Financial Statements of a Company Chapter Notes | Accountancy Class 12 - Commerce PDF Download

| Table of contents |

|

| Introduction |

|

| Meaning of Financial Statements |

|

| Nature of Financial Statements |

|

| Objectives of Financial Statements |

|

| Types of Financial Statements |

|

Introduction

- Once we grasp how a company secures its capital, the next step is to delve into the nature, objectives, and types of financial statements that the company is required to prepare. This includes understanding their contents, format, uses, and limitations.

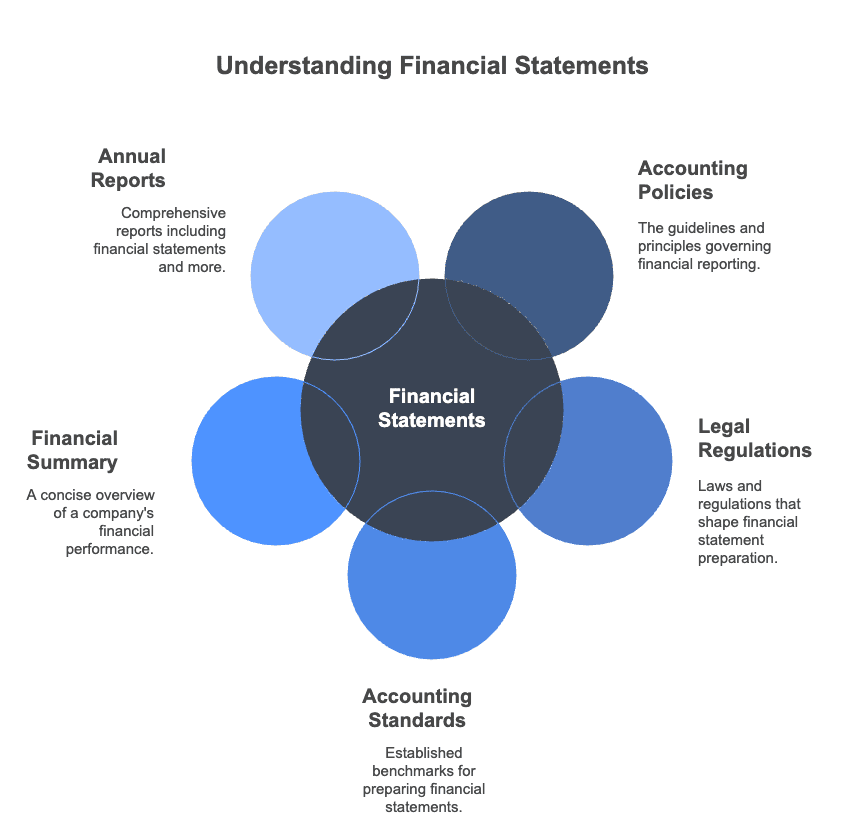

- Financial statements represent the final output of the accounting process. Their preparation is guided by accounting policies, accounting standards outlined in the Companies Act, and fundamental accounting concepts and principles. Additionally, these statements must adhere to legal regulations governing business operations.

- These statements summarise monetary information but do not include qualitative aspects such as industrial relations, climate, labour relations, or quality of work. Financial statements serve as the basic formal annual reports through which corporate management shares financial details with owners and various external parties, including investors, tax authorities, the government, and employees. They are interim reports: the Statement of Profit and Loss shows the profit or loss for a specific time period.

- Furthermore, financial statements are a vital part of the company’s annual report, alongside the directors' report, auditors' report, corporate governance report, and management discussion and analysis.

Meaning of Financial Statements

- Financial statements are the final outputs of the accounting process. They show the financial results of a specific period and the financial position at a certain date. These statements are created by summarising accounting data and provide essential information for assessing the profitability and financial status of a company. Their main goal is to offer the information necessary for decision-making by both management and external stakeholders interested in the company's affairs.

- These statements consist of the balance sheet (which shows the position at the end of the accounting period), the statement of profit and loss of a company, and the cash flow statement.

Limitations of Financial Statements

- Financial statements have limitations; they provide only aggregate information to meet general user needs.

- They are technical documents that require some accounting knowledge to understand.

- They reflect historical information but not current situations, which are vital for decision-making.

- While they indicate organisational performance in quantitative terms, they do not reflect qualitative aspects such as employee relations, work quality, or employee satisfaction.

- Financial statements are not always complete or entirely accurate, as income and expense flows are separated using subjective judgment alongside accepted concepts.

- Therefore, these statements require careful analysis before being used for decision-making.

Nature of Financial Statements

- Financial statements are the end products of the accounting process, made from recorded facts in monetary terms for a set period.

- These statements show the financial position at a specific date and the financial results over a period.

- The American Institute of Certified Public Accountants defines financial statements as tools for regularly reviewing management's progress, highlighting the status of investments and outcomes achieved.

- They combine recorded facts, accounting principles, procedures, and the legal environment affecting business operations.

- Corporations prepare and publish financial statements for the benefit of various stakeholders, acting as formal annual reports to communicate financial information to owners and other external parties.

- Financial statements do not convey qualitative details such as industrial relations, labour relations, or work quality.

- They are a key part of the company's annual report, alongside the directors' report, auditors' report, corporate governance report, and management discussion and analysis.

- The main aim of financial statements is to help users make informed decisions.

Recorded Facts:

- Financial statements depend on recorded facts represented as cost data from accounting records.

- Transactions are recorded at original or historical cost.

- Figures for accounts like cash, trade receivables, and fixed assets are sourced from accounting records.

- Assets bought at different times and prices are listed at their historical costs.

- As these figures are not based on current market prices, financial statements might not represent the actual current financial status of the business.

Accounting Conventions:

- Certain accounting conventions are adhered to when preparing financial statements.

- Inventory is valued at the lower of cost or market value.

- Assets are recorded at cost minus depreciation on the balance sheet.

- The materiality convention applies to minor items like stationery, treating them as expenses when purchased.

- Following accounting conventions makes financial statements comparable, straightforward, and realistic.

Postulates:

- Financial statements are based on key assumptions known as postulates.

- The going concern postulate assumes the enterprise will continue to operate in the foreseeable future, leading to a historical cost basis for asset valuation.

- The money measurement postulate assumes the value of money remains stable over time, despite changes in purchasing power.

- The realisation postulate recognises revenue in the year of sale, regardless of when the payment is received.

Personal Judgments:

- Financial statements frequently involve personal opinions, estimates, and judgments.

- Depreciation is determined based on the estimated useful life of fixed assets.

- Provisions for doubtful debts are established based on estimates and personal judgments.

- Valuing inventory involves choosing between cost and market value, requiring personal judgment.

- Personal opinions and estimates aim to prevent the overstatement of assets, liabilities, income, and expenses.

Objectives of Financial Statements

Financial statements serve as essential sources of information for shareholders and external parties to comprehend the profitability and financial position of a business. They offer insights into the business's performance over a specific period concerning its assets and liabilities, facilitating informed decision-making. The primary aim of financial statements is to aid users in their decision-making processes. The specific objectives include:

- Information on Economic Resources and Obligations: Financial statements are designed to provide adequate, reliable, and periodic information about a business's economic resources and obligations. This information is crucial for investors and external parties who may have limited access to such data.

- Earning Capacity Assessment: Financial statements aim to offer useful financial information that can be employed to predict, compare, and evaluate a business's earning capacity.

- Cash Flow Information: These statements are intended to provide information that is useful to investors and creditors for predicting, comparing, and evaluating potential cash flows in terms of amount, timing, and associated uncertainties.

- Management Effectiveness Evaluation: Financial statements supply information that is useful for assessing management's ability to utilise a business's resources effectively.

- Societal Impact Reporting: Financial statements report on a business organisation's activities that impact society, focusing on aspects that are measurable and significant within its social environment.

- Disclosure of Accounting Policies: Financial statements include disclosures about significant accounting policies and concepts followed during the accounting process, as well as any changes made during the year. This helps users understand the statements more clearly.

Types of Financial Statements

Financial statements commonly include two main documents: the balance sheet and the statement of profit and loss. These are essential for both external reporting and internal management purposes, such as planning, decision-making, and control.

In addition to the balance sheet and profit and loss statement, there is a need to understand the movement of funds and changes in the financial position of the company. For this reason, a cash flow statement is also prepared.

Every company registered under The Companies Act 2013 is required to prepare its balance sheet, statement of profit and loss, and accompanying notes per the revised Schedule III of the Act. This ensures alignment with accounting standards and compliance with new reforms.

Balance Sheet as of 31st March, 20.....

Important Features of Presentation

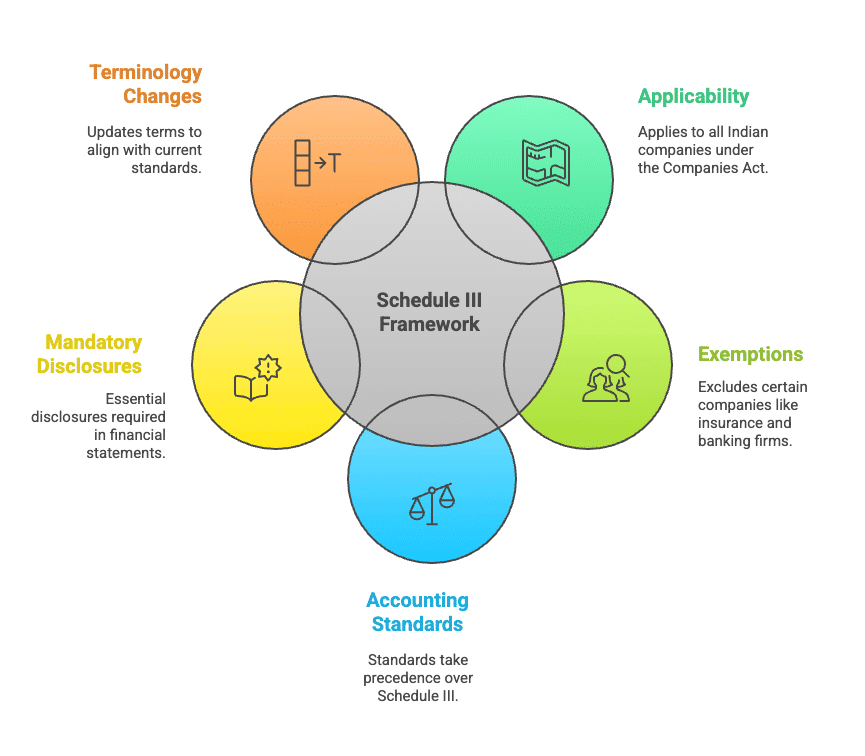

- Applicability: Schedule III applies to all Indian companies preparing financial statements under the Companies Act, 2013.

- Exemptions: It does not apply to insurance or banking companies, or to companies with specific balance sheet or income statement formats required by other Acts.

- Accounting Standards: Accounting standards take precedence over Schedule III.

- Mandatory Disclosures: Disclosures on the financial statements face or in the notes are essential and mandatory.

- Terminology: Terms in Schedule III have the meanings defined by applicable accounting standards.

- Detail Balance: A balance must be maintained between excessive details and the provision of important information.

- Current/Non-Current Bifurcation: Bifurcation of assets and liabilities into current and non-current categories is required.

- Rounding Off: Rounding off requirements is mandatory.

- Presentation Format: A vertical format for presenting financial statements is prescribed.

- Profit and Loss Statement: Debit balances in the statement of profit and loss should be disclosed as negative figures under "Surplus."

- Share Application Money: Mention of share application money pending allotment is mandatory.

- Terminology Changes: ‘Sundry Debtors’ and ‘Sundry Creditors’ are replaced with ‘Trade Receivables’ and ‘Trade Payables’.

Shareholders Fund:

The shareholders’ funds are sub-classified on the face of the balance sheet.

- Share Capital

- Reserves and Surplus

- Money received against Share Warrants

Share Capital:

Disclosures related to share capital should be included in the notes to accounts. The following additions or modifications are important:

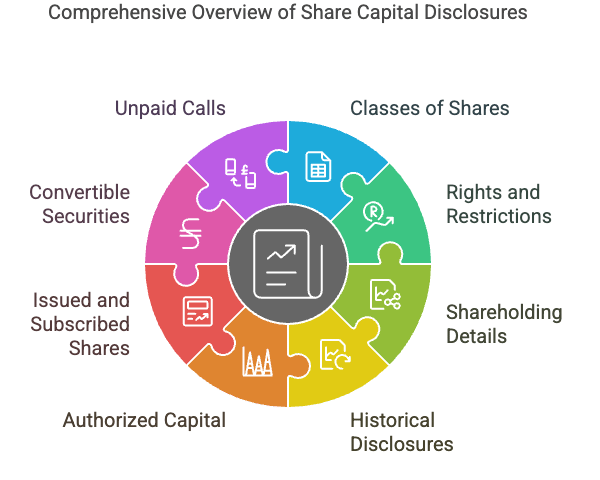

- For each class of shares, it is necessary to recognise the number of shares outstanding at the beginning and end of the reporting period.

- Details about the rights, preferences, and restrictions attached to each class of shares must be provided, including any limitations on the distribution of dividends and repayment of capital.

- To clarify the identity of the ultimate owners of the company, the following disclosures are required:

- Disclosure of shares held by the holding company or ultimate holding company: Include shares held by subsidiaries or associates of the holding company or ultimate holding company in aggregate for each class of shares.

- Disclosure of shares held by major shareholders: Specify the number of shares held by each shareholder owning more than 5% of the shares.

- Disclosure for the past 5 years: Provide information on the following:

- Aggregate number and class of shares allotted as fully paid up without payment in cash.

- Aggregate number and class of shares allotted as fully paid up by way of bonus shares.

- Aggregate number and class of shares bought back.

It is important to note that information about shareholders' funds is presented on the face of the financial statements only for broad and significant items, while details are provided in the Notes to Accounts.

- For each class of share capital, the following information should be disclosed:

- Authorised share capital: Number and amount of shares authorised.

- Issued and subscribed shares: Number of shares issued, subscribed, fully paid, and subscribed but not fully paid.

- Par value: Par value per share.

- Reconciliation: Reconciliation of the number of shares outstanding at the beginning and end of the accounting period.

- Rights and Restrictions: Rights, preferences, and restrictions attaching to each class of shares, including restrictions on dividend distribution and capital repayment.

- Shareholding by holding company: Aggregate number of shares held by the holding company, ultimate holding company, and subsidiaries or associates of the holding company or ultimate holding company for each class.

- Shares reserved for issue: Shares reserved for issue under options and contracts/commitments for the sale of shares/disinvestment, including terms and amounts.

- Past 5 years disclosures: For the past 5 years, disclose:

- Shares are reserved under contracts/commitments.

- Number and class of shares bought back.

- Number and class of shares allotted for consideration other than cash and bonus shares.

- Convertible securities: Terms of any securities convertible into equity/preference shares issued, along with the earliest date of conversion in descending order.

- Calls unpaid: Aggregate amount of calls unpaid.

- Forfeited shares: The amount originally paid up on forfeited shares.

Reserve and Surplus:

- Capital Reserve

- Capital Redemption Reserve

- Securities Premium Reserve

- Debenture Redemption Reserve

- Revaluation Reserve

- Share Options Outstanding Account

- Other Reserves(specifying nature and purpose)

- Surplus: balance in the statement of profit and loss, disclosing allocations and appropriations such as dividends, bonus shares, transfer to/from reserve, etc.

Significant additions/modifications regarding disclosure of reserve and surplus are as follows:

- A reserve that is represented by earmarked investments is called a "Fund."

- The 'Debit' balance of the profit and loss statement will be shown as a negative figure under the 'Surplus' section.

- After adjusting for any negative Surplus, the balance of "Reserve and Surplus" should still be displayed as "Reserve and Surplus", even if it results in a 'negative' figure.

- The share options outstanding account is now recognised as a separate item under 'Reserve and Surplus.'

- According to ICAI’s Guidance Note on accounting for employee share-based payments, a credit balance in the 'Stock Option Outstanding Account' must be shown in the balance sheet between share capital and reserves and surplus as part of shareholders' funds.

- Mandatory disclosure is required for share application money that is pending allotment.

Money Received Against Share Warrants:

- Money received by a company against share warrants is the amount that will be converted into shares at a specified date and rate.

- The company issues share warrants as an instrument against the money received.

- This amount is disclosed as a separate line item under "shareholder's fund."

Example: Dinkar Ltd. has an authorised capital of Rs. 50,00,000 divided into equity shares of Rs. 100 each. The company invited applications for 40,000 shares, applications for 36,000 shares were received. All calls were made and duly received except for 500 shares on which the final call of Rs. 20 was not received. The company forfeited 200 shares on which final call was not received. Show how share capital will appear in the balance sheet of the company. Also prepare ‘Notes to Accounts’ for the same.

Ans:

Current and Non-current Classification:

- In a classified balance sheet, assets and liabilities are divided into current and non-current categories.

- Current assets and current liabilities have specific criteria for classification, while non-current items are residual.

Current/Non-current Distinction:

- An item is classified as current if it meets any of the following criteria:

- Involved in the entity’s operating cycle.

- Expected to be realized or settled within twelve months.

- Held primarily for trading.

- Cash and cash equivalents.

- The entity does not have unconditional rights to defer settlement of the liability for at least 12 months after the reporting period.

- Items that do not meet these criteria are classified as non-current.

Important Points:

- Preliminary expenses must be completely written off in the year incurred. These should first be deducted from securities premium, with any remaining balance written off from the profit and loss statement.

- Borrowing costs, such as the discount on debentures, should be written off in the same year they are issued.

- Mandatory disclosure is required for share application money pending allotment.

- 'Sundry Debtors' and 'Sundry Creditors' have been replaced with 'Trade Receivables' and 'Trade Payables.'

Borrowings:

Total borrowings are categorised into long-term borrowings, short-term borrowings and current maturities to long-term debt.

(i) Loans that are repayable in more than twelve months/operating cycle are classified as long-term borrowings on the face of the balance sheet.

(ii) Loans repayable on demand or whose original tenure is not more than twelve months/operating cycle are classified as short-term borrowings on the face of the balance sheet.

(iii) Current maturities to long-term loans include the amount repayable within twelve months/operating cycle under other current liabilities with Note to Account.

Deferred tax assets/liabilities are always non-current. This is in accordance with Schedule III of the Companies Act.

- Trade payables are now referred to as Trade payables and are divided into current and non-current categories.

- Trade payables that will be settled after 12 months from the balance sheet date or beyond the operating cycle are classified as “other long-term liabilities”, with a Note to Accounts.

- This includes the purchase of goods and services during regular business activities.

- The balance of trade payables is shown as current liabilities on the balance sheet.

Proposed Dividend:

- The proposed dividend is suggested by the Board of Directors and approved by the shareholders during their Annual General Meeting.

- The Board puts forward the dividend after the annual accounts for the year are prepared.

- The Annual General Meeting of shareholders occurs afterwards, in the following financial year.

- Shareholders can reduce the proposed dividend amount but cannot increase it.

- As the declaration of the proposed (final) dividend depends on shareholder approval, it is shown as a contingent liability.

- AS-4, Contingencies and Events Occurring after the Balance Sheet Date, states that the proposed dividend will be included in the Notes to Accounts.

- Once the proposed dividend is declared by shareholders, it becomes a liability for the company and is recorded in the accounts.

- This means the proposed dividend from the previous year will be declared by shareholders this year, and this declared dividend will be recorded in the current year.

- The proposed dividend for this year will apply to the next financial year.

- In summary, a proposed dividend from the previous year will be recorded in the current year once it is declared by the shareholders at the annual general meeting.

Provisions:

- If a provision is likely to be settled within 12 months from the balance sheet date or within the operating cycle, it is classified as a short-term provision and listed under current liabilities on the balance sheet.

- Provisions that do not meet these conditions are classified as long-term provisions and listed under non-current liabilities.

Fixed Assets:

- There is no change in the treatment of fixed assets. Both tangible and intangible assets are considered non-current.

- Even if the useful life of an asset is less than 12 months, it still falls under non-current assets.

Investments:

- Investments are categorised as current and non-current.

- Investments expected to be realised within 12 months are considered current investments under current assets.

- Investments that are not expected to be realised within 12 months are classified as non-current investments under non-current assets.

- Both types of investments are displayed on the balance sheet.

Inventories:

- All inventories are always treated as current assets.

Trade Receivables:

- Trade receivables expected to be realised beyond 12 months from the reporting date or beyond the operating cycle from the date of recognition are classified as “Other non-current assets” under non-current assets with a note to accounts.

- Trade receivables expected to be realised within 12 months are classified as current assets and shown on the face of the balance sheet.

Cash and Cash Equivalents:

- Cash and cash equivalents are always classified as current assets.

- Amounts qualifying as cash and cash equivalents as per AS-3 are shown here.

- Disclosure of cash and cash equivalents is done in accordance with AS-3, taking precedence over Schedule III.

Example: Show the following items in the balance sheet of Sunfill Ltd. as at March 31, 2017:

Ans:

Form and content of Statement of Profit and Loss

Statement of Profit and Loss for the year ended ______________

The items of the statement of profit and loss are discussed as follows:

1. Revenue from operations: This includes:

- Sale of products

- Sale of services

- Other operating revenues

- For finance companies, revenue from operations also includes income from interest, dividends, and other financial services.

2. Other income:

- Interest income (in the case of a company other than a finance company),

- Dividend income,

- Net gain/loss on sale of investments,

- Other non-operating income (net of expenses directly attributable to such income).

3. Expense:

Example: From the following particulars, prepare Statement of profit and loss for the yearending March 2017, showing a profit before tax as per schedule III of the Companies Act, 2013.

Solution:

Uses and Importance of Financial Statements

Financial statements are crucial for various users such as management, investors, shareholders, creditors, government, bankers, employees, and the public. They provide essential information about the company's performance, helping these parties make informed economic decisions. Financial statements are a key part of the company's annual report, alongside the directors' report, auditors' report, corporate governance report, and management discussion and analysis.

- Report on stewardship function: Financial statements show how well management is performing to the shareholders. They highlight any gaps between what management achieves and what shareholders expect.

- Basis for fiscal policies: The government's fiscal and taxation policies are influenced by the financial performance of companies. Financial statements provide crucial information for shaping industrial, taxation, and economic policies.

- Basis for granting of credit: Banks and financial institutions rely on financial statements to decide whether to grant credit to corporate undertakings. These statements are essential for assessing the financial health of the borrowing entity.

- Basis for prospective investors: Both short-term and long-term investors use financial statements to evaluate the security, liquidity, and profitability of their investments. These statements help assess the company's solvency and potential returns.

- Guide to the value of the investment already made: Shareholders use financial statements to gauge the status, safety, and returns on their investments. This information aids in deciding whether to continue or discontinue their investment in the company.

- Aids trade associations in helping their members: Trade associations analyze financial statements to support and protect their members. They may establish standard ratios and develop uniform accounting systems based on this analysis.

- Helps stock exchanges: Financial statements enable stock exchanges to assess the transparency of companies' financial reporting. This information helps protect investors' interests and assists stockbrokers in evaluating companies' financial positions for pricing decisions.

Limitations of Financial Statements

- Even though great care is taken when preparing financial statements to provide detailed information to users, they have the following limitations:

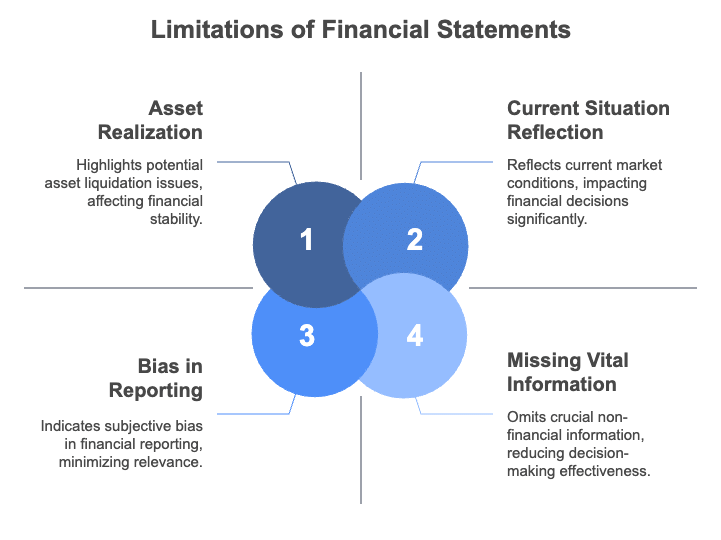

- Do not reflect current situation: Financial statements are based on historical cost. As the purchasing power of money changes, the values of assets and liabilities in these statements do not represent the current market situation.

- Assets may not realise: Accounting relies on certain conventions. Some assets may not achieve their stated values if the company is forced to liquidate. The assets shown on the balance sheet only represent unexpired or unamortised costs.

- Bias: Financial statements result from recorded facts, accounting concepts, conventions, and personal judgments made by accountants in various situations. Thus, bias may be present, and the financial position shown may not be realistic.

- Aggregate Information: Financial statements present aggregate information rather than detailed specifics, which may limit their usefulness in decision-making.

- Vital information missing: The balance sheet does not disclose information about market losses or the termination of agreements, which are crucial for the enterprise.

- No qualitative information: Financial statements include only monetary data, lacking qualitative insights such as industrial relations, climate, labour relations, and work quality.

- Interim reports: The Statement of Profit and Loss shows profit or loss for a specific period but does not indicate earning capacity over time. Similarly, the financial position in the balance sheet is accurate only at that moment, with no indication of future changes.

|

42 videos|199 docs|43 tests

|

FAQs on Financial Statements of a Company Chapter Notes - Accountancy Class 12 - Commerce

| 1. What are the primary financial statements of a company? |  |

| 2. What is the purpose of financial statements? | |

| 3. How do financial statements reflect the financial position of a company? | |

| 4. What is the importance of the Income Statement in financial analysis? | |

| 5. What are the main objectives of preparing financial statements? | |

ppt

,Important questions

,Sample Paper

,Extra Questions

,Summary

,mock tests for examination

,shortcuts and tricks

,Previous Year Questions with Solutions

,Viva Questions

,Financial Statements of a Company Chapter Notes | Accountancy Class 12 - Commerce

,study material

,MCQs

,past year papers

,practice quizzes

,Exam

,Free

,Objective type Questions

,video lectures

,Financial Statements of a Company Chapter Notes | Accountancy Class 12 - Commerce

,Semester Notes

,Financial Statements of a Company Chapter Notes | Accountancy Class 12 - Commerce

;

Chapter Notes: Financial Statements of a Company Free PDF Download

Importance of Chapter Notes: Financial Statements of a Company

Chapter Notes: Financial Statements of a Company

Chapter Notes: Financial Statements of a Company Commerce Questions

Study Chapter Notes: Financial Statements of a Company on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!