Class 12 Economics Solved Paper (2013 Delhi Set-III) | Additional Study Material for Commerce PDF Download

Ques 1: Give an example each of fixed cost and variable cost.

Ans: Example of Fixed Cost - Cost of Machinery Example of Variable Cost - Labour Cost (Wages and salaries)

Ques 2: The price elasticity of supply of a good is 0.8. Its price rises by 50 percent. Calculate the percentage increase in its supply.

Ans:

es = 0.8

ΔP = 50%

ΔQ=?

or, ΔQ= 40%

Percentage Change in Quantity Supplied is 40%.

Ques 3:

| Complete the following table: | ||

| Units of Labour | Average Product (Units) | Marginal Product (Units) |

| 1 | 16 | ..... |

| 2 | 20 | ..... |

| 3 | ..... | 20 |

| 4 | 18 | ..... |

| 5 | ..... | 8 |

| 6 | 14 | ..... |

Ans:

| Units of Labour | Average Product AP = TP/L | Marginal Product (Units) MPn = TPn - TPn-1 | Total Product TP=AP × L or, TPn = TPn-1+MPn |

| 1 | 16 | - | 16(1 ×16) |

| 2 | 20 | 24(40−16) | 40(2× 20) |

| 3 | 20(60−3) | 20 | 60(40+20) |

| 4 | 18 | 12(72−60) | 72(4 ×18) |

| 5 | 16(80−5) | 8 | 80(72+8) |

| 6 | 14 | 4(84−80) | 84(6 ×14) |

Ques 4: Explain 'freedom of entry and exit to firms in industry' features of monopolistic competition.

Ans: Freedom of entry and exit to firms in. a monopolistic industry implies that there exists no restriction tor the new entrants and existing firms to quit the industry. The new firms are attracted into the industry whenever price exceeds the minimum of short run average cost (SAC) In short run and whenever price exceeds the minimum of long run average cost (LAC) in the long run. Due to the free entry of the new firms in the industry, the quantity produce increases, which results in the rise of the supply of the output and finally, this pushes the equilibrium price down. Thus, the equilibrium price continues to fall, until it become equals to the minimum of average cost curve, where, all the firms earns normal profit. At this point, no new firm has any incentive to enter the industry.

Similarly, on the other hand, the existing firms leave the industry whenever the price falls short of the minimum of short run average cost curve (SAC) in the short run or whenever price falls short of the minimum of long run average cost (LAC) in the long run. This is because under such circumstances, the existing firms each losses and consequently wishes to quit. Now, as there are no restrictions imposed on the exit of the firms, so firm quits the industry. This leads to the fall in the supply of the commodity. Hence, the price start rising and reaches the point at LAC where a firm earns only normal profit.

Thus, it is due to freedom of the entry and exit to firms that price remains equal to the minimum of average cost implying the normal profit only.

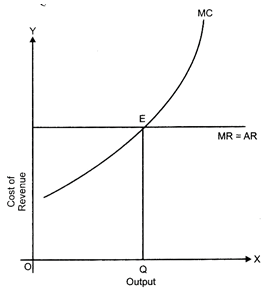

Ques 5: Give the meaning of producer's equilibrium. A produces that quantity of his product at which marginal cost and marginal revenue are equal. Is he earning maximum profits? Give reasons for your answer.

Ans: At a point where, MC = MR, the producers equilibrium is established. Yes, the producer earns maximum profit on this point. Because any deviation from this position will either reduce the profit of a firm or increase the losses.

MC refers to the additional cost that takes place by producing an additional unit of output. MR refers to the additional revenue that takes place by selling an additional unit.

When marginal cost is less than MR available from the sale of a product, the firm will go on increasing its output. When MC and MR are equal, the firm reaches on its equilibrium. After that point if a firm increases its output, MC will be greater than MR resulting in decline in profit. This diagram is related to the perfect competition, where the equilibrium output is OQ, where MR = MC.

Ques 6:

| Calculate 'sales' from the following data: | |

| (Rs in lakhs) | |

| Intermediate costs | 700 |

| Consumption of fixed capital | 80 |

| Change in stock | (-) 50 |

| Subsidy | 60 |

| Net value added at factor cost | 1300 |

| Exports | 50 |

Ans:

NVAFC = Rs 1,300

GDPMP = NVAFC - Subsidies + Consumption of fixed capital =1,300−60+80=Rs. 1,320

Also, we know that:

GDPMP = Sales + Change in stock - Intermediate Cost Sales = GDPMP - Change in stock +

intermediate Cost

=1,320−(−50)+700

i.e. Sales = Rs 2,070 Lakhs.

Ques 7: C = 50 + 0.5Y is the consumption function where C is consumption expenditure and Y is National Income and investment expenditure is 2,000 in an economy.

Calculate Equilibrium level of (National Income) Consumption expenditure of equilibrium level of national income.

Ans: Y = National Income, Consumption Function, C=50+0.5Investment, I= 2,000

(i) V=CIor Y= 50+0.5Y+2,000

or 0.5V=50+2,000=2,050

∴ Equilibrium level of National Income = 4,100

(ii) Given, C=50+0.5V

C=50+0.5(4,100)

0=50+2,050=2,100

∴ Consumption expenditure at equilibrium level = 2,100

Ques 8:

| Complete the following table: | |||

| Consumption expenditure (Rs) | Saving (Rs) | Income (Rs) | Marginal Propensity to consume |

| 100 | 50 | 150 | ..... |

| 175 | 75 | .... | ..... |

| 250 | 100 | .... | ..... |

| 325 | 125 | .... | .... |

Ans:

| Consumption expenditure (Rs) | Saving (Rs) | Income (Rs) | Marginal Propensity to consume |

| 100 | 50 | 150 | ?.. |

| 175 | 75 | 250 | 75/100=0.75 |

| 250 | 100 | 350 | 75/100=0.75 |

| 325 | 125 | 450 | 75/100=0.75 |

|

4 videos|168 docs

|

Free

,Summary

,past year papers

,MCQs

,Sample Paper

,Exam

,Class 12 Economics Solved Paper (2013 Delhi Set-III) | Additional Study Material for Commerce

,practice quizzes

,Class 12 Economics Solved Paper (2013 Delhi Set-III) | Additional Study Material for Commerce

,Viva Questions

,Previous Year Questions with Solutions

,Extra Questions

,study material

,shortcuts and tricks

,Class 12 Economics Solved Paper (2013 Delhi Set-III) | Additional Study Material for Commerce

,Important questions

,mock tests for examination

,Objective type Questions

,ppt

,Semester Notes

,video lectures

;

Class 12 Economics Solved Paper (2013 Delhi Set-III) Free PDF Download

Importance of Class 12 Economics Solved Paper (2013 Delhi Set-III)

Class 12 Economics Solved Paper (2013 Delhi Set-III) Notes

Class 12 Economics Solved Paper (2013 Delhi Set-III) Commerce Questions

Study Class 12 Economics Solved Paper (2013 Delhi Set-III) on the App

|

© EduRev

|

Education Revolution

|

|