B Com Exam > B Com Notes > Auditing and Secretarial Practice > Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com PDF Download

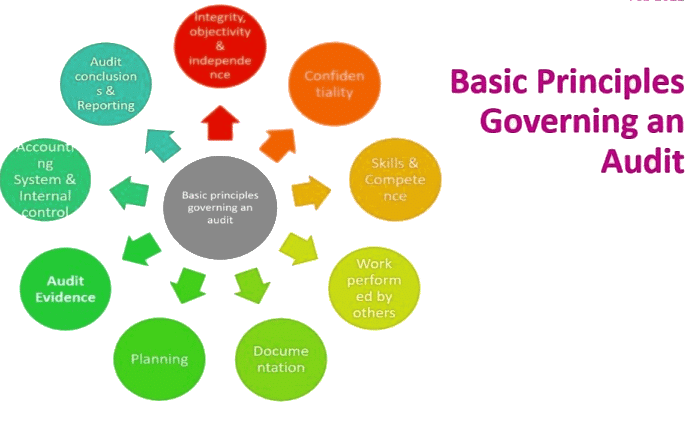

Basic Principles Governing an Audit

Audit and Assurance standards outline the fundamental principles that auditors must adhere to when conducting an audit of an organization's financial statements.

1. Integrity, Objectivity, and Independence

- Auditors must be honest, straightforward, and sincere in their approach. They have access to the entire financial records of the organization being audited and are entrusted with funds for the purpose of the audit.

- Auditors should maintain a high standard of integrity, keeping a separate account for any funds entrusted to them. Their opinions should be based on evidence rather than personal intuition, and their independence should not be questioned by the organization.

2. Confidentiality

- Auditors must maintain strict confidentiality regarding the information obtained during the audit. This information should not be disclosed to third parties unless there is a legal or professional obligation to do so with specific authority.

- Auditors should not use the information for personal gain or for the benefit of third parties.

3. Skill and Competence

- Auditors require specialized skills and competence to perform their work effectively. The audit report must be prepared with due care, and auditors should constantly update their knowledge and skills in accounting and auditing.

- The skills and competence acquired by auditors should be applied with care and diligence.

4. Work Performed by Others

- Auditors can delegate work to assistants or rely on the work of others, but they must provide proper directions and supervise the work appropriately.

- When relying on the work of another auditor, auditors should ensure the adequacy of the nature and purpose of the work and exercise caution when relying on the opinion or work of an expert.

5. Documentation

- Adequate documentation serves as evidence of the audit performed and supports the fact that the audit was conducted in accordance with basic principles.

- Maintaining working papers is useful for planning, performance, supervision, and review of the audit, and auditors are required to document matters supporting their audit work.

6. Planning

- Proper planning is essential for conducting an effective audit in an efficient and timely manner. Plans should include:

- Understanding the client's accounting system, policies, and internal control procedures.

- Establishing the expected degree of reliance on internal control.

- Determining and scheduling the nature, timing, and extent of audit procedures.

- Coordinating the work to be performed.

- Plans should be flexible and revised as needed based on audit requirements.

7. Audit Evidence

- Auditors collect evidence through tests and audit techniques to evaluate the financial statements. This includes compliance procedures to assess internal control effectiveness and substantive procedures to test transaction details and analyze ratios and trends.

- Audit evidence can be categorized into:

- Tests of details of transactions and balances.

- Analysis of ratios and trends, including inquiries into unusual fluctuations.

8. Accounting System and Internal Control

- Management should maintain an adequate accounting system with appropriate internal controls based on the size and nature of the business.

- The choice of audit techniques and extent of substantive procedures depend on the reliability of the internal control system, which is determined by its effectiveness.

- Auditors are responsible for evaluating the effectiveness of internal controls related to the accounting system to identify potential areas of material misstatement.

9. Audit Conclusions and Reporting

- Conclusions are drawn from the collected audit evidence and the auditor's understanding of the entity's business.

- Auditors should review and assess the conclusions before forming an opinion.

- The audit opinion is communicated in the audit report, which should comply with relevant statutory requirements or agreements.

There are three types of audit reports: unqualified report, qualified report, and adverse report.

Unqualified Report

- The auditor issues an unqualified report when satisfied that:

- The financial statements are prepared in accordance with generally accepted accounting principles (GAAP).

- The accounting policies have been consistently followed.

- All material matters are adequately disclosed as required by law.

Qualified Report

- A qualified report is issued when the auditor finds minor deviations from the above requirements.

Adverse Report

- An adverse report is given when there are material deviations that adversely affect the financial statements.

Disclaimer of Opinion

- If the information and explanations provided to the auditor are inadequate to form a conclusion, the auditor may disclaim from giving any opinion.

The document Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com is a part of the B Com Course Auditing and Secretarial Practice.

All you need of B Com at this link: B Com

|

54 videos|65 docs|22 tests

|

FAQs on Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice - Auditing and Secretarial Practice - B Com

| 1. What are the principles governing an audit? |  |

Ans. The principles governing an audit include independence, integrity, objectivity, professional competence and due care, confidentiality, and professional behavior. These principles ensure that auditors perform their duties with the highest level of ethics, competency, and confidentiality.

| 2. Why is independence important in an audit? | |

Ans. Independence is important in an audit because it ensures that auditors are free from any bias or undue influence that could compromise their objectivity and professional judgment. It allows auditors to provide an unbiased and objective opinion on the financial statements and enhances the credibility of the audit process.

| 3. What is the role of integrity in auditing? | |

Ans. Integrity is a fundamental principle in auditing that requires auditors to be honest, fair, and credible in their professional conduct. Auditors with integrity adhere to ethical standards, maintain professional skepticism, and provide reliable and trustworthy audit opinions.

| 4. How does professional competence and due care contribute to an effective audit? | |

Ans. Professional competence and due care require auditors to possess the necessary knowledge, skills, and expertise to perform their audit engagements effectively. It ensures that auditors stay updated with the latest auditing standards, regulations, and industry practices to provide high-quality audit services.

| 5. Why is confidentiality important in auditing? | |

Ans. Confidentiality is crucial in auditing as it ensures that auditors keep all the information obtained during the audit process confidential. It helps to maintain the trust of the audited entity and protects sensitive financial and non-financial information from unauthorized disclosure. Confidentiality also promotes open communication between auditors and their clients.

About this Document

3K Views

4.94/5

Rating

Oct 05, 2025

Last updated

Related Exams

Document Description: Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice for B Com 2025 is part of Auditing and Secretarial Practice preparation.

The notes and questions for Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice have been prepared according to the B Com exam syllabus. Information about Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice covers topics

like Basic Principles Governing an Audit and Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice Example, for B Com 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice.

Introduction of Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice in English is available as part of our Auditing and Secretarial Practice

for B Com & Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice in Hindi for Auditing and Secretarial Practice course.

Download more important topics related with notes, lectures and mock test series for B Com

Exam by signing up for free. B Com: Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com

Description

Full syllabus notes, lecture & questions for Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com - B Com | Plus excerises question with solution to help you revise complete syllabus for Auditing and Secretarial Practice | Best notes, free PDF download

Information about Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice

In this doc you can find the meaning of Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice defined & explained in the simplest way possible. Besides explaining types of

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice theory, EduRev gives you an ample number of questions to practice Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice tests, examples and also practice B Com

tests

Related Searches

ppt

,practice quizzes

,Extra Questions

,Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com

,Principles Governing an Audit - Auditing Concepts

,Exam

,Principles Governing an Audit - Auditing Concepts

,MCQs

,Principles Governing an Audit - Auditing Concepts

,Viva Questions

,Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com

,Summary

,study material

,Semester Notes

,shortcuts and tricks

,mock tests for examination

,video lectures

,past year papers

,Free

,Sample Paper

,Important questions

,Previous Year Questions with Solutions

,Auditing & Secretarial Practice | Auditing and Secretarial Practice - B Com

,Objective type Questions

;

Additional Information about Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice for B Com Preparation

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice Free PDF Download

The Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice is an invaluable resource that delves deep into the core of the B Com exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice now and kickstart your journey towards success in the B Com exam.

Importance of Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice

The importance of Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice cannot be overstated, especially for B Com aspirants.

This document holds the key to success in the B Com exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice Notes

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice Notes on EduRev are your ultimate resource for success.

Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice B Com Questions

The "Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice B Com Questions" guide is a valuable resource for all aspiring students preparing for the

B Com exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice on the App

Students of B Com can study Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Principles Governing an Audit - Auditing Concepts, Auditing & Secretarial Practice is prepared as per the latest B Com syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup