SSI Exemption - Central Excise Act,1944, Indirect Tax Laws | Indirect Tax Laws - B Com PDF Download

SSI units & Notification no.8/2003 – CE

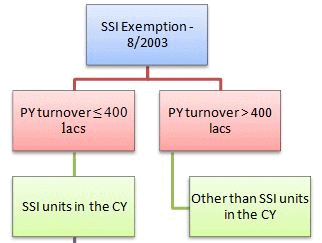

a. SSI stands for Small Scale Industries. Notification no.8/2003 provides relaxation to SSI units from central excise duty subject to certain conditions.

b. Thus, a manufacturer being an SSI unit is eligible for exemption from excise duty up to a turnover of ₹150 lacs (exemption limit) during the current year provided the turnover (aggregate clearances) in the previous year does not exceed ₹400 lacs. To reiterate, the exemption benefit would be available even if the turnover in the previous year is equal to ₹400 lacs. c. Manufacturers can make use of the exemption in the one of the following manners:

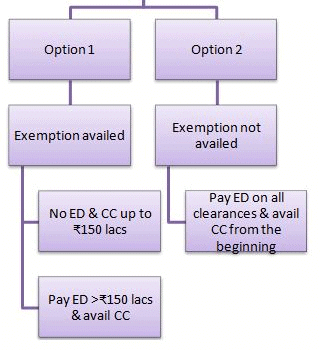

i. Claim exemption up to a turnover of ₹150 lacs, pay excise duty (ED) over this limit and avail cenvat credit (CC) on inputs once the limit exceeds.

ii. Without seeking exemption, pay full duty and claim cenvat credit on inputs from the beginning.

How is turnover/aggregate clearances of ₹400 lacs for previous year determined?

Typical format for computation:

|

Particulars ₹ Goods cleared with payment of excise duty x Non-excisable goods x Goods manufactured with brand name of others on payment of duty x Job work u/n no.214/86, 83/94, 84/94 etc x Export under bond through Merchant Exporter x |

*SSI notification no.8/2003, Job work notification no.214/86, 83/94, 84/94 etc

**EOU: 100% Export Oriented Unit; SEZ: Special Economic Zone; EHTP: Electronic Hardware Technology Park; STP: Software Technology Park; UN: United Nations

Specific exclusion from SSI exemption

SSI exemption is not applicable to the manufacturers of the following products:

a. Tea/Coffee

b. Ice-cream

c. Pan masala/Unbranded chewing tobacco

d. Sandalwood oil

e. Matches

f. Photographic plates & films

g. Stainless steel & aluminium circles

h. Refined copper & copper alloys

i. Tractors, motor vehicles, cars, chassis, motorcycles & mopeds

j. Watches (except where retail sale price is ≤ ₹500 per piece)

k. Revolvers, pistols, firearms

l. Travel sets for personal toilet m. Ceramic tiles other than those subjected to the process of printing, decorating

n. Power driven pumps for water not conforming Bureau of Indian Standards (BIS)

o. Products covered under compounded levy scheme

Declaration to be filed on reaching specified limit

a. SSI units whose turnover is more than specified limit (at present ₹90 lacs) but less than exemption limit (i.e. ₹150 lacs) have to file a declaration in the prescribed form.

b. Such declaration has to be filed only once in the lifetime of the assessee (and not every year).

Registration

SSI units whose turnover is ≤ ₹150 lacs are exempted from registration. Once the exemption limit exceeds, the unit shall compulsorily get registered with the Central Excise authorities.

Due date for payment

a. Once the turnover exceeds the exemption limit, SSI units are liable to pay ED.

b. Due date for payment of duty is 5th of the following month from the end of relevant quarter (6th in case of e-payment) for clearances during Apr-Feb, and 31st March for clearances during Mar.

c. SSI units (whether claiming benefit of exemption or not) are liable to pay ED on quarterly basis. Further, this relaxation is available for the entire financial year even if the SSI unit crosses the limit of ₹400 lacs during the current year.

Filing of return

Assessees are required to file quarterly return in ER3 on/before 10th of the following month from the end of the relevant quarter. For example, if the return pertains to I Qtr (Apr-Jun), the due date for filing ER3 would be 10th July.

Cenvat credit on capital goods

SSI units can claim cenvat credit on capital goods up to 100% in the year receipt of such goods (unlike Other-than-SSI units who are allowed 50% credit during the year of receipt).

Job work Job worker is exempt from basic excise duty if the supplier of raw material has undertaken payment of duty u/n no.214/86 (otherwise, job worker being manufacturer is liable to pay ED).

Audit

Audit of SSI units is conducted once in 2-5 years:

i. Duty range between ₹10 – 100 lacs: Once in 2 years

ii. Duty range < ₹10 lacs: Once in 5 yrs

SSI units having more than one unit

Where the SSI unit has more than one unit or place of business, the turnover of ₹400 lacs shall be calculated clubbing the turnover of all the units.

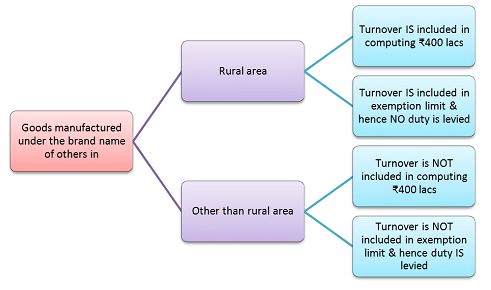

Goods manufactured under brand name of others

Where goods are manufactured under brand name of others, the inclusion of turnover under aggregate clearances limit and exemption limit are as follows:

However, the following transactions come under the purview of exemption limit even though these goods are manufactured under brand name of others. Hence the following are included in the turnover of ₹ 400 lacs:

1. Components or parts of any machinery/equipment/appliances cleared for use as original equipment in the manufacture of said machinery/equipment

2. Goods bearing brand or trade name of Khadi & Village Industries Commission

3. Goods bearing brand name of State Khadi & Village Industry Board

4. Goods bearing brand name of National Small Industries Corporation

5. Goods bearing brand name of Small Scale Industries Development Corporation or State Small Industries Corporation

6. Goods manufactured in a factory located in rural area

7. Goods like account books, registers, writing pads, file folders falling under heading 4820 or 4821 of I schedule of Central Excise Tariff Act, 1985, manufactured in a factory

8. Goods manufactured under the brand or trade name of others if these goods are in the nature of packing materials (viz. printed cartons of paper or paper board, metal containers, HDPE woven sacks, adhesive tapes, stickers, PP caps, crown corks, metal labels)

9. Printed laminated rolls bearing brand name of others 10. Plastic bottles & plastic containers used as packing material

Transactions not regarded as manufacture under brand name of others:

a. Affixing brand on school/security-agency/company/hotel readymade garments is not branding of readymade garment and such garments are eligible for SSI exemption (Circular No.947/8/2011-CX dated 21/06/2011)

b. Brand name when exclusively assigned to others for use within a particular territorial unit – SSI exemption available (Sadana Foods Vs CCE 2012 (284) ELT 257 (Tri – Bang)

|

60 videos|60 docs

|

FAQs on SSI Exemption - Central Excise Act,1944, Indirect Tax Laws - Indirect Tax Laws - B Com

| 1. What is SSI exemption under the Central Excise Act, 1944? |  |

| 2. What is the threshold limit for availing SSI exemption under the Central Excise Act, 1944? | |

| 3. How can a small-scale industry avail the SSI exemption under the Central Excise Act, 1944? | |

| 4. What are the advantages of availing SSI exemption under the Central Excise Act, 1944? | |

| 5. Are there any limitations or conditions associated with the SSI exemption under the Central Excise Act, 1944? | |

Exam

,1944

,Previous Year Questions with Solutions

,Semester Notes

,Indirect Tax Laws | Indirect Tax Laws - B Com

,Sample Paper

,Extra Questions

,ppt

,Important questions

,SSI Exemption - Central Excise Act

,SSI Exemption - Central Excise Act

,Summary

,1944

,SSI Exemption - Central Excise Act

,Viva Questions

,Free

,1944

,study material

,video lectures

,practice quizzes

,Objective type Questions

,mock tests for examination

,MCQs

,Indirect Tax Laws | Indirect Tax Laws - B Com

,shortcuts and tricks

,past year papers

,Indirect Tax Laws | Indirect Tax Laws - B Com

;

SSI Exemption - Central Excise Act,1944, Indirect Tax Laws Free PDF Download

Importance of SSI Exemption - Central Excise Act,1944, Indirect Tax Laws

SSI Exemption - Central Excise Act,1944, Indirect Tax Laws Notes

SSI Exemption - Central Excise Act,1944, Indirect Tax Laws B Com Questions

Study SSI Exemption - Central Excise Act,1944, Indirect Tax Laws on the App

|

© EduRev

|

Education Revolution

|

|