Financial & Accounting Systems: Notes (Part - 2) | Financial Management & Strategic Management for CA Intermediate PDF Download

Risks and Controls in an ERP Environment

The risks being discussed here are specific to ERP systems used.

Introduction

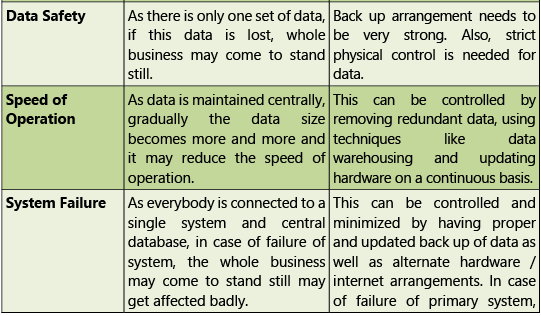

Major feature of an ERP System is Central Database. As the complete data is stored centrally at one place, ensuring safety of data and minimising risk of loss of data is a big challenge. In Non-Integrated System, data is stored by each department separately; hence this risk is low in such an environment. In an ERP environment, two major risks are faced by any organization:

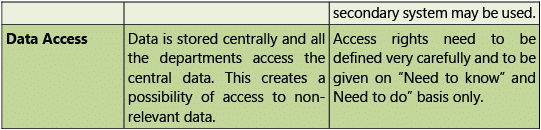

- Due to central database, all the persons in an organization access the same set of data on a day to basis. This again poses the risk of leakage of information or access of information to non-related people. E.g. A person from sales department checking salary of a person in production.

- Again, as there is central database, all users shall use the same data for recording of transactions. Hence, there is one more risk of putting incorrect data in the system by unrelated users. E.g. a person in Human Resource Department recording a purchase order. This is a risk due to central database only and controls are needed to minimise such type of risks.

ERP Implementation, its Risks and related Controls

ERP system implementation is a huge task and requires lot of time, money and above all patience. The success or failure of any ERP or saying it in terms of payback or ROI of an ERP, is dependent on its successful implementation and once implemented proper usage.

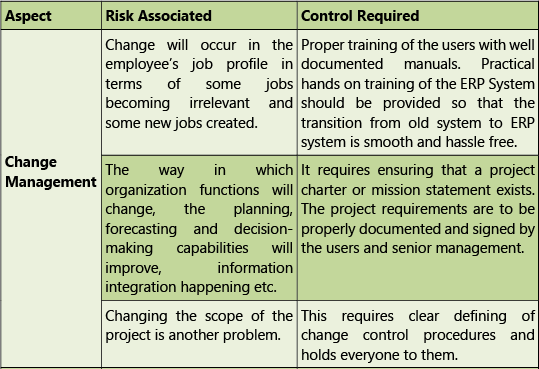

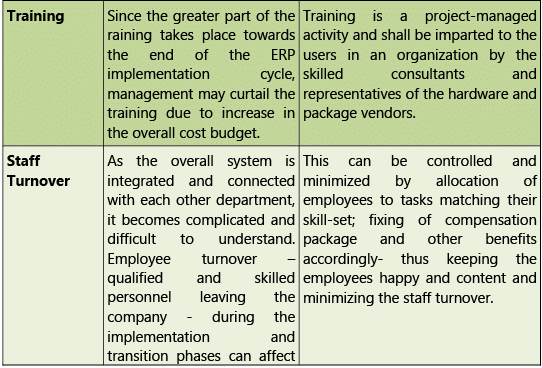

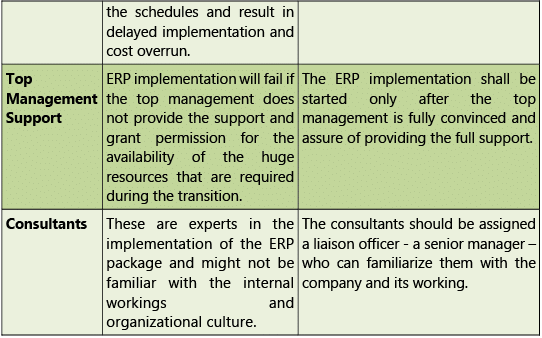

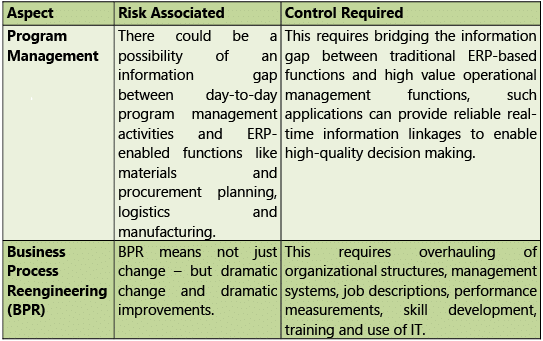

Tables 2.3.1(A,B,C,D,E) provide extensive discussion on the issues – People, Process, Technological, other implementation and post implementation issues that arise during implementation and related controls respectively.

- People Issues: Employees, Management, implementation team, consultants and vendors are the most crucial factor that decides the success or failure of an ERP System.

Table 2.3.1(A): Risks and corresponding Controls related to People Issues

- Process Risks: One of the main reasons for ERP implementation is to improve, streamline and make the business process more efficient, productive and effective.

Table 2.3.1(B): Risks and corresponding Controls related to Process Risks

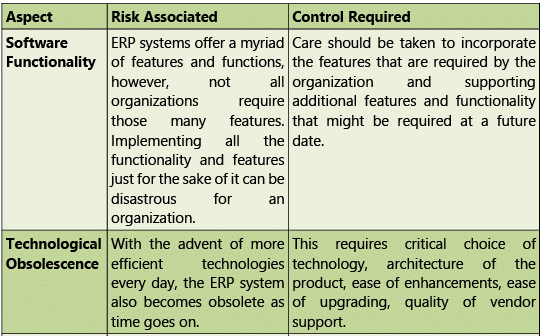

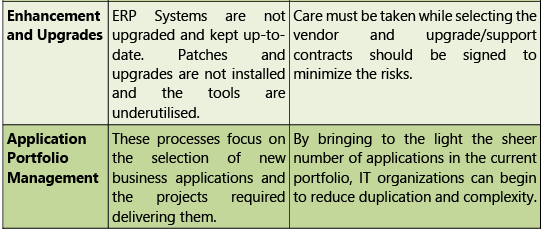

- Technological Risks: The organizations implementing ERP systems should keep abreast of the latest technological developments and implementation which is required to survive and thrive.

Table 2.3.1(C): Risks and corresponding Controls related to Technological Risks

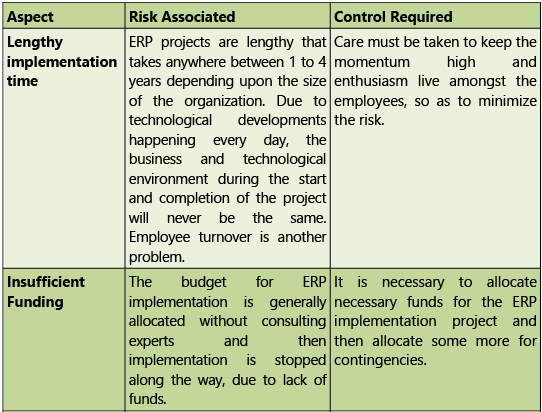

- Implementation Issues: Many times, ERP implementations are withdrawn because of the following factors.

Table 2.3.1(D): Risks and corresponding Controls related to some other implementation issues

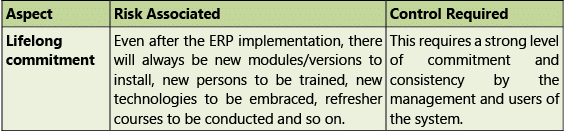

- Post Implementation issues: ERP operation and maintenance require a lifelong commitment by the company management and users of the system.

Table 2.3.1(E): Risks and corresponding Controls related to post- implementation issues

Role Based Access Control (RBAC) in ERP System

In computer systems security, Role-Based Access Control is an approach to restricting system access to authorized users. RBAC sometimes referred to as RoleBased Security is a policy neutral access control mechanism defined around roles and privileges that lets employees having access rights only to the information they need to do their jobs and prevent them from accessing information that doesn't pertain to them. It is used by most enterprises and can implement Mandatory Access Control (MAC) or Discretionary Access Control (DAC).

- MAC criteria are defined by the system administrator, strictly enforced by the Operating System and are unable to be altered by end users. Only users or devices with the required information security clearance can access protected resources. A central authority regulates access rights based on multiple levels of security. Organizations with varying levels of data classification, like government and military institutions, typically use MAC to classify all end users.

- Whereas, DAC involves physical or digital measures and is less restrictive than other access control systems as it offers individuals complete control over the resources they own. The owner of a protected system or resource sets policies defining who can access it.

The components of RBAC such as role-permissions, user-role and role-role relationships make it simple to perform user assignments. RBAC can be used to facilitate administration of security in large organizations with hundreds of users and thousands of permissions. Roles for staff are defined in organization and permission to access a specific system or perform certain operation is defined as per the role assigned. E.g. a junior accountant in accounting department is assigned a role of recording basic accounting transactions, an executive in human resource department is assigned a role of gathering data for salary calculations on monthly basis, etc.

Types of Access

While assigning access to Master Data, Transaction Data and Reports to different users; following options are possible.

(i) Create – Allows to create data;

(ii) Alter – Allows to alter data;

(iii) View – Allows only to view data; and

(iv) Print – Allows to print data.

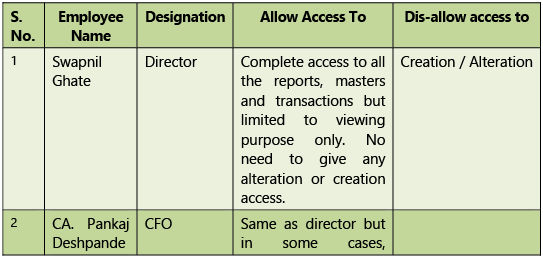

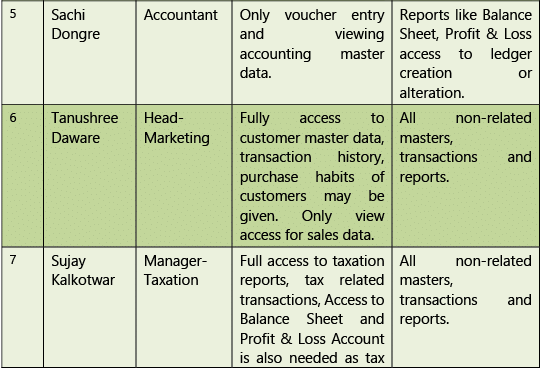

Example 4: Let us consider a small case study for better understanding of Role Based Access and Controls in Financial and Accounting Systems. Indradhanu Consulting Private Limited, a company dealing in project management is having different users as given in the Table 2.3.2 under.

Table 2.3.2: Users Database of Indradhanu Consulting Private Limited (Illustrative)

Audit of ERP Systems

The fundamental objectives of an audit of controls do not change in an ERP environment. When evaluating controls over ERP systems, decisions must be made regarding the relevance of operational internal control procedures to Information Technology (IT) controls. Specific control procedures for audit objectives must be tested. ERP systems should produce accurate, complete, and authorized information that is supportable and timely. In a computing environment, this is accomplished by a combination of controls in the ERP System, and controls in the environment in which the ERP system operates, including its operating system. Controls are divided into General Controls and Application Controls.

- General Controls include controls over Information Technology management controls addressing the information technology oversight process; Information Technology infrastructure, security management and software acquisition; monitoring and reporting information technology activities; business improvement initiatives; and development and maintenance. These controls apply to all systems − from mainframe to client/server to desktop computing environments. General controls can be further divided into Management Controls and Environmental Controls.

- Management Controls deal with organizations, policies, procedures, planning, and so on.

- Environmental Controls are the operational controls administered through the computer centre/computer operations group and the built-in operating system controls.

- Application Controls pertain to the scope of individual business processes or application systems. Individual applications may rely on effective operation of controls over information systems to ensure that interface data are generated when needed, supporting applications are available and interface errors are detected quickly.

Some of the questions auditors should ask during an ERP audit are pretty much the same as those that should be asked during development and implementation of the system:

- Does the system process as per GAAP (Generally Accepted Accounting Principles) and GAAS (Generally Accepted Auditing Standards)?

- Does it meet the needs for reporting, whether regulatory or organizational?

- Were adequate user requirements developed through meaningful interaction?

- Does the system protect confidentiality and integrity of information assets?

- Does it have controls to process only authentic, valid, accurate transactions?

- Are effective system operations and support functions provided?

- Are all system resources protected from unauthorized access and use?

- Are user privileges based on what is called “role-based access?”

- Is there an ERP system administrator with clearly defined responsibilities?

- Is the functionality acceptable? Are user requirements met? Are users happy?

- Have workarounds or manual steps been required to meet business needs?

- Are there adequate audit trails and monitoring of user activities?

- Can the system provide management with suitable performance data?

- Are users trained? Do they have complete and current documentation?

- Is there a problem-escalation process?

Auditing aspects in case of any ERP system can be summarized as under:

(i) Auditing of Data

- Physical Safety – Ensuring physical control over data.

- Access Control – Ensuring access to the system is given on “need to know” (a junior accountant need not view Profit & Loss Account of the business) and “need to do basis” (HR executive need not record a Purchase Order).

(ii) Auditing of Processes

- Functional Audit – This includes testing of different functions / features in the system and testing of the overall process or part of process in the system and its comparison with actual process. E.g. Purchase Process, Sales Process, Salary Calculation Process, Recruitment Process, etc. Auditor may check this process in the system and compare it with actual process. It is quite possible that all the aspect present in the actual process may not be integrated in the ERP system. There may be some manual intervention.

- Input Validations – This stands for checking of rules for input of data into the system. E.g. a transaction of cash sales on sales counter must not be recorded in a date other than today (not a future date or a back date), amount field must not be zero, stock item field shall not be empty, etc. Input validations shall change according to each data input form.

ERP Case Study of a Chartered Accountant Firm

As everybody is familiar with working environment in a Chartered Accountant (CA) firm, let us consider possibility of implementing ERP system in a CA Firm.

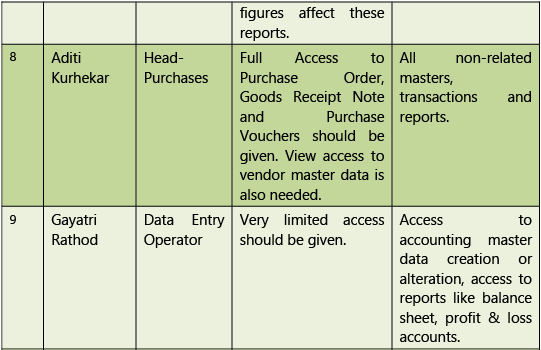

Example 5: Nirman Infrastructures Pvt. Ltd. a client of Ghate Deshpande & Co. (a CA Firm) receives a notice for scrutiny assessment from Income Tax Department. Following shall be the events in normal case.

(i) Client informs about receipt of notice to CA. Pankaj Deshpande (Partner) on phone and sends the copy of notice to CA Firm.

(ii) Notice is received at CA firm, read and understood. A task for giving reply to Income Tax Department is allotted to Sachi Dongre, an article clerk.

(iii) Sachi asks for some original documents (PAN, Memorandum of Articles, Agreements etc.) from client for working. These documents need to be returned to client after the work.(iv) Sachi works on this task, prepares the reply and submits it with Income Tax Department. Also, She updates CA. Pankaj Deshpande and Mayura (Accountant) about it.

(v) Bill is prepared by Mayura and approved by CA. Pankaj Deshpande.

(vi) Bill is submitted with client.

(vii) Documents are returned to client.

(viii) Cheque received from client against the bill submitted.

(ix) Receipt is recorded in books of accounts.

This is how a simple case is handled in a CA Firm. Let us now discuss important points regarding this case. In case of any ERP System, two aspects are very important – Communication (Internal and External) and Documentation.

Refer Fig. 2.5.1 to understand the workflow of CA Firm using Integrated System.

- Communication in this case is starting from client.

- Instead of client calling his CA, he should put the information as a service request in the central database maintained by CA Firm.

- As soon as service request is put by client into the system, one or more partner should be informed by the system about new service request.

- Partner shall convert this request into the task and allot it to one of the assistant.

- On allotment of task to the assistant, client must be updated about this task allotment.

- Article assistant shall contact client for requirement of information regarding work.

- Client shall submit the document through the system and update the information in central database.

- Article shall complete the work and send it for approval of his boss.

- After approval of work by article, client shall be automatically informed about it through the system only.

- Information shall be passed on to accounts department for preparation of bill for this assignment.

- Bill shall be raised from the system and sent to client through email.

- Client shall pay the fees and receipt is recorded in the same system.

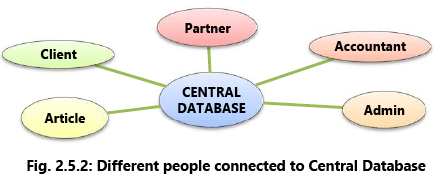

In this whole process, two important aspects, i.e. Communication and Documentation are taken care of in the best possible manner. Instead of a person communicating with other, system is communicating automatically after every updation. Fig. 2.5.2 showing different people connected to central database.

In case of an Integrated System, there shall be only one system of communication with others. But in case of non-integrated system people use multiple modes for communication like making a phone call, sending SMS, Email, WhatsApp or personal meeting. But the major problem with these multiple option is that there is no inter-connectivity between these modes and hence track of the overall process is not available.

Business Process Modules and their Integration with Financial and Accounting Systems

What is a Business Process?

A Business Process consists of a set of activities that are performed in coordination in an organizational and technical environment. These activities jointly realize a business goal. Each business process is enacted by a single organization, but it may interact with business processes performed by other organizations. To manage a process-

- The first task is to define it. This involves defining the steps (tasks) in the process and mapping the tasks to the roles involved in the process.

- Once the process is mapped and implemented, performance measures can be established. Establishing measurements creates a basis to improve the process.

- The last piece of the process management definition describes the organizational setup that enables the standardization and adherence to the process throughout the organization. Assigning enterprise process owners and aligning employees’ performance reviews and compensation to the value creation of the processes could accomplish this.

Process management is based on a view of an organization as a system of interlinked processes which involves concerted efforts to map, improve and adhere to organizational processes; whereas traditional organizations are composed of departments and functional stages, this definition views organization as networks or systems of processes. Process orientation is at the core of BPM.

Business Process Flow

As discussed earlier, a Business Process is a prescribed sequence of work steps performed to produce a desired result for the organization. A business process is initiated by a kind of event, has a well-defined beginning and end, and is usually completed in a relatively short period. Organizations have many different business processes such as completing a sale, purchasing raw materials, paying employees and paying vendors, etc. Each of the business processes has either a direct or indirect effect on the financial status of the organization. The number and type of business processes and how the processes are performed would vary across enterprises and is also impacted by automation. However, most of the common processes would flow a generic life cycle.

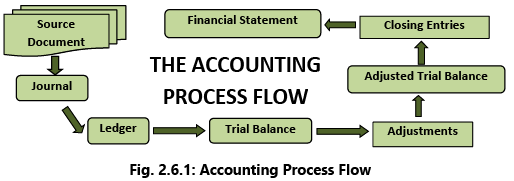

Example 6: Accounting Process Flow

Accounting or Book-keeping cycle covers the business processes involved in recording and processing accounting events of a company. It begins when a transaction or financial event occurs and ends with its inclusion in the financial statements. A typical life cycle of an accounting transaction may include the following transactions as depicted in Fig. 2.6.1:

(a) Source Document: A document that captures data from transactions and events.

(b) Journal: Transactions are recorded into journals from the source document.

(c) Ledger: Entries are posted to the ledger from the journal.

(d) Trial Balance: Unadjusted trial balance containing totals from all account heads is prepared.

(e) Adjustments: Appropriate adjustment entries are passed.

(f) Adjusted Trial balance: The trial balance is finalized post adjustments.

(g) Closing Entries: Appropriate entries are passed to transfer accounts to financial statements.

(h) Financial statement: The accounts are organized into the financial statements.

ERP - Business Process Modules (BPM)

A. Business Categories of BPM

There are three different nature and types of businesses that are operated with the purpose of earning profit. Each type of business has distinctive features.

- Trading Business – Trading simply means buying and selling goods without any modifications, as it is. Hence inventory accounting is a major aspect in this case. Purchase and sales transactions cover major portion of accounting. This industry requires accounting as well as inventory modules.

- Manufacturing Business – This type of business includes all aspects of trading business plus additional aspect of manufacturing. Manufacturing is simply buying raw material, changing its form and selling it as a part of trading. Here also, inventory accounting plays a major role. This type of industry requires accounting and complete inventory along with manufacturing module.

- Service Business – This type of business does not have any inventory. It is selling of skills/knowledge/efforts/time. E.g. Doctors, Architects, Chartered Accountants, are the professionals into service business. There may be other type of business into service, i.e. courier business, security service, etc. This industry does not require inventory module.

B. Functional Modules of ERP

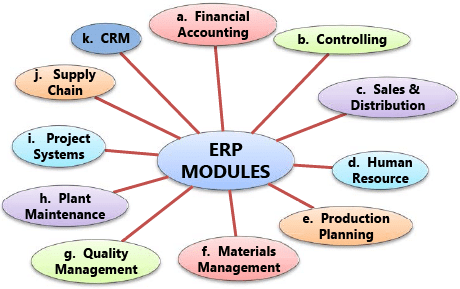

Business process may change per type of business. There may be different business units within a business. Hence different modules are possible in an integrated system. There may be modules as under. Fig. 2.6.2 shows different business process modules in ERP System. There may be some other modules also. Different types of industries require different modules. Fig. 2.6.2: ERP Modules(a) Financial Accounting Module

Fig. 2.6.2: ERP Modules(a) Financial Accounting Module

This module is the most important module of the overall ERP System and it connects all the modules to each other. Every module is somehow connected with module.

Following are the key features of this module.

- Tracking of flow of financial data across the organization in a controlled manner and integrating all the information for effective strategic decision making.

- Creation of Organizational Structure (Defining Company, Company Codes, business Areas, Functional Areas, Credit Control, Assignment of Company Codes to Credit Controls).

- Financial Accounting Global Settings (Maintenance of Fiscal Year, Posting Periods, defining Document types, posting keys, Number ranges for documents).

- General Ledger Accounting (Creation of Chart of Accounts, Account groups, defining data transfer rules, creation of General Ledger Account).

- Tax Configuration & Creation and Maintenance of House of Banks.

- Account Payables, accounts receivable, fixed assets, general ledger and cash management, etc. (Creation of Vendor Master data and vendor-related finance attributes like account groups and payment terms).

- Account Receivables (Creation of Customer Master data and customer-related finance attributes like account groups and payment terms).

- Asset Accounting.

- Integration with Sales and Distribution and Materials Management.

(b) Controlling Module

This module facilitates coordinating, monitoring, and optimizing all the processes in an organization. It controls the business flow in an organization. This module helps in analysing the actual figures with the planned data and in planning business strategies. Two kinds of elements are managed in Controlling Module − Cost Elements and Revenue Elements. These elements are stored in the Financial Accounting module.

Key features of this module are as under:

- Cost Element Accounting: This component provides overview of the costs and revenues that occur in an organization. The cost elements are the basis for cost accounting and enable the user the ability to display costs for each of the accounts that have been assigned to the cost element. Examples of accounts that can be assigned are Cost Centres, Internal Orders, WBS (Work Breakdown Structures).

- Cost Centre Accounting: This provides information on the costs incurred by the business. Cost Centres can be created for such functional areas as Marketing, Purchasing, Human Resources, Finance, Facilities, Information Systems, Administrative Support, Legal, Shipping/Receiving, or even Quality. Some of the benefits of Cost Centre Accounting are that the managers can set budget / cost Centre targets; Planning; Availability of Cost allocation methods; and Assessments / Distribution of costs to other cost objects.

- Activity-Based-Accounting: This analyses cross-departmental business processes and allows for a process-oriented and cross-functional view of the cost centres.

- Internal Orders: Internal Orders provide a means of tracking costs of a specific job, service, or task. These are used as a method to collect those costs and business transactions related to the task. This level of monitoring can be very detailed but allows management the ability to review Internal Order activity for better-decision making purposes.

- Product Cost Controlling: This calculates the costs that occur during the manufacture of a product or provision of a service and allows the management the ability to analyse their product costs and to make decisions on the optimal price(s) to market their products.

- Profitability Analysis: This allows the management to review information with respect to the company’s profit or contribution margin by individual market segment.

- Profit Centre Accounting: This evaluates the profit or loss of individual, independent areas within an organization.

(c) Sales and Distribution Module

Sales and Distribution is one of the most important modules. It has a high level of integration complexity. Sales and Distribution is used by organizations to support sales and distribution activities of products and services, starting from enquiry to order and then ending with delivery. Sales and Distribution can monitor a plethora of activities that take place in an organization such as products enquires, quotation (pre-sales activities), placing order, pricing, scheduling deliveries (sales activity), picking, packing, goods issue, shipment of products to customers, delivery of products and billings. In all these processes, multiple modules are involved such as FA (Finance & Accounting), CO (Controlling), MM (Material Management), PP (Production Planning), LE (Logistics Execution), etc.; which shows the complexity of the integration involved.

Sales and Distribution can monitor a plethora of activities that take place in an organization such as products enquires, quotation (pre-sales activities), placing order, pricing, scheduling deliveries (sales activity), picking, packing, goods issue, shipment of products to customers, delivery of products and billings. In all these processes, multiple modules are involved such as FA (Finance & Accounting), CO (Controlling), MM (Material Management), PP (Production Planning), LE (Logistics Execution), etc.; which shows the complexity of the integration involved.

Key features of Sales and Distribution Module are discussed as under:

- Setting up Organization Structure: Creation of new company, company codes, sales organization, distribution channels, divisions, business area, plants, sales area, maintaining sales offices, storage location;

- Assigning Organizational Units: Assignment of individual components created in the above activities with each other per design like company code to company, sales organization to company code, distribution channel to sales organization, etc.;

- Defining Pricing Components: Defining condition tables, condition types, condition sequences;

- Setting up sales document types, billing types, and tax-related components; and

- Setting up Customer master data records and configuration.

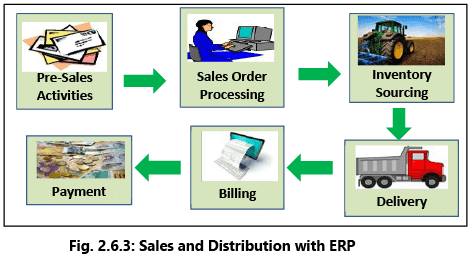

Sales and Distribution Process (Referring Fig. 2.6.3)

- Pre-Sales Activities: Include prospecting of customers, identifying prospective customers, gathering data, contacting them and fixing appointments, showing demo, discussion, submission of quotations, etc.

- Sales Order: Sales order is recorded in our books after getting a confirmed purchased order from our customer. Sales order shall contain details just like purchase order. E.g. Stock Item Details, Quantity, Rate, Due Date of Delivery, Place of Delivery, etc.

- Inventory Sourcing: It includes making arrangements before delivery of goods; ensuring goods are ready and available for delivery.

- Material Delivery: Material is delivered to the customer as per sales order. All inventory details are copied from Sales Order to Material Delivery for saving user’s time and efforts. This transaction shall have a linking with Sales Order. Stock balance shall be reduced on recording of this transaction.

- Billing: This is a transaction of raising an invoice against the delivery of material to customer. This transaction shall have a linking with Material Delivery and all the details shall be copied from it. Stock balance shall not affect again.

- Receipt from Customer / Payment: This is a transaction of receiving amount from customer against sales invoice and shall have a linking with sales invoice.

(d) Human Resource Module

This module enhances the work process and data management within HR department of enterprises. Right from hiring a person to evaluating one’s performance, managing promotions, compensations, handling payroll and other related activities of an HR is processed using this module. The task of managing the details and task flow of the most important resource i.e. human resource is managed using this module.

The most important objective of master data administration in Human Resources is to enter employee-related data for administrative, time-recording, training and payroll purposes. Payroll and Personnel departments deal with Human Resource of the organization. This department maintains total employee database. Wage, time and attendance related information comes to this department. They also prepare wage sheet for workmen; handle Provident Fund, ESI related formalities. This is perhaps the only module, which exchange very few information with other modules.

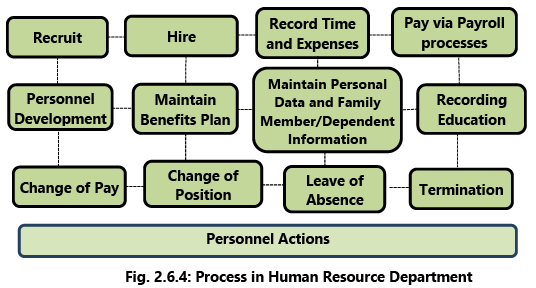

Concerning manpower, its requirement and utilization is one of the major chunks of profit for an organization. So, in this regard, every aspect of business transaction is taken care of by defining the master shifts master, Provident Fund (PF) ESI (Employees’ State Insurance) master, leave, holiday, loans, employee master, operations and suboperations masters etc. Also, the various input transaction such as Attendance Entry, Leave, holiday, Earning/Deduction entry, Advances etc. Finally, different types of Payroll reports, which can be of various types according to specified company standard. Fig. 2.6.4 showing processes involved in Human Resource Department.

- The module starts with the employee and workmen master.

- Employees being a part of a department so there will be provision of department and designation master. The job of this module is to record the regular attendance of every employee.

- Usage of magnetic card or finger print recognition devices will help to improve the attendance system and provide an overall security in terms of discarding proxy attendance.

- Moreover, if the attendance related information can be digitised then the major portion of monthly salary can be automated. But the authority should study the feasibility of this kind of system.

- This module will also deal with the financial entries like advance or loan to employees.

- From Holiday master provided with the module, the user could feed all possible holidays at the beginning of a year, so leave related information can be automated. This module will generate monthly wage sheet from which the salary payment can be made and respective accounts will be updated.

- All figures will be protected under password. Only authorized person will be eligible to access information from this module

(e) Production Planning (PP) Module

Production Planning (PP) Module is another important module that includes software designed specifically for production planning and management. This module also consists of master data, system configuration and transactions to accomplish plan procedure for production. PP module collaborates with Master Data, Sales and Operations Planning (SOP), Distribution Resource Planning (DRP), Production Planning, Material Requirements Planning (MRP), Capacity Planning, Product Cost Planning and so on while working towards production management in enterprises.

- Master Data – This includes the material master, work centres, routings and bill of materials.

- SOP - Sales and Operations Planning (SOP) provides the ability to forecast sales and production plans based on historical, current and future data.

- DRP - Distribution Resource Planning (DRP) allows companies the ability to plan the demand for distribution centres.

- Production Planning – This includes material forecasting, demand management, long term planning and master production scheduling (MPS).

- MRP - Material Requirements planning relies on demand and supply elements with the calculation parameters to calculate the net requirements from the planning run.

- Capacity Planning – This evaluates the capacity utilized based on the work centres available capacity to show capacity constraints.

- Product Cost Planning – This is the process of evaluating all the time values and value of component materials to determine the product cost.

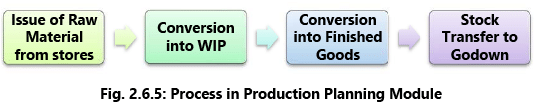

Conversion into Work In Process (WIP) may include more than one step. Also, conversion into Finished Goods may include packing process also.

(f) Material Management (MM) Module

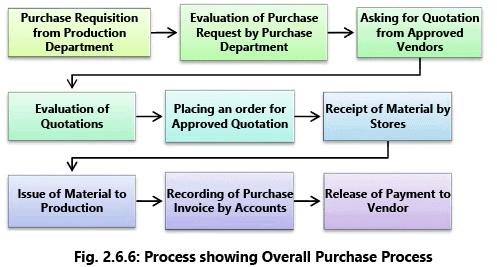

Material Management (MM) Module as the term suggests manages materials required, processed and produced in enterprises. Different types of procurement processes are managed with this system. Some of the popular sub-components in MM module are vendor master data; consumption based planning, purchasing, inventory management, invoice verification and so on. Material Management also deals with movement of materials via other modules like logistics, Supply Chain Management, sales and delivery, warehouse management, production and planning. Fig. 2.6.6 showing overall purchase process.

- Purchase Requisition from Production Department: Production department sends a request to purchase department for purchase of raw material required for production.

- Evaluation of Requisition: Purchase department shall evaluate the requisition with the current stock position and purchase order pending position and shall decide about accepting or rejection the requisition.

- Asking for Quotation: If requisition is accepted, quotations shall be asked to approve vendors for purchase of material.

- Evaluation of Quotations: Quotations received shall be evaluated and compared.

- Purchase Order: This is a transaction for letting an approved vendor know what we want to purchase, how much we want to purchase, at what rate we want to purchase, by what date we want the delivery, where we want the delivery. Hence, a typical purchase order shall have following information.

(i) Description of stock items to be purchased.

(ii) Quantity of these stock items.

(iii) Rate for purchases.

(iv) Due Date by which material is to be received.

(v) Godown where material is to be received.

- Receipt of Material: This is a transaction of receipt of material against purchase order which is commonly known as Material Receipt Note (MRN) or Goods Receipt Note (GRN). This transaction shall have a linking with Purchase Order. Information in Purchase Order is automatically copied to Material Receipt Voucher for saving time and efforts of user. Stock is increased after recording of this transaction.

- Issue of Material: Material received by stores shall be issued to production department as per requirement.

- Purchase Invoice: This is a financial transaction. Trial balance is affected due this transaction. Material Receipt transaction does not affect trial balance. This transaction shall have a linking with Material Receipt Transaction and all the details of material received shall be copied automatically in purchase invoice. As stock is increased in Material Receipt transaction, it will not be increased again after recording of purchase invoice.

- Payment to Vendor: Payment shall be made to vendor based on purchase invoice recorded earlier. Payment transaction shall have a linking with purchase invoice.

Please note that Purchase Order and Material Receipt are not part of financial accounting and does not affect trial balance. But these transactions are part of overall Financial and Accounting System.

(g) Quality Management Module

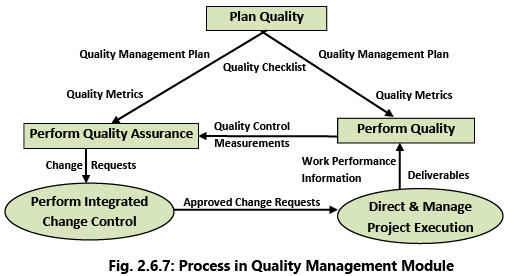

Quality Management (QM) Module helps in management of quality in productions across processes in an organization. This module helps an organization to accelerate their business by adopting a structured and functional way of managing quality in different processes. Quality Management module collaborates in procurement and sales, production, planning, inspection, notification, control, audit management and so on. Fig. 2.6.7 showing Process in Quality Management Module.

- Quality Planning: Quality planning is the process of planning the production activities to achieve the goals of meeting the customer requirements in time, within the available resources.

- Quality Control: It is a system for ensuring the maintenance of proper standards in manufactured goods, especially by periodic random inspection of the product. IT involves the checking and monitoring of the process and products with an intention of preventing non-conforming materials from going to the customer. Various result areas are identified for each process and studies are conducted to verify whether those results are being achieved.

- Quality Assurance: Quality assurance concentrates on identifying various processes, their interactions and sequence, defining the objectives of each process, identifying the key result areas and measures to measure the results, establishing the procedures for getting the required results, documenting the procedures to enable everyone to follow the same, educating the people to implement the procedures, preparing standard operating instructions to guide the people on work spot, monitoring and measuring the performance, taking suitable actions on deviations and continuously improving the systems.

- Quality Improvement: Quality improvement is a never-ending process. The customer’s needs and expectations are continuously changing depending on the changes in technology, economy, political situation, ambitions and dreams, competition, etc.

Quality Management Process includes the following:

- Master data and standards are set for quality management;

- Set Quality Targets to be met;

- Quality management plan is prepared;

- Define how those quality targets will be measured;

- Take the actions needed to measure quality;

- Identify quality issues and improvements and changes to be made;

- In case of any change is needed in the product, change requests are sent;

- Report on the overall level of quality achieved; and

- Quality is checked at multiple points, e.g. inwards of goods at warehouse, manufacturing, procurement, returns.

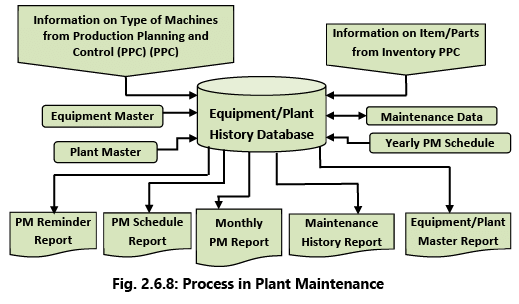

(h) Plant Maintenance Module

Plant Maintenance (PM) is a functional module which handles the maintaining of equipment and enables efficient planning of production and generation schedules. This application component provides us a comprehensive software solution for all maintenance activities that are performed within a company. It supports cost-efficient maintenance methods such as risk-based maintenance or preventive maintenance, and provides comprehensive outage planning and powerful work order management.

Objectives of Plant Maintenance Module

(i) To achieve minimum breakdown and to keep the plant in good working condition at the lowest possible cost.

(ii) To keep machines and other facilities in a condition that permits them to be used at their optimum (profit making) capacity without any interruption or hindrance.

(iii) To ensure the availability of the machines, buildings and services required by other sections of the factory for the performance of their functions at optimum return on investment whether this investment be in material, machinery or personnel.

Fig. 2.6.8 is showing process in Plant Maintenance.

- Equipment Master is a repository of the standard information that one needs related to a specific piece of equipment.

- Equipment/Plant Maintenance provides a variety of reports to help us to review and manage information about our equipment and its maintenance.

- Plant Maintenance (PM) Reports are used to review and manage information about preventive maintenance schedules and service types within any maintenance organization.

Different PM reports are required to review PM information, such as:

- Status of service types for a piece of equipment;

- Maintenance messages;

- The frequency of occurrence for selected service types; and

- All equipment transactions.

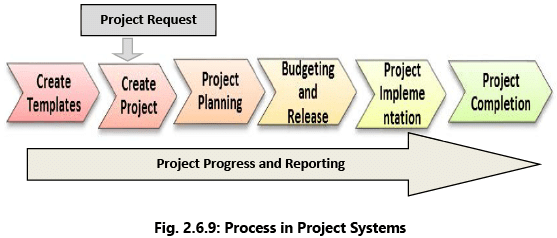

(i) Project Systems Module

This is an integrated project management tool used for planning and managing projects and portfolio management. It has several tools that enable project management process such as cost and planning budget, scheduling, requisitioning of materials and services, execution, until the project completion. Fig. 2.6.9 showing process in Project Systems.

Project System is closely integrated with other ERP modules like Logistics, Material Management, Sales and Distribution, Plant Maintenance, and Production Planning module etc. Before a project is initiated, it is required that project goal is clearly defined and the activities be structured. The Project Manager has a task to ensure that these projects are executed within budget and time and to ensure that resources are allocated to the project as per the requirement. In Project System, each process has a defined set of tasks to be performed known as process flow in Project Lifecycle. When a project request is received, a project is created and it undergoes the following steps in project process flow/lifecycle.

In Project System, each process has a defined set of tasks to be performed known as process flow in Project Lifecycle. When a project request is received, a project is created and it undergoes the following steps in project process flow/lifecycle.

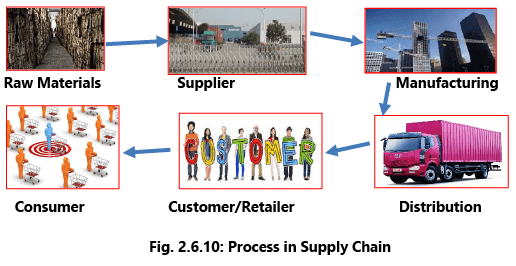

(j) Supply Chain Module

A Supply Chain is a network of autonomous or semi-autonomous business entities collectively responsible for procurement, manufacturing, and distribution activities associated with one or more families of related products. This module provides extensive functionality for logistics, manufacturing, planning, and analytics involving the activities like inventory, supply chain planning, supplier scheduling, claim processing, order entry, purchasing, etc. In other words, a supply chain is a network of facilities that procure raw materials, transform them into intermediate goods and then finished products, and then finally deliver the products to customers through a distribution system or a chain.

You can optimize your supply chain for months in advance; streamline processes such as supply network, demand, and material requirement planning; create detailed scheduling; refine production integration and maximize transportation scheduling. Fig. 2.6.10 showing process in supply chain. In Supply Chain Management System, any product which is manufactured in a company, first reaches directly from manufacturer to distributors where manufacturer sells the product to the distributor with some profit of margin. Distributors supply that product to retailer with his/her profit and then finally customers receive that product from retailer. This is called Supply Chain Management System which implies that a product reaches from manufacturer to customer through supply.

In Supply Chain Management System, any product which is manufactured in a company, first reaches directly from manufacturer to distributors where manufacturer sells the product to the distributor with some profit of margin. Distributors supply that product to retailer with his/her profit and then finally customers receive that product from retailer. This is called Supply Chain Management System which implies that a product reaches from manufacturer to customer through supply.

(k) Customer Relationship Management (CRM)

Customer Relationship Management is a system which aims at improving the relationship with existing customers, finding new prospective customers, and winning back former customers. This system can be brought into effect with software which helps in collecting, organizing, and managing the customer information. Information in the system can be accessed and entered by employees in different departments, such as sales, marketing, customer service, training, professional development, performance management, human resource development, and compensation. Details on any customer contacts can also be stored in the system. The rationale behind this approach is to improve services provided directly to customers and to use the information in the system for targeted marketing.

CRM manages the enterprise’s relationship with its customers. This includes determining who the high-value customers are and documenting what interactions the customers have had with the enterprise. Only large ERP packages have a CRM module. The CRM module uses the existing ERP tables as the source of its data. This is primarily the Contact, Customer, and Sales tables. CRM does not exchange transactions with other modules as CRM does not have transactions. Implementing a CRM strategy is advantageous to both small-scale and large-scale business ventures. Key benefits of a CRM module are as under.

- Improved customer relations: One of the prime benefits of using a CRM is obtaining better customer satisfaction. By using this strategy, all dealings involving servicing, marketing, and selling out products to the customers can be carried out in an organized and systematic way. Better services can be provided to customers through improved understanding of their issues and this in turn helps in increasing customer loyalty and decreasing customer agitation. In this way, continuous feedback from the customers regarding the products and services can be received. It is also possible that the customers may recommend the product to their acquaintances, when efficient and satisfactory services are provided.

- Increase customer revenues: By using a CRM strategy for any business, the revenue of the company can be increased. Using the data collected, marketing campaigns can be popularized in a more effective way. With the help of CRM software, it can be ensured that the product promotions reach a different and brand new set of customers, and not the ones who had already purchased the product, and thus effectively increase the customer revenue.

- Maximize up-selling and cross-selling: A CRM system allows up-selling which is the practice of giving customers premium products that fall in the same category of their purchase. The strategy also facilitates cross selling which is the practice of offering complementary products to customers, based on their previous purchases. This is done by interacting with the customers and getting an idea about their wants, needs, and patterns of purchase. The details thus obtained will be stored in a central database, which is accessible to all company executives. So, when an opportunity is spotted, the executives can promote their products to the customers, thus maximizing up-selling and cross selling.

- Better internal communication: Following a CRM strategy helps in building up better communication within the company. The sharing of customer data between different departments will enable them to work as a team. This is better than functioning as an isolated entity, as it will help in increasing the company’s profitability and enabling better service to customers.

- Optimize marketing: CRM enables to understand the customer needs and behavior in a better way, thereby allowing any enterprise to identify the correct time to market its product to the customers. CRM will also give an idea about the most profitable customer groups, and by using this information, similar prospective groups, at the right time will be targeted. In this way, marketing resources can be optimized efficiently and time is not wasted on less profitable customer groups.

Integration with Other Modules

Any ERP System is like a human body. There are different units and each unit relates to another units. All the units must work in harmony with other units to generate desired result. Following points are important for integration of modules with Financial and Accounting System:

- Master data across all the modules must be same and must be shared with other modules where-ever required.

- Common transaction data must be shared with other modules where-ever required.

- Separate voucher types to be used for each module for easy identification of department recording it.

- Figures and transaction may flow across the department, e.g. closing stock value is taken to Trading Account as well as Balance Sheet. Correct closing stock value is dependent on two things, complete and correct accounting of inventory transactions and appropriate method of valuation of closing stock. Closing stock quantity is required by Purchase Department, Stores Department, Accounts Department, and Production Department, Similarly, salary figures are used by Human Resource Department and Accounts Department simultaneously. Hence, it is necessary to design the system accordingly.

I. Integration Points

Some of the points regarding integration with other modules are discussed here.

(i) Material Management Integration with Finance and Controlling (FICO)

It is integrated in the area like Material Valuation, Vendor payments, Material costing etc. Whenever any inventory posting is done, it updates the General Ledger (G/L) accounts online in the background. Logistics invoice verification will create vendor liability in vendor account immediately on posting the document. Any advance given against the purchase order updates the Purchase Order history. For every inventory posting, there is corresponding Controlling document to update profit centre accounting reporting.

(ii) Human Resource Module Integration with Finance and Controlling

Attendance and leave record is used for calculation of salary on monthly basis. Salary is also a part of financial accounting. Hence salary processed and calculated by Human Resource Module shall be integrated with Finance & Controlling Module.

(iii) Material Management Integration with Production Planning (PP)

It is integrated in the areas like Material Requirement Planning, Receipts/issues against production orders, Availability check for stocks etc. Material requirement Planning is based on Stocks, expected receipts, expected issues. It generates planned orders or purchase requisitions which can be converted to purchase orders/Contracts. Inventory Management is responsible for staging of the components required for production orders. The receipt of the finished products in the Warehouse is posted in Inventory Management.

(iv) Material Management Integration with Sales and Distribution (SD)

It is integrated in the areas like Delivery, Availability Check, Stock transfers requirements etc. As soon as a sales order is created, it can initiate a dynamic availability check of stocks on hand. When the delivery is created, the quantity to be delivered is marked as “Scheduled for delivery”. It is deducted from the total stock when the goods issue is posted. Purchase order can be directly converted to delivery for a stock transfer requirement.

(v) Material Management Integration with Quality Management (QM)

It is integrated with QM for Quality inspection at Goods Receipt, In-process inspection etc. In the case of a goods movement, the system determines whether the material is subject to an inspection operation. If so, a corresponding activity is initiated for the movement in the Quality Management system. Based on quality parameters vendor evaluation is done.

(vi) Material Management Integration with Plant Maintenance (PM)

The material/service requirement is mentioned in Maintenance order. This leads to generation of Purchase Requisition. This PR will be converted to Purchase Order by MM. The goods for a PO will be in warded to Maintenance by MM. The spares which were reserved for maintenance order will be issued by MM against the reservation number.

Example 7: Let us consider a case of an ice-cream manufacturing company to see various examples of ERP modules.

A. Material Management Module

(a) Placing a purchase order for purchase of raw material like milk, dry fruits, milk powder, butter, essence, sugar, etc. on an approved vendor.

(b) Received raw material at stores.

B. Production Module

(a) Seeking raw material from stores.

(b) Converting raw material into WIP and WIP into finished goods.

(c) Sending the finished goods to cold room.

C. Supply Chain Module

(a) Distributing finished goods, i.e. ice cream to the customers.

(b) Keeping a track of all deliveries.

(c) Planning and scheduling of all deliveries.

D. Finance & Accounting

(a) Recording of all financial transactions.

(b) Payments to vendors.

(c) Collections from customers.

E. Human Resource Module

(a) Keeping record of all human resource related activities.

(b) Attendance, leave, salary calculations, joining and leaving of employees.

F. Sales & Distribution

(a) Performing pre-sales activities.

(b) Recording sales orders.

(c) Keeping track of all customer related transactions till collection against invoices.

study material

,mock tests for examination

,Sample Paper

,ppt

,past year papers

,Semester Notes

,Financial & Accounting Systems: Notes (Part - 2) | Financial Management & Strategic Management for CA Intermediate

,Extra Questions

,Free

,Exam

,Viva Questions

,practice quizzes

,MCQs

,Important questions

,Previous Year Questions with Solutions

,Summary

,Financial & Accounting Systems: Notes (Part - 2) | Financial Management & Strategic Management for CA Intermediate

,Objective type Questions

,video lectures

,shortcuts and tricks

,Financial & Accounting Systems: Notes (Part - 2) | Financial Management & Strategic Management for CA Intermediate

;

Financial & Accounting Systems: Notes (Part - 2) Free PDF Download

Importance of Financial & Accounting Systems: Notes (Part - 2)

Financial & Accounting Systems: Notes (Part - 2)

Financial & Accounting Systems: Notes (Part - 2) CA Intermediate Questions

Study Financial & Accounting Systems: Notes (Part - 2) on the App

|

© EduRev

|

Education Revolution

|

|