The bad debts provision is to be brought up to 5% on sundry debtors

- Closing stock ₹ 13,700

- Goods costing ₹ 1,000 were taken by the proprietor for personal use, but no entry was made

- Insurance prepaid ₹ 350

- Provide the manager's commission @ 5% on Net Profit after charging such commission

Solution:

FAQs on Chapter Notes - Financial Statements - II

| 1. What are the main components of a balance sheet and how do they relate to each other? |  |

| 2. How do I identify the difference between current assets and fixed assets on a balance sheet? | |

| 3. What's the purpose of showing liabilities separately as current and non-current on financial statements? | |

| 4. Why does equity value change when a company makes a profit or loss during the accounting period? | |

| 5. How can I use balance sheet information to calculate important financial ratios for SSC CGL exams? | |