UPSC Exam > UPSC Notes > Economics Optional Notes for UPSC > Keynes's Theory on Demand for Money

Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC PDF Download

Introduction

- The question to be asked in full is why is money demanded when money does not earn its holders any income whereas there are competing non-money financial assets in the economy which yield some income to their holders?

- One general answer can be that money yields its holders conveniences yield of non-pecuniary nature. This yield is rooted in the peculiar characteristic of money as the only generally acceptable means of payment, and so it’s perfect liquidity.

More concretely, Keynes said that money was demanded due to three main motives:

(i) The transactions motive,

(ii) The precautionary motive and

(iii) The speculative motive.

- Ever since this threefold classification of motives has become standard stock-in-trade of monetary economists. Later efforts to add other motives such as the finance motive by Keynes (1937) and Robertson (1938) and the diversification motive by Gurley and Shaw (1960) have not been successful.

- The three motives and corresponding demands for money are explained briefly first, to be followed by somewhat extended discussion of the individual components of the demand for money. The transactions motive gives rise to the transactions demand for money which refers to the demand for cash of the public for making current transactions of all kinds. This is inextricably bound with the use of money as the medium of exchange in a money-exchange economy.

- The precautionary motive induces the public to hold money to provide for contingencies requiring sudden expenditure and for unforeseen opportunities of advantageous purchase. This motive (demand) is a product of uncertainties of all kinds. The speculative motive giving rise to the speculative demand for money is the most important contribution Keynes made to the theory of the demand for money.

- It explains why the public may hold surplus cash (over and above that demanded due to the other two motives) in the face of interest- earning bonds (and other financial assets). The reason is that the holders of such speculative balances may anticipate such fall in future prices as will make the loss of foregone interest earnings look relatively smaller.

- So they wait with cash for bond prices to fall, avoid expected capital losses, and switch into bonds when the anticipated bond prices have been realized. The speculative demand for money is sometimes also called the asset demand for money—not a happy term, because, money being an asset, the entire demand for it is an asset demand.

- Related to the above is the distinction between active and idle balances made in the Keynesian literature. The active balances are defined as balances used as means of payments in national income- generating transactions. The rest are called idle balances. The distinction is useful to explain how changes in’ the income velocity of money come about and how the same quantity of money can support higher or lower levels of money expenditure when idle balances are converted into active balances or vice versa.

Question for Keynes's Theory on Demand for MoneyTry yourself: What are the three main motives for demanding money according to Keynes?View Solution

The Determinants of the Demand for Money

- Keynes made the demand for money a function of two variables, namely income (Y) 4 and the rate of interest (r). Being a Cambridge economist, Keynes retained the influence of the Cambridge approach to the demand for money under which Md is hypothesised to be a function of Y. But he argued that this explained only the transactions and the precautionary demand for money, and not the entire demand for money.

- The truly novel and revolutionary element of Keynes’ theory of the demand for money is the component of the speculative demand for money. Through it Keynes made (a part of) the demand for money a declining function of the rate of interest, the latter a purely monetary phenomenon and the sole carrier of monetary influences in the economy. Thus the speculative demand for money constitutes the main pillar of Keynes’ revolution in monetary theory and Keynes’ attack on the quantity theory of money. This is explained below.

- The speculative demand for money arises from the speculative motive for holding money. The latter arises from the variability of interest rates in the market and uncertainty about them. For simplicity Keynes -assumed that perpetual bonds are the only non-money financial asset in the economy, which compete with money in the asset portfolio of the public.

- Money does not earn its holders any interest income, but its capital value in terms of itself is always fixed. Bonds, on the other hand, yield interest income to their holders. But this income can be more than wiped out if bond prices fall in future. It can be shown algebraically that the price of a (perpetual) bond is given by the reciprocal of the market rate of interest times the coupon rate of interest.

- Suppose the coupon rate (i.e. interest payable on a bond) is Re 1 per year and the market rate f interest is 4 per cent per year. Then the market (price of the bond will) be Rs. 1/.04 X 1 = Rs. 25. If the market rate of interest rises to 5 per cent per year, the market price of the bond will fall to Rs. 1/.05 X I Rs. 20. Thus, bond price is seen as an inverse function of the rate interest.

- Economic units hold a part of their wealth in the form of financial assets. In the two-asset model of Keynes, these assets are money and (perpetual) bonds. Bond prices keep on changing from time to time. Therefore, they are subject to capital gains or losses. Thus, to a bond-holder the return from bond-holding per unit period (say a year) per Rs 1, is the rate of interest ± capital gain or loss per year, the time of making investment in bonds, the market rate of interest will be a given datum to an individual, but the future rate of interest or bond price, and so the expected rate of capital gain or loss will have to be anticipated. Hence the element of speculation in the bond market and as shown below, also in the money market.

- The speculators are of two kinds: bulls and bears. Bulls are those who expect the bond prices to rise in the future. Bears expect these prices to fall. In Keynes’ model, these expectations are assumed to be held with certainty. Bulls, then, are assumed to invest all their idle cash into bonds.

- Bears instead will move out of bonds into cash if their expected capital losses on bonds exceed interest income from bond-holding. Thereby they minimise their losses. Thus, the speculative demand for money arises only from bears. It is the demand for bearish hoards. These bears build up their cash balances to move into bonds when either bond prices have fallen as expected or when they come to expect that bond prices will rise in future.

- The above model implies an all-or-nothing behaviour on the part of individual asset holders. Either they are entirely into bonds (bulls) or entirely into cash (bears). That is, their portfolios are pure and not diversified.

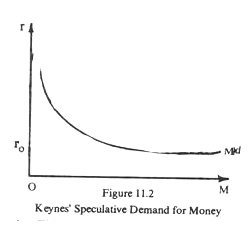

- To move to the aggregate speculative demand for money, Keynes assumed that different asset holders have different interest-rate expectations. Thus, at a certain very high rate of interest (and very low price of bonds), all may be bulls. Then, the speculative demand for money will be equal to hero. But at a lower rate of interest (higher bond price) some bulls will become bears and positive demand for speculative balances will emerge.

- At a still lower rate of interest (and still higher bond price), Tie more bulls will become bears and the speculative demand for higher still. Thus, Keynes derived a downward-sloping aggregate speculative demand curve for money with respect to the “a rate of interest, as shown in Figure 11.2.

Keynes also suggested the possibility of the existence of what is called the liquidity trap. This refers to a situation when at a certain rate of interest the (speculative) demand for money becomes perfectly elastic. This will come about when at that rate all the asset holders turn bears, so that none is willing to hold bonds and everyone wants to move into cash.

Keynes also suggested the possibility of the existence of what is called the liquidity trap. This refers to a situation when at a certain rate of interest the (speculative) demand for money becomes perfectly elastic. This will come about when at that rate all the asset holders turn bears, so that none is willing to hold bonds and everyone wants to move into cash.- In Figure 11.2, such a situation occurs at the rate of interest ro. Then, no amount of expansion of money-supply can lower the rate of interest further. The public is willing to hold the entire extra amount of money at ro. The extra liquidity created by the monetary authority gets trapped in the asset portfolios of the public without lowering r. The ro serves as the minimum r below which it cannot be lowered.

- Another element in Keynes’ theory of the speculative demand for money is the concept of the ‘normal’ rate of interest. Keynes postulated that at any moment there was a certain r which the asset holders regard as ‘normal’, as the r which will tend to prevail in the market under ‘normal conditions’. This ‘normal’ r acts as the benchmark with respect to which any actual r is judged as high or low.

- Differences of r expectations among asset holders then can be interpreted as differences about the level of the ‘normal’ r. The amount of money demanded for speculative purposes depends on the current level of r relative to this ‘normal’ r as seen by various individuals. If the latter changes, the quantity of money demanded at any particular r will also change.

- Since ‘normal’ r, or people’s expectation about it, cannot be taken as a time constant, Keynes argument implies that the relation between the demand for money and r will not be stable over time. This is an important result which has not been fully appreciated even by Keynes’ followers. It can be seen to damage Keynes’ own theory of the interest rate determination but more so the quantity theory of money and the effectiveness o monetary policy.

- Keynes’ micro theory of the speculative demand tor money has been called into question by Tobin (1958). It was noted above that for an individual Keynes’ explanation leads to a pure asset portfolio of either money or bonds. This is contrary to experience. In actual life mixed asset portfolios are the rule. Tobin’s alternative formulation yields such portfolios even at individual level. For this, unlike Keynes, he assumes that an individual does not hold his interest-rate expectations with certainty.

- Then liquidity preference is analysed as behaviour towards risk under uncertainty. Acting on uncertain interest-rate expectations means assuming some risk of capital loss. The degree of risk increases with every increase in the proportion of bonds in the asset portfolio. Normally, asset holders are risk averters, so that they will require a higher compensation (rate of interest) for undertaking higher risk.

- Thus, at a higher r more bonds and less money will be held in the portfolio and at a lower r less bonds and more money will be preferred. The result is a , diversified asset portfolio and a downward sloping asset demand curve for money with respect to r even at the micro level. On suitable assumptions, the aggregate asset demand for money is also shown as a declining function of r.

- Keynes’ theory of the speculative demand for money has also been criticised on the ground that it treats all non-money financial assets (NMFAs) as bonds. Such treatment is an unwarranted simplification, because a large number of such assets are unlike bonds in that their capital values are nominally fixed and do not vary (inversely) with r.

- In India, the examples of such NMFAs are fixed deposits with commercial banks, post offices, and public limited companies, national savings certificates, UTI units, etc. Substitution between them and money does not entail Keynes’ speculative motive, because they are not subject to variation in their nominal capital values. In their case, their rates of return influence as simple opportunity-cost variables without any element of speculation.

- Gurley and Shaw (1960) also do not favour keeping the Md function confined to a simple two-asset world. In their analysis of the effects of financial growth, exhibited by security differentiation and the growth of secondary securities, they have stressed the growing competition or asset substitution which money has to face from the NMFAs in the asset portfolios of wealth-holders.

- According to them, things being the same, this ever-growing asset substitution has to downward displacements of the demand for money, has made demand less stable, and made monetary policy less effective than before.

- Much systematic empirical work has not been done on these hypotheses. Most empirical studies on the demand for money have tended to ignore them. What little empirical work has been done for the USA (Fiege, 1964) does not lend definite support to the Gurley and Shaw hypotheses.

- After a fairly long detour, we come back to Keynes’ theory of the demand for money.

Keynes also suggested the possibility of the existence of what is called the liquidity trap. This refers to a situation when at a certain rate of interest the (speculative) demand for money becomes perfectly elastic. This will come about when at that rate all the asset holders turn bears, so that none is willing to hold bonds and everyone wants to move into cash.

Keynes also suggested the possibility of the existence of what is called the liquidity trap. This refers to a situation when at a certain rate of interest the (speculative) demand for money becomes perfectly elastic. This will come about when at that rate all the asset holders turn bears, so that none is willing to hold bonds and everyone wants to move into cash.Question for Keynes's Theory on Demand for MoneyTry yourself: According to Keynes' additive demand function for money, what does L1(Y) represent?View Solution

This is summed up in the following equation:

Md = L1(Y) + L(r). (11.3)

- It is an additive demand function with two separate components. L1(Y) represents the’ transactions and precautionary demand for money. Keynes made both an increasing function of the level of money income. In the Cambridge tradition, he tended to assume that L1(Y) had proportional form of the kind represented in Figure 11.1. The second component L 2 (r) represents the speculative demand for money, which, as shown above, Keynes argued to be a declining function of r. As shown in Figure 11.2, this relation was not assumed to be linear.

- Keynes’ additive form of the demand function for money of equation Md = L1(Y) + L(r). (11.3) has been discarded by Keynesians and other economists. It has been argued that money is one asset, not two, three, or many. The motives to hold it may be of any number. The same unit of money can serve all these motives. So the demand for it cannot be compartmenalised into separate components independent of each other.

- Also, as in Baumol-Tobin theory, the transactions demand for money also is interest elastic. The same can be argued for the precautionary demand for money too. The explanation of the speculative demand for money shows that this kind of demand will be an increasing function of total assets or wealth. If income is taken as a proxy for wealth, the speculative demand also becomes a function of both income and the rate of interest.

These arguments have led to the following revised form of the Keynesian demand function for money:

Md=L(Y,r), (11.4)

- where’ it is hypothesised that Md is an increasing function of Y and a declining function of r.

- The replacement of the simple Md function of equation Md = K Y, (11.1) by that of equation Md = L(Y,r), (11.4) has been the single most important revolution- any development in the field of monetary theory. It has also been the use of many battles between the neoclassical economists and the Keynesians. It has necessitated integration of value theory with monetary theory or of the real sector with the monetary sector, of which Hicks’ IS-LM model is a well-known example.

- This makes the simple quantity theory of money model suspect by making the income-velocity of money responsive to changes in the rate of interest. The latter changes can come about by any number of factors originating in the money market or the commodity market. Our main purpose in adding this paragraph to the text is to emphasise once again the importance of the demand function for money in monetary theory.

The document Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC is a part of the UPSC Course Economics Optional Notes for UPSC.

All you need of UPSC at this link: UPSC

|

66 videos|170 docs|74 tests

|

FAQs on Keynes's Theory on Demand for Money - Economics Optional Notes for UPSC

| 1. What is Keynes's theory on the demand for money? |  |

Ans. Keynes's theory on the demand for money states that individuals hold money for three main motives: transactional, precautionary, and speculative. The transaction motive refers to the need for money to facilitate day-to-day transactions, such as buying goods and services. The precautionary motive refers to the need for money to cover unexpected expenses or emergencies. The speculative motive refers to the desire to hold money as a store of value, anticipating future changes in interest rates or asset prices. According to Keynes, the demand for money is influenced by these three motives and is a key determinant of overall economic activity.

| 2. What are the determinants of the demand for money? | |

Ans. The determinants of the demand for money include income levels, interest rates, price levels, and the availability of alternative financial assets. As income levels increase, individuals tend to hold more money for transactions. Interest rates also play a significant role, as higher interest rates can incentivize individuals to hold less money and invest in other financial assets. Price levels can affect the demand for money indirectly by influencing the amount of money needed for transactions. If prices rise, individuals may need to hold more money to purchase the same goods and services. Finally, the availability of alternative financial assets, such as bonds or stocks, can also impact the demand for money as individuals may choose to hold these assets instead.

| 3. How does the demand for money affect overall economic activity? | |

Ans. The demand for money is a crucial factor in determining overall economic activity. When individuals and businesses demand more money, it indicates a higher level of economic transactions. This increased demand can stimulate economic growth and investment as businesses need to produce more goods and services to meet the demand. Conversely, a decrease in the demand for money may indicate a slowdown in economic activity, as individuals and businesses hold back on spending and investment. Therefore, policymakers closely monitor the demand for money to gauge the health and direction of the economy.

| 4. What is the transaction motive for holding money? | |

Ans. The transaction motive for holding money refers to the need to have money readily available to facilitate day-to-day transactions. This motive arises from the necessity to purchase goods and services, pay bills, and meet other financial obligations. Individuals and businesses hold money to ensure they have enough liquidity to engage in transactions without relying on credit or delayed payments. The transaction motive is influenced by factors such as income levels, price levels, and the frequency of transactions.

| 5. How does the speculative motive for holding money impact the demand for money? | |

Ans. The speculative motive for holding money refers to the desire to hold money as a store of value, anticipating future changes in interest rates or asset prices. When individuals expect interest rates to rise or asset prices to fall, they may choose to hold more money instead of investing in other financial assets. This increased demand for money reduces the overall demand for other assets and can impact interest rates and asset prices. Conversely, if individuals anticipate falling interest rates or rising asset prices, they may choose to hold less money and invest in alternative assets, leading to a decrease in the demand for money. The speculative motive thus influences the allocation of funds between money and other financial assets.

Related Exams

About this Document

|

Dec 25, 2024 Last updated |

Document Description: Keynes's Theory on Demand for Money for UPSC 2024 is part of Economics Optional Notes for UPSC preparation.

The notes and questions for Keynes's Theory on Demand for Money have been prepared according to the UPSC exam syllabus. Information about Keynes's Theory on Demand for Money covers topics

like Introduction, The Determinants of the Demand for Money and Keynes's Theory on Demand for Money Example, for UPSC 2024 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Keynes's Theory on Demand for Money.

Introduction of Keynes's Theory on Demand for Money in English is available as part of our Economics Optional Notes for UPSC

for UPSC & Keynes's Theory on Demand for Money in Hindi for Economics Optional Notes for UPSC course.

Download more important topics related with notes, lectures and mock test series for UPSC

Exam by signing up for free. UPSC: Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC

Description

Full syllabus notes, lecture & questions for Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC - UPSC | Plus excerises question with solution to help you revise complete syllabus for Economics Optional Notes for UPSC | Best notes, free PDF download

Information about Keynes's Theory on Demand for Money

In this doc you can find the meaning of Keynes's Theory on Demand for Money defined & explained in the simplest way possible. Besides explaining types of

Keynes's Theory on Demand for Money theory, EduRev gives you an ample number of questions to practice Keynes's Theory on Demand for Money tests, examples and also practice UPSC

tests

|

Explore Courses for UPSC exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

Related Searches

Extra Questions

,Important questions

,Summary

,Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC

,Exam

,practice quizzes

,past year papers

,Sample Paper

,Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC

,video lectures

,shortcuts and tricks

,mock tests for examination

,Semester Notes

,Keynes's Theory on Demand for Money | Economics Optional Notes for UPSC

,MCQs

,ppt

,study material

,Free

,Viva Questions

,Objective type Questions

,Previous Year Questions with Solutions

;

Additional Information about Keynes's Theory on Demand for Money for UPSC Preparation

Keynes's Theory on Demand for Money Free PDF Download

The Keynes's Theory on Demand for Money is an invaluable resource that delves deep into the core of the UPSC exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Keynes's Theory on Demand for Money now and kickstart your journey towards success in the UPSC exam.

Importance of Keynes's Theory on Demand for Money

The importance of Keynes's Theory on Demand for Money cannot be overstated, especially for UPSC aspirants.

This document holds the key to success in the UPSC exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Keynes's Theory on Demand for Money Notes

Keynes's Theory on Demand for Money Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Keynes's Theory on Demand for Money.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Keynes's Theory on Demand for Money Notes on EduRev are your ultimate resource for success.

Keynes's Theory on Demand for Money UPSC Questions

The "Keynes's Theory on Demand for Money UPSC Questions" guide is a valuable resource for all aspiring students preparing for the

UPSC exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Keynes's Theory on Demand for Money on the App

Students of UPSC can study Keynes's Theory on Demand for Money alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Keynes's Theory on Demand for Money,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Keynes's Theory on Demand for Money is prepared as per the latest UPSC syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup