B Com Exam > B Com Notes > Cost Accounting > FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting | Cost Accounting - B Com PDF Download

| Table of contents |

|

| Materials Costing Methods |

|

| First-In-Out (FIFO) |

|

| Last-In First-Out (LIFO) |

|

| Weighted Average Method (WAM) |

|

| Need for Material Control |

|

| Requirements of a System of Material Control |

|

Materials Costing Methods

- First-In-First-Out (FIFO) Costing Methods

- Average Costing Methods

- Last-In-First-Out (LIFO) Costing Method

- Other Materials Costing Methods—Month end average cost, last purchase price or market price at date of issue and standard cost.

First-In-Out (FIFO)

- This methods assumes that the goods purchased first or manufactured first are issued/sold first.

- That is the goods issued or sold currently are those which represent the earliest purchases amongst the goods held in inventory. This would mean that the goods which remain in stock after the sales, are those which represent the most recent purchases.

Last-In First-Out (LIFO)

- This methods is just the opposite if FIFO methods. This method assumes that the goods issued or sold out of the inventory are the ones most recently purchased manufactured.

- Therefore the goods held in stock represent the earlier purchases productions.

Weighted Average Method (WAM)

- This method assumes that all inventory available are best represented by a weighted average cost.

- The average cost of goods held in inventory is recalculated every time a fresh purchase is made and goods issued or sold out of inventory are priced at such average price till such time as the next lot is purchased.

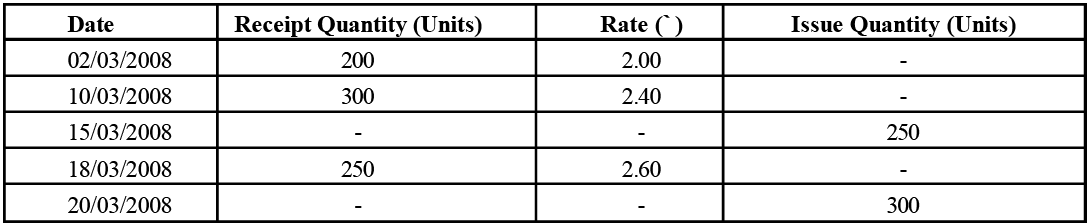

Example 1: The following transaction took place in respect of a material. Prepare a Stock register as per:

Prepare a Stock register as per:

(a) Simple Average Method

(b) Weighted Average Method.

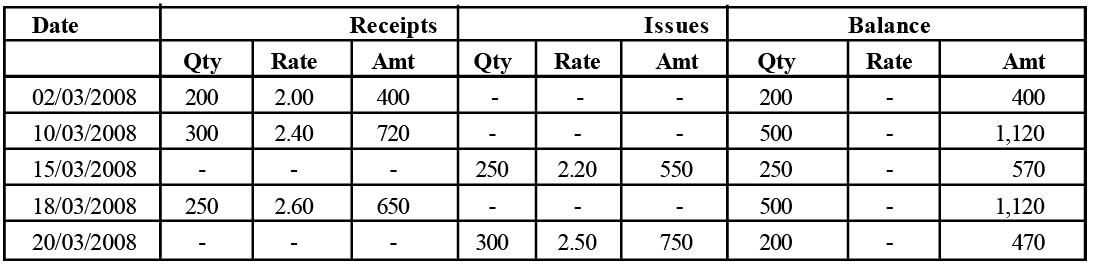

Sol: Stock Register (Simple Average Method)

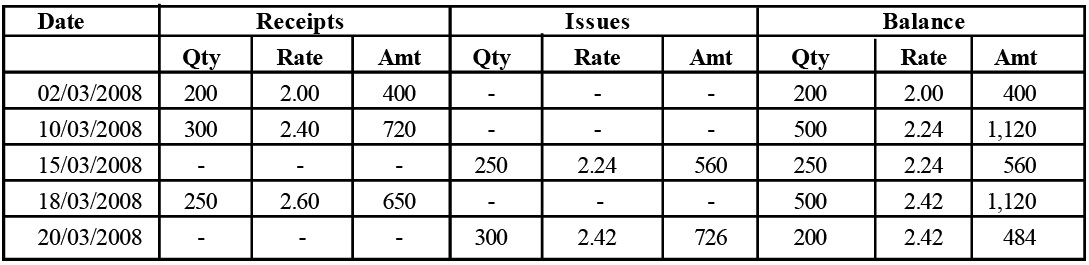

Stock Register (Weighted Average Method)

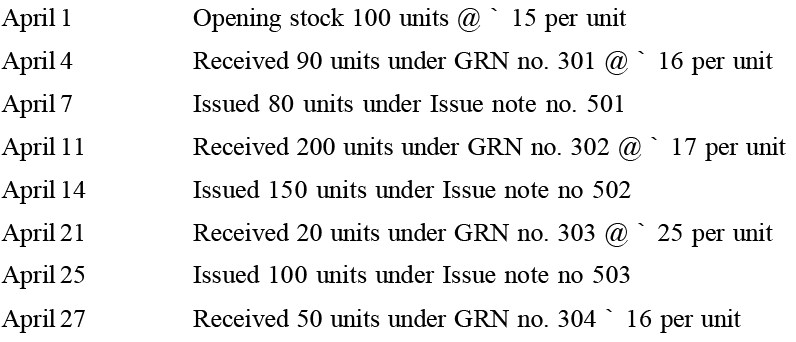

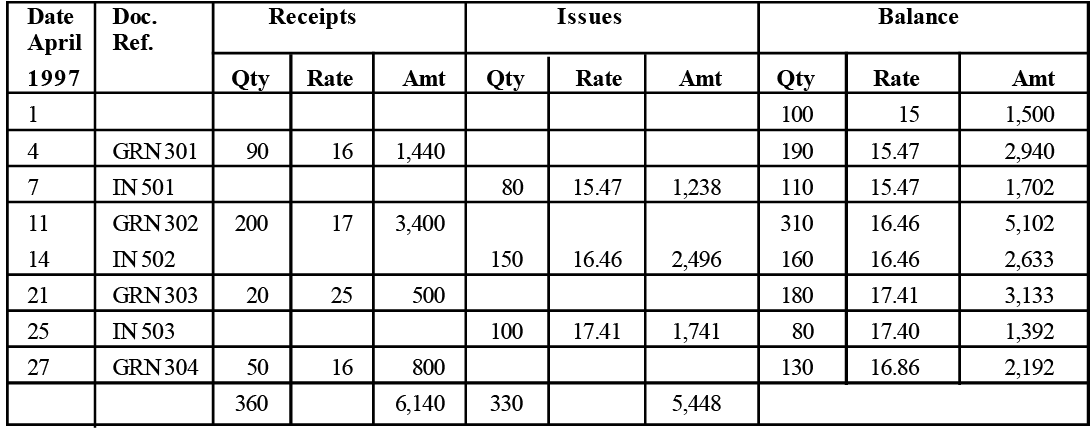

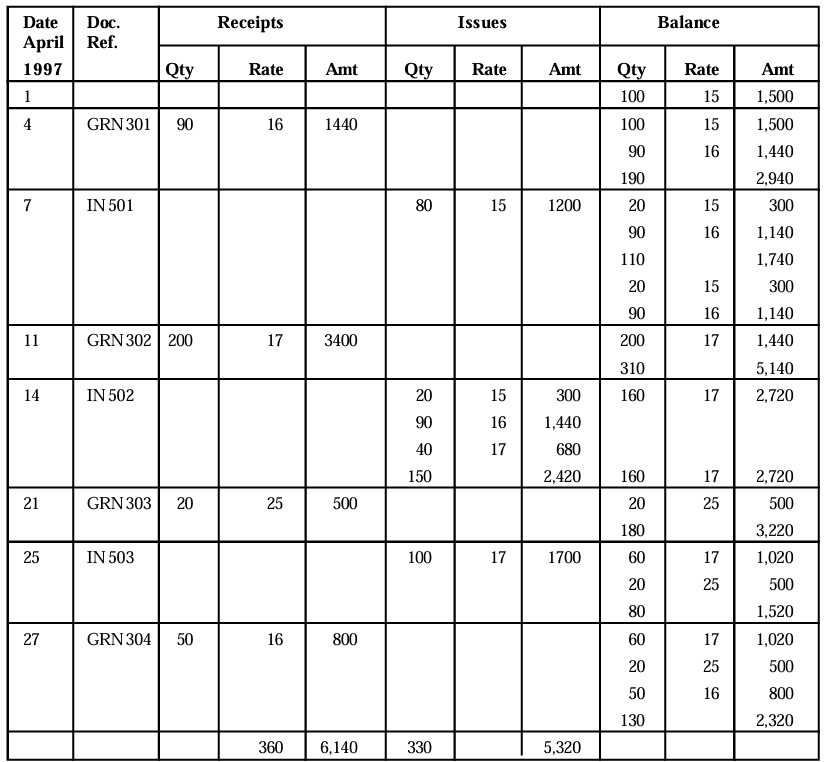

Example 2: From the following data you are required to compile a valued stock card in respect of material ‘Mikytoya’ for the month of April 2007 and value the closing stock by:

(a) Weighted average method

(b) First In First Out methnd

Sol: Stock Card (Weighted Average Method) FIFO Method

FIFO Method

Need for Material Control

- A crucial initial step in installing a cost and management accounting system is establishing proper control over materials and supplies from the moment they are ordered from suppliers until they are used in operations or sold as merchandise.

- Materials represent a significant asset and often constitute the largest expense in most businesses. Consequently, the efficiency of purchasing, storing, tracking, utilizing, and controlling materials can greatly influence a company’s success or failure.

- Without effective material control, surplus stock of certain items may accumulate, leading to unnecessary capital being tied up and potential losses due to deterioration and obsolescence. At the same time, shortages of other materials may occur at critical moments, causing production delays.

- Material purchasing is a specialized function that requires careful attention. A skilled buyer ensures that the right quantity and quality of materials are procured at the best price and delivered at the appropriate time. This contributes significantly to a business's overall efficiency and profitability. Effective material control helps eliminate waste and unnoticed losses.

- Proper control mechanisms minimize theft, mismanagement, deterioration, breakage, and excessive storage costs. Additionally, ensuring materials are readily available prevents unnecessary downtime in production.

- Finally, from a cost accounting perspective, accurate cost calculations depend on reliable records of material usage. If material issuance records are inadequate, cost statements will lack accuracy, undermining financial decision-making.

Requirements of a System of Material Control

The important requirements or essentials of adequate satisfactory system of materials control are as follows.

- Proper Coordination – Effective coordination among all departments involved in material purchasing, receiving, inspection, approval, storage, issuance, and accounting is crucial for efficient material management.

- Competent Purchasing Agent – Centralizing the purchasing function under a well-trained and competent purchasing agent ensures proper oversight and efficiency in procurement.

- Use of Standard Forms – Utilizing standardized forms for purchase orders, requisitions, and related documents with written and authorized instructions is essential for maintaining proper control over materials.

- Control through Budgeting – Implementing material, supply, and equipment budgets helps ensure cost efficiency in procurement and material usage.

- Storage Location – Materials and supplies should be stored in designated locations under strict supervision, with well-planned storage and issuance procedures.

- Perpetual Inventory System – A perpetual inventory system should be maintained to provide real-time tracking of stock levels and values, enabling comparisons between recorded and actual physical inventory.

- Setting Stock Levels – Minimum and maximum stock levels should be established to prevent inventory shortages or excessive stock accumulation. Additionally, reorder levels and economic order quantities should be determined for optimal purchasing.

- Storage Control and Issuance – A well-structured stores control system ensures materials are issued in the correct quantities and at the right time, based on departmental requisitions.

- Internal Checks – A system of internal checks should be in place to ensure that all material and equipment transactions are verified by reliable and independent officials.

- Controlling Accounts and Subsidiary Records – Maintaining controlling accounts and subsidiary records provides a detailed summary of material costs from procurement to consumption.

- Regular Reports – Periodic reports should be prepared for management, covering material purchases, stock issues, inventory balances, obsolete items, returned goods, and defective units, ensuring informed decision-making.

The document FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting | Cost Accounting - B Com is a part of the B Com Course Cost Accounting.

All you need of B Com at this link: B Com

|

103 videos|133 docs|14 tests

|

FAQs on FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting - Cost Accounting - B Com

| 1. What are FIFO, LIFO, and Weighted Average, and how are they related to material cost and cost accounting? |  |

Ans. FIFO (First-In, First-Out), LIFO (Last-In, First-Out), and Weighted Average are inventory costing methods used in cost accounting. These methods determine the value of ending inventory and cost of goods sold (COGS) based on the cost of materials or products. FIFO assumes that the first items purchased are the first items sold, LIFO assumes that the last items purchased are the first items sold, and Weighted Average assumes that all items have the same cost per unit regardless of when they were purchased.

| 2. What are the advantages and disadvantages of using FIFO, LIFO, and Weighted Average? | |

Ans. The advantages of using FIFO are that it generally results in higher net income during periods of inflation and better matches the physical flow of inventory. The disadvantages are that it can increase taxes and does not accurately reflect the current cost of inventory. The advantages of using LIFO are that it better matches the current cost of inventory and can result in lower taxes. The disadvantages are that it can result in lower net income during periods of inflation and does not accurately reflect the physical flow of inventory. The advantage of using Weighted Average is that it is simple and easy to calculate. The disadvantage is that it does not accurately reflect the physical flow of inventory or the current cost of inventory.

| 3. How does the choice of inventory costing method affect financial statements and income tax expense? | |

Ans. The choice of inventory costing method affects the value of ending inventory and cost of goods sold, which in turn affects the balance sheet and income statement. The method used can also affect income tax expense. For example, using FIFO during periods of inflation can result in higher net income and higher taxes, while using LIFO during the same period can result in lower net income and lower taxes.

| 4. Can a company switch inventory costing methods? | |

Ans. Yes, a company can switch inventory costing methods. However, the switch must be disclosed in the financial statements and the new method must be applied consistently going forward. In addition, the effect of the change on prior periods must be disclosed.

| 5. What factors should a company consider when choosing an inventory costing method? | |

Ans. A company should consider factors such as the nature of the business, the type of inventory, the stability of prices, the impact on financial statements, and tax implications. For example, a company with perishable goods may prefer FIFO to avoid spoilage, while a company with non-perishable goods may prefer LIFO to better match the current cost of inventory. Additionally, a company in an industry with stable prices may choose Weighted Average, while a company in an industry with fluctuating prices may choose FIFO or LIFO to better reflect the current cost of inventory.

About this Document

10.1K Views

4.64/5

Rating

Oct 08, 2025

Last updated

Related Exams

Document Description: FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting for B Com 2025 is part of Cost Accounting preparation.

The notes and questions for FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting have been prepared according to the B Com exam syllabus. Information about FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting covers topics

like Materials Costing Methods, First-In-Out (FIFO), Last-In First-Out (LIFO), Weighted Average Method (WAM), Need for Material Control, Requirements of a System of Material Control and FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting Example, for B Com 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting.

Introduction of FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting in English is available as part of our Cost Accounting

for B Com & FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting in Hindi for Cost Accounting course.

Download more important topics related with notes, lectures and mock test series for B Com

Exam by signing up for free. B Com: FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting | Cost Accounting - B Com

Description

Full syllabus notes, lecture & questions for FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting | Cost Accounting - B Com - B Com | Plus excerises question with solution to help you revise complete syllabus for Cost Accounting | Best notes, free PDF download

Information about FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting

In this doc you can find the meaning of FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting defined & explained in the simplest way possible. Besides explaining types of

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting theory, EduRev gives you an ample number of questions to practice FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting tests, examples and also practice B Com

tests

Related Searches

study material

,past year papers

,practice quizzes

,Important questions

,Summary

,Previous Year Questions with Solutions

,Exam

,ppt

,Extra Questions

,LIFO & Weighted Average - Material Cost

,mock tests for examination

,FIFO

,MCQs

,Cost Accounting | Cost Accounting - B Com

,Cost Accounting | Cost Accounting - B Com

,Cost Accounting | Cost Accounting - B Com

,LIFO & Weighted Average - Material Cost

,LIFO & Weighted Average - Material Cost

,shortcuts and tricks

,video lectures

,Free

,Objective type Questions

,Sample Paper

,Semester Notes

,FIFO

,FIFO

,Viva Questions

;

Additional Information about FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting for B Com Preparation

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting Free PDF Download

The FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting is an invaluable resource that delves deep into the core of the B Com exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting now and kickstart your journey towards success in the B Com exam.

Importance of FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting

The importance of FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting cannot be overstated, especially for B Com aspirants.

This document holds the key to success in the B Com exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting Notes

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting Notes on EduRev are your ultimate resource for success.

FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting B Com Questions

The "FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting B Com Questions" guide is a valuable resource for all aspiring students preparing for the

B Com exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting on the App

Students of B Com can study FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of FIFO, LIFO & Weighted Average - Material Cost, Cost Accounting is prepared as per the latest B Com syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup on EduRev and stay on top of your study goals

10M+ students crushing their study goals daily