ICAI Notes 2.4, Subsidiary Books - CA Foundation PDF Download

Learning Objectives

After studying this unit, you will be able to :

- Understand the techniques of recording transactions in Purchase Book, Sales Book; Returns Inward Book and Returns outward book; Bills Receivable and Bills Payable book.

- Learn the technique of posting from Subsidiary Books to Ledger.

- Understand that even if subsidiary books are maintained, journalisation is required for many other transactions and events.

- Learn the difference between the subsidiary books and principle books.

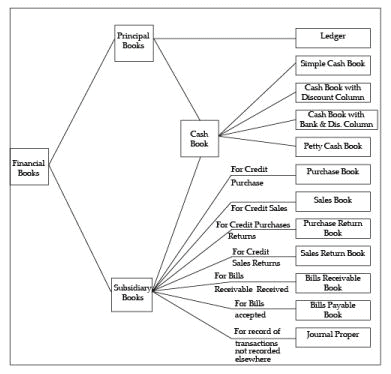

1. SUBSIDIARY BOOKS AND THEIR ADVANTAGES

In a Business most of the transactions generally relate to receipts and payments of cash, sale of goods and their purchase. It is convenient to keep a separate register for each such class of transactions one for receipts and payments of cash, one for purchase of goods and one for sale of goods. A register of this type is called a book of original entry or of prime entry. For transactions recorded in such books there will be no journal entry. The system by which transactions of a class are first recorded in the book, specially meant for it and on the basis of which ledger accounts are then prepared is known as the Practical System of Book keeping or even the English System. It should be noted that in this system, there is no departure from the rules of the double entry system.

These books of original or prime entry are also called subsidiary books since ledger accounts are prepared on their basis and, without the further process of ledger posting, a trial balance cannot be taken out.

Normally, the following subsidiary books are used in a business:

(i) Cash book to record receipts and payments of cash, including receipts into and payments out of the bank.

(ii) Purchases book to record credit purchases of goods dealt in or of the materials and stores required in the factory.

(iii) Purchase Returns Books to record the returns of goods and materials previously purchased.

(iv) Sales Book to record the sales of the goods dealt in by the firm.

(v) Sale Returns Book to record the returns made by the customers.

(vi) Bills receivable books to record the receipts of promissory notes or hundies from various parties.

(vii) Bills Payable Book to record the issue of the promissory notes or hundies to other parties.

(viii) Journal (proper) to record the transactions which cannot be recorded in any of the seven books mentioned above.

It may be noted that in all the above cases the word “Journal” may be used for the word “book”

Advantages of Subsidiary Books The use of subsidiary books affords the undermentioned advantages :

(i) Division of work : Since in the place of one journal there will be so many subsidiary books, the accounting work may be divided amongst a number of clerks.

(ii) Specialisation and efficiency : When the same work is allotted to a particular person over a period of time, he acquires full knowledge of it and becomes efficient in handling it. Thus the accounting work will be done efficiently.

(iii) Saving of the time : Various acconting processes can be undertaken simultaneously because of the use of a number of books. This will lead to the work being completed quickly.

(iv) Availability of informations : Since a separate register or book is kept for each class of transactions, the information relating to each transactions will be available at one place.

(v) Facility in checking: When the trial balance does not agree, the location of the error or errors is facilitated by the existence of separate books. Even the commission of errors and frauds will be checked by the use of various subsidiary books.

2. DISTINCTION BETWEEN SUBSIDIARY BOOKS AND PRIMARY BOOKS

The books in which transactions are first recorded to enable processing are called subsidiary books. The ledger and the cash book are the principle books since they furnish information for preparation of the trial balance and financial statements. The following chart will help you in understanding the difference between Subsidiary Books and Primary Books.

3. PURCHASES BOOK

To record the credit purchases of goods dealt in or materials and stores used in the factory, a separate register called the Purchases Book or the Purchases Journal, is usually maintained by firms. The ruling is given below:

It should be remembered that :

(i) Cash purchases are not entered in this book since these will be entered in the cash book; and

(ii) Credit purchases of things other than goods or materials, such as office furniture or typewriters are journalised -they also are not entered in the Purchases Book.

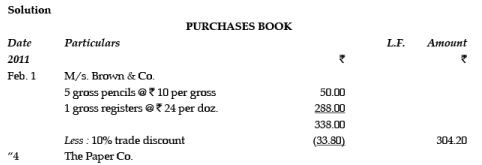

The particulars column is meant to record the name of the supplier and name of the articles purchased and the respective quantities. The amount in respect of each article is entered in the details column. After totaling the various amounts included in a single purchase, the amount for packing, or other charges is added and the amount for trade discount is deducted. The net amount is entered in the extreme right-hand column. The total in this column shows the total purchase made in a period.

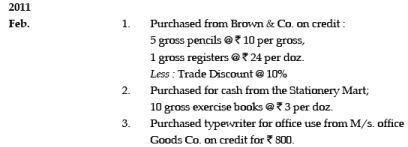

Illustration 1 The Rough Book of M/s. Narain & Co. contains the following :

Note : Purchases of cash and purchase for typewriter cannot be entered in the Purchase Book.

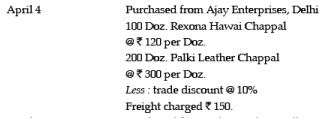

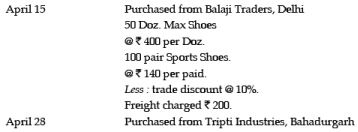

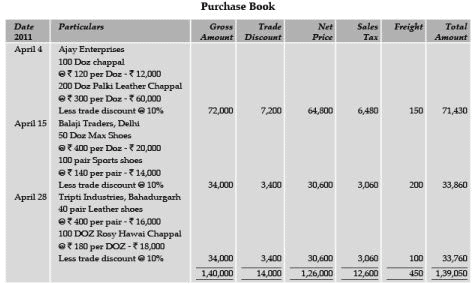

Illustration 2 Enter the following transactions in Purchase Book and post them into ledger.

2011

Purchase Account will be debited by net price and sales tax because sales tax is a part of cost of goods purchased.

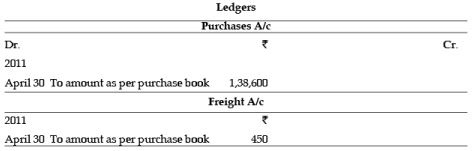

3.1 POSTING THE PURCHASES BOOK

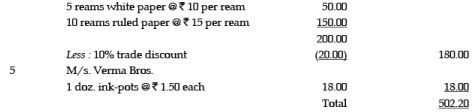

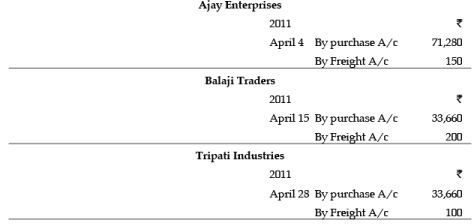

The Purchases Book shows the names of the parties from whom goods have been purchased on credit. These parties are now trade payables. Their accounts have to be credited for the respective amounts shown in the purchase book. The total of the amounts column shows the total purchases made in a period. The amount is debited to the Purchase Account to indicate receipt of goods. In illustration 11, the Purchases Account is debited by ` 502.12, M/s. Brown & Co. is credited by ` 304.12, the Paper Company by ` 180 and M/s. Verma Bros. by ` 18. The total of the amounts put on the credit side equals the debit. Thus the double entry is completed.

4. SALES BOOK

The Sales Book is a register specially kept to record credit sales of goods dealt in by the firm,cash sales are entered in the Cash Book and not in the Sales Book. Credit sales of things, other than the goods dealt in by the firm are not entered in the Sales Book ; they are journalised. The ruling is the same as for the Purchases Book.

Entries in the sales book are also made in the same manner as in the Purchase Book. The particulars column will record the name of the customers concerned together with particulars and quantities of the goods sold. For each item, the amount is entered in the details column ; after totalling the amounts for one sale, charges for packing etc; are added and the trade discount, if any is deducted: the net amount is put in the outer column. The total of this column will show the total credit sales for a period.

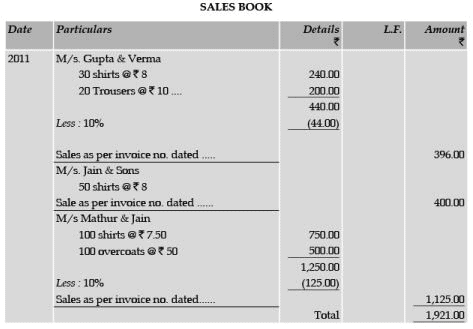

Illustration 3 The following are some of the transaction of M/s Kishore & Sons of the year 2011 as per their Waste Book. Make out their Sales Book.

Sold to M/s. Gupta & Verma on credit:

30 shirts @  8 per shirt.

8 per shirt.

20 trousers @ 10 per trouser.

Less : Trade Discount @ 10% Sold furniture to M/s. Sehgal & Co. on credit 80.

Sold 50 shirts of M/s. Jain & Sons @ 8 per shirt.

Sold 13 shirts to Cheap Stores @ 7.50 each for cash.

Sold on credit to M/s. Mathur & Jain.

100 shirts @ 7.50 per shirt

10 overcoats @50 per overcoat.

Less: Trade Discount @ 10%

Solution

Note : Cash sale and sale of furniture are not entered in Sales Book.

4.1 POSTING THE SALES BOOK

The names appearing in the Sales Book are of those parties which have received the goods. The accounts of the parties have to be debited with the respective amounts. The total of the Sales Book shows the credit sales made during the period concerned; the amount is credited to the Sales Account. In the illustration 12, 1,921 is credited to the Sales Account; 396 is debited to M/s. Gupta and Verma 400 to M/s Jain and Sons and1,125 to M/s Mathur & Jain. The amount put on the credit side is equal to the total of the amount put on the debit side. Thus, the double entry principle is followed correctly.

4.2. SALES BOOK WITH SALES TAX COLUMN

Sales Tax is one levied at the point of sales. Sales tax is collected by the seller from the customers on sales of goods and deposited the same with the state government. Sales tax is charged at a fixed percentage on the net price of the goods. It is calculated after giving trade discount, if any. Generally a separate column is provided in the Sales Book for sales tax so that a proper record is maintained regarding sales tax collected. Rates of sales tax vary from item to item and also on local sales and interstate sales (or say central sales). A separate column in sales book for each rate of sales tax helps the dealer in calculating sales tax liability accurately.

At the end of a certain period, generally quarterly or monthly, the total of sales tax column is credited to the Sales Tax Account. When sales tax is deposited with the sales tax department, the Sales Tax Account is debited and Cash/Bank Account is credited. When there is any credit balance in Sales Tax Account, it shows the amount payable as sales tax and hence be shown in the Balance Sheet as a liability.

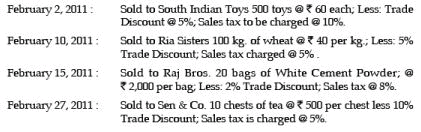

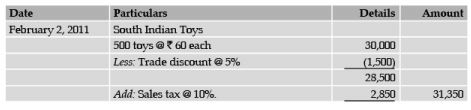

Illustration 4

Record the following transactions in Sales Book.

Solution Sales Book

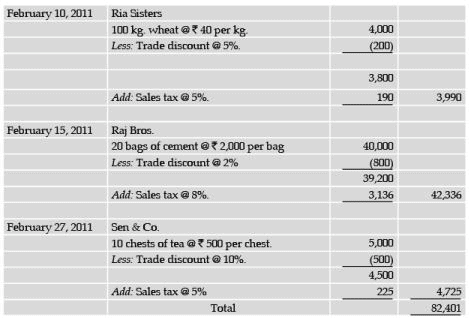

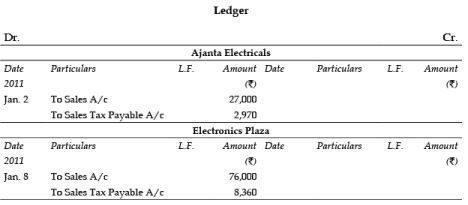

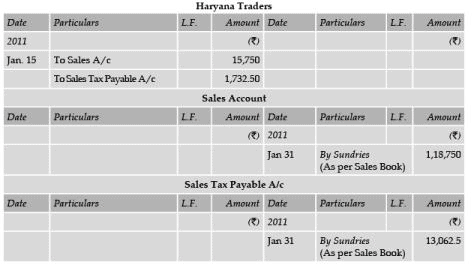

Illustration 5 Enter the following transactions in Sales Book of M/s. Pranat Engineers Ltd., Delhi -2011

Jan. 2. Sold to M/s. Ajanta Electricals, Delhi 5 pieces of colour T.V. @ 6,000/- each less trade Discount @10%

8 Sold to M/s. Ajanta Electricals Plaza, 10 pieces of Washing Machines @ 8,000/- each less trade discount 5%.

15 Sold to M/s. Haryana Traders, 5 pieces of Black & White T.V. @ 3,500/- each less trade discount @ 10%.

All sales are subject to 10% Sales Tax and 10% surcharge on sales tax.

Solution

Posting

If separate column of sales tax is provided then, each individual Trade receivable account will be debited by the total amount of respective sales bill, Sales Account and Sales Tax Payable Account shall be credited with the total of column of net sales and sales tax respectively.

Illustration 6 Post into the ledger the entries of Sales Book prepared in illustration 5.

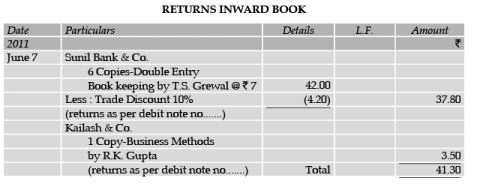

5. SALES RETURNS BOOK OR RETURNS INWARD BOOK

If customers frequently return the goods sold to them, it would be convenient to record the returns in a separate book, which is named as the Sales Returns Book or the returns Inward Book. The ruling of the book is similar to the Purchases or the Sales Book and entries are also made in the same manner. The following, assumed figures, will illustrate this:

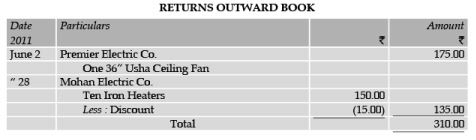

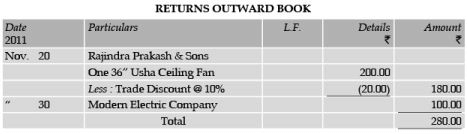

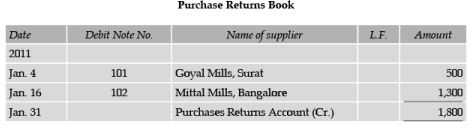

6. PURCHASE RETURNS OR RETURNS OUTWARD BOOK

Such a book conveniently records return of goods or material purchased to the suppliers-if however, the returns are not frequent, it may be sufficient to record the transaction in the journal. The ruling of the Purchase Returns or Returns Outward Book is similar to that of the Purchase Book; entries are also similarly made, as the illustration given below shows:

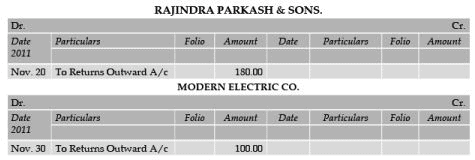

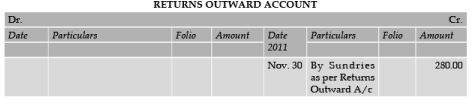

6.1 POSTING OF THE RETURN BOOKS

The Sales Return Book will show the total of the returns made by customers. Really, the total of the returns is in reduction of the sales. Properly, therefore, the amount may be debited to the Sales Account but, usually, a separate account called Returns Inward Account is opened and the total of the sales returns is debited to this accounts. The customers who have returned the goods are credited with the respective amounts.

It should be noted that on goods being received and accepted back from the customers, a credit note is issued to the customers concerned. This shows the amount to be credited to the customer’s account.

Similarly, when goods are returned to suppliers they will issue the necessary credit note; also the firm returning the goods will issue a debit note to the supplier, indicating the amount for which the supplier is liable on account of the return.

The total of Returns Outwards Book shows the total returns made. The amount can be credited to the purchase Account, but in practice, is credited to a separate account called Purchase Returns or Returns Outward Account. The suppliers whose names appear in the Book have received the goods, so their accounts have to be debited. This is shown in the illustration given below : Illustration 7 Post the following into the ledger

Solution LEDGER

6.2 BILLS RECEIVABLE BOOKS AND BILLS PAYABLE BOOKS

If the firm usually receives a number of promissory notes or hundies, it would be convenient to record the transaction in a separate book called the Bills Receivable Book. Similarly, if promissory notes or hundies are frequently issued, the Bills Payable Book will be convenient. This will be discussed later.

7. IMPORTANCE OF JOURNAL

Students are now familiar with the journal. They also know that :

(i) Cash transactions are recorded in the cash book;

(ii) Credit purchases of goods or materials are recorded in the purchases book;

(iii) Credit sales of goods are recorded in the sales book ;

(iv) Returns from customers are recorded in the sale returns book; and

(v) Returns to suppliers are entered in the purchase returns book.

Bill transactions are entered in the bills receivable books or the bills payable books, if these are maintained. Apart from the transactions mentioned above, there are some entries also which have to be recorded. For them the proper place is the journal. In fact, if there is no special book meant to record a transaction, it is recorded in the journal (proper). The role of the journal is thus restricted to the following types of entries :

(i) Opening entries : When books are started for the new year, the opening balance of assets and liabilities are journalised.

(ii) Closing entries : At the end of the year the profit and loss account has to be prepared. For this purpose, the nominal accounts are transferred to this account. This is done through journal entries called closing entries.

(iii) Rectification entries : If an error has been committed, it is rectified through a journal entry.

(iv) Transfer entries : If some amount is to be transferred from one account to another, the transfer will be made through a journal entry. (v) Adjusting entries : At the end of the year the amount of expenses or income may have to be adjusted for amounts received in advance or for amounts not yet settled in cash. Such an adjustment is also made through journal entries. Usually, the entries pertain to the following:

(a) Outstanding expenses, i.e., expenses incurred but not yet paid;

(b) Prepared expenses, i.e., expenses paid in advance for some period in the future;

(c) Interest on capital, i.e., the interest which the proprietor thinks proper to allow on his investment; and

(d) Depreciation, i.e., fall in the value of the assets used on account of wear and tear.

For all these, journal entries are necessary.

(vi) Entries on dishonour of Bills : If someone who accepted a promissory note (or bill) and is not able to pay in on the due date,a journal entry will be necessary to record the non-payment or dishonour.

(vii) Miscellaneous entries : The following entries will also require journalising:

(a) Credit purchase of things other than goods dealt in or materials required for production of goods e.g. credit purchase of furniture or machinery will be journalised.

(b) An allowance to be given to the customers or a charge to be made to them after the issue of the invoice.

(c) Receipt of promissory notes or issue to them if separate bill books have not been maintained.

(d) On an amount becoming irrecoverable, say, because, of the customer becoming insolvent.

(e) Effects of accidents such as loss of property by fire.

(f) Transfer of net profit to capital account.

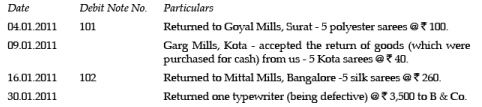

Illustration 8 From the following transactions, prepare the Purchases Returns Book of Alpha & Co., a Saree dealer and post them to ledger :

Solution

FAQs on ICAI Notes 2.4, Subsidiary Books - CA Foundation

| 1. What are subsidiary books in accounting? |  |

| 2. What is the purpose of using subsidiary books in accounting? | |

| 3. What is a cash book and how is it used in subsidiary books? | |

| 4. How is a sales book used in subsidiary books? | |

| 5. What is the significance of subsidiary books in financial reporting? | |

Subsidiary Books - CA Foundation

,ppt

,ICAI Notes 2.4

,ICAI Notes 2.4

,Semester Notes

,practice quizzes

,Summary

,Important questions

,Viva Questions

,Objective type Questions

,ICAI Notes 2.4

,Previous Year Questions with Solutions

,Subsidiary Books - CA Foundation

,Free

,Exam

,Sample Paper

,MCQs

,past year papers

,Subsidiary Books - CA Foundation

,Extra Questions

,video lectures

,shortcuts and tricks

,mock tests for examination

,study material

;

ICAI Notes 2.4, Subsidiary Books Free PDF Download

Importance of ICAI Notes 2.4, Subsidiary Books

ICAI Notes 2.4, Subsidiary Books

ICAI Notes 2.4, Subsidiary Books CA Foundation Questions

Study ICAI Notes 2.4, Subsidiary Books on the App

|

© EduRev

|

Education Revolution

|

|