Issue of Debentures - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com PDF Download

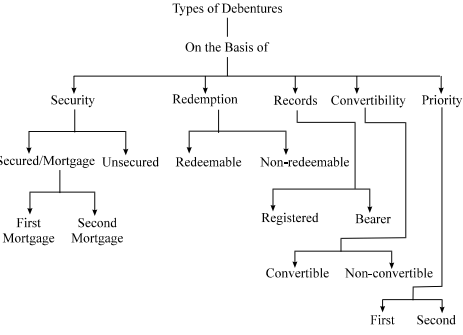

Debentures and Its Types

A Debenture is a unit of loan amount. When a company intends to raise the loan amount from the public it issues debentures. A person holding debenture or debentures is called a debenture holder. A debenture is a document issued under the seal of the company. It is an acknowledgment of the loan received by the company equal to the nominal value of the debenture. It bears the date of redemption and rate and mode of payment of interest. A debenture holder is the creditor of the company.

| As per section 2(12) of Companies Act 1956, “Debenture includes debenture stock, bond and any other securities of the company whether constituting a charge on the company’s assets or not”. |

Types of debentures

Debenture can be classified as under :

1. From security point of view

(i) Secured or Mortgage debentures : These are the debentures that are secured by a charge on the assets of the company. These are also called mortgage debentures. The holders of secured debentures have the right to recover their principal amount with the unpaid amount of interest on such debentures out of the assets mortgaged by the company. In India, debentures must be secured. Secured debentures can be of two types :

(a) First mortgage debentures : The holders of such debentures have a first claim on the assets charged.

(b) Second mortgage debentures : The holders of such debentures have a second claim on the assets charged.

(ii) Unsecured debentures : Debentures which do not carry any security with regard to the principal amount or unpaid interest are called unsecured debentures. These are called simple debentures.

2. On the basis of redemption

(i) Redeemable debentures : These are the debentures which are issued for a fixed period. The principal amount of such debentures is paid off to the debenture holders on the expiry of such period. These can be redeemed by annual drawings or by purchasing from the open market.

(ii) Non-redeemable debentures : These are the debentures which are not redeemed in the life time of the company. Such debentures are paid back only when the company goes into liquidation.

3. On the basis of Records

(i) Registered debentures : These are the debentures that are registered with the company. The amount of such debentures is payable only to those debenture holders whose name appears in the register of the company.

(ii) Bearer debentures : These are the debentures which are not recorded in a register of the company. Such debentures are transferrable merely by delivery. Holder of these debentures is entitled to get the interest.

4. On the basis of convertibility

(i) Convertible debentures : These are the debentures that can be converted into shares of the company on the expiry of predecided period. The term and conditions of conversion are generally announced at the time of issue of debentures.

(ii) Non-convertible debentures : The debenture holders of such debentures cannot convert their debentures into shares of the company.

5. On the basis of priority

(i) First debentures : These debentures are redeemed before other debentures.

(ii) Second debentures : These debentures are redeemed after the redemption of first debentures.

Issue of Debentures

By issuing debentures means issue of a certificate by the company under its seal which is an acknowledgment of debt taken by the company.

The procedure of issue of debentures by a company is similar to that of the issue of shares. A Prospectus is issued, applications are invited, and letters of allotment are issued. On rejection of applications, application money is refunded. In case of partial allotment, excess application money may be adjusted towards subsequent calls.

Issue of Debenture takes various forms which are as under :

1. Debentures issued for cash

2. Debentures issued for consideration other than cash

3. Debentures issued as collateral security.

Further, debentures may be issued

(i) at par,

(ii) at premium, and

(iii) at discount

Accounting treatment of issue of debentures for cash

1. Debentures issued for cash at par :

Following journal entries will be made :

(i) Application money is received

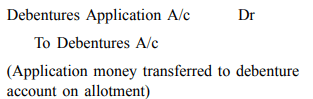

(ii) Transfer of debentures application money to debentures account on their allotment

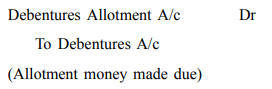

(iii) Money due on allotment

(iv) Money due on allotment is received

(v) First and final call is made

(vi) Debentures First and Final call money is received

Note : Two calls i.e. first call and second call may be made

Journal entries will be made on the lines made for first and final call

Illustration 1

Shining India Ltd. issued 5000 8% Debentures of Rs 100 each payable as follows

Rs 20 on Application

Rs 30 on Allotment

Rs. 50 on First and Final call

All the debentures were applied for and allotted. All the calls were duly received. Make necessary journal entries in the books of the company.

Solution :

Shining India Ltd.

|

S.No. |

Particulars |

Dr LF Rs |

Cr Amount Rs |

Amount |

|

1. |

Bank A/c ...Dr |

|

100000 |

|

|

|

To Debentures Application A/c |

|

|

100000 |

|

|

(Application money received for 5000 debentures) |

|

|

|

|

2. |

Debentures Application A/c Dr |

|

100000 |

|

|

|

To 8% Debentures A/c |

|

|

100000 |

|

|

(Application money transferred to Debentures A/c on allotment) |

|

|

|

|

3. |

Debentures Allotment a/c Dr |

|

150000 |

|

|

|

To 8% Debentures A/c |

|

|

150000 |

|

|

(Allotment money due on 5000 debentures @ Rs 30 per debenture) |

|

|

|

|

4. |

Bank A/c Dr |

|

150000 |

|

|

|

To Debentures Allotment A/c |

|

|

150000 |

|

|

(Allotment money received) |

|

|

|

|

5. |

Debentures First and Final call A/cDr |

|

250000 |

|

|

|

To 8% Debentures A/c |

|

|

250000 |

|

|

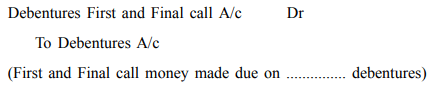

(Debentures first and final call money made due @ Rs 50 per debenture) |

|

|

|

|

6. |

Bank hie Dr |

|

250000 |

|

|

|

To Debentures First and Final call A/e |

|

|

250000 |

|

|

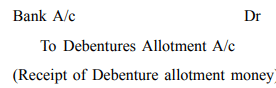

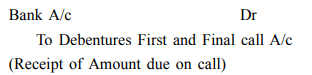

(Receipt of Debentures first and final call money) |

|

|

|

Over subscription

Company if receives applications for number of debentures that exceed the number of debentures offered for subscription, it is called over subscription. There can be following treatment of the excess application money received :

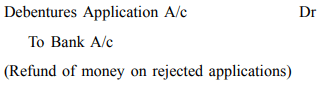

(a) The total amount of excess number of applications is refunded in case the applications are totally rejected.

(b) The amount of excess application money is totally adjusted towards amount due on allotment and calls

— in case partial allotment is made,

— the excess amount is adjusted towards sums due on allotment and rest of the amount is refunded.

Journal entries in the above cases will be as follows :

For refund of money if the applications are rejected

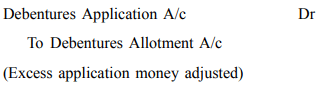

For adjustment of excess application money adjusted towards sum due on allotment

Illustration 2

ABC Ltd issued 5000 10% Debentures of Rs 100 each payable as Rs 40 on application and Rs 60 on allotment. Applications were received for 6000 debentures. Applicants for 500 debentures were sent letter of regret and money was returned. Allotment was made proportionately to the remaining applicants. Over subscription was applied to the amount due on allotment. All money was duly received.

Make journal entries for the above transactions in the books of the company

Solution : Journal entries

|

Date |

Particulars |

LF |

Dr Amount Rs |

Cr Amount Rs |

|

1. |

Bank A/c Dr To Debentures Application A/c |

|

240000 |

240000 |

| (Application money received ibr 6000 debentures @ Rs 40 per debenture) | ||||

| 2. |

Debentures Application A/c Dr To 10% Debentures A/c To Bank A/c To Debentures Allotment A/c |

240000 |

200000 20000 20000 |

|

| (Debenture application money of 5000 debentures transferred to debenture A/c on their allotment of 500 debentures returned and balance of 500 adjusted towards allotment) | ||||

| 3. |

Debentures Allotment A/c Dr To 10% Debentures A/c |

300000 | 300000 | |

| (Allotment money due on 5000 debentures @ Rs 60 per debenture) | ||||

| 4. |

Bank A/c Dr To Debentures Allotment A/c |

280000 | 280000 | |

| (Allotment money received) |

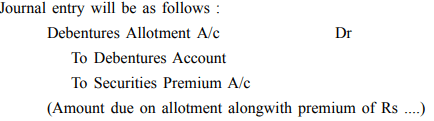

Issue of Debentures at Premium and at Discount

Debentures are said to be issued at premium when these are issued at a value which is more than their nominal value. For example, a debenture of Rs 100 is issued at Rs 110. This excess amount of Rs 10 is the amount of premium. The premium on the issue of debentures is credited to the Securities Premium A/c as per section 78 of the Companies Act, 1956.

Illustration 3

A company has issued 5000 10% Debentures of Rs 100 each at a premium of 20% payable as Rs 60 on application Rs 60 on allotment (including premium)

All the debentures were subscribed for and money was duly received. Make journal entries.

Solution

Journal entries

|

|

|

|

Dr |

Cr |

|

Dale |

Particulars |

LF |

Amount |

Amount |

|

1 |

Bank Avc Dr |

|

300000 |

|

|

|

To Debentures Application A/c |

|

|

300000 |

|

|

(Application money received) |

|

|

|

|

2. |

Debentures Application A/c Dr |

|

300000 |

|

|

|

To 1 Olo Debentures A/c |

|

|

300000 |

|

|

(Application money transferred to Debenture A/c) |

|

|

|

|

3. |

Debentures Allotment A/c |

|

300000 |

|

|

|

To 10% Debentures A/e |

|

|

200000 |

|

|

To Securities Premium A/c |

|

|

100000 |

|

|

(Amount due on allotment along with premium) |

|

|

|

|

4. |

Bank A'c Dr |

|

300000 |

|

|

|

To Debentures Allotment A/c |

|

|

300000 |

|

|

(Allotment money received) |

|

|

|

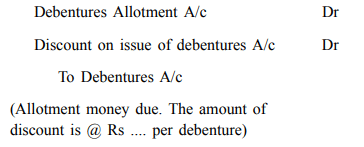

Issue of Debentures at Discount

When debentures are issued at less than their nominal value they are said to be issued at discount. For example, debenture of Rs 100 each is issued at Rs 90 per debenture. Companies Act, 1956 has not laid down any conditions for the issue of debentures at a discount as have been laid down in case of issue of shares at discount. However, there should be provision for issue of such debentures in the Articles of Association of the Company.

Journal entry for issue of debentures at discount (at the time of allotment)

Illustration 4

A company has issued 2000 9% debentures of Rs 100 each at a discount of 10% payable as

Rs 40 on application

Rs 50 on allotment

Make necessary journal entries.

Solution

|

|

|

|

|

Dr |

Cr |

|

Dale |

Particulars |

|

LF |

Amount |

Amount |

|

1. |

Bank Ac |

Dr |

|

80000 |

|

|

|

To Debentures Application A'c |

|

|

|

80000 |

|

|

(Application money received) |

|

|

|

|

|

2. |

Debentures Application A/c |

Dr |

|

80000 |

|

|

|

To 9% Debentures A/c |

|

|

|

80000 |

|

|

(Application money transferred to debenture A/c) |

|

|

|

|

|

3. |

Debentures Allotment A'c |

Dr |

|

100000 |

|

|

|

Debentures Discount A/e |

Dr |

|

20000 |

|

|

|

To 9% Debenture A/e |

|

|

|

120000 |

|

|

(Amount due on allotment, along with discount amount Rs 10 per debenture) |

|

|

|

|

|

4. |

Bank A/c |

Dr |

|

100000 |

|

|

|

To Debentures Allotment |

|

|

|

100000 |

|

|

(Receipt of allotment money) |

|

|

|

|

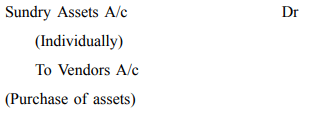

Issue of Debentures for consideration other than cash

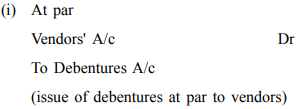

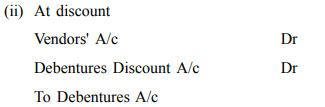

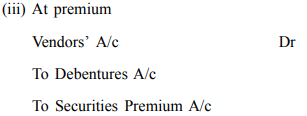

When a company purchases some assets and issues debentures as a payment for the purchase, to the vendors it is known as issue of debentures for consideration other than cash. Debentures can be issued to vendors at par, at premium and at discount

Accounting Treatment :

1. Purchase of Assets

2. Allotment of debentures

(Issue of debentures to vendors at a discount of Rs ... per debenture)

(issue of debentures to vendors at a premium of Rs .... per debenture)

Illustration 5

M.B. Electronics Ltd. purchased machinery for Rs 198000 and issued 9% debentures of Rs 100 each to the vendors. Make journal entries if the debentures were issued

(a) at par

(b) at a premium of Rs 10

(c) at a discount of Rs 10

Solution :

|

S.No. |

Particulars |

Dr Amount Rs |

Cr Amount Rs |

|

(a) |

Maehinary A/c ...Dr To Vendors Ac {Machine purchased) |

198000 |

198000 |

|

(b) |

Vendors A/c Dr To 9% Debentures A/c 1980 debentures of Rs 100 each issued to vendors |

198000 |

1980000 |

|

(c) |

Vendors A/c Dr |

198000 |

|

|

|

To 9% Debentures A/c |

|

180000 |

|

|

To Securities Premium A/c |

|

18000 |

|

|

(1800 debentures issued at a premium of Rs 10 per debenture) |

|

|

Working notes

Amount due = Rs 198000

Value of debenture including Rs 10 for premium = Rs 110

∴ Debenture amount (Nominal value) = 1800 × 100 = Rs 180000

Securities Premium Amount = 1800 × Rs 10 = Rs 18000

(Issue of 2200 9% debentures of Rs 100 each at a discount of Rs 10 per debenture)

Working notes

Amount due to vendor = Rs 198000

Value of one debenture at a discount of Rs 10 = Rs 90

No. of denentures to be issued = Rs 198000 ÷ Rs 90 = 2200

Debentures amount (Nominal value) = 2200 × Rs 100 = Rs 220000

Discount on issue of Debentures = 2200 × Rs 10 = Rs 22000

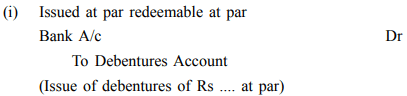

Issue of Debentures with conditions Stipulated to their Redemption (Journal entry)

Illustration 6

Make journal entries if 200 debentures of Rs 500 each have been issued as :

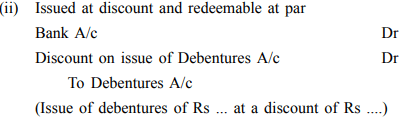

(i) Issued at Rs 500, redeemable at Rs 500

(ii) Issue at Rs 450; redeemable at Rs 500

(iii) Issued at Rs 550; redeemable at Rs 500

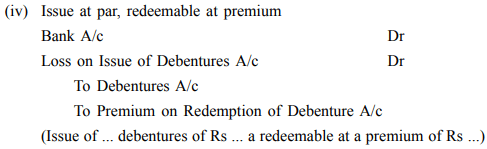

(iv) issued at Rs 500; redeemable at Rs 550

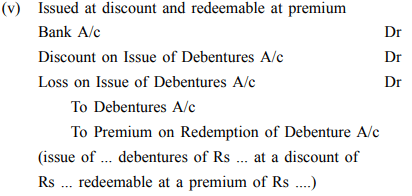

(v) Issued at Rs 450; redeemable at Rs 550

Solution : Journal

|

Dale |

Particulars |

LF |

Dr Amount Rs |

Cr Amount Rs |

|

|

Bank Ac Dr |

|

100000 |

|

|

|

To Debentures A/c |

|

|

100000 |

|

|

(Issue of 200 debentures @ of Rs 500 each) |

|

|

|

|

(ii) |

Bank A/c Dr |

|

90000 |

|

|

|

Discount on Issue of Debentures Ate Dr |

|

10000 |

|

|

|

To Debentures A/c |

|

|

100000 |

|

|

(Issue of 200 debentures of Rs 50 each at Rs 450) |

|

|

|

|

(iii) |

Bank A/c Dr |

|

110000 |

|

|

|

To Debentures A/c |

|

|

100000 |

|

|

To Securities Premium A/c |

|

|

10000 |

|

|

(Issue of 200 debentures of Rs 500 each at Rs 550) |

|

|

|

|

(iv) |

Bank Ac Dr |

|

10000 |

|

|

|

Loss on Issue of Debentures Ac Dr |

|

10000 |

|

|

|

To Debentures Ac |

|

|

100000 |

|

|

To Premium on redemption of debentures Ac |

|

10000 |

|

|

|

(Issue of 200 debentures of Rs 500 each at Rs 500 repayable at Rs 550) |

|

|

|

|

(v) |

Bank Ac Dr |

|

90000 |

|

|

|

Loss on Issue of Debentures Ac Dr |

|

10000 |

|

|

|

Discount on Issue of Debentures Ac Dr |

|

10000 |

|

|

|

To Debentures Ac |

|

|

100000 |

|

|

To Premium on Redemption of Debentures Ac |

|

20000 |

|

|

|

(Issue of 2000 Debentures of Rs 500 each at Rs 45 repayable at Rs 550) |

|

|

|

Issue of Debentures as Collateral Security

Collateral security means security given in addition to the principal security. It is a subsidiary or secondary security. Whenever a company takes loan from bank or any financial institution it may issue its debentures as secondary security which is in addition to the principal security. Such an issue of debentures is known as ‘issue of debentures as collateral security’. The lender will have a right over such debentures only when company fails to pay the loan amount and the principal security is exhausted. In case the need to exercise this right does not arise debentures will be returned back to the company. No interest is paid on the debentures issued as collateral security because company pays interest on loan.

In the accounting books of the company issue of debentures as collateral security can be credited in two ways.

(i) No journal entry to be made in the books of accounts of the company :

Debentures are issued as collateral security. A note of this fact is given on the liability side of the balance sheet under the heading Secured Loans and Advances.

Balance Sheet ...... Co. Ltd.

|

Capital & liabilities |

Amount Rs |

Assets Rs |

Amount Rs |

|

Debentures (.... debentures of Rs .... per debenture issued as collateral security Loan (Secured by the issue of .... debentures of Rs each issued as collateral security |

|

|

|

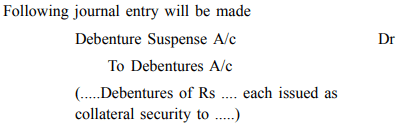

(ii) Entry to be made in the books of account the company

A journal entry is made on the issue of debentures as a collateral security, Debentures suspense A/c is debited because no cash is received for such issue.

In the Balance sheet of the issuing company it will be shown as udner :

Balance Sheet of ...... Co. Ltd.

|

Capital & Liabilities |

Amount Rs |

Assets Rs |

Amount Rs |

|

|

|

Bank |

|

|

Debenture |

|

Debenture suspense A/c |

|

|

(.... debenture of Rs .... each issued as collateral security as per contra) |

|

{Debenture issued as collateral security for loan as per contra) |

|

|

Loan |

|

|

|

Illustration 7

Sky Rocketing Company Ltd issued 6000 10% debentures of Rs 100 each to the bank as collateral security against a loan of Rs 500000 taken from the bank. Record the issue of debentures in the books of the company and show the issued Debentures in the Balance Sheet of the Company.

Solution

(i) No journal entry is required

Balance Sheet (Relevant) of Sky Rocketing Co. Ltd

|

Capital & Liabilities |

Amount |

Assets |

Amount |

|

Secured Loan |

500000 |

Current Assets & loans and Advance |

|

|

Bank: loan |

|

Cash at Bank |

500000 |

|

(Secured by 6000 10% debentures of Rs 100 each |

|

|

|

|

issued as collateral security) |

|

|

|

(ii) Journal

|

|

|

|

Dr |

Cr |

|

Date |

Particulars |

LF |

Amount |

Amount |

|

|

Debentures Suspense Ac Dr |

|

600000 |

|

|

|

To Debenture A/c |

|

|

600000 |

|

|

(Issue of 6000 10% debentures of Rs 100 each issued as collateral security to bank) |

|

|

|

Balance Sheet (Relevant) of Sky Rocketing Co. Ltd

|

Capital & Liabilities |

Amount Rs |

Assets |

Amount Rs |

|

Secured Loan |

|

Current Assets |

|

|

Bank loan |

500000 |

Cash at Bank |

500000 |

|

|

|

Miscellaneous expenditure Debenture suspense A/c |

600000 |

|

Debentures |

600000 |

(6000 Debentures of Rs 100 each issued as collateral security as per contra) |

|

|

(6000 10% debentures issued as collateral security) |

|

|

|

Discount on Issue of Debentures And Loss on Issue of Debentures

In case company issues debentures on discount the total amount of discount is not charged to profit and Loss Account of the company in the accounting year in which this discount is allowed. The amount of such discount is very heavy and to the company gets benefit from the loan by issuing debentures over a number of years. Hence some part of the amount of discount is written off every year. Generally it is written off prior to the redemption of these debentures.

As the amount of discount on issue of debentures is treated as a capital loss, it is shown on the asset side of the balance sheet of the company under the head “Miscellaneous Expenditure” until and by the amount it is not written off.

The amount of debenture discount can be written off in two ways :

1. All debentures are to be redeemed after a fixed period.

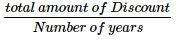

When the debentures are to be redeemed after a fixed period, the amount of discount will be distributed equally within the number of years spreaded between the issue of debentures and their redemption. The amount of discount on issue of debentures to be written off each year is calculated as

Amount of discount to be written off annually

Illustration 8

A company issues 1000 debentures of Rs 1000 each at a discount of 10% for a period of 5 years i.e. to be redeemed after 5 years. Calculate the amount of discount to be written off each year and prepare on issue of debentures discount account.

Solution

Amount to be written off each year = Rs 100000 5 = Rs 20000

Accounting Treatment

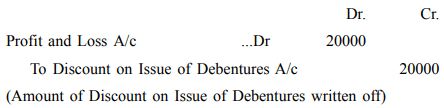

Journal entry to write off debenture discount each year

Discount on Issue of Debentures A/c

|

Dr. |

|

|

|

|

Cr. |

|

Date |

Particulars |

Amount Rs |

Date |

Particulars |

Amount Rs |

|

1st year |

|

|

1st year |

|

|

|

Jan 1 |

Debenture A/c |

100000 |

Dee 31 |

Profit & Loss A/c |

20000 |

|

|

|

|

Dec 31 |

Balance eld |

80000 |

|

|

|

100000 |

|

|

100000 |

|

2nd year |

|

|

2nd year |

|

|

|

Jan 1 |

Balance b/d |

80000 |

Dee. 31 |

Profit & Loss A/e |

20000 |

|

|

|

|

Dec.3 1 |

Balance cld |

60000 |

|

|

|

80000 |

|

|

80000 |

|

3rd year |

|

|

3rd year |

|

|

|

Jan 1 |

Balance b/d |

60000 |

Dee 31 |

Profit & Loss A/c |

20000 |

|

|

|

|

Dec 31 |

Balance cld |

40000 |

|

|

|

60000 |

|

|

60000 |

|

4th year |

|

|

4th year |

|

|

|

Jan 1 |

Balance b/d |

40000 |

Dec 31 |

Profit & Loss A/c |

20000 |

|

|

|

|

Dec 31 |

Balance cld |

20000 |

|

|

|

40000 |

|

|

40000 |

|

5th year |

|

|

5th year |

|

|

|

Jan 1 |

Balance b/d |

20000 |

Dec 31 |

Profit & Loss A/c |

20000 |

|

|

|

20000 |

|

|

20000 |

2. Debentures are redeemed in instalments

Debentures may also be redeemed in instalments but over a fixed period. In that case the amount of debenture discount will be written off each year in proportion to the amount of debentures redeemed.

Illustration 9

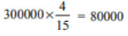

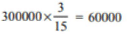

A company has issued 2000 9% debentures of Rs 1000 each at a discount of 10%. If the debentures are to be redeemed in five equal annual instalments, calculate the amount of Discount on Issue of Debentures to be written off each year and prepare Discount on Issue of Debentures A/c.

Solution

Calculation of Amount of Discount on Issue of Debentures Account

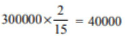

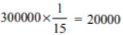

Total amount of Discount on Issue of Debentures A/c = (2000×Rs1000)×10/100 = Rs = 200000

|

Year end |

Outstanding amount of debenture |

Ratio |

Amount of Discount written off |

|

1st |

3000000 |

5 |

= 100000 |

|

2nd |

2400000 |

4 |

|

|

3rd |

1800000 |

3 |

|

|

4th |

1200000 |

2 |

|

|

5th |

600000 |

1 |

|

|

|

|

15 |

|

Journal entry

Similarly entry will be made every year with the respective amount of discount.

Discount on issue of Debentures account till the amount of discount is written off will be shown as under.

Discount on Issue of Debentures A/c

|

Dr |

|

|

|

|

Cr. |

|

Dale |

Particulars |

Amount Rs |

Date |

Particulars |

Amount Rs |

|

1st year |

|

|

1st year |

|

|

|

ian I |

Debentures A/e |

300000 |

Dec 31 |

Profit & Loss A/e |

100000 |

|

|

|

|

Dee 31 |

Balance eld |

200000 |

|

|

|

300000 |

|

|

300000 |

|

2nd year |

|

|

2nd year |

|

|

|

lan I |

Balance b/d |

200000 |

Dee. 31 |

Profit & Loss A/e |

80000 |

|

|

|

|

Dee.31 |

Balance eld |

120000 |

|

|

|

200000 |

|

|

200000 |

|

3rd year |

|

|

3rd year |

|

|

|

Jan 1 |

Balance b/d |

120000 |

Dec 31 |

Profit & Loss A/e |

60000 |

|

|

|

|

Dee 31 |

Balance cld |

60000 |

|

|

|

120000 |

|

|

120000 |

|

4th year |

|

|

4th year |

|

|

|

Jan 1 |

Balance b/d |

60000 |

Dec 31 |

Profit & Loss A/e |

40000 |

|

|

|

|

Dee 31 |

Balance cld |

20000 |

|

|

|

60000 |

|

|

60000 |

|

5th year |

|

|

5th year |

|

|

|

Jan 1 |

Balance b/d |

20000 |

Dec 31 |

Profit & Loss A/c |

20000 |

|

|

|

20000 |

|

|

20000 |

Loss on Issue of Debentures

You have learnt that a company may issue debentures with the stipulation that the repayment of the debentures on maturity will be made at premium. The amount of the premium payable is debited to Loss on Issue of

Debentures A/c at the time of issue of debentures. This amount will also be written off in the same manner as is done in case of writing off Discount on Issue of Debentures. This is illustrated as under :

(i) All Debentures are redeemed after fixed period

Journal Entry

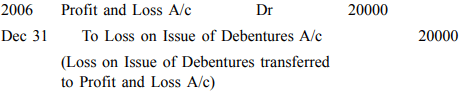

(Loss on Issue of Debentures written off)

Same journal entry will be made each year till the whole amount of the Loss on issue of Debentures is written off.

Calculation of the amount to be written off

Total Amount of Loss on Issue of Debentures/No. of years.

Illustration 10

A company issues 1000 10% Debentures of Rs 1000 each on 1st Jan, 2006 payable at a premium of 10% after 5 years. Make journal entries and open Loss on Issue of Debentures A/c for the year ending 31st December 2006.

Solution

Amount of Loss on issue of Debentures

Amount to be written off each year = Rs 100000/5 = 20000

Loss on issue of Debentures A/c

|

Dr. |

|

|

|

|

Cr. |

|

Dale |

Particulars |

Amount |

Date |

Particulars |

Amount |

|

2006 |

|

|

2006 |

|

|

|

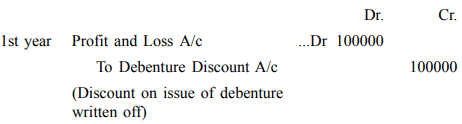

Jan I |

10% Debentures A/c |

100000 |

Dec 31 |

By Profit & Loss A/c |

20000 |

|

|

|

|

Dec 31 |

By Balance eld |

80000 |

|

|

|

100000 |

|

|

100000 |

|

2007 |

|

|

|

|

|

|

Jan 1 |

Balance b/d |

80000 |

|

|

|

Journal Entry

(ii) Debentures are Redeemed in Instalments

The amount of Loss on Issue of Debentures to be written off each year is calculated in the manner it is calculated in case of Discount on Issue of Debentures and accounting treatment is also the same.

Illustration 11

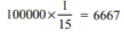

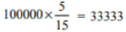

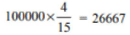

Refer Illustration No. 10. A company decides to redeem its debentures in five equal instalments beginning from the end of first year. Make journal entry for the writing off and show Loss on Issue of Debentures A/c for first year

Solution

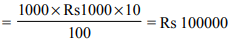

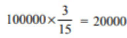

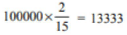

Amount of Loss on Issue of Debentures = 1000×Rs1000×Rs/10 = Rs 100000

Calculation of amount to be written off each year

|

Year end |

Amount Outstanding |

Ratio |

Amount of Loss to be written oft" each year |

|

1st |

1000000 |

5 |

|

|

2nd |

800000 |

4 |

|

|

3rd |

600000 |

3 |

|

|

4th |

400000 |

2 |

|

| 5th | 200000 | 1 |  |

| 15 |

Journal Entry

Loss on Issue of Debentures A/c

|

Dr. |

|

|

|

|

Cr. |

|

Dale |

Particulars |

Amount Rs |

Dale |

Particulars |

Amount Rs |

|

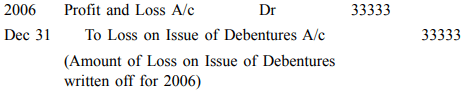

2006 |

|

|

2006 |

|

|

|

Jan 1 |

10% Debentures A/c |

100000 |

Dec 31 |

Profit & Loss A/e |

33333 |

|

|

|

|

Dec 31 |

Balance eld |

66667 |

|

|

|

100000 |

|

|

100000 |

|

2007 |

|

|

|

|

|

|

Jan 1 |

Balance b/d |

66667 |

|

|

|

Interest on Debentures

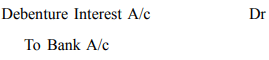

If you have seen an advertisement in newspaper regarding issue of debentures by a company, you must have noticed that ‘Debenture’ is always prefixed by a certain percentage say 9% Debentures or 12% Debentures. Have you ever thought what meaning does this prefix carry. It is the rate of interest per annum that will be paid to the debenture holders. Companies generally pay interest on its debentures after every six months. Journal entries that are made in the books of the company are as follows;

(i) Payment of Interest on Debentures

(Interest on ....% Debentures paid for six months ending ...@ ....% pa)

(ii) Transfer of Debenture Interest to Profit and Loss A/c

(Debenture Interest transferred to Profit and Loss A/c)

Illustration 12

X Ltd has issued 5000 9% Debentures of Rs 1000 each, on 1st April, 2006 Interest is payable after every six months. Make journal entries for the interest paid for the first six months after the date of issue.

Solution.

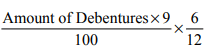

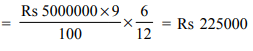

Calculation of Interest payable at six monthly intervals :

Amount of Debentures = 5000 × Rs 1000 = Rs 5000000

Interest on Debentures for six month ending 30th September, 2006

Journal Entry

| 2006 | Dr. | Cr. | |

|

30th Sept. |

Debentures Interest A/c Dr (Interest on 5000 9% Debentures @ Rs 1000 per debenture paid for 6 months ending 30th Sept 2006) |

225000 |

225000 |

|

2007 |

|

|

|

|

31 st Mar |

Profit and Loss A/c Dr To Debentures Interest A/c (Debenture Interest transferred to profit and Loss A/c) |

225000 |

225000 |

|

89 videos|82 docs|20 tests

|

FAQs on Issue of Debentures - Advanced Corporate Accounting - Advanced Corporate Accounting - B Com

| 1. What is a debenture? |  |

| 2. What are the types of debentures? | |

| 3. What is the process of issuing debentures? | |

| 4. What are the advantages of issuing debentures for a company? | |

| 5. What are the risks associated with investing in debentures? | |

Semester Notes

,Objective type Questions

,Issue of Debentures - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,Issue of Debentures - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,practice quizzes

,video lectures

,Sample Paper

,Important questions

,past year papers

,Issue of Debentures - Advanced Corporate Accounting | Advanced Corporate Accounting - B Com

,mock tests for examination

,Summary

,Previous Year Questions with Solutions

,Exam

,shortcuts and tricks

,ppt

,Free

,Viva Questions

,MCQs

,Extra Questions

,study material

;

Issue of Debentures - Advanced Corporate Accounting Free PDF Download

Importance of Issue of Debentures - Advanced Corporate Accounting

Issue of Debentures - Advanced Corporate Accounting Notes

Issue of Debentures - Advanced Corporate Accounting B Com Questions

Study Issue of Debentures - Advanced Corporate Accounting on the App

|

© EduRev

|

Education Revolution

|

|