Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management | Accountancy and Financial Management - B Com PDF Download

Risk and Uncertainly In Capital Budgeting

Capital budgeting requires the projection of cash inflow and outflow of the future. The future in always uncertain, estimate of demand, production, selling price, cost etc., cannot be exact.

For example: The product at any time it become obsolete therefore, the future in unexpected. The following methods for considering the accounting of risk in capital budgeting. Various evaluation methods are used for risk and uncertainty in capital budgeting are as follows:

(i) Risk-adjusted cut off rate (or method of varying discount rate)

(ii) Certainly equivalent method.

(iii) Sensitivity technique.

(iv) Probability technique

(v) Standard deviation method.

(vi) Co-efficient of variation method.

(vii) Decision tree analysis.

(i) Risk-adjusted cutoff rate (or Method of varying)

This is one of the simplest method while calculating the risk in capital budgeting increase cut of rate or discount factor by certain percentage an account of risk. Exercise 13

The Ramakrishna Ltd., in considering the purchase of a new investment. Two alternative investments are available (X and Y) each costing Rs. 150000. Cash inflows are expected to be as follows:

Cash Inflows

Year | Investment X Rs. | Investment Y Rs. |

1 | 60,000 | 65,000 |

2 | 45,000 | 55,000 |

3 | 35,000 | 40,000 |

4 | 30,000 | 40,000 |

The company has a target return on capital of 10%. Risk premium rate are 2% and 8% respectively for investment X and Y. Which investment should be preferred?

Solution

The profitability of the two investments can be compared on the basis of net present values cash inflows adjusted for risk premium rates as follows:

Investment X | Investment Y | |||||

Year | Discount Factor10% + 2% = 12% | Cash Inflow Rs. | Present Value Rs. | Discount Factor 10% + 8%=18% | Cash Inflow Rs. | Present Values |

1 | 0.893 | 60,000 | 53,580 | 0.847 | 85,000 | 71,995 |

2 | 0.797 | 45,000 | 35,865 | 0.718 | 55,000 | 39,490 |

3 | 0.712 | 35,000 | 24,920 | 0.609 | 40,000 | 24,360 |

4 | 0.635 | 30,000 | 19,050 | 0.516 | 40,000 | 20,640 |

| 1,33,415 |

| 1,56,485 | |||

Investment X

Net present value = 133415 – 150000

= – Rs. 16585

Investment Y

Net present value = 156485 – 150000

= Rs. 6485

As even at a higher discount rate investment Y gives a higher net present value, investment Y should be preferred.

(ii) Certainly equivalent method

It is also another simplest method for calculating risk in capital budgeting info reduceds expected cash inflows by certain amounts it can be employed by multiplying the expected cash inflows by certainly equivalent co-efficient in order the uncertain cash inflow to certain cash inflows.

Exercise 14

There are two projects A and B. Each involves an investment of Rs. 50,000. The expected cash inflows and the certainly co-efficient are as under:

| Project A | Project B | ||

Year | Cash inflows | Certainly co-efficient | Cash inflows | Certainly Co-efficient |

1 | 35,000 | 0.8 | 25,000 | 0.9 |

2 | 30,000 | 0.7 | 35,000 | 0.8 |

3 | 20,000 | 0.9 | 20,000 | 0.7 |

Risk-free cutoff rate is 10%. Suggest which of the two projects. Should be preferred.

Solution

Calculations of cash Inflows with certainly:

Year | Project A | Project B | ||||

| Cash Inflow | Certainly Co-efficient | Certain Cash Inflow | Cash Inflow | Certainly Co-efficient | Certain Cash Inflow |

1 | 35,000 | .8 | 28,000 | 25,000 | .9 | 22,500 |

2 | 30,000 | .7 | 21,000 | 35,000 | .8 | 28,000 |

3 | 20,000 | .9 | 18,000 | 20,000 | .7 | 14,000 |

Calculation of present values of cash inflows:

Year | Project A | Project B | |||

| Discount Factor @ 10% | Cash Inflows | Present Values | Cash Inflows | Present Value |

1 | 0.909 | 28,000 | 25,452 | 22,500 | 20,453 |

2 | 0.826 | 21,000 | 17,346 | 28,000 | 23,128 |

3 | 0.751 | 18,000 | 13,518 | 14,000 | 10,514 |

Total |

|

| 56,316 |

| 54,095 |

Project A = Net present value = Rs. 56,316 – 50,000 = Rs. 6,316

Project B = Net present value = 54,095 – 50,000 = Rs. 4,095

As the net present value of project A in more than that of project B. Project A should be preferred:

(iii) Sensitivity technique

When cash inflows are sensitive under different circumstances more than one forecast of the future cash inflows may be made. These inflows may be regarded on ‘Optimistic’, ‘most likely’ and ‘pessimistic’. Further cash inflows may be discounted to find out the net present values under these three different situations. If the net present values under the three situations differ widely it implies that there is a great risk in the project and the investor’s is decision to accept or reject a project will depend upon his risk bearing activities.

Exercise 15

Mr. Selva is considering two mutually exclusive project ‘X’ and ‘Y’. You are required to advise him about the acceptability of the projects from the following information.

| Project X Rs. | Projects Y Rs. |

Cost of the investment | 1,0,0000 | 1,00,000 |

Forecast cash inflows per annum for 5 years |

|

|

Optimistic | 60,000 | 55,000 |

Most likely | 35,000 | 30,000 |

Pessimistic | 20,000 | 20,000 |

(The cut-off rate may be assumed to be 15%).

Solution

Calculation of net present value of cash inflows at a discount rate of 15%. (Annuity of Re. 1 for 5 years).

For Project X

Event | Annual cash Inflow Rs. | Discount factor @ 15 % | Present value Rs. | Net Present value Rs. |

Optimistic | 60,000 | 3.3522 | 2,01,132 | 1,01,132 |

Most likely | 35,000 | 3.3522 | 1,17,327 | 17,327 |

Pessimistic | 20,000 | 3.3522 | 67,105 | (32,895) |

For Project Y

Event | Annual cash Inflow Rs. | Discount factor @ 15 % | Present value Rs. | Net Present value Rs. |

Optimistic | 55,000 | 3.3522 | 1,84,371 | 84,371 |

Most likely | 30,000 | 3.3522 | 1,00,566 | 566 |

Pessimistic | 20,000 | 3.3522 | 67,105 | (32,895) |

The net present values on calculated above indicate that project Y is more risky as compared to project X. But at the same time during favourable condition, it is more profitable also. The acceptability of the project will depend upon Mr. Selva’s attitude towards risk. If he could afford to take higher risk, project Y may be more profitable.

(iv) Probability technique

Probability technique refers to the each event of future happenings are assigned with relative frequency probability. Probability means the likelihood of future event. The cash inflows of the future years further discounted with the probability. The higher present value may be accepted.

Exercise 16

Two mutually exclusive investment proposals are being considered. The following information in available.

| Project A (Rs.) | Project B ( Rs.) | |

| Cost | 10,000 | 10,000 |

Cash inflows Year | Rs. | Probability | Rs. | Probability |

1 | 10,000 | .2 | 12,000 | .2 |

2 | 18,000 | .6 | 16,000 | .6 |

3 | 8,000 | .2 | 14,000 | .2 |

Assuming cost of capital at (or) advise the selection of the project:

Solution

Calculation of net project values of the two projects.

Project A

Year | P.V. Factor @ 10 % | Cash Inflow | Probability | Monetary Value | Present Value Rs. |

1 | 0.909 | 10,000 | .2 | 2,000 | 1,818 |

2 | 0.826 | 18,000 | .6 | 10,800 | 8,921 |

3 | 0.751 | 8,000 | .2 | 1,600 | 1,202 |

Total Present value = 11,941

Cost of Investment = 10,000

Net present value = 1,941

Project B

Year | P.V. Factor @ 10 % | Cash Inflow | Probability | Monetary Value | Present Value Rs. |

1 | 0.909 | 12,000 | .2 | 2,400 | 2,182 |

2 | 0.826 | 14,000 | .6 | 8,400 | 6,938 |

3 | 0.751 | 14,000 | .2 | 2,800 | 2,103 |

Total present value = 11,223

Cost of investment = 10,000

Net present value = 1,223

As net present value of project A is more than that of project B after taking into consideration the probabilities of cash inflows project A is more profitable one.

(v) Standard deviation method

Two Projects have the same cash outflow and their net values are also the same, standard durations of the expected cash inflows of the two Projects may be calculated to measure the comparative and risk of the Projects. The project having a higher standard deviation in said to be more risky as compared to the other.

Exercise 17

From the following information, ascertain which project should be selected on the basis of standard deviation.

Project X | Project Y | ||

Cash inflow Probability | Cash inflow Probability | ||

Rs. | Rs. | ||

3,200 | .2 | 32,000 | .1 |

5,500 | .3 | 5,500 | .4 |

7,400 | .3 | 7,400 | .4 |

8,900 | .2 | 8,900 | .1 |

Solution

Project X

Cash inflow | Deviation from Mean (d) | Square Deviations d2 | Probability | Weighted Deviations (td2) |

1 | 2 | 3 | 4 | 5 |

3,200 | (-) 6,250 | 9,30,25,000 | .2 | 18,60,500 |

5,500 | (-) 750 | 56,2,500 | .3 | 1,68,750 |

7,400 | (+) 1,150 | 13,22,500 | .3 | 3,96,750 |

8,900 | (+) 2,650 | 70,22,500 | .2 | 14,04,500 |

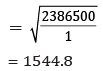

n= 1 , ∑fd2 = 38,30,500

Standard Deviation (6)

Project Y

1 | 2 | 3 | 4 | 5 |

3,200 | (-) 3,050 | 9,30,25,000 | .1 | 9,30,250 |

5,500 | (-) 750 | 5,62,500 | .4 | 2,25,000 |

7,400 | (+) 1,150 | 13,22,500 | .4 | 5,29,000 |

8,900 | (+) 2,650 | 70,22,500 | .1 | 7,02,250 |

n= 1 , ∑fd2 = 3830500

Standard deviation(6)

As the standard deviation of project X is more then that of project Y, A is more risky.

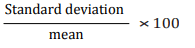

(vi) Co-efficient of variation method

Co-efficient of variation is a relative measure of dispersion. It the projects here the same cost but different net present values, relatives measure, i.e., Co-efficient of variation should be risk induced. It can be calculated as:

Co-efficient of variation =

Exercise 18

Using figure of previous example compute co-efficient of variation and suggest which proposal should be accepted:

Solution

As the co-efficient of variation of project ‘X’ in more then that ‘Y’ project X in more risk. Hence, project Y should be selected.

(vii) Decision tree analysis

In the modern business world, putting the investments are become more complex and taking decisions in the risky situations. So, the decision tree analysis helpful for taking risky and complex decisions, because it consider all the possible event’s and each possible events are assigned with the probability.

Construction of Decision Tree

- Defined the problem

- Evaluate the different alternatives

- Indicating the decision points

- Assign the probabilities of the monetary values

- Analysis the alternatives.

Accept/Reject criteria

If the net present values are in positive the project may be accepted otherwise it is rejected.

Exercise 19

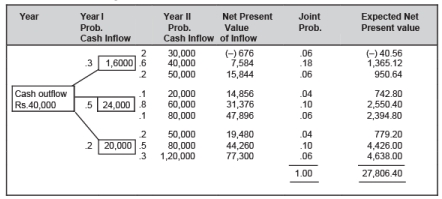

Mr. Kumar in considering an investment proposal of Rs.40,000. The expected returns during the left of the investment are as under:

Year I

Event | Cash Inflow | Probability |

(i) | 16,000 | .3 |

(ii) | 24,000 | .5 |

(iii) | 20,000 | .2 |

Year II

Cash inflows in year 1 are:

| 16,000 | 24,000 | 20,000 | |||

| Cash Inflows (Rs.) | Prob | Cash Inflows (Rs.) | Prob | Cash Inflows (Rs.) | Prob |

(i) | 30,000 | .2 | 40,000 | .1 | 5,000 | .2 |

(ii) | 40,000 | .6 | 60,000 | .8 | 8,000 | .5 |

(iii) | 50,000 | .2 | 80,000 | .1 | 12,000 | .3 |

using 10% as the cost of capital, advise about the acceptability of the proposal:

Solution

Calculation of net present values of cash inflows

As the proposal yields a net present value of +27806.40 at a discount for of 10% other proposal may be accepted.

|

61 videos|78 docs|12 tests

|

FAQs on Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management - Accountancy and Financial Management - B Com

| 1. What is the difference between risk and uncertainty in capital budgeting? |  |

| 2. What are the different types of risk in capital budgeting? | |

| 3. How can risk and uncertainty be managed in capital budgeting? | |

| 4. How does risk and uncertainty affect the capital budgeting decision? | |

| 5. What are the limitations of using risk and uncertainty analysis in capital budgeting? | |

Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Exam

,Previous Year Questions with Solutions

,Extra Questions

,mock tests for examination

,ppt

,Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,Objective type Questions

,shortcuts and tricks

,Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management | Accountancy and Financial Management - B Com

,video lectures

,Free

,Semester Notes

,MCQs

,Important questions

,Sample Paper

,Viva Questions

,Summary

,practice quizzes

,study material

,past year papers

;

Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management Free PDF Download

Importance of Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management

Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management Notes

Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management B Com Questions

Study Risk and Uncertainty In Capital Budgeting - Accountancy and Financial Management on the App

|

© EduRev

|

Education Revolution

|

|