Trial Balance and Errors (Part - 2) - Commerce PDF Download

Page No 14.29:

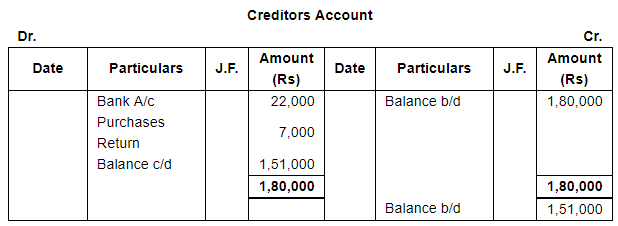

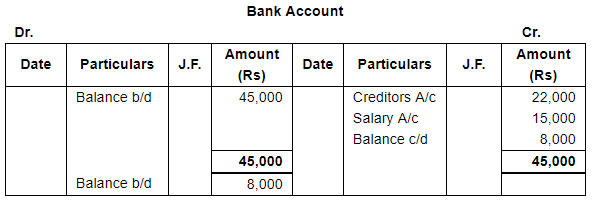

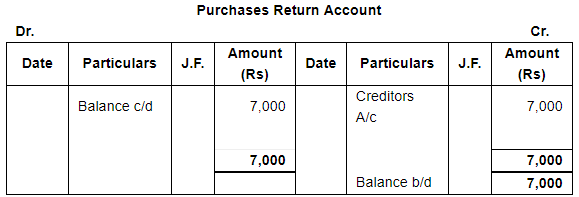

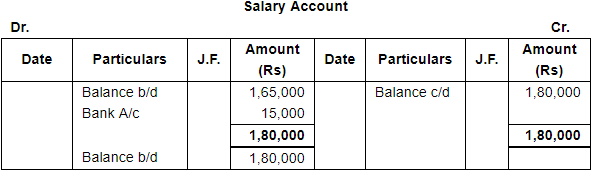

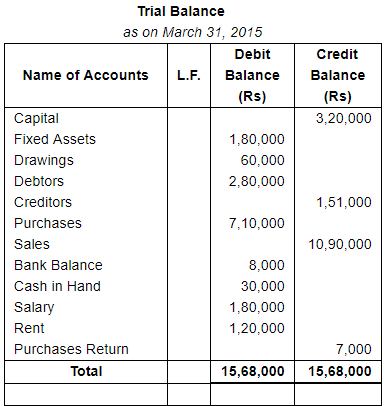

Question 6:

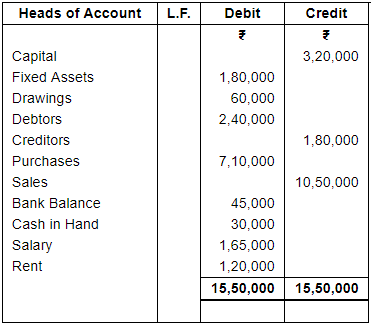

Following is the Trial Balance as at 31st March, 2015:

Having prepared the Trial Balance, it was discovered that following transactions remained unrecorded:

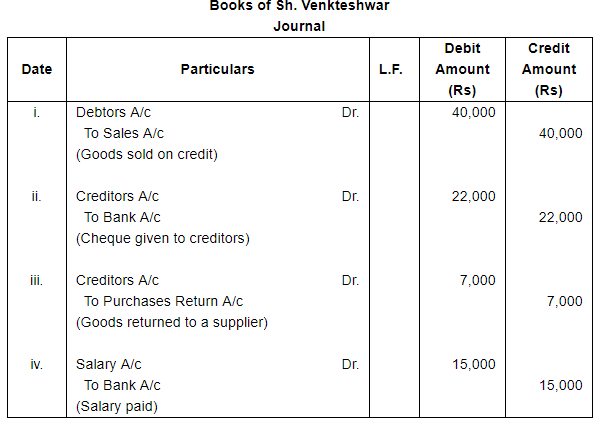

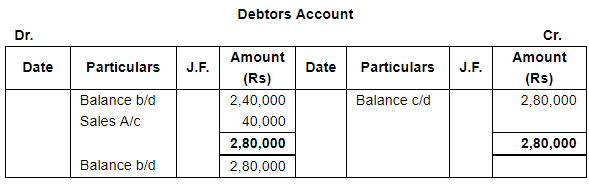

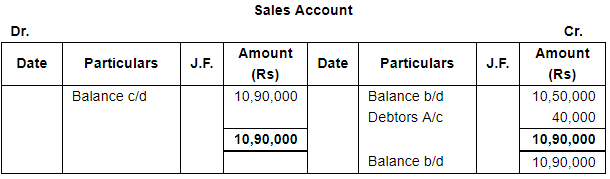

(i) Goods were sold on credit amounting to ₹ 40,000.

(ii) Paid to creditors ₹ 22,000 by cheque.

(iii) Goods worth ₹ 7,000 were returned to a supplier.

(iv) Paid salary ₹ 15,000 by cheque.

Required:

(i) Pass Journal entries for the above mentioned transactions and post them into Ledger

(ii) Redraft the Trial Balance.

ANSWER:

Page No 14.30:

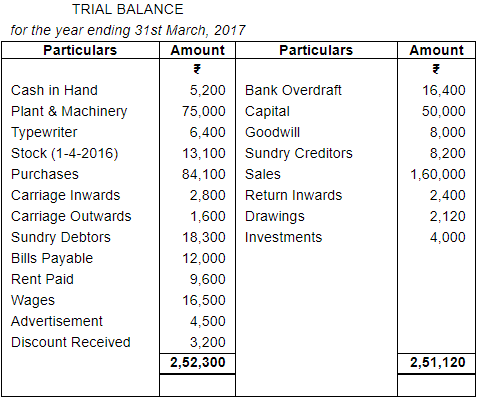

Question 7:

The following is the Trial Balance prepared by an inexperienced accountant. Redraft it in a correct form and give necessary notes : −

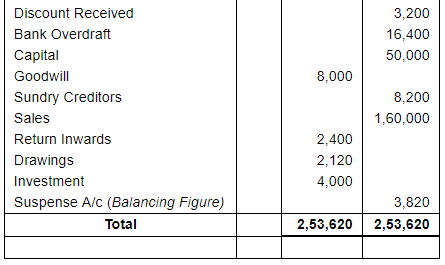

ANSWER:

Note: Since, the Trial Balance does not tally, thus, the difference of Rs 3,820 is transferred to the Credit Balance Column of Trial Balance

Page No 14.30:

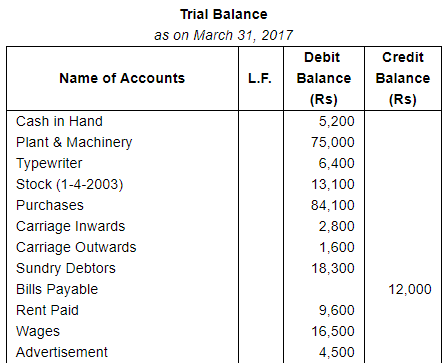

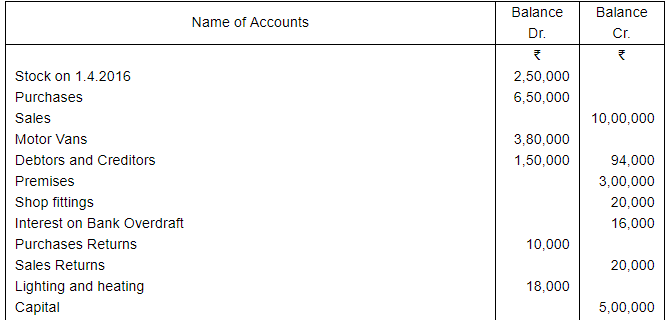

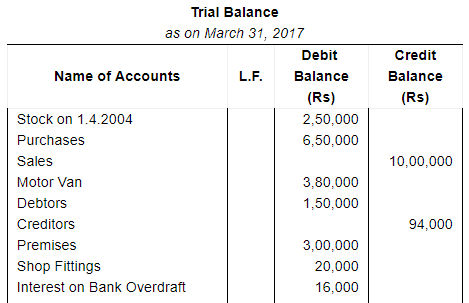

Question 8:

A book-keeper extracted the following Trial Balance as at 31st March, 2017 :

You are required to redraft the trial balance correctly.

ANSWER:

Note: Closing Stock of Rs 3,30,000 will not appear in Trial Balance, because it has not been accounted yet.

Page No 14.31:

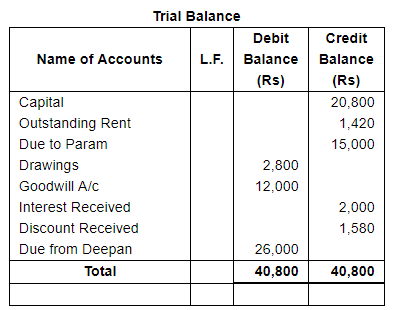

Question 9:

From the following ledger balances prepare trial balance :

Capital ₹ 20,800, Rent outstanding ₹ 1,420, Amount due to Param, ₹ 15,000, Drawing ₹ 2,800, Goodwill ₹ 12,000, Interest received ₹ 2,000, Discount received ₹ 1,580, Amount due from Deepan ₹ 26,000.

ANSWER:

FAQs on Trial Balance and Errors (Part - 2) - Commerce

| 1. What is a trial balance? |  |

| 2. What are the types of errors that can occur in a trial balance? | |

| 3. How do you identify errors in a trial balance? | |

| 4. What are some common causes of errors in a trial balance? | |

| 5. How can trial balance errors be rectified? | |

Exam

,mock tests for examination

,Objective type Questions

,Trial Balance and Errors (Part - 2) - Commerce

,Sample Paper

,Summary

,past year papers

,Trial Balance and Errors (Part - 2) - Commerce

,Extra Questions

,Important questions

,study material

,MCQs

,ppt

,shortcuts and tricks

,video lectures

,Free

,Trial Balance and Errors (Part - 2) - Commerce

,Previous Year Questions with Solutions

,practice quizzes

,Semester Notes

,Viva Questions

;

Trial Balance and Errors (Part - 2) Free PDF Download

Importance of Trial Balance and Errors (Part - 2)

Trial Balance and Errors (Part - 2) Notes

Trial Balance and Errors (Part - 2) Commerce Questions

Study Trial Balance and Errors (Part - 2) on the App

|

© EduRev

|

Education Revolution

|

|