Journal, Ledger and Trial Balance - Accountancy and Financial Management

Introduction

The Double Entry System of accounting was developed in the 15th century in Italy by Luca Pacioli. It forms the fundamental framework of modern bookkeeping. Under this system every business transaction has two aspects and both aspects are recorded. For example, when furniture is purchased, either the business pays cash (reducing the Cash asset) or incurs a liability to a supplier (increasing Creditors). Thus each transaction affects at least two accounts and is recorded twice - once on the debit side of one account and once on the credit side of another.

Objectives

- Understand the Double Entry System and its historical basis.

- Determine how debit and credit are applied to business transactions.

- Classify accounts into personal, real and nominal accounts.

- Learn definitions and purpose of Journal and Ledger, and the process of journalising.

- Become familiar with the technique of ledger posting, balancing accounts and preparing a Trial Balance.

- Understand the accounting cycle and the sequence of accounting activities from transaction to financial statements.

Accounting Equation

The entire structure of the Double Entry System is founded on the Accounting Equation, which shows the equality between the resources owned by a business and the claims on those resources.

Assets = Liabilities + Capital

In words: total assets of a company are equal to the combined total of external claims (liabilities) and owners' claims (capital). Any change in assets must be matched by a change in liabilities, capital, or both - this is the dual aspect concept of accounting.

Effect of Transactions on the Accounting Equation

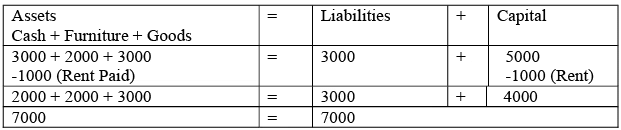

1. Start a business with Rs. 5,000 as capital.

2. Purchase furniture for Rs. 2,000 cash.

Note: Cash (an asset) decreases by Rs. 2,000 while Furniture (another asset) increases by Rs. 2,000. Total assets remain unchanged.

3. Purchase goods for Rs. 3,000 on credit.

Note: Inventory (asset) increases by Rs. 3,000 while Creditors (liability) increase by Rs. 3,000.

4. Paid Rs. 1,000 for rent.

Note: Rent is an expense and reduces capital (owner's equity). Cash decreases and capital is reduced via the expense.

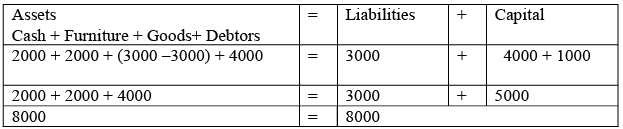

5. Sold goods costing Rs. 3,000 on credit for Rs. 4,000.

Note: Debtors (asset) increase by Rs. 4,000; cost of goods sold reduces inventory (asset) by Rs. 3,000; the profit of Rs. 1,000 increases capital.

When transactions become numerous, accounts are represented in the T-form or two-column format. The left side is the Debit side and the right side is the Credit side. An entry on the left is called a debit, and an entry on the right is called a credit. The typical layout of a T-account is shown below.

Ref. indicates the ledger reference (page or folio) where the corresponding entry is recorded.

Rules of Debit and Credit (Effects on Accounts)

- When an asset increases, the asset account is debited; when an asset decreases, it is credited.

- When a liability increases, the liability account is credited; when a liability decreases, it is debited.

- When owner's capital increases, the capital account is credited; when capital decreases, it is debited.

- Profit increases capital and is therefore credited; a loss reduces capital and is debited.

These may be summarised as:

- Increase in assets → Debit; Decrease in assets → Credit

- Increase in liabilities → Credit; Decrease in liabilities → Debit

- Increase in owner's capital → Credit; Decrease in owner's capital → Debit

- Increase in expenses/losses → Debit; Decrease in expenses/losses → Credit

- Increase in revenue/income → Credit; Decrease in revenue/income → Debit

Note that the words debit and credit indicate the two sides of an account and do not by themselves imply good or bad. The Dual Aspect Concept ensures that total debits always equal total credits.

Classification of Accounts

Accounts are classified in two complementary ways: by nature (asset, liability, etc.) and by type (personal, real, nominal).

By Nature (according to the accounting equation)

- Assets - resources owned by the firm (e.g., Cash, Machinery, Furniture).

- Liabilities - amounts owed to outsiders (e.g., Creditors, Loans).

- Capital - owners' funds invested in the business.

- Expenses - amounts spent in carrying on operations (e.g., Wages, Rent).

- Income - amounts earned by the firm (e.g., Sales, Interest Received).

By Type

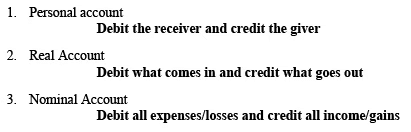

- Personal Account - relates to persons or entities (e.g., Ram, ABC & Co.).

- Real Account - relates to tangible or intangible assets (e.g., Machinery, Land, Stock).

- Nominal Account - relates to incomes, expenses, gains and losses (e.g., Rent, Salary, Commission). Nominal accounts are temporary - their balances are transferred to the Profit & Loss account at year end.

From the three basic classifications the traditional rules for debit and credit are often given as:

Debit denotes:

- For a person, that they have received a benefit which the firm has to account for (e.g., when the firm owes them future service or money).

- For goods or properties, that their stock or value has increased.

- For expenses, that the firm has incurred a cost or loss.

Credit denotes:

- For a person, that they have provided a benefit to the firm and are therefore entitled to receive cash, goods or services from the firm.

- For goods or properties, that their quantity or value has decreased.

- For income or profit accounts, that the firm has earned revenue.

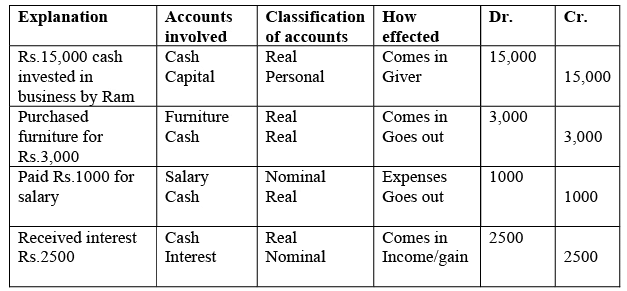

Illustration 1

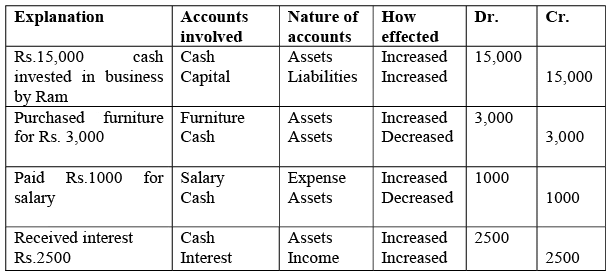

- Ram started business with Rs. 15,000.

- He purchased furniture for Rs. 3,000.

- Salary paid Rs. 1,000.

- Received interest Rs. 2,500.

Solution as per debit/credit rules of accounting equation

Solution as per three basic rules of classification of accounts

Definitions of Journal and Ledger

Journal: Transactions are first recorded in the journal to indicate which account is to be debited and which is to be credited. The journal is called the book of original entry or primary book, and transactions are recorded in chronological order with a brief narration.

Ledger: The ledger is a book that contains individual accounts prepared from journal entries. It is called the book of final entry or secondary book, since posting to the ledger is done after journalising.

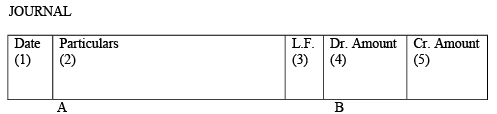

The Journalising Process

The journal records each transaction, indicating the accounts to be debited and credited, the amounts and a short narration. A typical journal format includes columns for date, account titles and narration, ledger folio (reference), debit amount and credit amount.

- The date of the transaction is recorded in the date column.

- The account to be debited is written first (close to the account-title column) followed by the abbreviation Dr.

- The account to be credited is written on the next line, prefixed by the word To.

- A brief narration explaining the transaction is recorded below the entry.

- The ledger folio (page reference) is entered when the posting to ledger is done.

- Debit and credit amounts are entered in their respective columns.

Before journalising, determine accounts affected and whether they should be debited or credited by applying the debit-credit rules or the accounting equation.

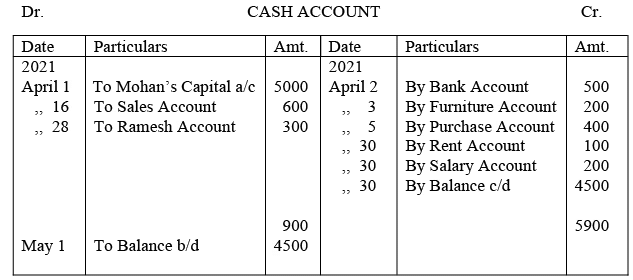

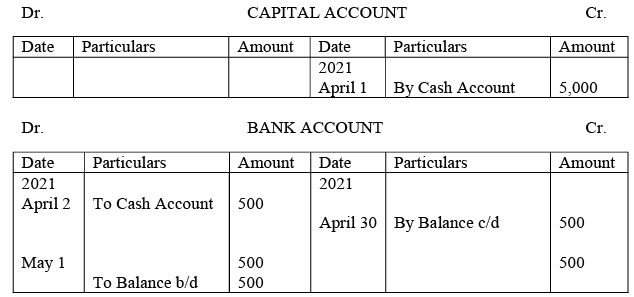

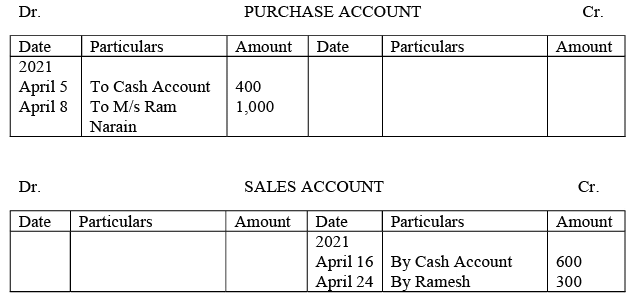

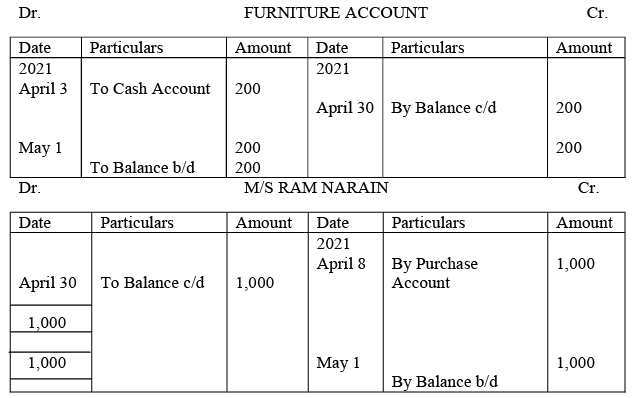

Ledger Posting

The ledger is the principal book containing all individual accounts. Ledger posting organises journal entries into classified accounts so we can determine balances for each account and ultimately prepare financial statements. Personal accounts show amounts receivable from debtors and payable to creditors; real accounts show assets and stock; nominal accounts show incomes and expenses.

Consider the following journal entry:

From this journal entry we will prepare two ledger accounts: the Furniture Account and the ABC Furniture & Co. account. While posting, observe the following:

- A ledger entry records the contra account name (i.e., the name of the other account in the journal entry) rather than repeating the name of the ledger the entry is posted to.

Posting the above journal entry into the Furniture Account is done as follows:

Because Furniture was debited in the journal, the Furniture ledger is debited and the contra account name ABC Furniture & Co. is shown in the particulars column. The ABC Furniture & Co. ledger will show a corresponding credit entry with the contra account name Furniture Account as the particulars.

The posting of transactions from the earlier illustration continues as follows:

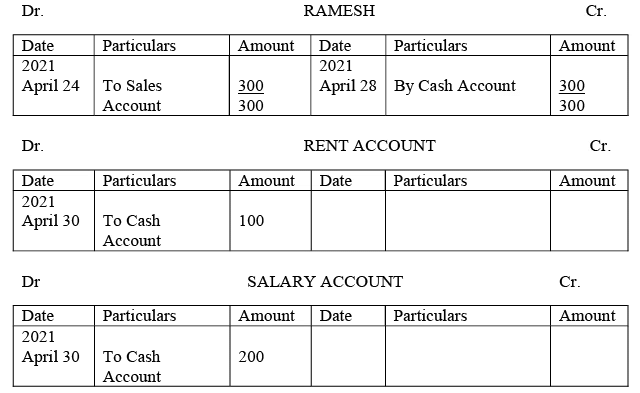

Balancing an Account

At the end of a period it is necessary to find the balance of each ledger account. Balancing involves totalling both debit and credit sides and recording the difference as the balance on the smaller side so that both sides become equal.

For example, if the debit total is Rs. 1,000 and the credit total is Rs. 850, the difference Rs. 150 is a debit balance. This is shown on the credit side as By Balance c/d (carried down). On the next accounting period the balance is brought forward on the debit side as To Balance b/d (brought down).

Nominal accounts (expenses and incomes) are not carried forward; their balances are transferred to the Profit & Loss Account at year end. Personal and real accounts may carry forward balances to the next period.

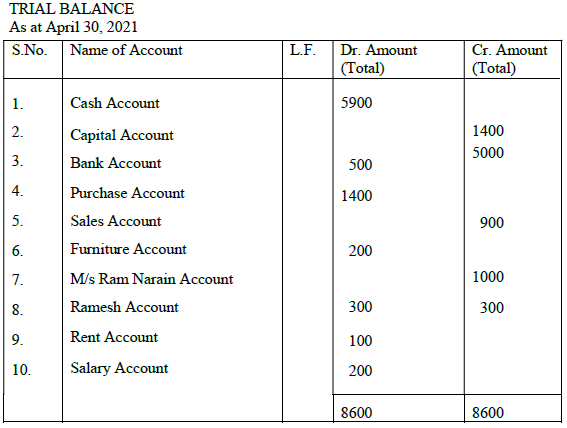

Trial Balance

A Trial Balance is a statement in which the debit and credit balances of all ledger accounts are listed in two separate columns. It is prepared after posting and balancing the ledger accounts. The primary purpose of a Trial Balance is to test the arithmetical accuracy of posting and balancing: the total of the debit column should equal the total of the credit column.

Agreement of the Trial Balance provides reasonable assurance that the books are arithmetically correct, but it does not guarantee absolute accuracy. Certain errors cannot be detected by a Trial Balance.

Errors Undetectable by a Trial Balance

- Error of complete omission: A transaction was not recorded at all.

- Error of original entry: The wrong amount was entered on both sides of a journal entry.

- Error of reversal: Debit and credit accounts were reversed though amounts are correct.

- Error of principle: A transaction is recorded in the wrong type of account (e.g., recording a capital expenditure as revenue expenditure).

- Error of commission: The correct amount is recorded but in the wrong account (often due to oversight).

Objectives of Preparing a Trial Balance

- To check the arithmetical accuracy of ledger posting and balancing.

- To provide a convenient basis for preparing final accounts.

- To act as a summary of the balances contained in the ledger.

- To assist in locating bookkeeping errors.

Format of a Trial Balance

The Total Method and the Balance Method

Total Method (Gross Trial Balance): The totals of the debit and credit sides of each ledger account are entered respectively in the debit and credit columns of the Trial Balance.

Balance Method (Net Trial Balance): Only the balances of ledger accounts (net of debits and credits) are entered - debit balances in the debit column and credit balances in the credit column.

Limitations of the Trial Balance

- Transactions not recorded in the journal will not appear in the Trial Balance.

- Identical errors in both debit and credit (e.g., posting the same wrong amount on both sides) will not be detected.

- Wrong accounts used in entries (but with correct totals) will still allow the Trial Balance to agree.

- Partial or double posting errors may leave the Trial Balance unchanged.

The Accounting Cycle

The accounting cycle is the sequence of steps followed in recording and reporting financial transactions. It begins with the occurrence of transactions and ends with preparation of financial statements and closing of books for the period.

- Business transactions occur (sales, purchases, payments, receipts).

- Transactions are analysed and recorded in appropriate journals.

- Journal entries are posted to the general ledger accounts.

- Ledger accounts are balanced and a Trial Balance is prepared.

- If the Trial Balance does not agree, errors are located and corrected.

- Adjusting entries (for accruals, prepayments, depreciation, etc.) are made and posted.

- Adjusted Trial Balance is prepared and financial statements (Trading & Profit & Loss Account and Balance Sheet) are drawn up.

- Closing entries are passed to transfer nominal account balances to the capital/profit accounts, and the cycle restarts for the next accounting period.

The accounting cycle resembles an information processing flow: input (transactions) → process (journalising, posting, adjusting) → output (financial statements).

FAQs on Journal, Ledger and Trial Balance - Accountancy and Financial Management

| 1. What are the rules of Debit and Credit in accounting? |  |

| 2. What is the purpose of a Ledger in accounting? | |

| 3. What are Ledger Accounts and how are they different from a Ledger? | |

| 4. What is the difference between a Journal and a Ledger in accounting? | |

| 5. What is the purpose of a Trial Balance in accounting? | |