Worksheet: Production and Costs- 1 | Economics Class 11 - Commerce PDF Download

| Table of contents |

|

| Multiple Choice Questions |

|

| Match the Following |

|

| True or False |

|

| Very Short Answers |

|

| Short Answers |

|

| Long Answers |

|

Multiple Choice Questions

Q1: Which of the following is NOT a factor of production?

(a) Land

(b) Money

(c) Labor

(d) Entrepreneurship

Q2: What is the primary goal of production in economics?

(a) Maximizing Costs

(b) Maximizing Profits

(c) Minimizing Labor

(d) Minimizing Production

Q3: Which cost remains constant regardless of the level of production?

(a) Variable Cost

(b) Total Cost

(c) Fixed Cost

(d) Marginal Cost

Q4: What does the Law of Diminishing Marginal Returns state?

(a) Marginal cost decreases as production increases

(b) Marginal cost remains constant as production increases

(c) Marginal cost increases as production increases

(d) Marginal cost is unrelated to production

Q5: Which market structure is characterized by a large number of sellers and buyers, similar products, and easy entry and exit?

(a) Monopoly

(b) Oligopoly

(c) Perfect Competition

(d) Monopolistic Competition

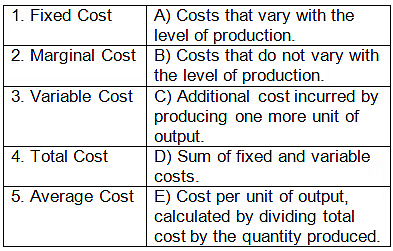

Match the Following

Q1: Match the production term with its corresponding definition:

True or False

Q1: Total cost is the sum of fixed and variable costs.

Q2: Marginal cost is the change in total cost when one more unit is produced.

Q3: Average variable cost decreases as production increases.

Q4: Economic costs include both explicit and implicit costs.

Q5: In perfect competition, firms have control over the market price.

Very Short Answers

Q1: Define Production Function.

Q2: What is Economies of Scale?

Q3: Explain Opportunity Cost.

Q4: Differentiate between Fixed Costs and Variable Costs.

Q5: What is a Production Possibility Curve?

Short Answers

Q1: Explain the Law of Diminishing Marginal Returns.

Q2: Discuss the Relationship between Average Cost and Marginal Cost.

Q3: Explain the Concept of Break-Even Point.

Q4: Discuss the Characteristics of Perfectly Competitive Markets.

Q5: Explain the Concept of Short-Run and Long-Run Production.

Long Answers

Q1: Discuss the Factors Influencing Production Decisions.

Q2: Explain the Concept of Economies and Diseconomies of Scale.

Q3: Discuss the Role of Production Function in Business Decision-Making.

Q4: Explain the Concept of Opportunity Cost with Examples.

Q5: Discuss the Impact of Production Costs on Pricing Strategies.

You can access the solutions to this worksheet here.

|

59 videos|222 docs|43 tests

|

FAQs on Worksheet: Production and Costs- 1 - Economics Class 11 - Commerce

| 1. What are fixed costs in production? |  |

| 2. How are variable costs different from fixed costs? | |

| 3. What is the total cost of production? | |

| 4. How do economies of scale affect production costs? | |

| 5. How can a firm minimize production costs? | |

Worksheet: Production and Costs- 1 | Economics Class 11 - Commerce

,Sample Paper

,practice quizzes

,study material

,MCQs

,past year papers

,Viva Questions

,Objective type Questions

,Important questions

,Previous Year Questions with Solutions

,video lectures

,mock tests for examination

,Semester Notes

,Worksheet: Production and Costs- 1 | Economics Class 11 - Commerce

,Summary

,Exam

,Worksheet: Production and Costs- 1 | Economics Class 11 - Commerce

,Free

,shortcuts and tricks

,Extra Questions

,ppt

;

Worksheet: Production and Costs- 1 Free PDF Download

Importance of Worksheet: Production and Costs- 1

Worksheet: Production and Costs- 1 Notes

Worksheet: Production and Costs- 1 Commerce Questions

Study Worksheet: Production and Costs- 1 on the App

|

© EduRev

|

Education Revolution

|

|