Best Study Material for UGC NET Exam

UGC NET Exam > UGC NET Notes > UGC NET Commerce Preparation Course > Basic Concepts of Income Tax

Basic Concepts of Income Tax | UGC NET Commerce Preparation Course PDF Download

Income Tax Law

Income tax is a tax imposed on the total income of a taxpayer, defined as a person liable under this Act, for the relevant financial year. To comprehend the Income Tax law in India, one must carefully study the following components:

- Income-tax Act, 1961: This legislation governs the levy of income tax in India. Enacted on April 1, 1962, it consists of 298 sections and XIV schedules. The Act covers aspects like determining taxable income, tax obligations, assessment procedures, appeals, penalties, and prosecutions. It undergoes annual revisions through additions and deletions made by the Annual Finance Act passed by the Parliament.

- Annual Finance Acts: Each year, the Finance Minister introduces a Finance Bill during the Parliament's Budget Session. Upon approval by both Houses of Parliament and the President's assent, the Finance Bill transforms into the Finance Act. Amendments to the Income-tax Act, 1961, and other tax laws are incorporated through the Finance Act. The Finance Bill also specifies the Income tax rates and other tax details outlined in various schedules attached to it. Therefore, while the Income-tax Act remains a stable law, its practical application is determined by the Annual Finance Act.

- Income-tax Rules, 1962: Central Board of Direct Taxes (CBDT) oversees the administration of direct taxes and is authorized under section 295 of the Income Tax Act to create rules to facilitate the Act's objectives. These rules, collectively known as Income-tax Rules, 1962, were initially established in 1962 to ensure the proper implementation of the Income-tax Act, 1961. It is crucial to understand these rules in conjunction with the Income-tax Act, 1961.

The authority to formulate rules under this section includes the ability to apply them retrospectively, starting from the Act's commencement date. However, any retrospective application should not unfairly prejudice the interests of taxpayers. - Circulars and Notifications: Circulars are periodically issued by the CBDT to address specific issues and clarify uncertainties related to the provisions of the Income Tax Act. These circulars serve as guidance for officers and taxpayers. While binding on the department, they do not hold the same weight for taxpayers, who can benefit from favorable circulars.

Notifications, on the other hand, are released by the Central Government to enforce the Act's provisions. For instance, under section 10(15)(iv)(h), the Central Government exempts interest on bonds and debentures subject to specified conditions through notifications. Additionally, the CBDT has the authority to establish and modify rules through notifications, such as prescribing guidelines for skill development projects under section 35CCD. - Judicial decisions:

- Significance: Judicial decisions play a crucial role in interpreting income tax laws as they fill gaps left by legislation.

- Supreme Court rulings: Decisions made by the Supreme Court are binding across the nation and establish legal precedents.

- High Court rulings: Decisions by High Courts apply within the states where the respective High Courts have jurisdiction.

Charge of Income-tax: [Sec. 4]

Taxation in India is authorized by law, particularly through Section 4 of the Income-tax Act, 1961, granting the Central Government the power to levy income tax. This pivotal section outlines the following key points:

- Tax Rates: Tax rates for each year are set by the Annual Finance Act.

- Entities Taxed: Every individual specified under section 2(31) is subject to taxation.

- Income Tax Basis: Tax is based on the total income earned during the previous year, not the assessment year, with exceptions noted in sections 172, 174, 174A, 175, and 176.

- Compliance: Taxation must adhere to the provisions outlined in the Act.

Section 4 is foundational in income tax law, as it is the primary provision from which a person’s tax liability originates.

Question for Basic Concepts of Income Tax

Try yourself:

Which authority is responsible for issuing circulars to provide guidance on income tax laws?View Solution

Assessment Year

Assessment year is a 12-month period starting on 1st April every year. It is the year in which the total income earned in the previous year is taxed. For example, income earned in the previous year 2022-23 is taxed in the assessment year 2023-24 (1.4.2023 to 31.3.2024).

Previous Year

The previous year is the year in which income is earned. It is the financial year immediately before the assessment year. Taxes on income earned in the previous year are paid in the assessment year. All taxpayers follow a consistent previous year, starting from 1st April to 31st March.

Person: [Sec. 2(31)]

Income tax is imposed on the total income of the previous year of every 'person.' It's crucial to understand who falls under the term 'Person.' Here are the seven categories:

- Individual

- Hindu Undivided Family (HUF)

- Company

- Firm

- Association of Persons (AoP) or Body of Individuals (BoI), whether incorporated or not

- Local authority

- Artificial juridical person not fitting into the above categories, like a university or deity

According to Explanation to Sec. 2(31), an AoP/BoI/Local authority or any artificial juridical person is considered a 'person,' regardless of whether they were formed for profit-making purposes or not.

Question for Basic Concepts of Income Tax

Try yourself:

Who falls under the category of 'Person' for income tax purposes?View Solution

Assessee: [Sec. 2(7)]

Assessee refers to a person who is liable to pay any tax or sum of money under the relevant tax laws. It encompasses the following categories:

Categories of Assessee:

- Every individual subject to a tax assessment procedure under this Act is considered an assessee. This includes situations where the assessment of their income is being carried out.

- Any person recognized as an assessee as per the provisions of this Act. This extends to cases where an individual is responsible for the income of another person, like the legal representative of a deceased individual.

- Any individual categorized as an assessee in default according to the Act. For instance, if a person is obligated to deduct tax at the source but fails to do so or does not remit the deducted tax to the government, they are considered an assessee in default.

Principles relating to Income under Income-tax Act

The following are important principles relating to income:

- Income generally refers to revenue receipts. However, under the Income-tax Act, 1961, certain capital receipts like capital gains from the sale of assets such as land are also considered as income.

- For tax purposes, income is considered as net receipts, not gross receipts. Net receipts are calculated by deducting the expenses related to earning such receipts.

- Income can be taxable either on a due basis or a receipt basis, as specified under the respective head of income.

- When computing income under the heads 'Profits and gains of business or profession' and 'Income from other sources', the accounting method regularly followed by the taxpayer should be considered, which can be either the cash system or mercantile system.

- Income earned during the year (previous year) is chargeable to tax in the next year (assessment year). For example, income from the Previous Year 2022-23 will be taxed in the Assessment Year 2023-24.

- There are exceptions to the above principle known as Accelerated assessments under sections 172, 174, 174A, and 175, which are discussed in the chapter 'Liability in Special Cases'.

Income: [Sec. 2(24)]

The definition of 'Income' under section 2(24) is broad and non-exhaustive, meaning certain items may be considered as income based on their general meaning, even if they are not specifically listed. The term 'Income' includes:

- Profits and gains

- Dividends

- Voluntary contributions to trusts for charitable or religious purposes, or to educational institutions, hospitals, or electoral trusts

- Perquisites or profits in lieu of salary taxable under section 17

- Special allowances for office or employment duties

- Benefits or perquisites received by directors or persons with substantial interest in a company

- Benefits or perquisites to a trustee or representative assessee

- Sums chargeable under sections 28, 41, and 59

- Capital gains taxable under section 45

- Profits from insurance businesses or co-operative societies

- Winnings from lotteries, games, gambling, or betting

- Contributions received from employees for provident or welfare funds

- Amounts received from Keyman insurance policies

- Certain sums taxable under section 56(2)

- Money or property received without consideration as per section 56(2)(vii) or (via)

- Consideration from share issues exceeding fair market value under section 56(2)(viib)

- Forfeited advances from capital asset negotiations

- Compensation or payments referred to in section 56(2)(xi)

- Assistance in the form of subsidies, grants, or reimbursements from the government, except those covered under section 43(1) or for the corpus of a trust established by the government.

Question for Basic Concepts of Income Tax

Try yourself:

Which of the following items is considered as income under the Income-tax Act?View Solution

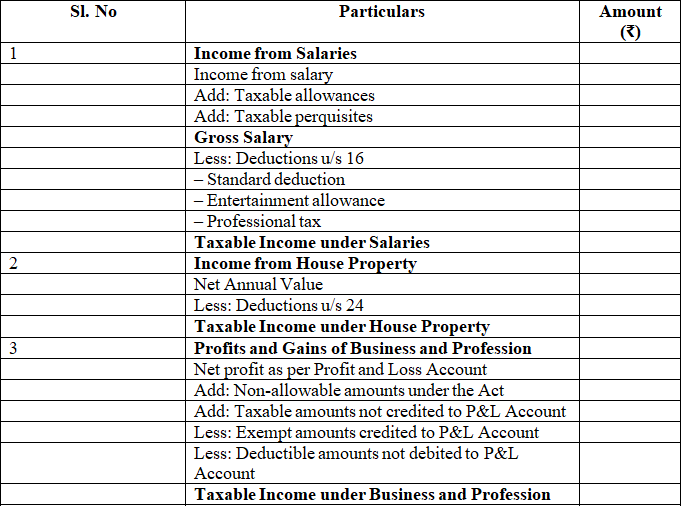

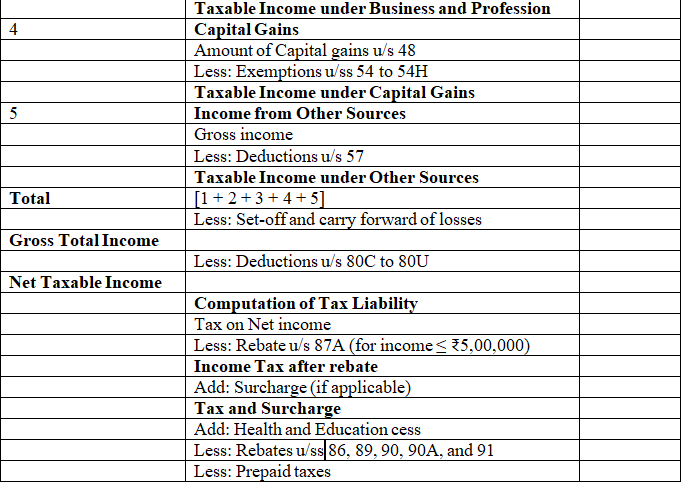

Heads of Income

- Salaries: Covered under Sections 15 to 17 of the Income-tax Act, 1961.

- Income from House Property: Regulated by Sections 22 to 27.

- Profits and Gains of Business or Profession: Governed by Sections 28 to 44DB.

- Capital Gains: Addressed in Sections 45 to 55A.

- Income from Other Sources: Detailed in Sections 56 to 59.

Gross Total Income: Gross Total Income is the sum of income computed under the aforementioned five heads, considering clubbing provisions, and adjustments of set off and carry forward of losses.

Total Income and Computation of Tax Liability

Total income refers to the Gross Total Income (GTI) after deductions available under sections 80C to 80U.

|

Download the notes

Basic Concepts of Income Tax

|

Download as PDF |

Download as PDF

Exemption and Deduction in respect of income

- Exemption for income means that specific income doesn't contribute to any income category, thus not counted in total income calculation.

- Deduction for income entails including the income under the relevant income category for Gross Total Income calculation, allowing deductions afterward. These deductions can be claimed from the specific income category or from the Gross Total Income.

- Specific payments or contributions can qualify for deductions. For instance, Section 10 exempts certain incomes, while sections 54, 54b, 54d, 54ec, 54f, 54g, 54ga, 54gb, 54H offer exemptions for capital gains. Section 16 covers deductions like standard deduction, entertainment allowance, and professional tax from gross salary. Section 24 provides standard deduction and interest deduction on loans under 'Income from House Property.'

- Chapter VI-A (sections 80C to 80U) allows deductions from the assessee's gross total income.

- Exemptions cannot surpass taxable income, but deductions can exceed it.

Rounding off of Income: Section 288A

The total income calculated as per the Income Tax Act will be rounded off to the nearest multiple of Rs. 10. If the last digit is five or more, it will be rounded up to the next higher multiple of 10. If the last digit is less than five, it will be rounded down to the next lower multiple of 10.

|

Take a Practice Test

Test yourself on topics from UGC NET exam

|

Practice Now |

Practice Now

Question for Basic Concepts of Income Tax

Try yourself:

Which section of the Income Tax Act governs the computation of deductions available under sections 80C to 80U?View Solution

Rounding off of Tax: Section 288B

The total income tax amount and refund due, computed according to the Act, will be rounded off to the closest multiple of Rs. 10. If the last digit is five or more, it will be rounded up to the next higher multiple of 10. If the last digit is less than five, it will be rounded down to the next lower multiple of 10.

Disclaimer

The information on this website serves as general information and not legal advice. While efforts are made to ensure accuracy, Taxmann holds no liability for any misinformation.

Taxmann

Taxmann Publications has an internal Research & Editorial Team composed of Chartered Accountants, Company Secretaries, and Lawyers. Led by editor-in-chief Mr. Rakesh Bhargava, this team is committed to delivering accurate and trustworthy content. They employ a six-sigma method aimed at achieving zero errors in their publications and research platforms.

Their process involves several key practices:

- Sourcing statutory information from authorized, credible sources.

- Ensuring all recent judicial and legislative updates are included.

- Creating analytical pieces on relevant and complex topics to help readers grasp the concepts and implications.

- Guaranteeing that all published content is comprehensive, precise, and clear.

- Supporting evidence-based statements with proper legal references like Sections, Circular Numbers, and Notifications.

- Strictly adhering to rules of grammar, consistency, and style.

- Using a clear, uniform font and size across both print and digital formats for readability.

The document Basic Concepts of Income Tax | UGC NET Commerce Preparation Course is a part of the UGC NET Course UGC NET Commerce Preparation Course.

All you need of UGC NET at this link: UGC NET

|

235 docs|166 tests

|

FAQs on Basic Concepts of Income Tax - UGC NET Commerce Preparation Course

| 1. What is the meaning of the term 'Assessment Year' in Income Tax Law? |  |

| 2. What is the 'Previous Year' as per the Income Tax Act? | |

Ans. The 'Previous Year' is the financial year in which the income is earned by the taxpayer. It is the year preceding the 'Assessment Year.' For instance, if the assessment year is 2023-2024, then the previous year is the financial year from April 1, 2022, to March 31, 2023.

| 3. Who qualifies as a 'Person' under Section 2(31) of the Income Tax Act? | |

Ans. Under Section 2(31) of the Income Tax Act, the term 'Person' includes individuals, Hindu Undivided Families (HUF), companies, firms, associations of persons, bodies of individuals, and any other artificial juridical person. This broad definition ensures that various entities are liable for income tax.

| 4. What are the different 'Heads of Income' as per the Income Tax Act? | |

Ans. The Income Tax Act categorizes income into five 'Heads of Income':

1. Income from Salary

2. Income from House Property

3. Income from Business or Profession

4. Income from Capital Gains

5. Income from Other Sources.

Each head has specific provisions for calculating taxable income and applicable deductions.

| 5. What is the significance of exemptions and deductions in income tax? | |

Ans. Exemptions and deductions in income tax reduce the taxable income of an individual or entity. Exemptions refer to specific types of income that are not taxed, while deductions are amounts that can be subtracted from total income to arrive at the taxable income. These provisions are essential for ensuring taxpayers are not overburdened and to encourage investments and savings.

Related Exams

About this Document

4.77/5

Rating

Apr 05, 2025

Last updated

Document Description: Basic Concepts of Income Tax for UGC NET 2025 is part of UGC NET Commerce Preparation Course preparation.

The notes and questions for Basic Concepts of Income Tax have been prepared according to the UGC NET exam syllabus. Information about Basic Concepts of Income Tax covers topics

like Income Tax Law, Assessment Year, Previous Year, Principles relating to Income under Income-tax Act, Heads of Income, Exemption and Deduction in respect of income, Rounding off of Income: Section 288A , Rounding off of Tax: Section 288B and Basic Concepts of Income Tax Example, for UGC NET 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Basic Concepts of Income Tax.

Introduction of Basic Concepts of Income Tax in English is available as part of our UGC NET Commerce Preparation Course

for UGC NET & Basic Concepts of Income Tax in Hindi for UGC NET Commerce Preparation Course course.

Download more important topics related with notes, lectures and mock test series for UGC NET

Exam by signing up for free. UGC NET: Basic Concepts of Income Tax | UGC NET Commerce Preparation Course

Description

Full syllabus notes, lecture & questions for Basic Concepts of Income Tax | UGC NET Commerce Preparation Course - UGC NET | Plus excerises question with solution to help you revise complete syllabus for UGC NET Commerce Preparation Course | Best notes, free PDF download

Information about Basic Concepts of Income Tax

In this doc you can find the meaning of Basic Concepts of Income Tax defined & explained in the simplest way possible. Besides explaining types of

Basic Concepts of Income Tax theory, EduRev gives you an ample number of questions to practice Basic Concepts of Income Tax tests, examples and also practice UGC NET

tests

Related Searches

Sample Paper

,Semester Notes

,Viva Questions

,past year papers

,Free

,Previous Year Questions with Solutions

,mock tests for examination

,Basic Concepts of Income Tax | UGC NET Commerce Preparation Course

,shortcuts and tricks

,Objective type Questions

,Basic Concepts of Income Tax | UGC NET Commerce Preparation Course

,Exam

,Extra Questions

,video lectures

,MCQs

,Basic Concepts of Income Tax | UGC NET Commerce Preparation Course

,study material

,ppt

,practice quizzes

,Summary

,Important questions

;

Additional Information about Basic Concepts of Income Tax for UGC NET Preparation

Basic Concepts of Income Tax Free PDF Download

The Basic Concepts of Income Tax is an invaluable resource that delves deep into the core of the UGC NET exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Basic Concepts of Income Tax now and kickstart your journey towards success in the UGC NET exam.

Importance of Basic Concepts of Income Tax

The importance of Basic Concepts of Income Tax cannot be overstated, especially for UGC NET aspirants.

This document holds the key to success in the UGC NET exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Basic Concepts of Income Tax Notes

Basic Concepts of Income Tax Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Basic Concepts of Income Tax.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Basic Concepts of Income Tax Notes on EduRev are your ultimate resource for success.

Basic Concepts of Income Tax UGC NET Questions

The "Basic Concepts of Income Tax UGC NET Questions" guide is a valuable resource for all aspiring students preparing for the

UGC NET exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Basic Concepts of Income Tax on the App

Students of UGC NET can study Basic Concepts of Income Tax alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Basic Concepts of Income Tax,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Basic Concepts of Income Tax is prepared as per the latest UGC NET syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup