Phillips Curve - Macroeconomics | Macro Economics - B Com PDF Download

The Phillips curve

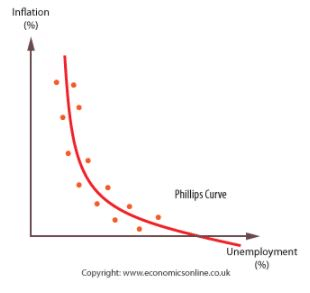

The Phillips curve shows the relationship between unemployment and inflation in an economy. Since its ‘discovery’ by British economist AW Phillips, it has become an essential tool to analyse macro-economic policy.

The Phillips curve and fiscal policy

Background

After 1945, fiscal demand management became the general tool for managing the trade cycle. The consensus was that policy makers should stimulate aggregate demand (AD) when faced with recession and unemployment, and constrain it when experiencing inflation. It was also generally believed that economies faced either inflation or unemployment, but not together - and whichever existed would dictate which macro-economic policy objective to pursue at any given time. In addition, the accepted wisdom was that it was possible to target one objective, without having a negative effect on the other. However, following publication of Phillips’ research in 1958, both of these assumptions were called into question.

Phillips analysed annual wage inflation and unemployment rates in the UK for the period 1860 – 1957, and then plotted them on a scatter diagram. The data appeared to demonstrate an inverse and stable relationship between wage inflation and unemployment. Later economists substituted price inflation for wage inflation and the Phillips curve was born. When economists from other countries undertook similar research, they also found very similar curves for their own economies.

Phillips analysed annual wage inflation and unemployment rates in the UK for the period 1860 – 1957, and then plotted them on a scatter diagram.

Explaining the Phillips curve

The curve suggested that changes in the level of unemployment have a direct and predictable effect on the level of price inflation. The accepted explanation during the 1960’s was that a fiscal stimulus, and increase in AD, would trigger the following sequence of responses:

An increase in the demand for labour as government spending generates growth.

The pool of unemployed will fall.

Firms must compete for fewer workers by raising nominal wages.

Workers have greater bargaining power to seek out increases in nominal wages.

Wage costs will rise.

Faced with rising wage costs, firms pass on these cost increases in higher prices.

Exploiting the Phillips curve

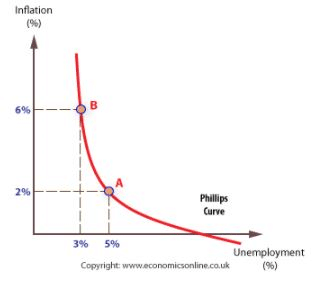

It quickly became accepted that policy-makers could exploit the trade off between unemployment and inflation - a little more unemployment meant a little less inflation.

During the 1960s and 70s, it was common practice for governments around the world to select a rate of inflation they wished to achieve, and then expand or contract the economy to obtain this target rate. This policy became known as stop-go, and relied strongly on fiscal policy to create the expansions and contractions required.

The breakdown of the Phillips curve

By the mid 1970s, it appeared that the Phillips Curve trade off no longer existed - there no longer seemed a stable pattern. The stable relationship between unemployment and inflation appeared to have broken down. It was possible to have a number of inflation rates for any given unemployment rate.

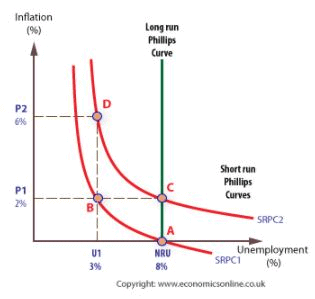

American economists Friedman and Phelps offered one explanation - namely that there is not one Phillips curve, but a series of short run Phillips Curves and a long run Phillips Curve, which exists at the natural rate of unemployment (NRU). Indeed, in the long-run, there is no trade-off between unemployment and inflation.

The new-Classical explanation – the importance of expectations

Although there are disagreements between new-Classical economists andmonetarists, the general line of argument about the breakdown of the Phillips curve runs as follows.

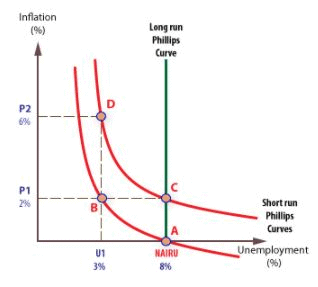

Assume that the economy starts from an equilibrium position at point A, with inflation currently at zero, and unemployment at the natural rate of 10% (NRU = 10%). Secondly, given the public’s concern with unemployment, assume the government attempts to expand the economy quickly by way of a fiscal (or monetary) stimulus, so that AD increases and unemployment falls.

Initially, the economy moves to B, and there is a fall in unemployment to 3% (at U1) as jobs are created in the short term. Having more bargaining power, workers bid-up their nominal wages. As wage costs rise, prices are driven-up to 2% (at P1). The effects of the stimulus to AD quickly wear out as inflation erodes any gains by households and firms. Real spending and output return to their previous levels, at the NRU.

According to the new-Classical view, what happens next depends upon whether the price inflation has been understood and expected – in which case there is no money illusion – or whether it is not expected – in which case, money illusion exists. If workers have bid-up their wages in nominal terms only, they have suffered from money illusion, falsely believing they will be better off – in this case, the economy will move back to point A at the NRU, but with inflation only a temporary phenomenon. However, if they understand that price inflation will erode the value of their nominal wage increases, they will bargain for a wage rise that compensates them for the price rise. Again, the economy will move back to the NRU (with unemployment at 10%), but this time carrying with it the embedded inflation rate of 2% an move to point C. The economy will hop to SRPC2 (which has a higher level of expected inflation – i.e. 2%, rather than 0%). Any further attempt to expand the economy by increasing AD will move the economy temporarily to D. However, in the long-run the economy will inevitably move back to the NRU.

The conclusion drawn was that any attempt to push unemployment below its natural rate would cause accelerating inflation, with no long-term job gains. The only way to reverse this process would be to raise unemployment above the NRU so that workers revised their expectations of inflation downwards, and the economy moved to a lower short-run Phillips curve

Using AD/AS to demonstrate the Phillips Curve effect

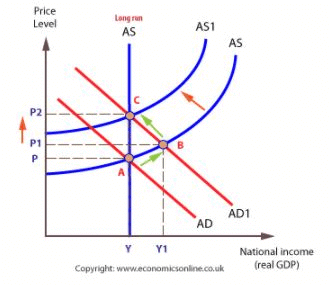

This process can also be explained through AD-AS analysis.

Assume the economy is at a stable equilibrium, at Y. An increase in government spending will shift AD from AD to AD1, leading to a rise in income to Y1, and a fall in unemployment, in the short term.

However, households will successfully predict the higher price level, and build these expectations into their wage bargaining.

As a result, wage costs rise and the AS shifts up to AS1 and the economy now moves back to Y, but with a higher price level of P2.

New Keynesian interpretation

New Keynesians explain the breakdown of the simple Phillips curve in terms of the Non-Accelerating Inflation Rate of Unemployment (NAIRU.

NAIRU

NAIRU, which exists at the Long Run Phillips Curve, is the rate of unemployment at which inflation will stabilise - in other words, at this rate of unemployment, prices will rise at the same rate each year.

Does the trade-off still exist?

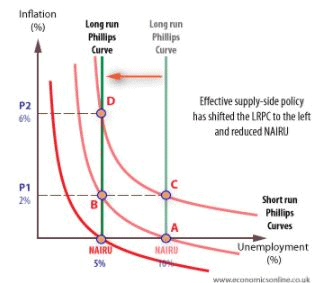

Between 1993 and 2008, unemployment fell to record lows, but inflation did not rise, as predicted by the Phillips curve. Many economists explain this by pointing to the successful supply-side policies that have been pursued over the last 20 years.

Supply-side policies

It is argued that the effectiveness of supply side policies has meant that the economy can continue to expand without inflation.

Indeed, many argue that the long run Phillips Curve still exists, but that for the UK it has shifted to the left.

UK Inflation and Unemployment - 1993 - 2017

Statistics on inflation and unemployment for the UK support the view that the extreme trade off between unemployment and inflation that occurred in the past no longer exists, with both unemployment and inflation falling between 2011 and 2016.

However, the inverse statistical relationship returned once more with unemployment falling to 4.3% in September 2017, while inflation rose back towards 3% - its highest level for 4 years. However, the cause of the inflationary episode from 2016 is more associated with the cost-push inflation that followed the fall in sterling, post-Brexit, rather than demand-pull pressures.

Up until the most recent inflationary surge, it was clear that long term supply side reforms meant that the UK could expand without experiencing the kind of demand-pull inflation associated with previous upturns in the business cycle. The improvements in labour market flexibility have helped, along with increased labour migration – both of which have eased pressure in the labour market at times of growth.

The independence of the Bank and England also played a role in ‘reducing expectations’ of inflation and weakening the link between current and future inflation. However, this does not necessarily mean that a Phillips Curve no longer exists. During the period 2007 to 2009 the Phillips Curve relationship appeared to have re-established itself, with unemployment rising and inflation falling, and again, the recent post-Brexit period is characterised by falling unemployment and rising inflation.

|

59 videos|61 docs|29 tests

|

FAQs on Phillips Curve - Macroeconomics - Macro Economics - B Com

| 1. What is the Phillips Curve in macroeconomics? |  |

| 2. How does the Phillips Curve affect monetary policy? | |

| 3. Are there any criticisms of the Phillips Curve theory? | |

| 4. How does the Phillips Curve impact the business cycle? | |

| 5. Can the Phillips Curve accurately predict future inflation and unemployment rates? | |

Summary

,past year papers

,ppt

,Phillips Curve - Macroeconomics | Macro Economics - B Com

,shortcuts and tricks

,Semester Notes

,Free

,Previous Year Questions with Solutions

,mock tests for examination

,Objective type Questions

,Phillips Curve - Macroeconomics | Macro Economics - B Com

,Phillips Curve - Macroeconomics | Macro Economics - B Com

,video lectures

,Important questions

,MCQs

,practice quizzes

,Sample Paper

,Viva Questions

,study material

,Exam

,Extra Questions

;

Phillips Curve - Macroeconomics Free PDF Download

Importance of Phillips Curve - Macroeconomics

Phillips Curve - Macroeconomics Notes

Phillips Curve - Macroeconomics B Com Questions

Study Phillips Curve - Macroeconomics on the App

|

© EduRev

|

Education Revolution

|

|