Chapter Notes- Unit 3: Supply

Introduction

- In a market economy, the sellers of goods and services make up the supply side. These sellers can be individuals, companies, or even governments.

- The term demand means the amount of a product or service that consumers are ready and able to buy at different prices over a certain time period.

Conversely, supply refers to how much of a product or service producers are willing and able to provide to the market at various prices during a specific time period. There are three key points about supply:

- Supply indicates what a company offers for sale in the market, but it does not guarantee that all of it will be sold.

- To have supply, there must be both the willingness and the ability to supply. The cost of production usually affects this ability.

- Supply is considered a flow, meaning it is measured over a certain time frame. The quantity supplied is expressed as a certain amount per unit of time, such as per day, week, or year.

Determinants of Supply

Supply of a product or service is influenced by various factors apart from its price. Some of the key determinants are:- Price of the Good: Higher prices of a good lead to increased supply as firms aim to maximize profits.

- Prices of Related Goods: If the prices of other goods increase, firms may shift resources to produce those goods instead. For example, if the price of wheat rises, farmers may allocate more land to wheat production at the expense of corn and soybeans.

Factors Affecting Supply

1. Prices of Factors of Production: The cost of production is a crucial factor influencing supply. If a firm's costs exceed its potential earnings from selling a product, it won't sell anything. When the price of an input rises, supply decreases. Increases in costs such as wages, raw material prices, and interest rates lead producers to reduce the quantity they are willing to supply. Conversely, lower input costs enhance profitability, encouraging existing firms to expand and allowing new firms to enter the market.- For instance, a rise in land costs significantly impacts the production of goods like wheat, which require substantial land, while having a minimal effect on the production of goods like automobiles, which require less land.

- Thus, changes in the price of a factor of production can alter the relative profitability of different products, prompting producers to shift their focus and altering the supply of various commodities.

2. State of Technology: The supply of a product is also dependent on the state of technology. The implementation of advanced technology, such as automation, enhances production efficiency and lowers production costs.

Innovations and inventions enable the production of more or better goods using the same resources, thereby increasing the supply of certain products while decreasing the supply of others. Factors such as the availability of spare production capacity and the ease and cost of substituting production factors also influence supply.

3. Government Policy: Government regulations and policies play a significant role in determining how much firms are willing or allowed to sell. The production of goods may be subject to various taxes, such as excise duty, sales tax, and import duties, which raise production costs. As a result, the quantity supplied of a good typically increases when its market price rises.

- Conversely, subsidies and other financial assistance programs for producers lower production costs and incentivize firms to increase supply.

- However, government restrictions, such as import quotas on consumer products and inputs or rationing of input supplies, can lead to a decrease in production.

The Law of Supply

- Producers are generally willing to sell their products at a price that covers the cost of producing an additional unit. The willingness to supply depends on the difference between the selling price and the production cost. The greater this difference, the more willing producers are to supply the good.

- Supply refers to the quantity of a good that is offered for sale in relation to various factors, with price being the most common factor. However, supply can also be influenced by factors such as technology and scale of operations.

- The law of supply states that, all else being equal, the quantity of a good produced and offered for sale increases as its price rises and decreases as its price falls. This principle is based on the idea that higher prices lead to higher profits, incentivizing producers to supply more.

While the law of supply holds true in many cases, there are exceptions. For instance, in certain situations like the supply of labor at very high wages, supply may decrease instead of increase. The behavior of supply varies depending on the specific phenomenon and the extent of possible adjustments in supply.

- Supply refers to the amount of a particular commodity that producers are willing to offer for sale at different prices. The quantity supplied depends on the price of the commodity, and other factors affecting supply are assumed to be constant.

- Market Supply represents the total supply of a commodity provided by all individual firms or their supply agencies. It gives the amounts of the commodity supplied per time period at various alternative prices by all producers in the market.

- Law of Supply states that, other things being equal, the quantity supplied of a good rises when the price of the good rises.

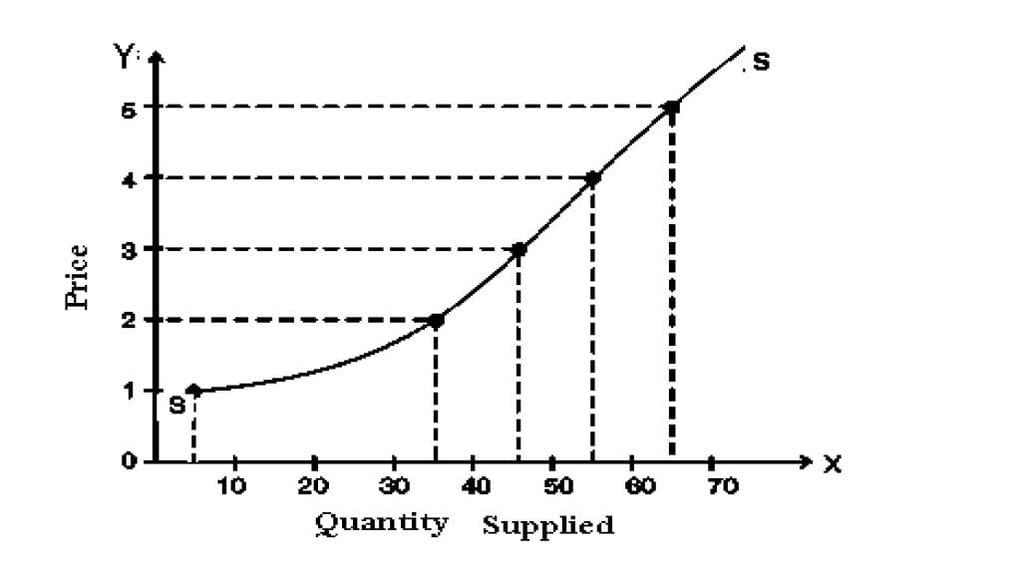

- Supply Schedule is a tabular presentation of the law of supply. It shows the different prices of a commodity and the corresponding quantities that suppliers are willing to offer for sale, with all other variables held constant.

- Supply Curve is a graphical representation of the supply schedule. It indicates the quantity of a good that producers are willing to sell at various prices, assuming that other factors affecting quantity supplied remain constant.

- Upward Slope of Supply Curve indicates that as price increases, the quantity supplied of the commodity also increases. This positive relationship between price and quantity is reflected in the upward slope of the supply curve.

Movements on the Supply Curve: Increase or Decrease in Quantity Supplied

- Increase in Quantity Supplied: When the supply of a good increases due to a rise in its price, we observe an upward movement along the supply curve, indicating an increase in the quantity supplied. A higher market price leads to an expansion of supply, prompting producers to offer more goods for sale.

- Decrease in Quantity Supplied: Conversely, when the market price falls, there is a contraction in supply as producers have less incentive to offer their products for sale. This results in a downward movement along the supply curve, indicating a decrease in the quantity supplied.

Shifts in the Supply Curve: Increase or Decrease in Supply

- Increase in Supply: A shift of the supply curve to the right indicates an increase in supply. This occurs when factors other than the commodity's price change in a way that enhances supply. For instance, at a given price, more goods are offered for sale at each price level.

- Decrease in Supply: Conversely, a shift to the left of the supply curve signifies a decrease in supply. This happens when factors other than price negatively impact supply, leading to less quantity being offered for sale at each price level.

Just like with demand curves, a change in the price of the good itself results in a movement along the supply curve and a change in quantity supplied.

Elasticity of Supply

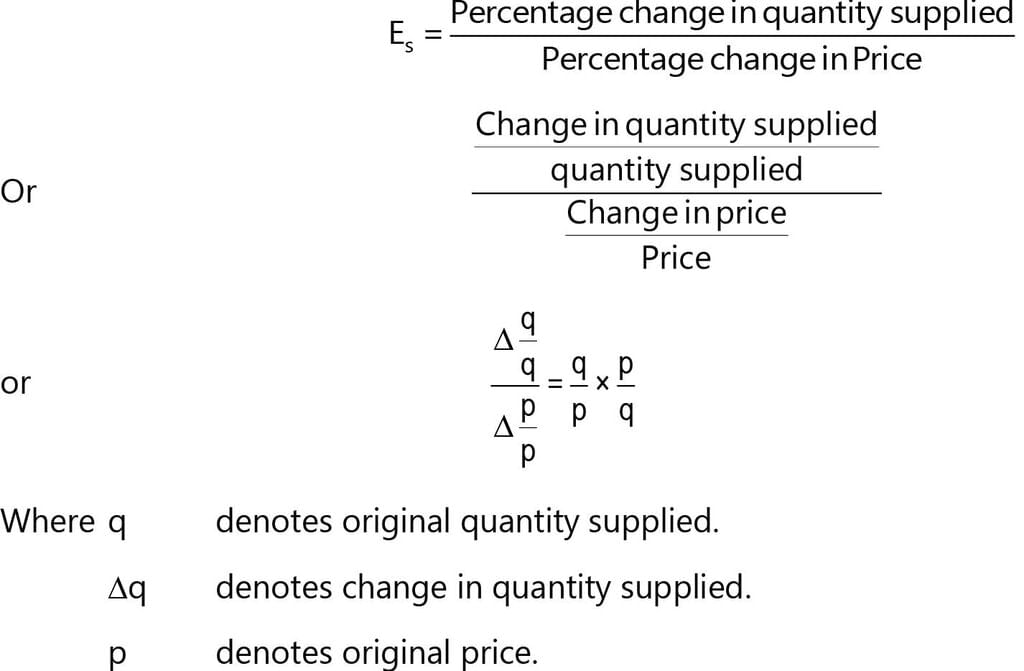

The elasticity of supply measures how responsive the quantity supplied of a good is to changes in its price. It is calculated by dividing the percentage change in quantity supplied by the percentage change in price. The formula is as follows:E = Percentage change in quantity supplied / Percentage change in price

E = (Δq / q) / (Δp / p)

Where:

- q denotes the original quantity supplied.

- Δq denotes the change in quantity supplied.

- p denotes the original price.

- Δp denotes the change in price.

Example:

Given:

Price of commodity X increases from ₹ 2,000 to ₹ 2,100 per unit.

Quantity supplied increases from 2,500 units to 3,000 units.

To Calculate:

Elasticity of supply (E)Formula:

E = (∆q / ∆p)Where:

∆q = Change in quantity supplied = 3,000 - 2,500 = 500 units

∆p = Change in price = ₹ 2,100 - ₹ 2,000 = ₹ 100

p = Initial price = ₹ 2,000

q = Initial quantity supplied = 2,500 unitsCalculation:

E = (∆q / ∆p) = (500 / 100) = 5Conclusion:

Elasticity of Supply = 5, which indicates that the supply is highly elastic.

Types of Supply Elasticity

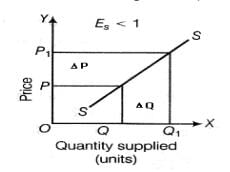

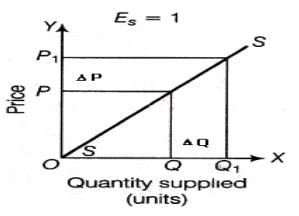

1. Perfectly Inelastic Supply : When the quantity supplied of a good remains unchanged regardless of price changes, the elasticity of supply is zero. This situation is depicted by a vertical supply curve. In such cases, the quantity supplied is not affected by price fluctuations at all.2. Relatively Less Elastic Supply : If the supply of a good changes less than proportionately in response to a price change, the elasticity of supply is less than one. This means that the percentage change in quantity supplied is smaller than the percentage change in price. In this scenario, the quantity supplied is not very responsive to price changes.

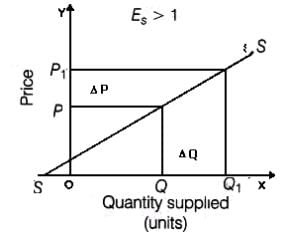

3. Relatively Greater Elastic Supply : When the elasticity of supply is greater than one, it indicates that the quantity supplied responds substantially to a small change in price. In this case, the percentage change in quantity supplied is greater than the percentage change in price. This means the supply is relatively elastic.

3. Relatively Greater Elastic Supply : When the elasticity of supply is greater than one, it indicates that the quantity supplied responds substantially to a small change in price. In this case, the percentage change in quantity supplied is greater than the percentage change in price. This means the supply is relatively elastic. 4. Unit Elastic Supply : If the elasticity of supply is exactly one, it means that the relative change in quantity supplied is equal to the relative change in price. In this case, the percentage change in quantity supplied is the same as the percentage change in price. Unit elastic supply represents a boundary between elastic and inelastic supply.

4. Unit Elastic Supply : If the elasticity of supply is exactly one, it means that the relative change in quantity supplied is equal to the relative change in price. In this case, the percentage change in quantity supplied is the same as the percentage change in price. Unit elastic supply represents a boundary between elastic and inelastic supply.

5. Perfectly Elastic Supply: Perfectly elastic supply is the extreme case where the price elasticity of supply approaches infinity, and the supply curve becomes horizontal. In this scenario:

- Infinite Elasticity: Elasticity of supply is considered infinite (E = ∞) or perfectly elastic. This means that no quantity is supplied at a lower price, and even a tiny change in price leads to an enormous change in quantity supplied.

- Producer Response: Producers are willing to supply any quantity demanded at a specific price. A small increase in price results in a massive increase in quantity supplied.

Varying Elasticity of Supply: In some situations, the elasticity of supply is not constant but changes along the supply curve. Consider an industry with limited production capacity:

- Initial Response to Price Changes: At lower levels of quantity supplied, firms are more responsive to price changes. For example, when the price increases from P1 to P2, the quantity supplied increases more than proportionately (from Q1 to Q2). This is because firms have idle capacity at this stage.

- Full Capacity and Limited Elasticity: As firms reach their full production capacity, further increases in output require significant investments, such as building new plants. At this point, the supply becomes less elastic. To encourage firms to increase output, prices must rise substantially (from P3 to P4).

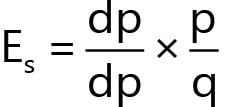

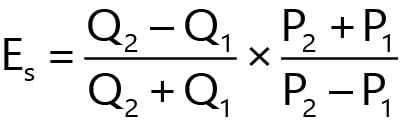

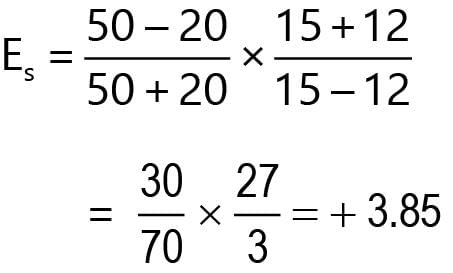

Measurement of Supply Elasticity

Point Elasticity of Supply is measured at a specific point on the supply curve using the formula: Es = (dq/dp) × (p/q) . Arc Elasticity of Supply measures elasticity between two prices using the formula:

Determinants of Elasticity of Supply

The price elasticity of supply hinges on how flexibly sellers can adjust the quantity of a good they produce and sell. The easier it is for sellers to modify their output, the higher the price elasticity of supply. Here are the key factors that determine elasticity of supply:

- Cost Implications: When increasing production leads to significant cost hikes, producers are less inclined to boost supply in response to price increases, resulting in lower price elasticity of supply. Conversely, if costs remain constant or rise minimally with increased output, supply becomes more elastic. Products with intricate production processes or longer production times tend to have lower elasticity of supply. For instance, the supply of aircraft and cruise ships is less elastic compared to that of motorbikes.

- Time Factor: The responsiveness of quantity supplied to price changes improves with time, enhancing the elasticity of supply. Shorter time frames may not allow sellers sufficient opportunity to secure resources, explore alternatives, and adjust production strategies in reaction to price fluctuations. In the long run, firms can establish new facilities, and new entrants can enter the market to augment supply.

- Number of Producers and Competition: Supply becomes more elastic when there is a plethora of producers and a high level of competition among them. Elasticity of supply is also greater when there are fewer barriers to market entry.

- Production Capacity: Supply is elastic if firms are not operating at full capacity. Availability of spare production capacity enables firms to ramp up output without incurring additional costs. Generally, greater spare capacity correlates with higher elasticity of supply.

- Availability of Raw Materials: Elasticity of supply is higher when key raw materials and inputs are readily and affordably accessible. If it is easier to draw productive resources into the industry, the supply curve becomes more elastic. Conversely, difficulties in procuring resources economically lead to increased production costs and lower supply elasticity.

- Stock Levels: Firms with adequate stocks of raw materials, components, and finished goods can respond to price increases with higher supply. Commodities that can be stored easily and inexpensively without losing value typically exhibit elastic supply.

- Factor Substitution: The ease and cost of factor substitution influence price elasticity of supply. If the factors of production are readily available and can be substituted or increased with ease, firms can respond quickly to price increases. Conversely, if production relies on materials that are scarce, have long delivery times, or are highly specialized, supply elasticity diminishes. Similarly, if labor is scarce, highly skilled, and specific, requiring lengthy training periods, elasticity of supply is reduced. For example, professionals like physicians in healthcare and chartered accountants in accounting services exhibit low supply elasticity due to the specialized nature of their skills.

When both capital and labor can easily switch between different occupations, the elasticity of supply for a product is higher compared to situations where capital and labor are not easily transferable. For instance, a printing press can quickly change its output from printing magazines to greeting cards. Similarly, when the prices of a particular vegetable drop, farmers are encouraged to switch to producing a different crop. Products that are produced continuously have greater supply elasticity than those produced infrequently.

Expectations about future prices also influence supply elasticity. If sellers anticipate a significant price increase in the future, they may be less responsive to a current price increase.

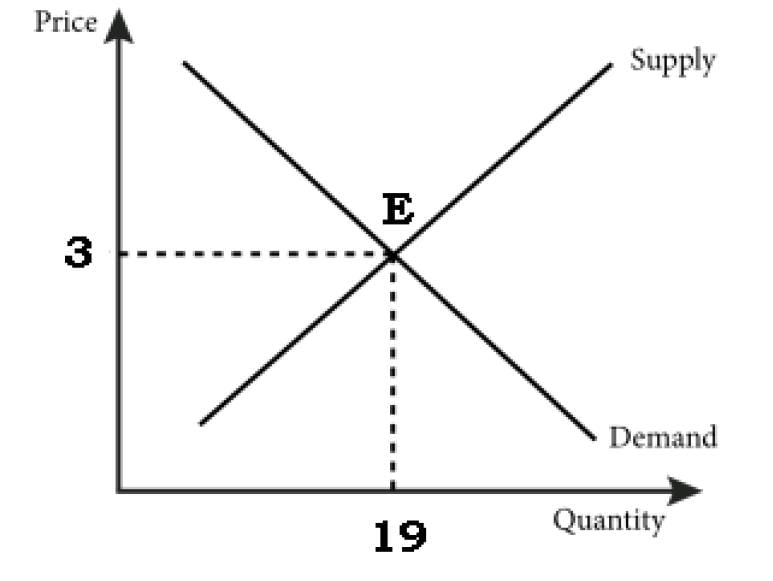

Equilibrium Price

- Equilibrium Price is the price at which the quantity demanded by consumers equals the quantity supplied by producers.

- It is determined by the intersection of the demand and supply curves in the market.

Key Points:

- At the equilibrium price, there is no shortage or surplus of goods in the market.

- The equilibrium price is also known as the market clearing price because it clears the market of any excess supply or demand.

- Microeconomic theory, often called price theory, focuses on the determination of market prices and the behavior of consumers and producers in response to price changes.

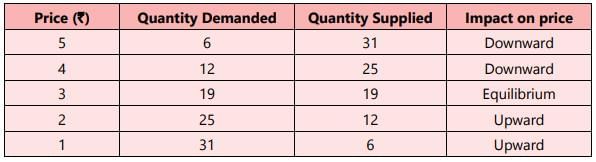

- The table and diagram provided illustrate the concept of equilibrium price, showing how changes in price affect the quantity demanded and supplied.

Impact of Price Changes:

Impact of Price Changes:

- If the price is set above the equilibrium level , the quantity demanded decreases while the quantity supplied increases, leading to excess supply.

- For example, if the price is set at ₹5, the quantity demanded may drop to 6 units while the quantity supplied could be 31 units, creating a surplus.

- This surplus forces sellers to lower their prices until the quantity demanded matches the quantity supplied.

- Conversely, if the price is set below the equilibrium level , the quantity demanded increases while the quantity supplied decreases, leading to a shortage.

- The market will then adjust, pushing prices up until equilibrium is restored.

Conclusion:

Conclusion:

- The equilibrium price is a crucial concept in microeconomics as it represents the point of balance in the market where both consumers and producers are satisfied.

- Understanding how prices affect supply and demand helps in analyzing market behavior and making informed economic decisions.

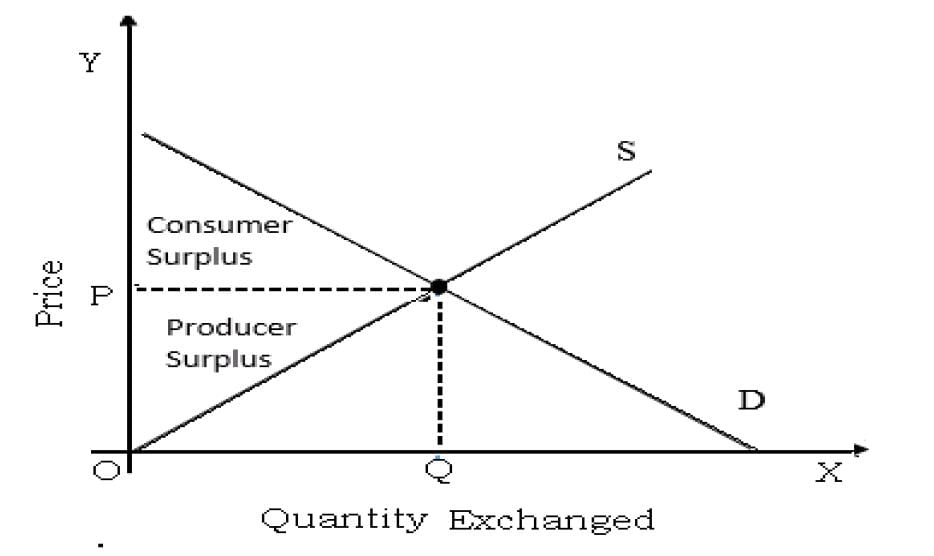

Market Equilibrium and Social Efficiency

Market equilibrium refers to a situation where the quantity of a good or service demanded by consumers matches the quantity supplied by producers at a specific price. This balance ensures that there is no surplus or shortage in the market. Social efficiency , on the other hand, measures the overall welfare benefits to society from the exchanges occurring in the market. It is the sum of consumer surplus and producer surplus .

- Consumer surplus: is an indicator of the welfare and satisfaction consumers derive from purchasing goods or services at prices lower than what they are willing to pay. It reflects the extra benefit consumers receive when they pay less than their maximum price threshold.

- Producer surplus represents the advantage producers gain from selling a product at a price higher than their minimum acceptable price. It occurs when the market price exceeds the lowest price at which producers are willing to supply the good. This surplus is illustrated by the area above the supply curve and below the price level.

When the market price reaches equilibrium, producer surplus diminishes because the price at which sellers are willing to sell aligns with the price they receive. At this point, both producers and consumers achieve their maximum possible surplus, indicating a state of social efficiency.

FAQs on Chapter Notes- Unit 3: Supply

| 1. What are the main determinants of supply? |  |

| 2. What does the Law of Supply state? | |

| 3. What is the difference between a movement along the supply curve and a shift in the supply curve? | |

| 4. How is the elasticity of supply measured? | |

| 5. What factors determine the elasticity of supply? | |