Class 11 Economics Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

Q.1. Under which market form, a firm is a price taker?

Ans. A firm is a price taker under perfectly competitive market form.

Q.2. In which market form are the products homogeneous?

Ans. The products are homogeneous in the perfectly competitive market form.

Q.3. In which market form.AR. and MR of a firm always equal?

Ans. AR and MR of a firm are always equal under perfect competition.

Q.4. Define perfect competition.

Ans. Perfect competition is a market situation in which a large number of sellers sell homogeneous product with free entry and exit conditions.

Q.5. Name the characteristics which make monopolistic competition different from perfect competition.

Ans. The characteristic of homogeneous product makes monopolistic competition different from perfect competition.

Q.6. In which market form a firm cannot influence the price of the product?

Ans. A firm cannot influence the price of the product under perfect competition.

Q.7. In which market demand curve of a firm is perfectly elastic?

Ans. Market demand curve of a firm is perfectly elastic under perfect competition.

Q.8. What is the effect on price when a perfectly competitive firm tries to sell more?

Ans. The price will remain same when a perfectly competitive firm tries to sell more as its demand curve is perfectly elastic.

Q.9. What is meant by the term ‘price taker’ in the context of a firm?

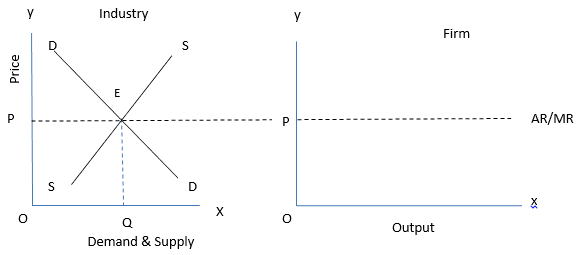

Ans. The price of the product under perfect competition is determined in the industry by the market forces of demand and supply and hence, an individual firm is merely a price taker.

Q.10. Mention three features of perfect competition.

Ans. Following are the three main features of perfect competition:

(i) There are large number of buyers and sellers in the market.

(ii) The products sold by each firm are homogeneous or identical.

(iii) There is free entry and exit of firms.

Q.11. Explain what happens to profits in the long run if the firms are free to enter the industry.

Ans. The freedom to entry and exit ensures that the firms earn just the normal profits in the long run. If the existing firms earn above-normal profits, new firms will enter the industry. This will raise the supply and bring the price down. The profits will fall till each firm is once again earning only the normal profits.

Q.12. Explain what happens to losses in the long run if the firms are free to leave the industry.

Ans. The freedom to entry and exit ensures that the firms earn just the normal profits in the long run. If the existing firms are incurring losses, the incompetent firms will start leaving the market. As a result, the supply will fall and the price will go up. The price will continue to rise till the losses are wiped out and firms are just earning normal profits.

Q.13. Explain feature ‘large number of sellers and buyers’ of a perfect competitive market.

Or

There are large number of buyers in a perfectly competitive market. Explain the significance of this feature.

Ans. There is such large number of buyers and sellers that none of them is in a position to influence the price in the market. Each buyer purchases only a small fraction of the total purchases in the market and is not in a position to influence the price of the good by restricting his purchase. Likewise, each seller produces only a small fraction of the total output in the market and is not in a position to influence the price of the good by withdrawing. The price of a good is determined by the whole industry, that is, by the combined actions of all the sellers and buyers.

Q.14. Explain the implication of‘perfect knowledge about market’ under perfect competition.

Ans. Perfect competition requires that all the buyers and sellers must possess perfect knowledge about the existing market conditions, especially regarding the market price, quantities and sources of supply. With the availability and use of perfect knowledge, no buyer could be charged a price different from the market price. Similarly, no seller would unnecessarily incur loss by selling at a price lower than the prevailing market price. In this way, perfect knowledge ensures market transactions at a uniform price.

Q.15. Define Total Revenue.

Ans. Total Revenue (TR) means the total amount of money, which a firm receives from the sale of goods and services produced by it during a given period.

Q.16. Define Marginal Revenue.

Ans. Marginal Revenue (MR) is the addition made to the Total Revenue by the sale of one more unit of output.

Q.17. What is the relationship between Total Revenue, price and quantity sold?

Ans. Total Revenue (TR) of the firm is obtained by multiplying the market price of the good (P) with the firm’s output (q). That is,

TR = P x q

Q.18. What is the relationship between price and Marginal Revenue for a competitive firm?

Ans. For a competitive firm, price and Marginal Revenue are equal (P = MR).

Q.19. What will be the behaviour of Marginal Revenue in a market for a product where a firm can sell any quantity at the given price?

Ans. Marginal Revenue will remain constant in a market for a product where a firm can sell any quantity at the given price.

Q.20. What is meant by revenue in economics?

Ans. Revenue refers to the money receipts of the producer from the sale of output.

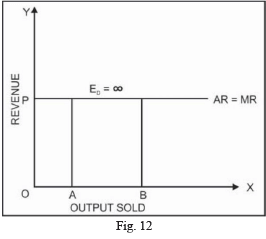

Q.21. Draw in a single diagram the Average Revenue and Marginal Revenue curves of a firm, which can sell any quantity of the good at a given price. Explain.

Ans. In a perfectly competition market, a firm can sell any quantity of the good at a given price. This can be explained with the help of a diagram.

In the diagram, the firm can sell any quantity of the commodity it produces at a given price OP. Price remain constant whether quantity demanded is OA or OB, or even zero.

Q.22. Give three reasons for a rightward shift of supply curve of a commodity.

Ans. Three factors responsible for a rightward shift of the supply curve of a good are:

(i) A technological advancement

(ii) A fall in the price of input

(iii) An increase in the number of firms in the market

Q.23. Explain the determinants of the market supply of a commodity.

Ans. Market supply curve is derived by the horizontal summation of individual supply curves. The determinants of the market supply of a commodity are as follows:

(i) Number of Firms: An increase (a decrease) in the number of firms shifts the market supply curve to the right (left).

(ii) Technological Changes: Technological progress shifts the market supply curve to the right. Similarly, technological degradation shifts the market supply curve to the left.

(iii) Input Price Changes: An increase (a decrease) in an input price shifts the supply curve to the left (right).

(iv) Change in the Excise Tax Rate: An increase (a decrease) in the excise tax shifts the market supply curve to the left (right).

(v) Change in the Price of Related Products: An increase (a decrease) in the price of a substitute good in production shifts the supply curve of a good to the left (right).

Q.24. State three causes of decrease in supply.

Ans. Following are the three causes of decrease in supply:

(i) Increase in the excise tax

(ii) Increase in the price of raw material or inputs

(iii) Technical degradation

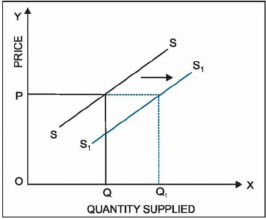

Q25. Explain the effect of technical progress on the supply of a good?

Or

Explain how technological progress is a determinant of supply of a good by a firm.

Ans. Supply of a particular good depends on the state of technology available to produce it. If there are improvements in the technology, it is possible to produce more goods with the same resources. As a result, there will be a lower cost of production. The Average and Marginal Costs facing a firm will be much less than earlier. Hence, supply curve will shift to the right from SS to SS . The quantity supplied by a firm increases from Q to Q at the existing price (P).

Q26. Explain the effect of rise in input prices on the supply of a good.

Ans. A change in the input prices affects a firm’s supply curve. If the price of an input, say, the wage rate of labour increases, the cost of production will also increase. The consequent increase in the firm’s Average Cost at any level of output is usually accompanied by an increase in the firm’s Marginal Cost at any level of output. That is, there is a leftward (or upward) shift of the MC curve. This means that the firm’s supply curve shifts to the left. At any given market price, the firm now supplies fewer units of output. In other words, an increase (decrease) in input prices is expected to shift the supply curve of a firm to the left (right).

Q27. Explain briefly why a firm under perfect competition is a price taker, not a price maker.

Ans. A firm under perfect competition is a price taker, not a price maker because the price is determined by the market forces of demand of supply. This price is known as the equilibrium price. All the firms in the industry have to sell their outputs at this equilibrium price. The reason is that the number of firms under perfect competition is so large. So no firm can influence the price by its supply. All firms produce homogeneous products.

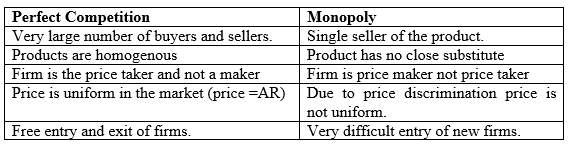

Q28. Distinguish between monopoly and perfect competition.

Ans.

Q29. How does an increase in the price of substitute goods in consumption affect the equilibrium price of a good? Explain with a diagram.

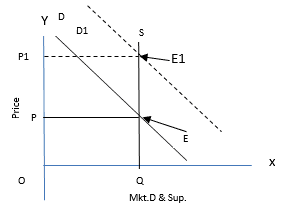

Ans. An increase in the price of substitute goods (coke) will cause an increase in demand for its related goods (Pepsi). The demand curve for Pepsi will shift to the right side. The supply curve of Pepsi remains the same. It will lead to an increase in the equilibrium price of Pepsi and an increase in quantity.

Result: Price increases from OP to OP1.Quantity demand increases from OQ to OQ1.

Q30. Show with the help of a diagram the effect on equilibrium price and quantity when supply is perfectly inelastic and demand increases and decreases.

Ans.

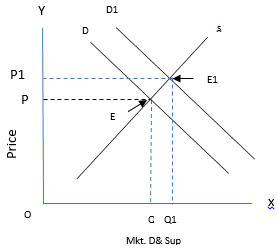

When supply is perfectly inelastic and demand increases. The demand curve shifts to towards right. The new demand curve D1 intersects the supply curve at point E1.

Result: Price increases from OP to OP1 and quantity demand remains unchanged.

|

59 videos|222 docs|43 tests

|

FAQs on Class 11 Economics Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

| 1. What are the main characteristics of perfect competition? |  |

| 2. How does a firm maximize profit under perfect competition? | |

| 3. What happens to a firm in perfect competition in the long run? | |

| 4. How does perfect competition affect consumer welfare? | |

| 5. Can a firm in perfect competition influence market prices? | |

study material

,Exam

,Free

,Sample Paper

,Extra Questions

,Semester Notes

,Summary

,Viva Questions

,mock tests for examination

,Class 11 Economics Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

,Class 11 Economics Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

,shortcuts and tricks

,Important questions

,practice quizzes

,ppt

,video lectures

,Objective type Questions

,MCQs

,Previous Year Questions with Solutions

,past year papers

,Class 11 Economics Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

;

Short Questions With Answers - The Theory Of The Firm Under Perfect Competition Free PDF Download

Importance of Short Questions With Answers - The Theory Of The Firm Under Perfect Competition

Short Questions With Answers - The Theory Of The Firm Under Perfect Competition Notes

Short Questions With Answers - The Theory Of The Firm Under Perfect Competition Commerce

Study Short Questions With Answers - The Theory Of The Firm Under Perfect Competition on the App

|

© EduRev

|

Education Revolution

|

|