Accounts from Incomplete Records Chapter Notes | SSC CGL Tier 2 - Study Material, Online Tests, Previous Year PDF Download

ACCOUNTS FROM INCOMPLETE RECORDS

LEARNING OBJECTIVES

After studying this lessons you will be able to:

- Define the concept of incomplete records:

- Distinguish between Double entry system and Accounts from incomplete records.

- Ascertain the amount of profit or loss using" Statement of Affairs" method.

- Differentiate between Balance Sheet and Statement of Affairs.

- Prepare Statement of Affairs using given data.

Suggested Methodology

- Illustration Method

- Discussion Method Introduction:

Some small size business entities do not follow the double entry system of maintaining the accounting records instead they maintains books of accounts under the system Accounting from incomplete records. The system in which no set rules of double entry system are followed is called Accounts from incomplete records. Sometimes, it is also termed as 'Single Entry System'

Under this system only the following accounts are maintained:

- Cash book

- The personal A/C

- Some Real A/C according to need

Note: Nominal accounts are not maintained underthis system.

Under this system of maintaining accounts:

- Both the aspects of only certain transactions are recorded e.g. cash received from debtors or cash paid to creditors.

- One aspect of some transactions are recorded e.g. cash paid for the purchase of goods.

- Some financial events are not recorded at all e.g. depreciation charged on fixed assets.

Points to remember

- Accounting Principles and Accounting Standards are not followed property underthis system.

- Original vouchers provide base for preparing the accounts.

- This method is highly flexible because it can be adjusted according to the needs of the organisation.

- Profit or loss is ascertained by either Statement of Affairs method or' Conversion into Double entry Method:

Uses of Incomplete Records

Books according to this system can be maintained only by those small entities in the form of sole Proprietorship or Partnership firms that are not bound to keep records of business transactions as per double entry system. Companies cannot maintain books underthis system because of legal provisions.

Uses of Reasons for keeping incomplete Records

- Simple Method : It is easy and simple as under this method one does not require any special knowledge of the principles for recording of transactions.

- Less Expensive : As under this method only few accounts are prepared therefore business firm does not requires more start for recording the transactions.

- Flexible Method : This method is highly flexible because it can be adjusted according to the needs of the organisation.

- Suitable for small Concerns : This method is most suitable to small business concerns which have mostly cash transactions and very few Assets & Liabilities.

- Easy to calculate profit or / loss : It is easier to calculate profit or loss under this method.

Limitations of Incomplete Records

- Incomplete method : This method is incomplete method of maintaining the accounting records as the aspects, debits and credits, of every transaction are recorded.

- Arithmatical Accuracy cannot be checked : Under this system no real and nominal accounts are maintained. As such a trial balance cannot be prepared to check the arithmetical accuracy of the books of accounts.

- True profit or loss cannot be ascertained : As under this system all the accounts are not prepared like Nominal A/C which is the base for calculating actual profit. So the profit ascertained under this method is not reliable.

- True financial position of the business cannot be judged :Since real accounts are not maintained. It is not possible to prepare a balance sheet showing the true financial position of the business.

- No recognition in the assessment of income Tax & Sales Tax:The system fails to reveal the true profit and sales of a business. As such, the accounts maintained under the system are not accepted by Tax authorities.

- Preparation of Trial Balance not possible : This method does not record both the aspect of a transaction. So trial balance is not possible as all debit and credit items was not there.

Distinction between Single Entry System and Double Entry System

Points of Distinction | Double entry system | Incomplete Records system |

(i) Aspects | Both aspects of transactions are recorded. | One aspect of transactions is recorded. |

(ii) Types of Accounts | All the three types of accounts personal real and nominal are prepared. | Only personal and cash accounts are prepred. |

(iii) Trial Balance | Trail balance is prepared. | Trial balance cannot be prepared. |

(iv) Profit & loss | Profit is ascertained by preparing profit and Loss Account. | It is not possible to prepare Profit and Loss Account. Profit is calculated by preparing Statement of profit. |

(v) Financial Position | Balance Sheet is prepared to ascertain financial position. | Balance Sheet is not prepared. Statement of affairs gives a rough idea of financial position. |

(vi) Proof | Accounting records are treated as proof in the Court of Law. | Accounting record are not treated as proof in the court of Law. |

(vii) Tax Authorities | Tax authorities recognise this system. | Tax authorities do not recognise this system. |

(viii) Suitability | It is suitable in all the cases. | It is suitable only in case of small business houses. |

Ascertainment of Profit or Loss

The main objective of any business enterprise is to earn profits. In case of organization maintaining accounts under incomplete records the amount of profit or loss can be ascertained by following two method

- Statement of affaire method or net worth method

- Conversion in Double entry method (not in syllabus)

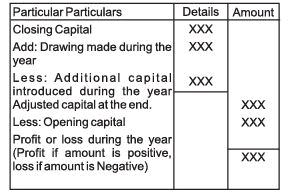

Statement of Affairs Method

Under this method, Profits or losses of the business are ascertained by comparing the Capital at the end and Capital at the beginning of the accounting period.

- When Capital at the end is more than the capital in the beginning during an Accounting period (with the necessary adjustment) there will be profit.

Profits = Closing Capital - Opening Capital - When Capital at the beginning is more than capital at the end during an Accounting Period, (with the necessary adjustment) there will be loss.

Losses = Opening Capital - Closing Capital

Capital at the beginning is calculated by preparing an 'Opening statement of Affairs' and similarly, capital at the end is calculated by preparing a 'Closing Statement of Affairs.

Notes

Under this method two statements are prepared:

- Statement of affairs, for calculating opening and closing capital.

- Statement of profit or loss, for calculating profit or loss.

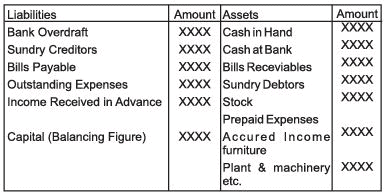

STATEMENT OF AFFAIRS

A Statement of affairs is a statement showing the balances of assets (including cash and bank balance) on the right hand side and the balance of liabilities on the left hand side, on a particulars date. The difference in the total of two sides is known as capital.

Capital = Total Assets - Total liabilities

A statement of affairs is very similar to Balances Sheet as prepared for the business entities maintaining accounts under double entry system, through it should not be described as a Balance Sheet

A Statement of Affairs is prepared as follows :

Step 1: Calculate the amount of 'Opening capital' (If not given in the Question) by preparing Statement of Affairs at the beginning of the accounting period.

Step2: Calculate the amount of 'Closing Capital' by preparing 'Statement of Affair' at the end of the accounting period.

Step 3: Calculation of Profit or Loss by preparing Statement of profit or Loss in the following manner Statement of Profit or Loss forthe year ended.

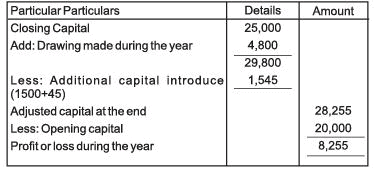

Capital on 1 st April 2015 20,000

Capital on 31st march 2015 25,000

Drawings made during the year 4,800

He sold his investment of 1500 at 3% premium and brought that money into the business. You are required to prepare a statement of profit or loss.

Solution:

Statement of Profit for two year ended 2015-16

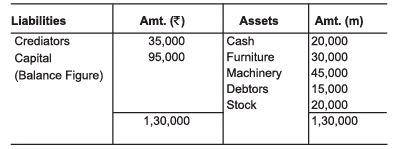

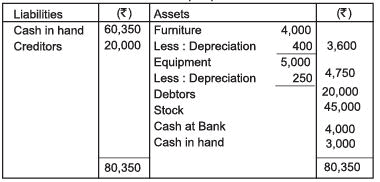

2 Mr. Hemant started his business on 1 st April 2015 with a capital of 1,00,000. He follow a single entry system. At the end of the year i.e. on 31 st March, 2016 the position of Assets & Liabilities was:

Cash in hand 20,000

Furniture 30,000

Machinery 45,000

Debtors 15,000

Stock 20,000

Creditors 35,000

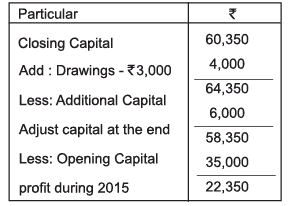

15,000 as additional capital. Calculate profit & loss and prepare statement of affairs as on 31.3.16.Statement of affairs

(as at 31st March, 2016)

Statement of Profit and Loss

(for the year ended 31st March 2016)

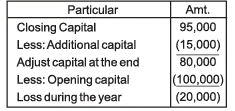

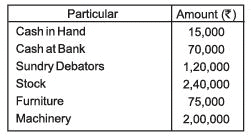

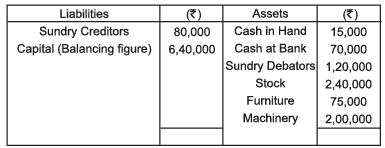

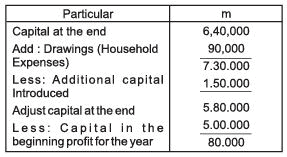

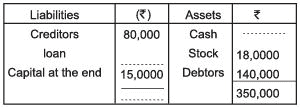

Aarushi started a business with a capital of 5,00,000, At the end of the year her position was.

Sundry creditors on this date totalled 80,000. During the year she introduced a further capital m 1,50,000 and withdrew for household expenses 90,000. A certain her profit and prepare statement of affairs at the end of year.

Statement of Profit or Loss

Illustration 4

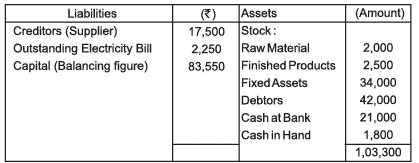

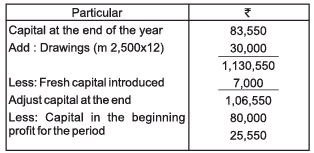

Miss Pooja runs a business. She was not maintaining her accounts on the double entry system. On April, 2015 She started the business with a capital of 80,000. One March 31,2016 her incomplete records could provide the following data.

- Amount due to suppliers of raw materials 17,500

- Stock of raw material 2,000 and finished product ? 2,500

- Fixed assets 34,000

- Amount due from customers 42,000

- She had withdrawn 2,500 per month for meeting her personal expenses.

- She had introduced 7,000 as capital during the year.

- She has cash at bank 21,000 and cash in hand 1,800

- Outstanding electricity bill 2,250

Calculate the profit / loss of her business during the year using statement of affairs method.

SOLUTIONS

STATEMENTS OF AFFAIRS as at 31st March 2016

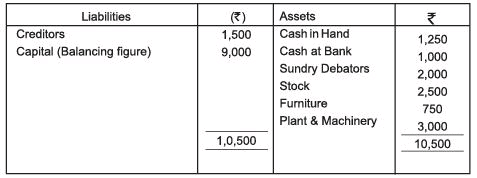

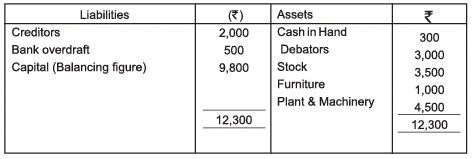

Illustration 5: Mr. Shiva keeps his book by single entry. His position on 1st April, 2015 was as follows: cash in hand 1250; Cash at bank 1,000 Debtors 2,000; Stock2,500. Furniture 750; Creditors 1,500; Plant and Machinery 3,000 His Position on 31 st March, 2016 was follows:

Cash 300, Debtors 3,000, Stock 3,500, Furniture 1,000, Plant and Machines, 4,500 Creditors2,000 Bank Overdraft500 During the year he with drew 450 for his domestic expenses and introduced 750 as fresh Capital.

STATEMENT OF AFFAIRS As on 1st April, 2015

STATEMENT OF AFFAIRS As on 1st April, 2016

STATEMENT OF PROFIT OR LOSS for the year ended 31 st march, 2016

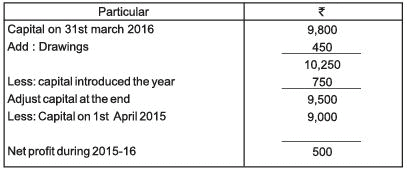

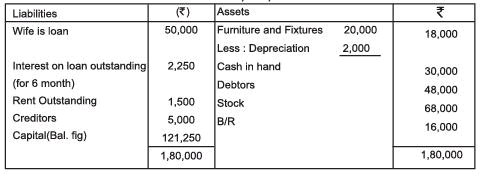

1,00,000He immediately bought furniture and fixtures for 20,000. On 30th June, he borrowed ?50,000 from his wife @ 9% p.a. (interest not yet paid) and introduced a further capital of his own amounting to 11,500. He drew at the rate of 3,000 per month at the end of each month for his household expenses. On 31 st December, 2015 his position was as follows:

Furniture and Fixtures to be depreciated by 10% Ascertain the profit or loss made by Naman Jain during 2015

Books of Naman Jain

STATEMENT OF AFFAIRS as on Dec, 31 ,2015

STATEMENT OF PROFIT OR LOSS during 2015

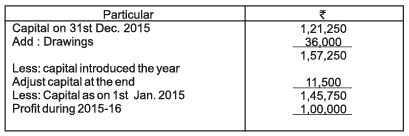

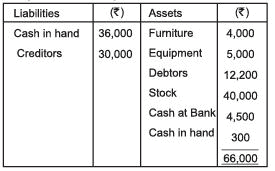

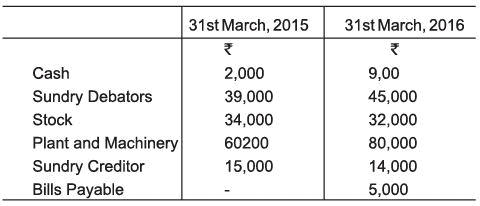

Illustration 7 : Mr. A a trader does not keep proper books of accounts. However, A provides the following particular.

31,30,2015 31,3,2016

Cash in Hand 300 4,000

Cash in Bank 4500 3,000

Stock 40,000 45,000

Debators 12,200 20,000

Equipment 5,000 5,000

Creditor 30,000 20,000

Furniture 4000 4,000

During the year 2009-10, Mr A introduced 6,000 as additional capital and withdraw 4,000 as drawings. He writes off 10% on furniture and 5% on equipment as depreciation. Prepare a statement showing the profit or loss made by him for the year ended 31 st March 2016.

STATEMENT OF AFFAIRS

as on 31,03,2016

EXERCISE

- What is meant by incomplete records systems of accounting ?

- Give any four advantages of single entry system of accounting ?

- State four points of differences between incomplete Records and Double entry system.

- Name the main accounts maintained in 'Accounts from incomplete Records'.

- Write four limitations of Incomplete Records.

PRACTICAL PROBLEMS

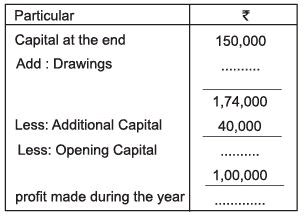

1) Himanshu Gupta who keeps his books on single entry, tells you that his capital on 31-03-2016 was Rs. 28,700 and his capital on 1 - 4-2015 was Rs. 19,200. He further informs you that during the year he withdraw for his household purposes Rs. 8,420. He sold his investments of Rs. 10,000 at 2% premium and brought that money into the business. You are required to calculate profit or loss for the year 2016.

Ans. (Profit ,720)

,720)

2. Mr. Anand started a business with a capital of Rs 4,50,000. At the end of the year his position was:

Amount (Rs)

Cash in Hand 15.000

Cash in Bank 75.000

Sundry Debtors 1.10.000

Stock 2.30.000

Furniture 55.000

Sundry creditors at this date totalled Rs 80,000 During the year he introduced a fresh Capital of Rs. 1,80,000 and withdraw for household expenses Rs. 90,000 You are required to calculate profit or loss during the year.

Ans. (Capital 580,000, Profit during the year40,000)

3. Ravi started business on Jan 01,2015 with a capital of Rs. 4,50,000 On Dec, 31,2015 his position was as under:

Cash 100,000

Bills Receivable 75,000

Stock 48,000

Land and Building 1,80,000

Furniture 50,000

He owned Rs. 45,000 to her friend Parul on that date. He withdrew Rs. 8,000 per month for household purposes. Ascertain his Profit or loss for the year ended Dec, 31,2005.

Ans. (Closing capital 4,07,000 Profit 54000)

5) Mr. Mehta keeps incomplete records his Assets and liabilities were as under.

During 20-15-16 he introduced 10,000 as new capital. He withdraw 3,000 every month for his household expenses. Ascertain his Profit for the year ended 31 st March 2016

Ans. Opening Capital 1,20,000 Closing Capital 1,38,000 Profit ^44000

6) Mrs. Pooja started with a capital of 40,000 on 1st july, 2015. She borrowed from her friend a sum of 100,000 @ 10% per annum (Interest paid) for business and brought further amount for capital 17500. On December 31,2015 her position was:

Cash 30,000

Stock 47,000

Deptor 35,000

Crechtors 30,000

She withdraw 1800 per month for the year calculate profit or loss for the year.

Ans. (Closing Capital 45,000, Profit 2300)

7) Problems based on missing information Fill in the missing figures in the following:

STATEMENT OF AFFAIRS as on 31st December, 2015

STATEMENT OF PROFIT for the year ending 31st December 2015

Ans. (Profile during the year 34,000)

|

1335 videos|1432 docs|834 tests

|

FAQs on Accounts from Incomplete Records Chapter Notes - SSC CGL Tier 2 - Study Material, Online Tests, Previous Year

| 1. What is meant by incomplete records in accounting? |  |

| 2. What are the methods used to prepare accounts from incomplete records? | |

| 3. What are the limitations of preparing accounts from incomplete records? | |

| 4. What are the advantages of preparing accounts from incomplete records? | |

| 5. How can a business improve its accounting records from incomplete to complete? | |

Previous Year

,Free

,Viva Questions

,Important questions

,Previous Year

,Summary

,Sample Paper

,Online Tests

,Online Tests

,Objective type Questions

,study material

,Previous Year

,Accounts from Incomplete Records Chapter Notes | SSC CGL Tier 2 - Study Material

,mock tests for examination

,Previous Year Questions with Solutions

,Online Tests

,video lectures

,shortcuts and tricks

,ppt

,Accounts from Incomplete Records Chapter Notes | SSC CGL Tier 2 - Study Material

,practice quizzes

,Extra Questions

,Accounts from Incomplete Records Chapter Notes | SSC CGL Tier 2 - Study Material

,Semester Notes

,MCQs

,past year papers

,Exam

;

Chapter Notes - Accounts from Incomplete Records Free PDF Download

Importance of Chapter Notes - Accounts from Incomplete Records

Chapter Notes - Accounts from Incomplete Records

Chapter Notes - Accounts from Incomplete Records SSC CGL Questions

Study Chapter Notes - Accounts from Incomplete Records on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!