Best Study Material for CA Foundation Exam

CA Foundation Exam > CA Foundation Notes > Accounting for CA Foundation > Chapter Notes- Unit 2: Ledgers

Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation PDF Download

| Table of contents |

|

| Introduction |

|

| Specimen of Ledger Accounts |

|

| Posting |

|

| Balancing an Account |

|

| Summary |

|

Introduction

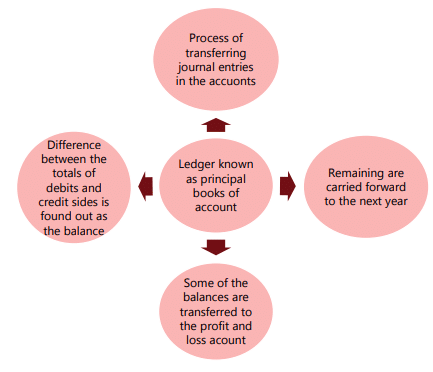

Once the initial transactions are recorded in the journal, these entries are classified and arranged by preparing accounts. The book that encompasses all categories of accounts (including personal, real, and nominal accounts) is known as the Ledger. It is acknowledged as the primary book of accounts where the balance for each account is determined.

Specimen of Ledger Accounts

A ledger account consists of two sides: the debit side (left) and the credit side (right). Each side contains four columns: (i) Date, (ii) Particulars, (iii) Journal folio, which indicates the page from which the entries are sourced for posting, and (iv) Amount.

Question for Chapter Notes- Unit 2: Ledgers

Try yourself:

Which columns are included in a ledger account?View Solution

Posting

The act of moving debit and credit entries from the journal to categorized accounts in the ledger is referred to as posting.

|

Test: Ledgers - 2

|

Start Test |

Start Test

Rules regarding Posting of Entries in the Ledger

- A separate account is created in the ledger book for each unique account, and entries from the Journal are transferred to the corresponding account accordingly. It is customary to use the terms ‘To’ and ‘By’ when recording transactions in the ledger.

- The term ‘To’ is found in the specific column for accounts listed on the debit side, while ‘By’ appears with accounts noted in the credit column.

- These terms ‘To’ and ‘By’ do not carry intrinsic meanings but are used to indicate the account that is debited and credited. The account that is debited in the journal must also be debited in the ledger, referencing the respective credit account.

Balancing an Account

- At the conclusion of each month, year, or designated reporting period, it may be necessary to determine the balance in an account. For instance, if an individual has purchased goods worth ₹1,000 but has only paid ₹850, they owe ₹150, which represents the balance in their account. To find the balance in any account, both sides of the account are totaled, and the smaller amount is subtracted from the larger amount to find the difference. If the credit side exceeds the debit side, it indicates a credit balance, and vice versa. The credit balance is recorded on the debit side as "To Balance c/d"; "c/d" signifies "carried down."

- This adjustment ensures that both sides are equal. The totals are then displayed on both sides opposite one another. The credit balance is noted on the credit side as "By balance b/d" (meaning brought down). This signifies the opening balance for the new period. Similarly, a debit balance is recorded on the credit side as "By Balance c/d," with the totals written on both sides as previously mentioned, and then the debit balance is placed on the debit side as "To Balance b/d," marking the opening balance for the new period. It is important to note that nominal accounts do not carry a balance; their end balances are transferred to the profit and loss account.

- Only the balances of personal and real accounts are ultimately reflected in the balance sheet at the end of the accounting period. The capital account is adjusted for profit or loss (i.e., net of nominal accounts) at the period's end.

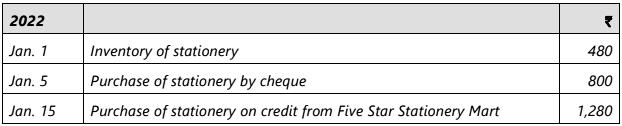

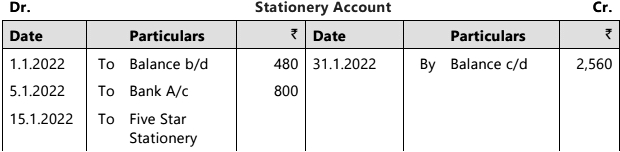

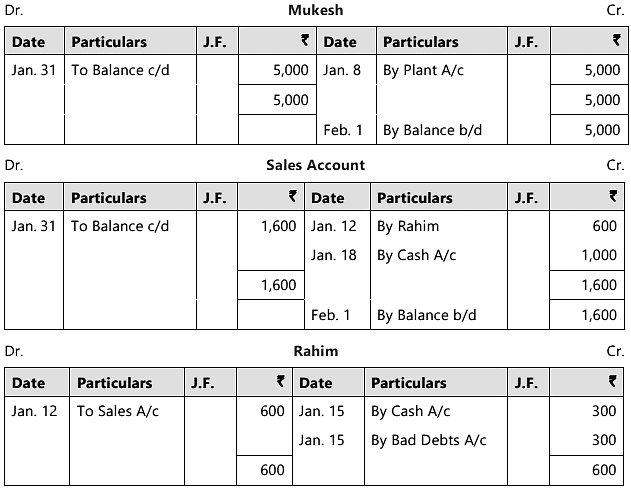

Illustration 1: Prepare the Stationery Account of a firm for the month of Jan. 2022 duly balanced off, from the following details:

Sol:

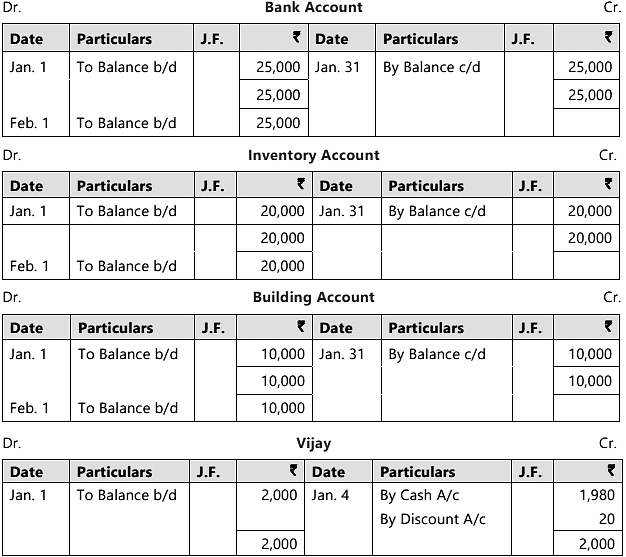

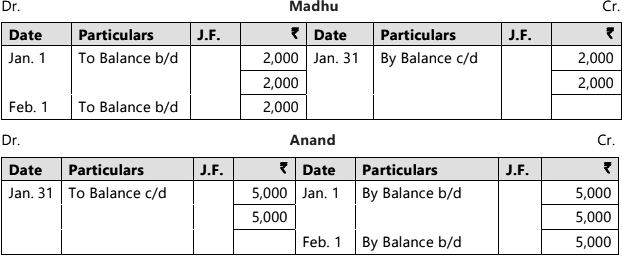

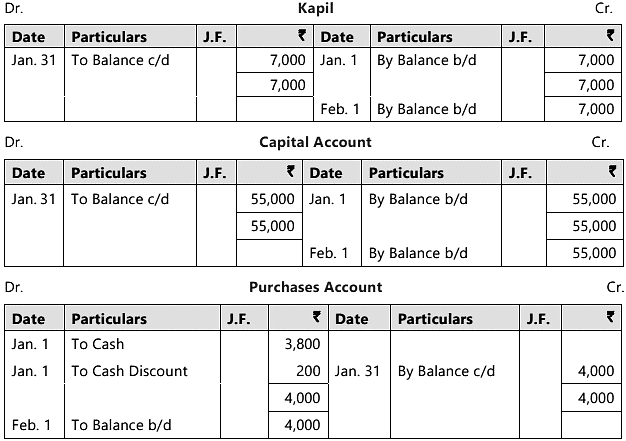

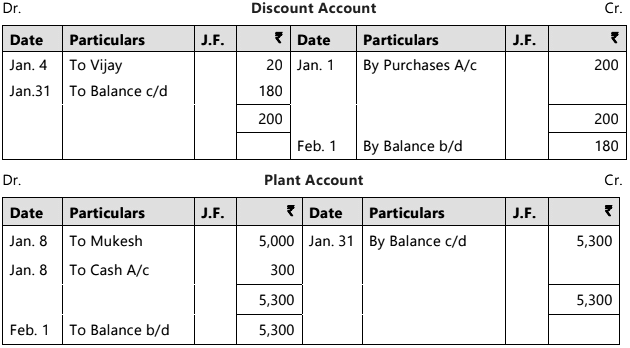

Illustration 2: Prepare the ledger accounts on the basis of following transactions in the books of a trader.

Debit Balances on January 1, 2022:

Cash in Hand ₹ 8,000, Cash at Bank ₹ 25,000, inventory of Goods ₹ 20,000, Building ₹ 10,000. Trade receivables: Vijay ₹ 2,000 and Madhu ₹ 2,000.

Credit Balances on January 1, 2022:

Trade payables: Anand ₹ 5,000 and Kapil ₹7,000, Capital ₹ 55,000

Following were further transactions in the month of January, 2022:

Jan. 1 Purchased goods worth ₹ 5,000 (payable at later date) for cash less 20% trade discount and 5% cash discount.

Jan. 4 Received ₹ 1,980 from Vijay and allowed him ₹ 20 as discount.

Jan. 8 Purchased plant from Mukesh for ₹5,000 and paid ₹100 as cartage for bringing the plant to the factory and another ₹200 as installation charges.

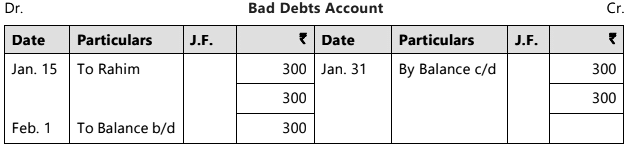

Jan. 12 Sold goods to Rahim on credit ₹600.

Jan. 15 Rahim became insolvent and could pay only 50 paise in a rupee.

Jan. 18 Sold goods to Ram for cash ₹1,000.

Sol:

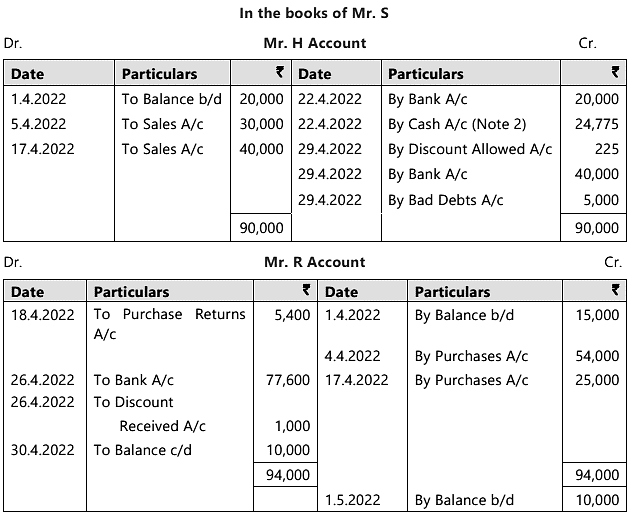

Illustration 3: The following data is given by Mr. S, the owner, with a request to compile only the two personal accounts of Mr. H and Mr. R, in his ledger, for the month of April, 2022.

1 Mr. S owes Mr. R ₹ 15,000; Mr. H owes Mr. S ₹ 20,000.

4 Mr. R sold goods worth ₹ 60,000 @ 10% trade discount to Mr. S.

5 Mr. S sold to Mr. H goods prices at ₹ 30,000.

17 Record a purchase of ₹ 25,000 net from R, which were sold to H at a profit of ₹15,000.

18 Mr. S rejected 10% of Mr. R’s goods of 4th April.

19 Mr. S issued a cash memo for ₹10,000 to Mr. H who came personally for this consignment of goods, urgently needed by him.

22 Mr. H cleared half his total dues to Mr. S, enjoying a ½% cash discount (of the payment received, ₹ 20,000 was by cheque).

26 R’s total dues (less ₹10,000 held back) were cleared by cheque, enjoying a cash discount of ₹1,000 on the payment made.

29 Close H’s Account to record the fact that all but ₹ 5,000 was cleared by him, by a cheque, because he was declared bankrupt.

30 Balance R’s Account.

Sol:

Working Notes:

- Sale of ₹ 10,000 on 19th April is a cash sales, therefore, it will not be recorded in the Personal Account of Mr. H; and

- On 22nd April, Mr. H owes Mr. S ₹ 90,000, amount paid by Mr. H ½ of ₹ 90,000 less½% discount i.e., ₹ 45,000– ₹ 225 = ₹ 44,775. Out of this amount, ₹ 20,000 paid by cheque and the balance of ₹ 24,775 in cash.

Note:

The balances of all nominal accounts are shifted to the Profit and Loss account during the preparation of financial statements, as nominal accounts represent revenues/incomes/gains or expenses/losses. Consequently, the overall outcome of all nominal accounts is represented in the Profit and Loss account for an accounting period, which is then transferred to the Capital Account. The balances of all accounts related to assets and liabilities (both personal and real) are shown in the Balance Sheet at the conclusion of the accounting period.

|

Download the notes

Chapter Notes- Unit 2: Ledgers

|

Download as PDF |

Download as PDF

Summary

- The process of moving journal entries to the accounts opened in the Ledger is referred to as posting.

- The Ledger serves as the primary accounting book and offers comprehensive details about all financial transactions related to each individual account.

- The balance is determined by calculating the difference between the totals of the debit and credit sides. Some of these balances (specifically nominal accounts) are transferred to the profit and loss account, while others are carried over to the next period/year, as reflected in the balance sheet, depending on the type of account.

The document Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation is a part of the CA Foundation Course Accounting for CA Foundation.

All you need of CA Foundation at this link: CA Foundation

|

68 videos|160 docs|83 tests

|

FAQs on Unit 2: Ledgers Chapter Notes - Accounting for CA Foundation

| 1. What is a ledger account in accounting? |  |

| 2. How do you post transactions to a ledger account? | |

Ans. To post transactions to a ledger account, you first record the transaction in the journal, which includes the date, account titles, and amounts. Then, you transfer this information to the corresponding ledger accounts by debiting one account and crediting another, ensuring that the double-entry accounting principle is maintained.

| 3. What is the process of balancing a ledger account? | |

Ans. Balancing a ledger account involves calculating the total debits and credits for that account. You subtract the smaller total from the larger one to find the balance. This balance is then recorded in the ledger, ensuring that it reflects the current financial position of the account.

| 4. Why is it important to maintain accurate ledger accounts? | |

Ans. Maintaining accurate ledger accounts is crucial because they provide a clear and organized record of all financial transactions. This accuracy is essential for preparing financial statements, ensuring compliance with accounting standards, and facilitating effective financial analysis and decision-making.

| 5. What are the key components of a ledger account format? | |

Ans. The key components of a ledger account format include the account title, date, details/description of the transaction, debit column, credit column, and the balance carried forward. Each transaction is recorded in a systematic manner to ensure clarity and accuracy.

Related Exams

About this Document

4.68/5

Rating

Apr 19, 2025

Last updated

Document Description: Chapter Notes- Unit 2: Ledgers for CA Foundation 2025 is part of Accounting for CA Foundation preparation.

The notes and questions for Chapter Notes- Unit 2: Ledgers have been prepared according to the CA Foundation exam syllabus. Information about Chapter Notes- Unit 2: Ledgers covers topics

like Introduction, Specimen of Ledger Accounts, Posting, Balancing an Account, Summary and Chapter Notes- Unit 2: Ledgers Example, for CA Foundation 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Chapter Notes- Unit 2: Ledgers.

Introduction of Chapter Notes- Unit 2: Ledgers in English is available as part of our Accounting for CA Foundation

for CA Foundation & Chapter Notes- Unit 2: Ledgers in Hindi for Accounting for CA Foundation course.

Download more important topics related with notes, lectures and mock test series for CA Foundation

Exam by signing up for free. CA Foundation: Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation

Description

Full syllabus notes, lecture & questions for Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation - CA Foundation | Plus excerises question with solution to help you revise complete syllabus for Accounting for CA Foundation | Best notes, free PDF download

Information about Chapter Notes- Unit 2: Ledgers

In this doc you can find the meaning of Chapter Notes- Unit 2: Ledgers defined & explained in the simplest way possible. Besides explaining types of

Chapter Notes- Unit 2: Ledgers theory, EduRev gives you an ample number of questions to practice Chapter Notes- Unit 2: Ledgers tests, examples and also practice CA Foundation

tests

Related Searches

Viva Questions

,practice quizzes

,Objective type Questions

,study material

,past year papers

,Free

,Sample Paper

,Summary

,Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation

,Previous Year Questions with Solutions

,Exam

,Extra Questions

,mock tests for examination

,Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation

,Unit 2: Ledgers Chapter Notes | Accounting for CA Foundation

,Important questions

,MCQs

,ppt

,video lectures

,shortcuts and tricks

,Semester Notes

;

Additional Information about Chapter Notes- Unit 2: Ledgers for CA Foundation Preparation

Chapter Notes- Unit 2: Ledgers Free PDF Download

The Chapter Notes- Unit 2: Ledgers is an invaluable resource that delves deep into the core of the CA Foundation exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Chapter Notes- Unit 2: Ledgers now and kickstart your journey towards success in the CA Foundation exam.

Importance of Chapter Notes- Unit 2: Ledgers

The importance of Chapter Notes- Unit 2: Ledgers cannot be overstated, especially for CA Foundation aspirants.

This document holds the key to success in the CA Foundation exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Chapter Notes- Unit 2: Ledgers

Chapter Notes- Unit 2: Ledgers Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Chapter Notes- Unit 2: Ledgers.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Chapter Notes- Unit 2: Ledgers Notes on EduRev are your ultimate resource for success.

Chapter Notes- Unit 2: Ledgers CA Foundation Questions

The "Chapter Notes- Unit 2: Ledgers CA Foundation Questions" guide is a valuable resource for all aspiring students preparing for the

CA Foundation exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Chapter Notes- Unit 2: Ledgers on the App

Students of CA Foundation can study Chapter Notes- Unit 2: Ledgers alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Chapter Notes- Unit 2: Ledgers,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Chapter Notes- Unit 2: Ledgers is prepared as per the latest CA Foundation syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup