Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities | Auditing and Secretarial Practice - B Com PDF Download

Goodwill

What It Is:

Goodwill is the excess of purchase price over the fair market value of a company's identifiable assets and liabilities.

How It Works (Example):

Goodwill is created when one company acquires another for a price higher than the fair market value of its assets; for example, if Company A buys Company B for more than the fair value of Company B's assets and debts, the amount left over is listed on Company A's balance sheet as goodwill.

The account for goodwill is located in the assets section of a company’s balance sheet. It is an intangible asset,as opposed to physical assets like buildings and equipment.

Goodwill is an accounting construct that is required under Generally Accepted Accounting Principles (GAAP).The concept can be best illustrated with an example:

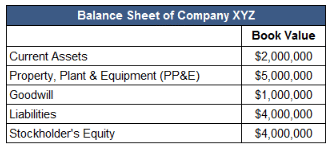

Assume that Company ABC wants to acquire Company XYZ. ABC purchases all of the outstanding stock of XYZ for $8,000,000. On the acquisition date, Company XYZ lists the following assets and liabilities:

An appraisal estimates the fair market value (FMV) of the PP&E at $7 million. The book value of all the other assets and liabilities is equal to FMV.

The fair value of XYZ's assets and liabilities is $2,000,000 + $7,000,000 - $4,000,000 = $5,000,000. We leave out the goodwill listed on XYZ's balance sheet because it's not a real asset being purchased by ABC -- it's an accounting construct XYZ was required to list pursuant to a prior acquisition.

ABC paid $8,000,000 for the stock, so on its next balance sheet, ABC will list an account called Goodwill that will have a value of $3,000,000.

The stock of many well-known companies is worth more than the value of their assets. To cite notable examples, the majority of Coca-Cola's share value is not in its brick-and-mortar bottling plants, but instead in the brand name and "secret formula" of its storied soft drink brand.

Why It Matters:

Even though goodwill is listed as an asset, it can't be bought or sold. Many analysts prefer to not consider it when they are examining a firm's assets. One commonly used measure is "tangible book value," which excludes non-cash balance sheet items like goodwill and amortization.

The appropriate value of goodwill is very hard to define. It is possible for an acquiring company to pay too much for the acquiree, and if the acquired net assets fall in value, the acquiring company must write them down (a process called "impairment"). Impairment charges flow to the income statement, and will negatively affect EPS and the firm's stock price.

Inventory

What It Is:

Inventory is the collection of unsold products waiting to be sold. Inventory is listed as a current asset on a company's balance sheet.

How It Works (Example):

Inventory is commonly thought of as the finished goods a company accumulates before selling them to end users. But inventory can also describe the raw materials used to produce the finished goods, goods as they go through the production process (referred to as "work-in-progress" or WIP), or goods that are "in transit.

There are generally five reasons companies maintain inventories:

- To meet an anticipated increase in demand;

- To protect against unanticipated increases in demand;

- To take advantage of price breaks for ordering raw materials in bulk;

- To prevent the idling of a whole factory if one part of the process breaks down; and,

- To keep a steady stream of material flowing to retailers rather than making a single shipment of goods to retailers.

Inventory can also be used as collateral to obtain financing in some cases.

The basic requirement for counting an item in inventory is economic control rather than physical possession. Therefore, when a company purchases inventory, the item is included in the purchaser's inventory even if the purchaser does not have physical possession of those items.

Inventory is usually classified in its own category as an asset on the balance sheet, following receivables. It is important to note that the balance sheet's inventory account should also reflect costs directly or indirectly incurred in making an item ready for sale,including the purchase price of the item as well as the freight, receiving, unpacking, inspecting, storage, maintenance, insurance, taxes,and other costs associated with it.

Why It Matters:

Inventory is a key component of calculating cost of goods sold (COGS) and is a key driver of profit, total assets, and tax liability. Many financial ratios, such as inventory turnover, incorporate inventory values to measure certain aspects of the health of a business.

For these reasons, and because changes in commodity and other materials prices affect the value of a company's inventory, it is important to understand how a company accounts for its inventory. Common inventory accounting methods include first in, first out (FIFO), last in, first out (LIFO), and lower of cost or market (LCM). Some industries, such as the retail industry, tailor these methods to fit their specific circumstances. Public companies must disclose their inventory accounting methods in the notes accompanying their financial statements.

Given the significant costs and benefits associated with inventory, companies spend considerable amounts of time calculating what the optimal level of inventory should be at any given time, and changes in inventory levels can send mixed messages to investors. Increases in inventory may signal that a company is not selling effectively, is anticipating increased sales in the near future (such as during the holidays), or has an inefficient purchasing department.

Declining inventories may signal that the company is selling more than it expected, has a backlog, is experiencing a blockage in its supply chain, is expecting lower sales, or is becoming more efficient in its purchasing activity.

Because there are several ways to account for inventory and because some industries require more inventory than others, comparison of inventories is generally most meaningful among companies within the same industry using the same inventory accounting methods, and the definition of a "high" or "low" inventory level should be made within this context.

Investments

A company’s balance sheet may show funds it has invested in other companies. Investments appear on a balance sheet in several ways: as common or preferred shares, mutual funds and notes payable.

Common shares : Common shares are issued to business owners and other investors as proof of the money they have paid into a company. Of all shareholders, common shareholders have the least claim on a company’s assets.

Preferred shares : Preferred shares are issued to business owners and other investors as proof of the money they have paid into a company.

Mutual Funds : A mutual fund is a professionally-managed investment scheme, usually run by an asset management company that brings together a group of people and invests their money in stocks, bonds and other securities.

Notes payable are long-term liabilities that indicate the money a company owes its financiers—banks and other financial institutions as well as other sources of funds such as friends and family. They are long-term because they are payable beyond 12 months, though usually within five years.

Sometimes they are made to put excess cash to work for short periods. Other times they are used more strategically over longer periods.

For small businesses, short-term investments are typically placed in highly liquid money-market funds and/or in interest-bearing bank accounts. Longer term investments could entail the purchase of shares in a private business. These can be highly illiquid and could be made to have some control over an important relationship (for example., with a supplier or large customer).

Investments held for one year or more appear as long-term assets on the balance sheet. Investments used to generate cash within the current operating period (within 12 months) appear as current assets and are called “treasury balances” or “marketable securities.

|

54 videos|65 docs|22 tests

|

FAQs on Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities - Auditing and Secretarial Practice - B Com

| 1. What is the difference between goodwill, inventory, and investments? |  |

| 2. How are goodwill, inventory, and investments verified? | |

| 3. How are goodwill, inventory, and investments valued? | |

| 4. What are the implications of overvalued or undervalued goodwill, inventory, and investments? | |

| 5. How do changes in the value of goodwill, inventory, and investments affect a company's financial statements? | |

past year papers

,Semester Notes

,Inventory & Investments - Verification and Valuation of Assets and Liabilities | Auditing and Secretarial Practice - B Com

,Goodwill

,Viva Questions

,Important questions

,MCQs

,video lectures

,Extra Questions

,Sample Paper

,Exam

,study material

,practice quizzes

,Free

,Previous Year Questions with Solutions

,Inventory & Investments - Verification and Valuation of Assets and Liabilities | Auditing and Secretarial Practice - B Com

,ppt

,Objective type Questions

,shortcuts and tricks

,Goodwill

,Goodwill

,Summary

,mock tests for examination

,Inventory & Investments - Verification and Valuation of Assets and Liabilities | Auditing and Secretarial Practice - B Com

;

Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities Free PDF Download

Importance of Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities

Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities Notes

Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities B Com Questions

Study Goodwill, Inventory & Investments - Verification and Valuation of Assets and Liabilities on the App

|

© EduRev

|

Education Revolution

|

|