ICAI Notes 9.3: Redemption of Preference Shares - 3 - CA Foundation PDF Download

5. REDEMPTION OF PARTLY CALLED-UP PREFERENCE SHARES

One of the conditions of redemption is that only fully paid up preference shares can be redeemed by a company. If the examination problem states that it is decided to redeem preference shares which are partly called up, then it is assumed that final call on these shares is demanded and received before proceeding with redemption of these shares. If information about both fully paid and partly paid preference shares is provided, then, only fully paid shares are redeemed.

Illustration 11

The Balance Sheet of XYZ as at 31st December, 2012 inter alia includes the following:

| Rs | |

| 50,000, 8% Preference Shares of Rs 100 each, Rs 70 paid up | 35,00,000 |

| 1,00,000 Equity Shares of Rs 100 each fully paid up | 1,00,00,000 |

| Securities Premium | 5,00,000 |

| Capital Redemption Reserve | 20,00,000 |

| General Reserve | 50,00,000 |

Under the terms of their issue, the preference shares are redeemable on 31st March, 2013 at 5% premium. In order to finance the redemption, the company makes a rights issue of 50,000 equity shares of Rs 100 each at Rs 110 per share, Rs 20 being payable on application, Rs 35 (including premium) on allotment and the balance on 1st January, 2014. The issue was fully subscribed and allotment made on 1st March, 2013. The money due on allotment were received by 31st March, 2013. The preference shares were redeemed after fulfilling the necessary conditions of Section 55 of the Companies Act, 2013. The company decided to make minimum utilisation of general reserve.

You are asked to pass the necessary Journal Entries and show the relevant extracts from the balance sheet as on 31st March, 2013 with the corresponding figures as on 31st December, 2012.

Solution

Journal Entries

| Rs | Rs | ||

| 8% Preference Share Final Call A/c | Dr. | 15,00,000 | |

| To 8% Preference Share Capital A/c | 15,00,000 | ||

| (For final call made on preference shares @ Rs 30 each to make them fully paid up) | |||

| Bank A/c | Dr. | 15,00,000 | |

| To 8% Preference Share Final Call A/c | 15,00,000 | ||

| (For receipt of final call money on preference shares) | |||

| Bank A/c | Dr. | 10,00,000 | |

| To Equity Share Application A/c | 10,00,000 | ||

| (For receipt of application money on 50,000 equity shares @ Rs 20 per share) | |||

| Equity Share Application A/c | Dr. | 10,00,000 | |

| To Equity Share Capital A/c | 10,00,000 | ||

| (For capitalisation of application money received) | |||

| Equity Share Allotment A/c | Dr. | 17,50,000 | |

| To Equity Share Capital A/c | 12,50,000 | ||

| To Securities Premium A/c | 5,00,000 | ||

| (For allotment money due on 50,000 equity shares @ Rs 35 per share including a premium of Rs 10 per share) | |||

| Bank A/c | Dr | 17,50,000 | |

| To Equity Share Allotment A/c | 17,50,000 | ||

| (For receipt of allotment money on equity shares) | |||

| 8% Preference Share Capital A/c | Dr | 50,00,000 | |

| Premium on Redemption of Preference Shares A/c | Dr. | 2,50,000 | |

| To Preference Shareholders A/c | 52,50,000 | ||

| (For amount payable to preference shareholders on redemption at 5% premium) | |||

| Securities Premium A/c | Dr. | 2,50,000 | |

| To Premium on Redemption A/c | 2,50,000 | ||

| (For writing off premium on redemption of preference shares) | |||

| General Reserve A/c | Dr. | 27,50,000 | |

| To Capital Redemption Reserve A/c | 27,50,000 | ||

| (For transfer of CRR the amount not covered by the proceeds of fresh issue of equity shares i.e., 50,00,000 - 10,00,000 - 12,50,000) | |||

| Preference Shareholders A/c | Dr. | 52,50,000 | |

| To Bank A/c | 52,50,000 | ||

| (For amount paid to preference shareholders) |

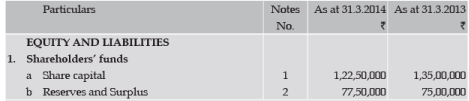

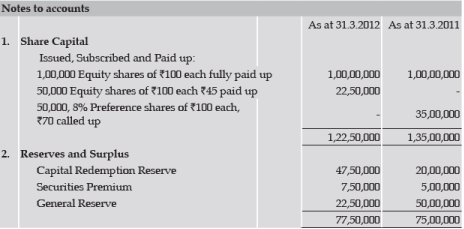

Balance Sheet (extracts)

Note: Amount received (excluding premium) on fresh issue of shares till the date of redemption should be considered for calculation of proceeds of fresh issue of shares. Thus, proceeds of fresh issue of shares are ` 22,50,000 (` 10,00,000 application money plus ` 12,50,000 received on allotment towards share capital).

6. REDEMPTION OF FULLY CALLED BUT PARTLY PAID-UP PREFERENCE SHARES

The problem of unpaid calls on fully called up shares may be studied under following categories:

6.1 WHEN CALLS-IN-ARREARS IS RECEIVED By THE COMPANY

If the amount of unpaid calls is received by the Company before redemption, the entry passed is as under:

After receipt of calls in arrears, the shares become fully paid up and, then, company can proceed with redemption in the normal course.

6.2 IN CASE OF FORFEITED SHARES

If, on getting a proper notice from the company, the shareholders fail to pay the unpaid calls, the Board of Directors may decide to forfeit the shares and cancel these shares instead of reissuing the forfeited shares because redemption of these share is due immediately or in near future. In this case, entry for forfeiture is passed as usual.

FAQs on ICAI Notes 9.3: Redemption of Preference Shares - 3 - CA Foundation

| 1. What is the meaning of redemption of preference shares? |  |

| 2. What are the ways in which preference shares can be redeemed? | |

| 3. What is the difference between redemption of preference shares and buyback of shares? | |

| 4. Can a company redeem its preference shares before the specified redemption date? | |

| 5. What happens to the preference shareholders after the redemption of their shares? | |

Important questions

,ICAI Notes 9.3: Redemption of Preference Shares - 3 - CA Foundation

,Viva Questions

,Exam

,study material

,practice quizzes

,Extra Questions

,Free

,mock tests for examination

,Objective type Questions

,ICAI Notes 9.3: Redemption of Preference Shares - 3 - CA Foundation

,Summary

,Sample Paper

,Semester Notes

,ppt

,shortcuts and tricks

,MCQs

,past year papers

,Previous Year Questions with Solutions

,ICAI Notes 9.3: Redemption of Preference Shares - 3 - CA Foundation

,video lectures

;

ICAI Notes 9.3: Redemption of Preference Shares - 3 Free PDF Download

Importance of ICAI Notes 9.3: Redemption of Preference Shares - 3

ICAI Notes 9.3: Redemption of Preference Shares - 3

ICAI Notes 9.3: Redemption of Preference Shares - 3 CA Foundation Questions

Study ICAI Notes 9.3: Redemption of Preference Shares - 3 on the App

|

© EduRev

|

Education Revolution

|

|