Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner | Crash Course of Accountancy - Class 12 - Commerce PDF Download

Death Test

Time – 50 mins

M.M.- 20

Q1. On 31st March 2015 the Balance Sheet of Punit, Rahul and Seema was as follows

Liabilities | Assets | ||

Capitals: | 1,40,000 | Buildings | 40,000 |

Punit 60,000 | Machinery | 60,000 | |

Rahul 50,000 | Patents | 12,000 | |

Seema 30,000 | Stock | 20,000 | |

Reserves | 20,000 | Cash | 42,000 |

Creditors | 14,000 |

They were sharing Profit and loss in the ratio 5:3:2. Seema died on October 1, 2015. It was agreed between her executors and the remaining partners that:

i. Goodwill be valued at 2 years’ purchase of the average profits of the previous five years, which were: 2010-11: 30,000; 2011-12: 26,000; 2012-13: 24,000; 2013-14: 30,000 and 2014-15: 40,000.

ii. Patents be valued at 16,000; Machinery at 56,000; Buildings at 60,000.

iii. Profit for the year 2015-16 be taken as having been accrued at the same rate as that in the previous year.

iv. Interest on capital be provided at 10% p. a.

v. A sum of 15,500 was paid to her executors immediately.

Prepare Revaluation Account, Seema’s Capital Account and Seema’s executors Account. (6 mark)

Q2. A, B and C are partners in a firm sharing profits in the ratio of 5 : 3 : 2 respectively. Their Balance Sheet as on 31st December, 2012 was as follows :

Liabilities | Amount | Assets | Amount |

Capitals : | Patents | 1,10,000 | |

A | 3,00,000 | P & L | 2,00,000 |

B | 2,50,000 | Machinery | 3,00,000 |

C | 1,50,000 | Stock | 1,00,000 |

Creditors | 1,10,000 | Debtors | 80,000 |

Reserves | 60,000 | Cash | 80,000 |

8,70,000 | 8,70,000 |

A died on 1st October, 2013, due to illness. It was agreed between the firm and A‖s executors that the amount due to A will be used for construction of a Charitable Hospital in a village. As per the agreement :

(i) Goodwill was valued at 2 years purchase of average profits of last 4 years, which were : 2009 – Rs. 1,00,000; 2010 – Rs. 1,60,000; 2011 – Rs. 1,80,000

(ii) Patents were revalued at Rs. 90,000; Machinery at Rs. 2,80,000 and Building at Rs. 2,50,000.

(iii) A‖s share of profit till the date of his death will be calculated on the basis of the profit of the year 2012.

(iv) Interest on capital will be provided at 10% p.a.

(v) Amount due to A’s executors will be transferred to Charity account.

Prepare a capital account to be presented to his executor. (6 mark)

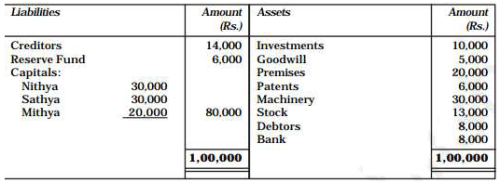

Q3. Nithya, Sathya and Mithya were partners sharing profits and losses in the ratio of 5:3:2. Their Balance Sheet as on December 31, 2002 was as follows :

Balance Sheet at December 31, 2002

Mithya dies on May 1, 2002. The agreement between the executors of Mithya and the partners stated that :

(a) Goodwill of the firm be valued at 2 ½ times the average profits of last four years. The profits of four years were : in 1998, Rs.13,000; in 1999, Rs.12,000; in 2000, Rs.16,000; and in 2001, Rs.15,000.

(b) The patents are to be valued at Rs.8,000, Machinery at Rs.25,000 and Premises at Rs.25,000.

(c) The share of profit of Mithya should be calculated on the basis of the profit of 2002.

(d) Provide interest @ 12% p.a. on capital. (6 mark)

|

79 docs|43 tests

|

FAQs on Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner - Crash Course of Accountancy - Class 12 - Commerce

| 1. What is retirement of a partner? |  |

| 2. How is retirement of a partner different from the death of a partner? | |

| 3. What are the reasons for the retirement of a partner? | |

| 4. How is the retirement of a partner accounted for in the partnership firm? | |

| 5. What are the implications of the retirement of a partner on the partnership firm? | |

past year papers

,Exam

,mock tests for examination

,study material

,Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner | Crash Course of Accountancy - Class 12 - Commerce

,Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner | Crash Course of Accountancy - Class 12 - Commerce

,video lectures

,Free

,practice quizzes

,Sample Paper

,Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner | Crash Course of Accountancy - Class 12 - Commerce

,shortcuts and tricks

,Viva Questions

,Important questions

,Extra Questions

,Objective type Questions

,Previous Year Questions with Solutions

,Summary

,MCQs

,Semester Notes

,ppt

;

Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner Free PDF Download

Importance of Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner

Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner Notes

Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner Commerce

Study Sample Questions (Part - 2) - Retirement of a Partner Death of a Partner on the App

|

© EduRev

|

Education Revolution

|

|