B Com Exam > B Com Notes > Accountancy and Financial Management > Statement of Financial Position (Balance Sheet) - Financial Analysis and Management

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com PDF Download

The Statement of Financial Position

- The Statement of Financial Position shows the financial structure of a business at a specific point in time

- It identifies a businesses assets and liabilities and specifies the capital (equity) used to fund the business

- The Statement of Financial Position is also known as the Balance Sheet

- It is called the balance sheet, as net assets should equal the total equity

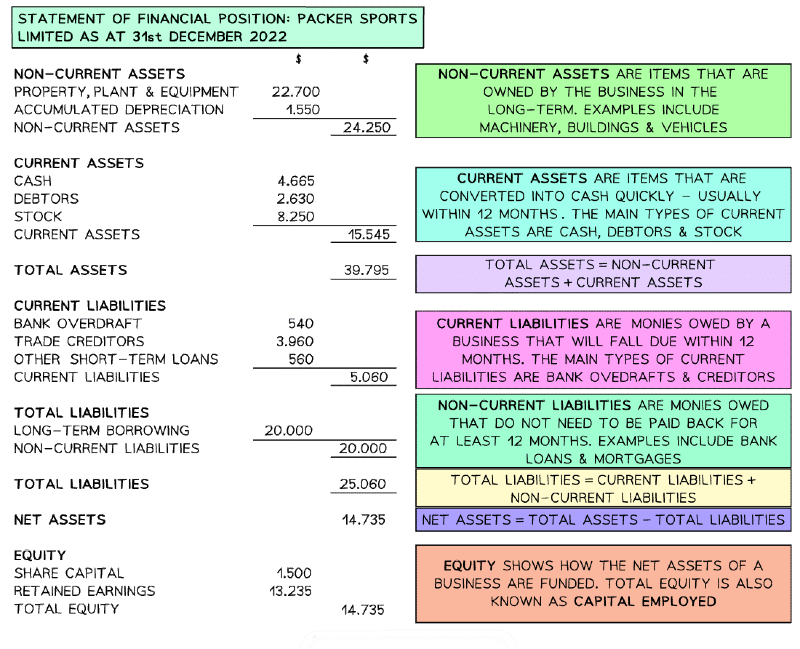

The statement of financial position

Calculating the total assets

- On the stated date Packer Sports Ltd owned non-current assets worth $24,250

- It owns property, plant and machinery that is valued at $22,700

- These assets have been depreciated by $1,550

- The value of its current assets was $15,545, comprised of cash, debtors and stock

- Total assets were therefore

$ 24 comma 250 plus $ 15 comma 545 space equals space $ 39 comma 795

Calculating total liabilities

- On the stated date Packer Sports Ltd had current liabilities worth $5,060, comprised of a bank overdraft, trade creditors and other short-term loans

- The value of its long-term liabilities were $20,000

- Total liabilities were therefore

$ 5 comma 060 space plus space $ 20 comma 000 space equals space $ 25 comma 060

Calculating the net assets

- Packer Sports Limited's net assets were therefore

$ 39, 795 - $ 25 comma 060 space equals space $ 14 comma 735

Calculating total equity

- Net assets of $14,735 were funded through share capital of $1,500 and retained earnings of $13,235

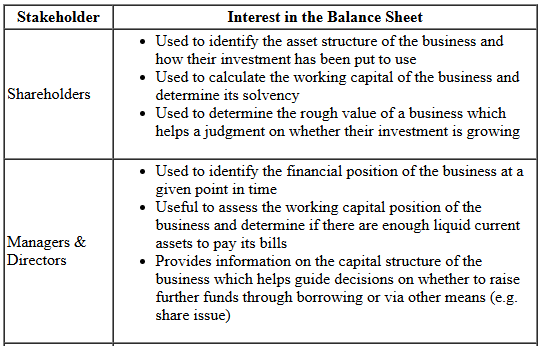

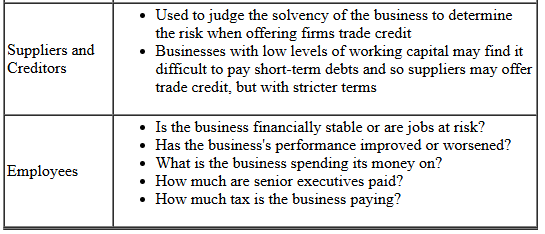

How Stakeholders use the Statement of Financial Position

Stakeholders will use the Statement of Financial Position alongside the Statement of Profit or Loss to perform ratio analysis and compare performance over time or with other businesses

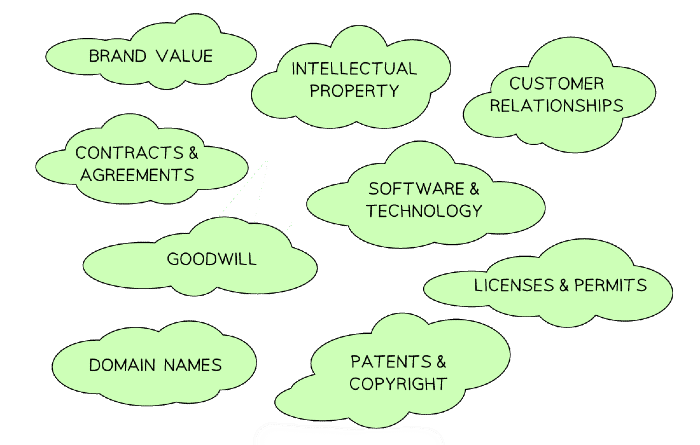

Different types of Intangible Assets

- Intangible assets are non-physical assets that cannot physically be held but hold value for a business

- Businesses need to account for intangible assets in their annual reports as it adds to the value of the business

Intangible assets

Intellectual property

- This includes patents, trademarks, patents and copyrights which protect unique ideas, inventions, artistic works, and brand names

Brand value

- The reputation and recognition associated with a brand has a value

- It includes the brand name, logo, slogans, and customer loyalty to the brand

Customer relationships

- Long-term relationships with customers including customer lists, contracts, and customer loyalty programs

- These relationships can provide recurring revenue and a competitive advantage

Software and technology

- Proprietary software, computer programs and technology systems that are crucial to a business's operations or provide a competitive advantage

Contracts and agreements

- Long-term contracts, lease agreements, licensing agreements and franchise agreements that have value and contribute to future cash flows

- Agreements with employees or business partners that restrict them from competing with the company for a specific period which protect the company's interests and market position (non compete contract)

Goodwill

- The value of a company's reputation, customer base and brand

- Goodwill often represents the premium paid when one business takes over or merges with another business

Domain names and other online assets

- Valuable domain names, websites, social media accounts and online platforms that drive customer engagement, traffic, and online presence

Licenses and permits

- Licenses, permits, and regulatory approvals that grant exclusive rights or access to certain markets or resources, often issued by governments

The document Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com is a part of the B Com Course Accountancy and Financial Management.

All you need of B Com at this link: B Com

|

61 videos|79 docs|12 tests

|

FAQs on Statement of Financial Position (Balance Sheet) - Financial Analysis and Management - Accountancy and Financial Management - B Com

| 1. What is a Statement of Financial Position (Balance Sheet)? |  |

Ans. A Statement of Financial Position, also known as a Balance Sheet, is a financial statement that provides a snapshot of a company's financial health at a specific point in time. It presents the company's assets, liabilities, and shareholders' equity, representing what the company owns, owes, and the residual interest of its owners, respectively. This statement helps in assessing the company's financial stability and measuring its ability to meet its financial obligations.

| 2. What is the purpose of financial analysis and management? | |

Ans. Financial analysis and management involve evaluating a company's financial performance, making informed decisions, and implementing strategies to maximize profitability, liquidity, and efficiency. The purpose is to assess the company's financial health, identify areas for improvement, and make sound financial decisions for the long-term success of the business. Financial analysis and management help stakeholders understand the company's financial position, make investment decisions, and plan for the future.

| 3. What does the "B Com" qualification refer to in the article title? | |

Ans. "B Com" refers to the Bachelor of Commerce degree, which is an undergraduate program focused on developing a strong foundation in various areas of business, finance, accounting, and economics. The article title indicates that the content is related to financial analysis and management within the context of the Bachelor of Commerce program. Students pursuing this degree gain knowledge and skills in financial analysis, accounting principles, and financial management, enabling them to understand and interpret financial statements like the Statement of Financial Position.

| 4. What are some common items found in a Statement of Financial Position? | |

Ans. A Statement of Financial Position includes various items that provide insights into a company's financial status. Some common items found in this statement include:

- Current assets: Cash, accounts receivable, inventory, prepaid expenses, etc.

- Non-current assets: Property, plant, and equipment, intangible assets, long-term investments, etc.

- Current liabilities: Accounts payable, accrued expenses, short-term loans, etc.

- Non-current liabilities: Long-term debt, deferred tax liabilities, etc.

- Shareholders' equity: Common stock, retained earnings, additional paid-in capital, etc.

| 5. How can a Statement of Financial Position be used for financial decision making? | |

Ans. The Statement of Financial Position provides crucial information for financial decision making. It helps stakeholders assess a company's liquidity, solvency, and financial stability, guiding their decisions. For example, potential investors can analyze the statement to evaluate the company's financial health before making investment decisions. Lenders use this statement to assess creditworthiness and determine the interest rates for loans. Managers use the statement to track financial performance, identify areas of improvement, and make informed decisions about resource allocation, investments, and financing options.

About this Document

2.1K Views

4.87/5

Rating

Oct 15, 2025

Last updated

Related Exams

Document Description: Statement of Financial Position (Balance Sheet) - Financial Analysis and Management for B Com 2025 is part of Accountancy and Financial Management preparation.

The notes and questions for Statement of Financial Position (Balance Sheet) - Financial Analysis and Management have been prepared according to the B Com exam syllabus. Information about Statement of Financial Position (Balance Sheet) - Financial Analysis and Management covers topics

like How Stakeholders use the Statement of Financial Position, Different types of Intangible Assets and Statement of Financial Position (Balance Sheet) - Financial Analysis and Management Example, for B Com 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Statement of Financial Position (Balance Sheet) - Financial Analysis and Management.

Introduction of Statement of Financial Position (Balance Sheet) - Financial Analysis and Management in English is available as part of our Accountancy and Financial Management

for B Com & Statement of Financial Position (Balance Sheet) - Financial Analysis and Management in Hindi for Accountancy and Financial Management course.

Download more important topics related with notes, lectures and mock test series for B Com

Exam by signing up for free. B Com: Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com

Description

Full syllabus notes, lecture & questions for Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com - B Com | Plus excerises question with solution to help you revise complete syllabus for Accountancy and Financial Management | Best notes, free PDF download

Information about Statement of Financial Position (Balance Sheet) - Financial Analysis and Management

In this doc you can find the meaning of Statement of Financial Position (Balance Sheet) - Financial Analysis and Management defined & explained in the simplest way possible. Besides explaining types of

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management theory, EduRev gives you an ample number of questions to practice Statement of Financial Position (Balance Sheet) - Financial Analysis and Management tests, examples and also practice B Com

tests

Related Searches

Semester Notes

,past year papers

,Summary

,video lectures

,Viva Questions

,study material

,Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com

,Important questions

,Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com

,Extra Questions

,Objective type Questions

,mock tests for examination

,Free

,practice quizzes

,Previous Year Questions with Solutions

,shortcuts and tricks

,Sample Paper

,ppt

,MCQs

,Exam

,Statement of Financial Position (Balance Sheet) - Financial Analysis and Management | Accountancy and Financial Management - B Com

,

Additional Information about Statement of Financial Position (Balance Sheet) - Financial Analysis and Management for B Com Preparation

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management Free PDF Download

The Statement of Financial Position (Balance Sheet) - Financial Analysis and Management is an invaluable resource that delves deep into the core of the B Com exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Statement of Financial Position (Balance Sheet) - Financial Analysis and Management now and kickstart your journey towards success in the B Com exam.

Importance of Statement of Financial Position (Balance Sheet) - Financial Analysis and Management

The importance of Statement of Financial Position (Balance Sheet) - Financial Analysis and Management cannot be overstated, especially for B Com aspirants.

This document holds the key to success in the B Com exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management Notes

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Statement of Financial Position (Balance Sheet) - Financial Analysis and Management.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Statement of Financial Position (Balance Sheet) - Financial Analysis and Management Notes on EduRev are your ultimate resource for success.

Statement of Financial Position (Balance Sheet) - Financial Analysis and Management B Com Questions

The "Statement of Financial Position (Balance Sheet) - Financial Analysis and Management B Com Questions" guide is a valuable resource for all aspiring students preparing for the

B Com exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Statement of Financial Position (Balance Sheet) - Financial Analysis and Management on the App

Students of B Com can study Statement of Financial Position (Balance Sheet) - Financial Analysis and Management alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Statement of Financial Position (Balance Sheet) - Financial Analysis and Management,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Statement of Financial Position (Balance Sheet) - Financial Analysis and Management is prepared as per the latest B Com syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup