Financial Statements (Part - 1) - Commerce PDF Download

Page No 21.38:

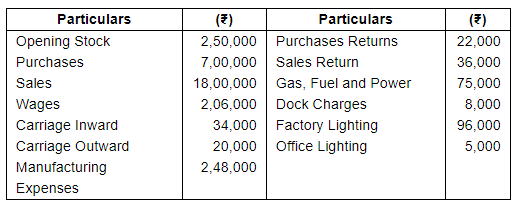

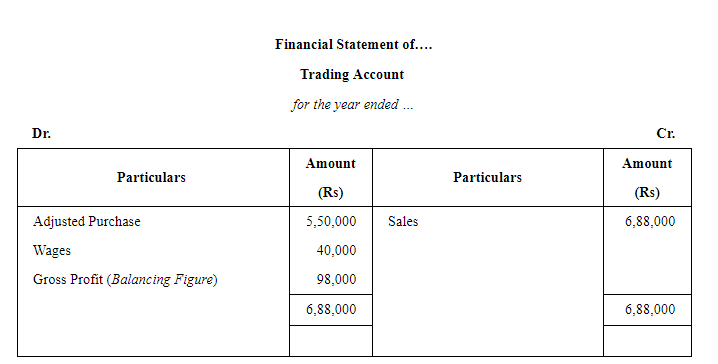

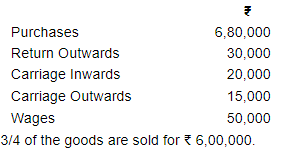

Question 1:

Prepare a Trading Account from the following particulars for the year ended 31st March 2017:-

Closing Stock is valued at ₹ 6,00,000.

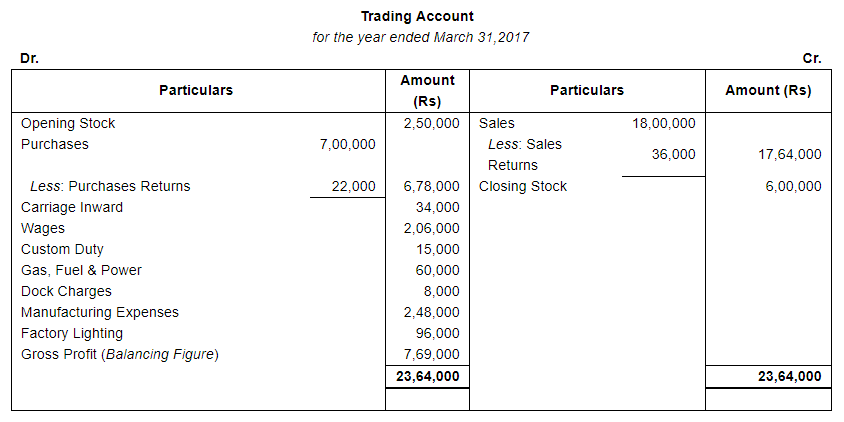

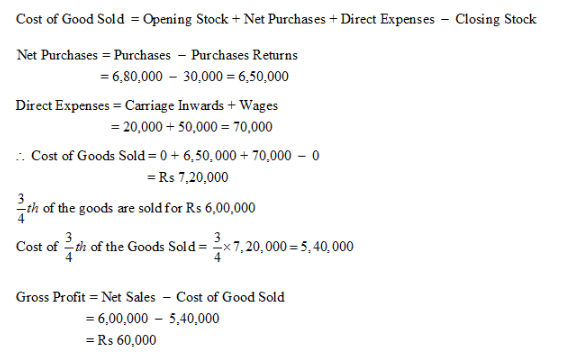

ANSWER:

Page No 21.39:

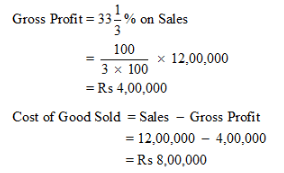

Question 2(A):

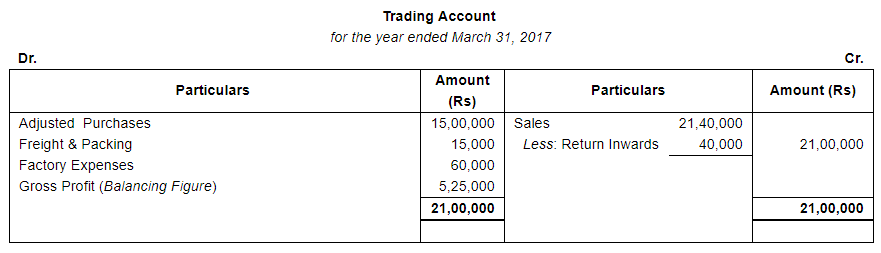

From the following information, prepare the Trading Account for the year ended 31st March, 2017:

Adjusted Purchases ₹ 15,00,000; Sales ₹ 21,40,000; Returns Inwards ₹ 40,000; Freight and Packing ₹ 15,000; Packing Expenses on Sales ₹ 20,000; Depreciation ₹ 36,000; Factory Expenses ₹ 60,000; Closing Stock ₹ 1,20,000.

ANSWER:

Note: Closing Stock will not be shown on the Credit side of Trading Account since it has already been adjusted while calculating adjusted purchases.

Adjusted Purchases = Opening Stock + Net Purchases – Closing Stock

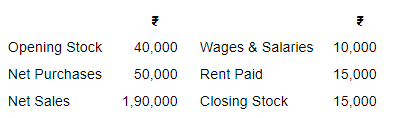

Question 2(B):

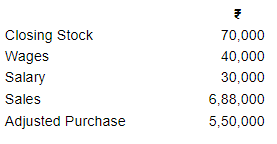

Calculate Gross Profit from the following information:

ANSWER:

Note: As adjusted purchases is given, it means opening and closing stock are already adjusted. So, these two stocks will not be considered while calculating Gross Profit.

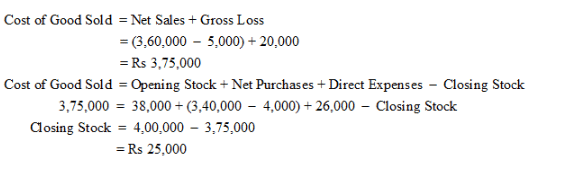

Question 3(A):

Calculate cost of goods sold from the following:

ANSWER:

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Cost of Goods Sold = 40,000 + 50,000 + 10,000 – 15,000 = ₹ 85,000

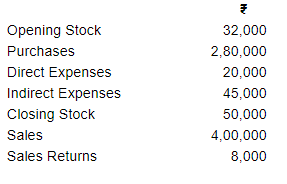

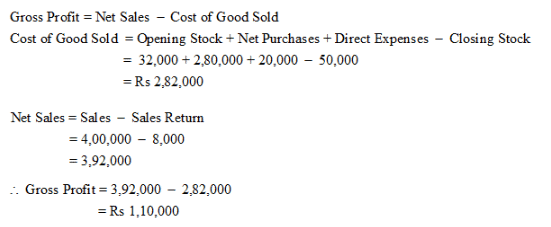

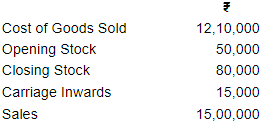

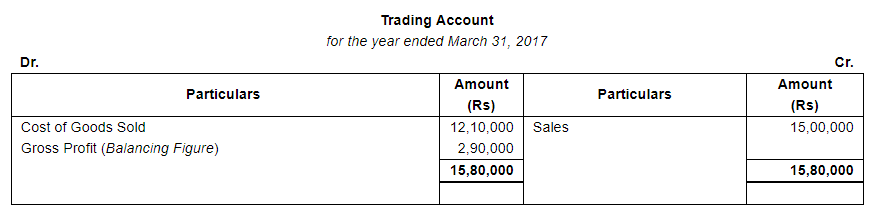

Question 3(B):

Ascertain cost of Goods Sold and Gross Profit from the following:

ANSWER:

Question 4:

Calculate Gross Profit on the basis of the following information:

ANSWER:

Page No 21.40:

Question 5(A):

Calculate Closing Stock and Cost of Goods Sold:

Opening Stock ₹ 5,000; Sales ₹ 16,000; Carriage Inwards ₹ 1,000; Sales Returns ₹ 1,000; Gross Profit ₹ 6,000; Purchase ₹ 10,000; Purchase Returns ₹ 900.

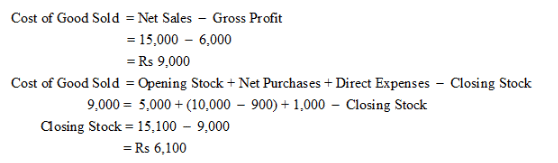

ANSWER:

Question 5(B):

Calculate Closing Stock from the following:

ANSWER:

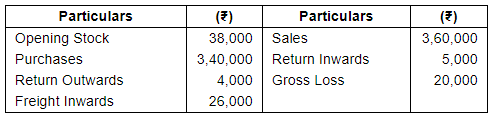

Question 6:

From the following information, prepare the Trading Account for the year ended 31st March, 2017:

ANSWER:

Note:

So, when the value of cost of goods sold is given, the items used to calculate it (i.e. opening stock, net purchases, direct expenses and closing stock) will not appear in the Trading Account.

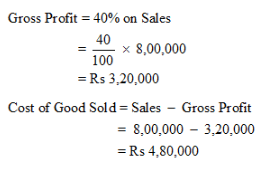

Question 7(A):

Calculate gross profit and cost of goods sold from the following information:

Net Sales ₹ 8,00,000

Gross Profit is 40% on Sales

ANSWER:

Question 7(B):

Calculate gross profit and cost of goods sold from the following information:

Net Sales - ₹ 12,000

Gross Profit  on sale

on sale

ANSWER:

Page No 21.41:

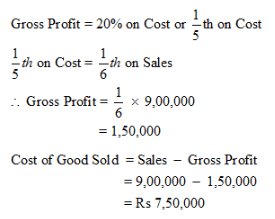

Question 8:

Calculate the gross profit and cost of goods sold from the following information:

Net Sales ₹ 9,00,000

Gross Profit is 20% on cost.

ANSWER:

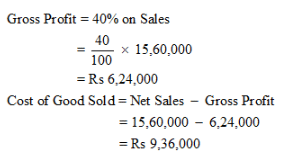

Question 9:

Ascertain the value of closing stock from the following:

| ₹ | |

| Opening Stock | 1,20,000 |

| Purchases during the year | 9,30,000 |

| Sales during the year | 15,60,000 |

| Rate of Gross Profit | 40% on Sales |

ANSWER:

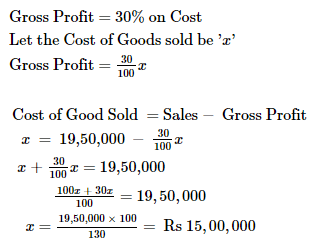

Question 10:

Calculate closing stock from the following details:

| ₹ | |

| Opening Stock | 4,80,000 |

| Purchase | 13,60,000 |

| Sales | 19,50,000 |

G.P. is 30% on Cost.

ANSWER:

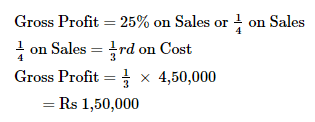

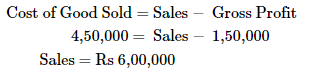

Question 11:

Calculate Net Sales and G.P. from the following:

Cost of Goods Sold - ₹ 4,50,000

G.P. - 25% on Sales

ANSWER:

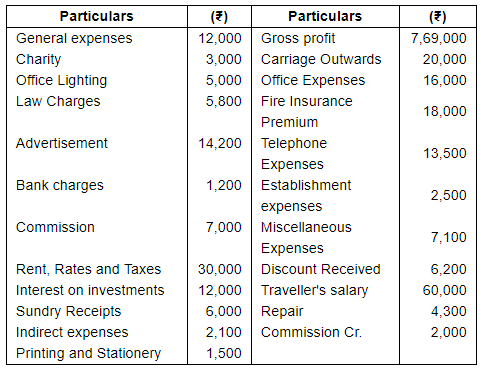

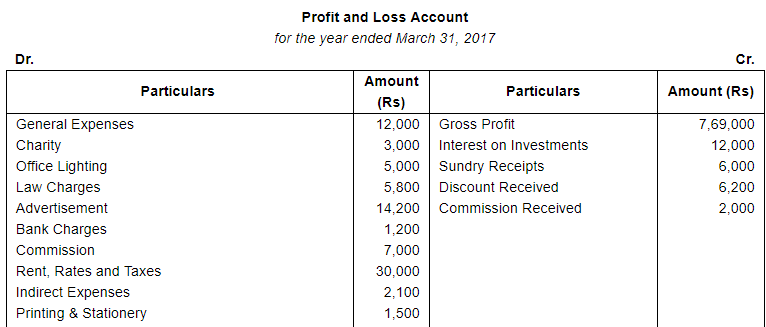

Question 12:

Prepare Profit and Loss Account for the year ended 31st March, 2017 from the following particulars:-

ANSWER:

Page No 21.42:

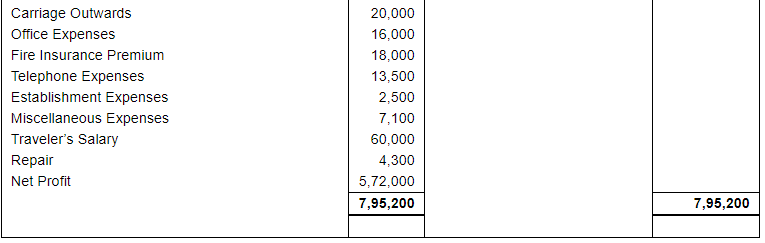

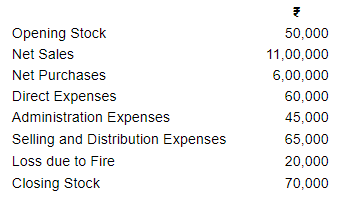

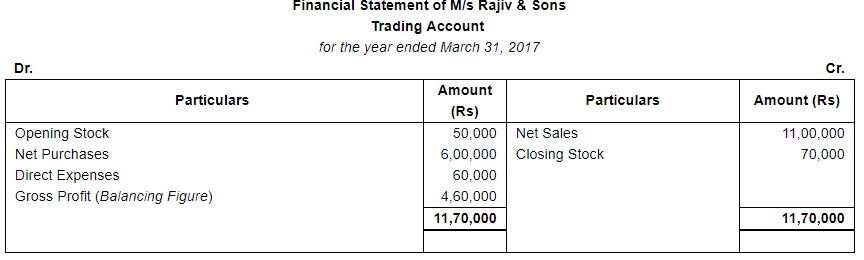

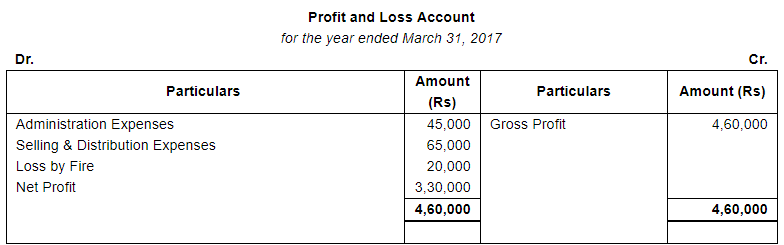

Question 13:

Calculate the amount of gross profit, operating profit and net profit on the basis of the following balances extracted from the books of M/s Rajiv & Sons for the year ended March 31, 2017.

ANSWER:

Working Notes:

Working Notes:

Operating Profit = Net Profit − Non-Operating Income + Non-Operating Expenses

= 3,30,000 − 0 + 20,000

= Rs 3,50,000

Loss by Fire is a non-operating expense, thus, added to the net profit to arrive at operating profit.

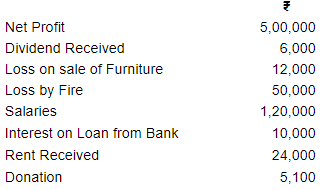

Question 14:

Calculate operating profit from the following:

ANSWER:

Operating Profit = Net Profit − Non-Operating Income + Non-Operating Expenses

Non-Operating Income = Dividend Received + Rent Received

= 6,000 + 24,000 = 30,000

Non-Operating Expenses = Loss on Sale of Furniture + Loss by Fire + Interest on Loan + Donation = 12,000 + 50,000 + 10,000 + 5,100 = Rs 77,100

∴ Operating Profit = 5,00,000 − 30,000 + 77,100 = Rs 5,47,100

Note: Salary being an operating expense was already taken into account while determining net profit, thus, it will be ignored now.

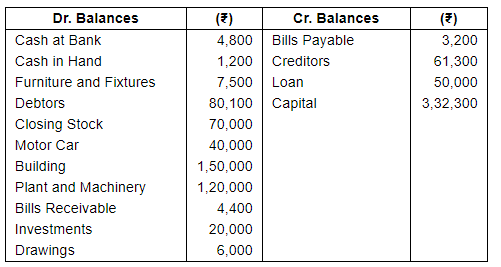

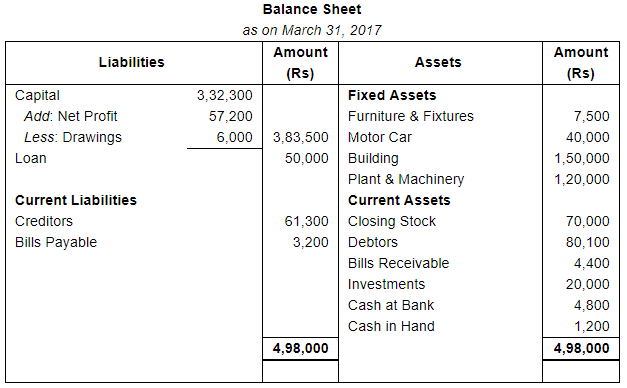

Question 15:

A merchant has earned a Net Profit of ₹ 57,200 for the year ended 31st March, 2017. Other balances in his Ledger are as under:-

Prepare his Balance Sheet as at 31st March, 2017.

ANSWER:

Page No 21.43:

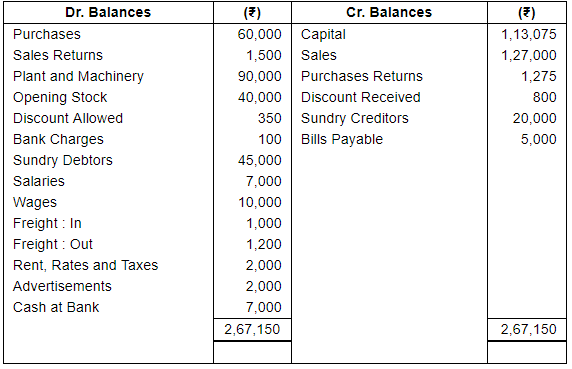

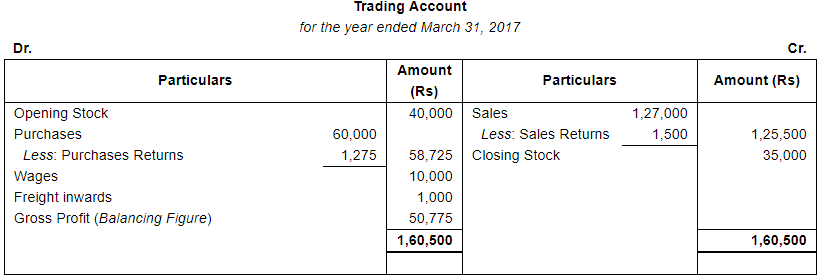

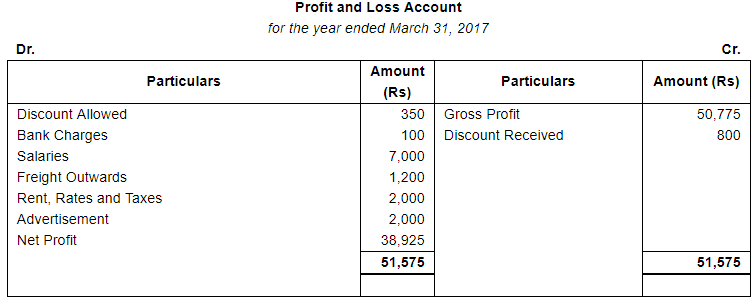

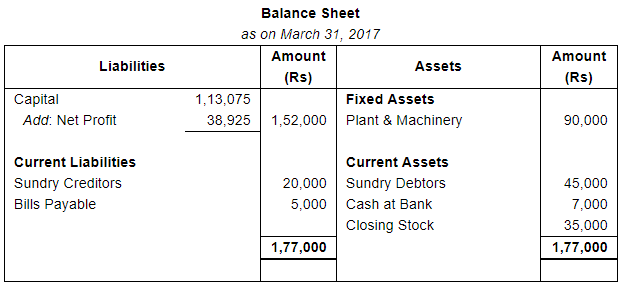

Question 16:

The Trial Balance shows the following balances as at 31st March, 2017:-

Closing Stock was valued at ₹ 35,000. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date.

ANSWER:

FAQs on Financial Statements (Part - 1) - Commerce

| 1. What are financial statements? |  |

| 2. Why are financial statements important? | |

| 3. What is the purpose of an income statement? | |

| 4. How is a balance sheet useful? | |

| 5. What information can be obtained from the statement of cash flows? | |

Important questions

,Previous Year Questions with Solutions

,study material

,Summary

,ppt

,MCQs

,Financial Statements (Part - 1) - Commerce

,video lectures

,Objective type Questions

,Free

,Financial Statements (Part - 1) - Commerce

,mock tests for examination

,Exam

,Financial Statements (Part - 1) - Commerce

,shortcuts and tricks

,Semester Notes

,Sample Paper

,past year papers

,Viva Questions

,Extra Questions

,practice quizzes

;

Financial Statements (Part - 1) Free PDF Download

Importance of Financial Statements (Part - 1)

Financial Statements (Part - 1) Notes

Financial Statements (Part - 1) Commerce Questions

Study Financial Statements (Part - 1) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!