CBSE Accounts Sample Paper - 2 (2018-19) | Sample Papers for Class 12 Commerce PDF Download

CBSE SAMPLE QUESTION PAPER ACCOUNTANCY (055) CLASS-XII

Time allowed: 3 hours

Max Marks : 80

General Instructions:

(1) This question paper contains two parts A and B.

(2) Part A is compulsory for all.

(3) Attempt only one option of Part B.

(4) Part A contains 17 questions of which:

Question 1 to 6 are carry 1 mark each.

Question 7 to 11 are carry 3 marks each.

Question 11 and 12 are carry 4 marks each.

Question 13 to 15 are carry 6 marks each.

Question 16 and 17 are carry 8 marks each.

Part A: ACCOUNTING FOR PARTNERSHIP FIRMS AND COMPANIES

Q1. Any change in the relationship of existing partners which results in an end of the existing agreement and enforces making of a new agreement is called

(a) Revaluation of partnership.

(b) Reconstitution of partnership.

(c) Realization of partnership.

(d) None of these.

Ans. (b) Reconstitution of partnership.

Q2. Karan, Nakul and Asha were partners in a firm sharing profits and losses in the ratio 3:2:1. At the time of admission of partner, the goodwill of the firm was valued at Rs. 2,00,000. The accountant of the firm passed the entry in the books of accounts and thereafter showed goodwill at Rs. 2,00,000 as an asset in the Balance Sheet. Was he correct in doing so? Why?

Ans. No, the accountant’s decision is not correct because according to AS-26, goodwill should be recorded in the books only when consideration in money or money’s worth has been paid for it.

Q3. Anu, Bina and Charan are partners. The firm, had given a loan of Rs. 20,000 to Bina. They decided to dissolve the firm. In the event of dissolution, the loan will be settled by:

(a) Transferring it to debit side of Realization account.

(b) Transferring it to credit side of Realization account.

(c) Transferring it to debit side of Bina’s capital account.

(d) Bina paying Anu and Charan privately.

Ans. (C) Transferring it to debit side of Bina’s capital account.

Q4. Differentiate between ‘Capital Reserve’ and ‘Reserve Capital’.

Ans. ‘Capital Reserve’ is the reserve that is created out of capital profits/gains whereas, that part of the share capital which has not yet been called up and has been kept as reserve to be called up in the event of the winding up of the company is called ‘Reserve Capital’

Q5. Metcalf Ltd. Issued 50,000 shares of Rs. 100 each payable Rs. 20 on application (on 1st May 2012); Rs. 30 on allotment (on 1st January 2013); Rs. 20 first call (on 1st July 2013) and the balance on final call (on 1st February 2014). Shankar, a shareholder holding 5,000 shares did not pay the first call on the due date. The second call was made and Shankar paid the first call amount along with second call. All sums due were received.

Total amount received on 1st February was:

(a) Rs. 15,00,000

(b) Rs. 16,00,000

(c) Rs. 10,00,000

(d) Rs. 11,00,000

Ans. Rs. 16,00,000.

Q6. Abha and Beena were partners sharing profits and losses in the ratio of 3:2. On April 1st 2013, they decided to admit Chanda for 1/5th share in the profits. They had a reserve of Rs. 25,000 which they wanted to show in their new balance sheet. Chanda agreed and the necessary adjustments were made in the books. On October 1st 2013, Abha met with an accident and died. Beena and Chanda decided to admit Abha’s daughter Fiza in their partnership, who agreed to bring Rs. 2,00,000 as capital. Calculate Abha’s share in the reserve on the date of her death.

Ans. Rs. 12,000.

Q7. State any three purposes for which securities premium can be utilized.

Ans. The amount received as securities premium can be used for following purposes (any

three):

(a) In purchasing its own shares.

(b) Issuing fully paid bonus shares to the members.

(c) Writing off preliminary expenses of the company.

(d) Writing off the expenses of, or the commission paid, or discount allowed on any issue of

securities or debentures of the company.

(e) Providing for the premium payable on the redemption of any redeemable preferences

shares or any debentures of the company.

Q8. Ankur and Bobby were into the business of providing software solution in India. They were sharing profits and losses in the ratio 3:2. They admitted Rohit for a 1/5 share in the firm. Rohit, an alumni of ITT, Chennai would help them to expand their business to various South African countries where he had been working earlier. Rohit is guaranteed a minimum profit of Rs. 2,00,000 for the year. Any deficiency in Rohit’s share is to be borne by Ankur and Bobby in the ratio 4:1. Losses for the year were Rs. 10,00,000. Pass the necessary journal entries.

Ans.

Journal

Date | Particulars | L.F | Debit (Rs.) | Credit (Rs.) |

| Ankur’s Capital A/c Dr. Bobby’s Capital A/cDr. Rohit’s Capital A/cDr. To Profit and Loss A/c (Being loss debited to partners’ capital accounts) | 4.80.000 3.20.000 10,00,000 2,00,000 4,00,000 3.20.000 80.000 | ||

Ankur’s Capital A/c Dr. Bobby’s Capital A/cDr. To Rhoit’s Capital A/c (being the deficiency borne by Ankur and Bobby in the ratio 4:1) | ||||

Q9. Newbie Ltd. Was registered with an authorized capital of Rs. 5,00,000 divided into 50,000 equity shares of Rs. 10 each. Since the economy was in robust shape, the company decided to offer to the public for subscription 30,000 equity shares of Rs. 10 each at a premium of Rs. 20 per share. Applications for 28,000 shares were received and allotment was made to all applicants. All calls were made and duly received except the final call of Rs.2 per share on 200 shares. Show the ‘Share Capital’ in the Balance Sheet of Newbie Ltd. As per Schedule VI of the Companies Act 1956. Also prepare Notes to

Accounts for the same.

Ans.

Balance Sheet of Newbie Ltd. as at:

Particulars | Note No. | (Rs.) |

Equity and Liabilities (1) Shareholders’ funds Share capital | 1 | 2,79,600 |

Notes to Accounts

Particulars | (Rs.) |

1. Share Capital Authorized Share Capital

Issued Share Capital

Subscribed Share Capital Subscribed and not fully paid

Less calls in arrears(400) | 5,00,000 |

3,00,000 | |

2,79,600 |

Q10. Drumbeats Ltd. Had a prosperous shoe business. They were manufacturing shoes in India and exporting to Italy. Being a socially aware organization, they wanted to pay

back to the society. They decided to not only supply free shoes to 50 orphanages in various parts of the country but also given employment to children from those

orphanages who were above 18 years of age. In order to meet the fund requirements, they decided to raise 50,000 equity shares of Rs. 50 each and 40,000 9% debentures of Rs. 40 each. Pass the necessary journal entries for issue of shares and debentures. Also identify one value which the company wants to communicate to the society.

Ans.

Journal

Particulars | L.F | Debit (Rs.) | Credit (Rs.) |

Bank A/c Dr. To Share Application and Allotment A/c (Being the amount of application money received on 50,000 shares @ Rs. 50 per share) |

| 25,00,000 | 25,00,000 |

Share Application and Allotment A/c Dr. To Share Capital A/c (Being the amount transferred to share capital) |

| 25,00,000 | 25,00,000 |

Bank A/cDr. To 9% Debentures Application and Allotment A/c (Being the amount received on 9% Debenture application and allotment on 40,000 Debentures @ Rs. 40 per debentures) |

| 16,00,000 | 16,00,000 |

9% Debentures Application and Allotment A/c Dr. To 9% Debentures A/c (Being The amount transferred to Debentures A/c.) |

| 16,00,000 | 16,00,000 |

Value which the company wants to communicate to the society: (Any one)

· Social responsibility

· Generation of employment opportunities.

Q11. Following is the Balance Sheet of Punita, Rashi and Seema who are sharing profits in

the ratio 2:1:2 as on 31st March 2013.

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Creditors | 38,000 | Building | 2,40,000 |

| Bill Payable | 2,000 | Stock | 65,000 |

| Capitals: |

| Debtors | 30,000 |

| Punita1,44,000 |

| Cash at bank | 5,000 |

| Rashi92,000 | 3,60,000 | Profit and Loss Account | 60,000 |

Punita died on 30th September 2013. She had withdrawn 44,000 from her capital on July 1,2013. According to the partnership agreement, she was entitled to interest on capital @8% p.a. Her share of profit till the date of death was to be calculated on the basis of the average profits of the last three years. Goodwill was to be calculated on the years ended 2009-10, 2010-11 and 2011-12 were Rs. 30,000, Rs. 70,000 and Rs. 80,000 respoectively.

Prepare Punita’s account to be rendered to her executors.

Ans.

Punita’s Capital Account

Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

|

| By Balance b/d | 1,00,000 |

To P&L A/c | 24,000 | By interest on capital | 4,880, |

To Punita’s A/c | 1,22,880 | By P&L Suspense A/c | 6,000 |

Executor’s A/c | By Rashi’s Capital A/c By Seema’s Capital A/c | 12,000 24,000 | |

| 1,46,880 |

| 1,46,880 |

Q12. Kanika and Gautam are partners doing a dry cleaning business in Lucknow sharing profits in the ration 2:1 with capitals Rs. 5,00,000 and Rs. 4,00,000 respectively. Kanika withdrew the following amounts during the year to pay the hosted expenses of her son.

Rs. 1st Aprila - 10,000

1st June - 9,000

1st Nov - 14,000

1st Dec. - 5,000

Gautam withdrew Rs. 15,000 on the first day of April, July, October and January to pay rent for the accommodation of his family. He also paid Rs. 20,000 per month as rent for

the office of partnership which was in a nearby shipping complex.

Calculate interest on Drawings @6% p.a.

Ans.

Calculation of Interest on drawings:

Kanika

3,00,000

Gautam

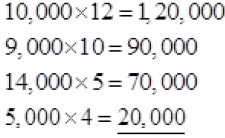

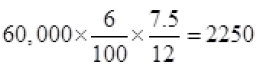

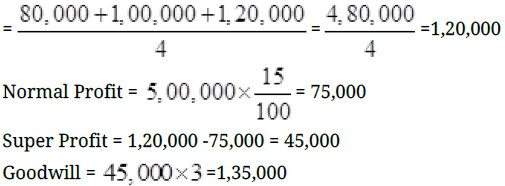

Q13. (a) A firm earned profits of Rs. 80,000, Rs. 1,00,000, Rs. 1,20,000 and Rs. 1,80,000 during 2010-11, 2011-12, 2012-13 and 2013-14 respectively. The firm has capital

investment of Rs. 5,00,000. A fair rate of return on investment is 15% p.a. Calculate goodwill of the firm based on three years’ purchase of average super profits of last four years.

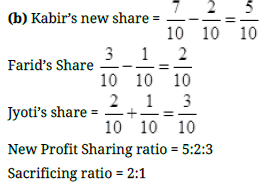

(b) Kabir and Farid are partners sharing profits and losses in the ratio of 7:3. Kabir surrenders 2/10th from his share and Farid surrenders 1/10ths form his share in favor of jyoti, a new partner. Calculate new profit sharing ratio and sacrificing ratio.

Ans. (a) Average Profit Method =

Q14. (a) Sunrise Company Ltd. Has an equity share capital of Rs. 10,00,000. The company earns a return on investment of 15% on its capital. The company need funds for diversification. The finance manager had the following options: (i) Borrow Rs. 5,00,000 @15% p.a. from a bank payable in four equal quarterly installments starting from the end of the fifth year (ii) Issue Rs. 5,00,000, 9% Debentures of Rs. 100 each redeemable at a premium of 10% after five years. To increase the return to the shareholders, the company opted for option

(ii) Pass the necessary journal entries for issue of debentures.

(b) Walter Ltd. Issued Rs. 6,00,000 8% Debentures of Rs.100 each redeemable after 3 years either by draw of lots or by purchase in the open market. At the end of three years, finding the market price of debentures at Rs. 95 per debenture. It purchased all its debentures for immediate cancellation. Pass necessary journal entries for cancellation of debentures assuming the company has sufficient balance in Debenture Redemption Reserve.

Ans. (a)

| Date | Particulars | L.F | Debit (Rs.) | Credit (Rs.) |

|

| Bank A/c Dr. To 9% Debenture Application and Allotment A/c (Being Debenture application money received) |

| 5,00,000 | 5,00,000 |

|

| 9% Debenture Application and Allotment A/c Dr. Loss on issue of Debentures A/c Dr. |

|

|

|

| To 9% Debenture A/c To Premium on redemption of Debentures A/c (Being issue of debentures at par, redeemable at a premium) |

| 5,00,000 50,000 | 5,00,000 50,000 |

| Own debentures A/c Dr. To Bank A/c (Being 60,000 debentures purchased for cancellation @ Rs.75) |

| 5,70,000 | 5,70,000 |

| 8% Debentures A/c Dr. To Own Debentures A/c To Gain on Cancellation of Debentures A/c (Being debentures cancelled) |

| 6,00,000 | 5.70.000 30.000 |

| Gain on Cancellation of Debentures A/c Dr. To Capital Reserve (Being the gain transferred to Capital Reserve) |

| 30,000 | 30,000 |

| Debenture Redemption Reserve A/c Dr. To General Reserve (Being the Amount of Debenture Redemption Reserve Transferred to General Reserve) |

| 3,00,000 | 3,00,000 |

Q15. Ashish and Neha were partners in a firm sharing profits and losses in the ratio 4:3. They decided to dissolve the firm on 1st May 2014. From the information given below,

complete Realization A/c, Partner’s Capital Accounts and Bank A/c:

Realisation A/c

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| To sundry assets: -Machinery -Stock -Debtors | 5.60.000 90.000 | By Sundry liabilities: -Creditors -Ashish’s wife’s loan | 40,000 |

| To Bank: | 55,000 | By Bank: | 25,000 |

| -Creditors To Ashish’s Capital A/c; |

| -Machinery -Debtors | 4.80.000 10.000 |

-Ashish’s wife’s loan | 34,000 | By Ashish’s Capital A/c: |

|

To Neha’s Capital A/c; |

| Stock1,28,000 | 1,98,000 |

(Realisation expenses) | 7,000 | -typewriter70,000 | 40,000 |

To profit transferred to: | 7,000 | By Neha’s Capital A/c |

|

Ashish’s capital A/c 4,000 |

| -Debtors |

|

Neha’s capital A/c 3,000 |

|

|

|

| 7,93,000 |

| 7,93,000 |

Partner’s Capital A/c

| Ashish |

|

| Ashish |

| |

Particulars | (Rs.) | Neha (Rs.) | Particulars | (Rs.) | Neha (Rs.) | |

To Realisation A/c |

|

| By |

|

| |

|

|

|

| |||

To Bank A/c |

|

| By |

|

| |

4,00,000 | 4,50,000 |

|

| |||

By | ||||||

|

|

|

|

|

nk A/c

Particulars | Amount (Rs.) | Particulars | Amount (Rs.) | |

To Balance A/c To Realisation A/c |

| By Realisation A/c By Ashish’s Loan A/c By Ashish’s Capital A/c By Neha’s Capital A/c |

| |

4,000 4,00,000 | ||||

4,00,000 | ||||

|

|

|

|

Ans.

Realisation A/c

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| To sundry assets: -Machinery -Stock -Debtors | 5.60.000 90.000 | By Sundry liabilities: -Creditors -Ashish’s wife’s loan |

|

To Bank: |

| By Bank: | 40,000 |

-Creditors | 55,000 | -Machinery | 25,000 |

To Ashish’s Capital A/c; |

| -Debtors | 4,80,000 |

-Ashish’s wife’s loan | 34,000 | By Ashish’s Capital A/c: | 10,000 |

To Neha’s Capital A/c; |

| Stock1,28,000 | 1,98,000 |

(Realisation expenses) | 7,000 | -typewriter70,000 | 40,000 |

To profit transferred to: |

| By Neha’s Capital A/c |

|

Ashish’s capital A/c 4,000 | 7,000 | -Debtors |

|

Neha’s capital A/c 3,000 |

|

|

|

| 7,93,000 |

| 7,93,000 |

Partner’s Capital A/c

Particulars | Ashish (Rs.) | Neha (Rs.) | Particulars | Ashish (Rs.) | Neha (Rs.) |

To Realisation A/c To Balance A/c | 1,98,000 4,00,000 | 40.000 4.50.000 | By Balance b/d By Realisation A/c | 5.60.000 34.000 | 4.80.000 7.000 |

By Realisation A/c | 4,000 | 3,000 | |||

| 5,98,000 | 4,90,000 |

| 5,98,000 | 4,90,000 |

Bank A/c

Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

|

| By Realisation A/c | 40,000 |

To Balance A/c | 4,04,000 | By Ashish’s Loan A/c | 4,000 |

To Realisation A/c | 4,90,000 | By Ashish’s Capital A/c | 4,00,000 |

|

| By Neha’s Capital A/c | 4,50,000 |

| 8,94,000 |

| 8,94,000 |

Q16. A and B are partners in a firm sharing profits and losses in the ratio 3:1. They admit C for a 1/4 share on 31st March 2014 when their Balance Sheet was as follows:

| Liabilities | Amount (Rs.) | Assets | Amount (Rs.) |

| Employees Provident fund |

| Stock |

|

Workmen’s Compensation Fund Investment Fluctuation Reserve Capitals: A B | 17.000 6.000 4,100 54.000 35.000 | Debtors50,000 Less Provision for Doubtful debts2,000 Investments Cash Goodwill | 15.000 48.000 7.000 6,100 40.000 |

| 1,16,100 |

| 1,16,100 |

The following adjustments were agreed upon:

(a) C brings in Rs. 16,000 as goodwill and proportionate capital.

(b) Bad debts amounted to Rs. 3,000.

(c) Market value of investment is Rs. 4,500.

(d) Liability on account of workmen’s compensation reserve amounted to Rs. 2,000.

Prepare Revaluation A/c and Partner’s Capital A/cs.

OR

X, Y and Z are partners in a firm sharing profits in proportion of 1/2, 1/6 and 1/3

respectively. The Balance Sheet as on April 1, 2014 was as follows:

| Amount |

| Amount | |

Liabilities | (Rs.) | Assets | (Rs.) | |

Employees Provident fund | 12,000 | Freehold Premises | 40,000 | |

Sundry Creditors | 18,000 | Machinery | 30,000 | |

General Reserve | Furniture | 12,000 | ||

12,000 | ||||

Capitals | Stock | 22,000 | ||

30,000 | ||||

X | Debtors20,000 |

| ||

30,000 | ||||

Y | Less provision for Doubtful debts1,000 | 19,000 | ||

28,000 | ||||

Z | Cash | 7,000 | ||

| 1,30,000 |

| 1,30,000 |

Z retires from the business and the partners agree that: (a) Machinery is to be depreciated by 10%

(a) Machinery is to be depreciated by 10%

(b) Provision for bad debts is to be increased to Rs. 1,500.

(c) Furniture was taken over by Z for Rs. 14,000.

(d) Goodwill is valued at Rs. 21,000 on Z’s retirement

(e) The continuing partners’ have decided to adjust their capitals in their new profit

sharing ratio after retirement of Z. Surplus or deficit if any, in their capital accounts

will be adjusted through their current accounts.

Prepare Revaluation A/c and Partners’ Capital A/c’s

Ans.

Revaluation A/c

Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

To bad debts | 1,000 | By loss transferred to: A’s Capital A/c B’s Capital A/c | 750 250 |

| 1,000 |

| 1,000 |

Partner’s Capital Accounts

Particulars | A(Rs.) | B(Rs.) | C(Rs.) | Particulars | A(Rs.) | B(Rs.) | C(Rs.) |

To Goodwill A/c To revaluation A/c To Balance c/d | 30,000 750 39,450 | 10,000 250 30,150 | 23,200 23,2000 | By Balance b/d By Cash A/c By Investment fluctuation fund By Workmen’s Compensation fund By premium for good will | 54.000 1,200 3.000 12.000 | 35.000 400 1.000 4,000 | 23,200 |

| 70,200 | 40,400 | 23,200 |

| 70,200 | 40,400 | 23,200 |

OR

Revaluation A/c

Particulars | (Rs.) | Particulars | (Rs.) |

To Machinery To Provision for doubtful debts | 3,000 500 | By Furniture By Loss transferred to; X’s Capital A/c Y’s Capital A/c Z’s Capital A/c | 2,000 750 250 500 |

| 3,500 |

| 3,500 |

Partner’s Capital Accounts

Particulars | X(Rs.) | Y(Rs.) | Z(Rs.) | Particulars | X(Rs.) | Y(Rs.) | Z(Rs.) |

To Furniture To Z’s Capital A/c To revaluation A/c To Z’s Loan A/c To Y’s Current A/c To Balance c/d | 5,250 750 45,000 | 1,750 250 15.00 15.000 | 14,000 500 24,500 | By Balance b/d By General Reserve By X’s Capital A/c By Y’s Capital A/c By X’s Current A/c | 30.000 6.000 15,000 | 30.000 2.000 | 28,00 4,000 5,250 1,750 |

| 51,000 | 32,000 | 39,000 |

| 51,000 | 32,000 | 39,000 |

Q17. Amrit Ltd. Issued 50,000 shares of Rs. 10 each at a premium of Rs. 2 per share payable as Rs.3 on application, Rs.4 on allotment (including premium), Rs.2 on first call

and the remaining on second call. Application were received for 75,000 shares and a pro-rata allotment was made to all the applicants.

All moneys due were received except allotment and first call from Sonu who applied for 1,200 shares. All his shares were forfeited. The forfeited shares were reissued for

Rs. 9,600. Final call was not made. Pass necessary journal entries.

Ans. IN THE BOOK OF AMRIT LTD.

JOURNAL

Date | Particulars | L.F | Debit | Credit |

|

|

| (Rs.) | (Rs.) |

| Bank A/c Dr. To Share Application A/c (Being application money received on 75,000, shares @Rs.3 per share) |

| 2,25,000 | 2,25,000 |

| Share Application A/c Dr. To Share Capital A/c To Bank A/c (Being application money adjusted) |

| 2,00,000 | 1,00,000 1,00,000 |

| Bank A/cDr. To Share Allotment A/c (Being allotment money received) OR |

| 1,23,000 | 1,23,000 |

| Bank A/c Dr. Calls in Arrears A/c Dr. To Share Allotment A/c (Being allotment money received) |

| 1.23.000 2.000 | 1,25,00 |

| 8Share First Call A/cDr. To Share Capital A/c (Being first call due on 50,000 shares) |

| 1,00,000 | 1,00,000 |

| Bank A/cDr. To Share First Call A/c (Being first call money received) OR |

| 98,400 | 98,400 |

| Bank A/c Dr. |

| 98,400 | 1,00,000 |

| Calls in Arrears A/c Dr. To Share First Call A/c (Being first call money received) |

| 1,6000 |

|

| Share Capital A/cDr. Securities Premium Reserve A/c Dr. To Share Forfeiture A/c To Share allotment A/c |

|

|

|

| To Share First Call A/c |

| 5.600 1.600 | 3,600 |

| (Being 800 shares forfeited for nonpayment of |

| 2,000 | |

| allotment money and first call) |

| 1,600 | |

| OR Share Capital A/cDr. Securities Premium Reserve A/c Dr. |

| 5,600 | 3,600 |

| To Share Forfeiture A/c |

| 1,600 | 3,600 |

| To Calls in Arrears A/c (Being 800 shares forfeited for nonpayment of allotment money and first call) |

| 9,600 | 5,600 |

| Bank A/cDr. To Share Capital A/c To Securities Premium Reserve A/c (Being 800 Shares Reissued) |

|

| 4,000 |

| Share Forfeiture A/c Dr. To Capital Reserve A/c (Being Share forfeiture amount transferred to Capital Reserve A/c |

| 3,600 | 3,600 |

PART B: ANALYSIS OF FINANCIAL STATEMENTS

Q18. Cash deposit with the bank with a maturity date after two months belongs to which

of the following while preparing cash flow statement:

(a) Investing activities

(b) Financing activities

(c) Cash and Cash equivalents

(d) Operating activities.

Ans. (c) Cash and Cash equivalents

Q19. Fin serve Ltd is carrying on a Mutual Fund business. It invested Rs. 30,00,000 in shares and Rs. 15,00,000 in debentures of various companies during the year It received Rs. 3,00,000 as dividend and interest. Find out cash flows from investing activities.

Ans.

Cash flows from investing activities – Nil

Q20. (a) Name the sub heads under the head ‘Current Liabilities’ in the Equity and

Liabilities part of the Balance Sheet as per Schedule VI of the companies Act 1956.

(b) State any two objectives of Financial Statements Analysis.

Ans.

(a) CURRENT LIABILITIES

(a) Short term borrowings

(b) Trade payables

(c) Other current liabilities

(d) Short term provisions

(b) Objectives of Financial Statements Analysis (any two)

(i) Helps in assessing the earning capacity or profitability

(ii) Helps in assessing managerial efficiency

(iii) Helps in assessing the long them and short term solvency of the enterprise.

(iv) Helps in inter-firm comparison.

(v) Helps in forecasting and preparing budgets.

(vi) Helps the users in understanding complicated matter in a simplified manner.

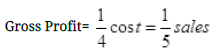

Q21. (a) From the following details, calculate opening inventory: Closing inventory Rs. 60,000; Total Revenue from operations Rs. 5,00,000 (including cash revenue from operations Rs. 1,00,000); Total purchases Rs. 3,00,000 (including credit purchases Rs. 60,000). Goods are sold at a profit of 25% on cost.

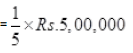

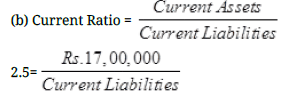

(b) Current assets of a company are Rs. 17,00,000. Its current ratio is 2.5 and liquid ratio

is 0.95.

Ans.

(a) Total revenue from operations = Rs. 5,00,000

= Rs. 1,00,000

Cost of Revenue from operations = Net revenue from operations – Gross Profit

= Rs. 5,00,000 – Rs. 1,00,000

= Rs. 4,00,000

Cost of Revenue from operations = Opening Inventory + Net Purchases- Closing inventory

Rs. 4,00,000 = Opening inventory + Rs. 3,00,000-Rs. 60,000

Opening inventory = Rs. 1,60,000

Quick Assets=Rs. 6,46,000

Inventory= Current Assets – Quick Assets

= Rs. 17,00,000 – Rs. 6,46,000

= Rs. 10,54,000

Ans. Current Liabilities= Rs. 6,80,000

Inventory = Rs. 10,54,000

Q22. Nimani Ltd. is into the business of back office operation. Honesty and hard work are the two pillars on which the business has been built. It has a good turnover and profits.

Encouraged by huge profits, it decided to give the workers bonus equal to two months salary. Following is the Comparative Statement of Profit and Loss of Nimani Ltd. for the years ended 31st March 2013 and 2014.

(a) Calculate Net Profit ratio for the years ending 31 st March 2013 and 2014.

(b) Identify any two values which Nimani Ltd. wants to communicate to the society.

Particulars | Note No. | 2013-13 (Rs.) | 2013-14 (Rs.) | Absolute Change | Percentage change |

Revenue form operations | 20,00,000 | 30,00,000 | 10,00,000 | 50 | |

Less Employee benefit | 8,00,000 | 10,00,000 | 2,00,000 | 25 | |

expenses |

|

|

|

| |

Profit before tax | 12,00,000 | 20,00,000 | 8,00,000 | 66.67 | |

Tax rate 40% | 4,80,000 | 8,00,000 | 3,20,000 | 66.67 | |

Profit after tax | 7,20,000 | 12,00,000 | 4,80,000 | 66.67 | |

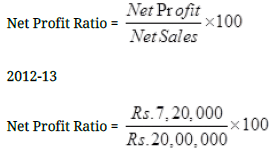

Ans. (a) Calculation of Net Profit Ratio:

= 36%

2013-14

= 40%

Values that Himani Ltd. wants to communicate to the society:

Social responsibility

· Welfare of employees.

Q23. Following are the Balance Sheets of Krishna Ltd. as on 31st March 2013 and 2014:

Particulars | Note No. | 2013-14 (Rs.) | 2012-13 (Rs.) |

1. EQUITY AND LIABILITIES (1) Shareholders’ funds (a) Share capital |

| 14,00,000 | 10,00,000 |

(b) Reserves and surplus | 1 | 5,00,000 | 4,00,000 |

(2) Non-current Liabilities (a) Long term-borrowings | 5,00,000 | 1,40,000 | |

(3) Current liabilities (a) Trade payables |

| 1,00,000 | 60,000 |

(b) Short term Provisions | 2 | 80,000 | 60,000 |

Total | 25,80,000 | 16,60,000 | |

II. ASSETS (1) Non-current assets (a) Fixed assets (i) Tangible Assets |

| 16,00,000 | 9,00,000 |

(ii) Intangible Assets |

| 1,40,000 | 2,00,000 |

(2) Current Assets (a) Inventories | 3 4 | 2,50,000 | 2,00,000 |

(b) Trade receivables | 5,00,000 | 3,00,000 | |

(c) Cash and cash equivalents |

| 90,000 | 60,000 |

Total |

| 25,80,000 | 16,60,000 |

Notes to Accounts:

S.No. | Particulars | 31.3.2014 (Rs.) | 31.3.2014 (Rs.) |

| Reserve and Surplus: |

|

|

1. | Surplus (i.e. balance in Statement of Profit and |

|

|

| Loss) | 5,00,000 | 4,00,000 |

| General Reserve |

|

|

2. | Short term Provisions |

|

|

| Provision for tax | 80,000 | 60,000 |

3. | Tangible assets |

|

|

| Machinery | 17,60,000 | 10,00,000 |

| Less Accumulated depreciation | (1,60,000) | (1,00,000) |

4. | Intangible Assets |

|

|

| Goodwill | 1,40,000 | 2,00,000 |

Prepare a Cash flow statement after taking into account the following adjustment

(i) Tax paid during the year amounted to Rs. 70,000.

Ans. In the books of Krishna Ltd.

Cash Flow Statement

For the year ended 31st March’14

Particulars | Rs. | Rs. |

Cash flow from operating activities |

|

|

Net Profit Before Tax (Working Note 1) | 1,90,00 |

|

Add non-cash operating/non cash items: | 60,000 |

|

Depreciation on machinery | 60,000 |

|

Goodwill Written off | 3,10,000 |

|

Operating Profit before working capital changes | 40,000 |

|

Add increase in Trade Payables | (50,000) |

|

Less Increase in Inventories | (2,00,000) |

|

Increase in Trade Receivables | 1,00,000 |

|

Cash generated from operation | (70,000) |

|

Less : Increase tax paid |

|

|

Cash flow from operating activities |

| 30,0000 |

|

|

|

cash flow from investing activities Purchase of Fixed Assets | (7,60,000) |

|

Cash used in investing activities |

| (7,60,000) |

cash flow from financing Activities Issue of share Long term borrowings | 4,00,000 3,60,000 |

|

cash flow from Financing Activities |

| 7,60,000 |

Net Increase in Cash & Cash equivalent Add opening balance of cash and cash Equivalent Closing balance of Cash & Cash Equivalent | 30.000 60.000 | |

90,000 | ||

Working Note I:

Calculation of Net Profit Before Tax

Surplus i.e. Balance in Statement of Profit and Loss1,00,000

Add provision for tax 90,000

1,90,000

Provision for Tax A/c

Particulars | Amount (Rs.) | Particulars | Amount (Rs.) |

To cash (tax paid) To balance c/d | 70.000 80.000 | By balance b/d By provision made during the year | 60,000 90,000 |

| 1,50,000 |

| 1,50,000 |

|

130 docs|5 tests

|

FAQs on CBSE Accounts Sample Paper - 2 (2018-19) - Sample Papers for Class 12 Commerce

| 1. What is the importance of studying accounts in CBSE Class 12? |  |

| 2. How can I improve my performance in CBSE Class 12 Accounts exam? | |

| 3. What are the key topics that I should focus on for the CBSE Class 12 Accounts exam? | |

| 4. Are there any recommended reference books for CBSE Class 12 Accounts preparation? | |

| 5. How can I score well in the practical component of the CBSE Class 12 Accounts exam? | |

MCQs

,practice quizzes

,CBSE Accounts Sample Paper - 2 (2018-19) | Sample Papers for Class 12 Commerce

,Sample Paper

,Semester Notes

,CBSE Accounts Sample Paper - 2 (2018-19) | Sample Papers for Class 12 Commerce

,ppt

,shortcuts and tricks

,Summary

,video lectures

,Important questions

,mock tests for examination

,Extra Questions

,Previous Year Questions with Solutions

,Objective type Questions

,Free

,CBSE Accounts Sample Paper - 2 (2018-19) | Sample Papers for Class 12 Commerce

,Viva Questions

,study material

,past year papers

,Exam

;

CBSE Accounts Sample Paper - 2 (2018-19) Free PDF Download

Importance of CBSE Accounts Sample Paper - 2 (2018-19)

CBSE Accounts Sample Paper - 2 (2018-19) Notes

CBSE Accounts Sample Paper - 2 (2018-19) Commerce Questions

Study CBSE Accounts Sample Paper - 2 (2018-19) on the App

|

© EduRev

|

Education Revolution

|

|