Revision Notes: Theory of Supply | Economics for Grade 9 PDF Download

| Table of contents |

|

| Supply |

|

| Types of Supply |

|

| Law of Supply |

|

| Elasticity of Supply |

|

Supply

Supply refers to the quantity of a commodity that producers are willing to sell to consumers within a specific time frame. It represents a desired flow, indicating how much firms are prepared to sell, rather than what they actually sell.

Supply vs. Stock:

- Supply : Refers to the quantity of a commodity that is actively brought into the market for sale. It reflects actual sales and is measured as a flow of goods over a specific period.

- Stock : Represents the total volume of a commodity that has the potential to be brought into the market for sale. It indicates potential supply and is not measured as a flow over time.

Types of Supply

Based on time, there are three types of supply:

- Market Period Supply: In this scenario, the supply of a commodity cannot be altered at all, even if the price increases, due to the lack of time.

- Short Period Supply: During this period, the supply of a commodity can be increased, but only by utilizing more variable factors such as skilled labor and raw materials. The size of the production plant cannot be changed in the short term.

- Long Period Supply: In the long run, the supply of a commodity can be increased by expanding both the size of the production plant and the variable factors of production.

Factors Affecting Supply

- Price of the Product: When the price of a product increases and exceeds the marginal cost of production, it allows the firm to earn higher profits. This incentivizes the firm to increase the supply of the product.

- Prices of Factors of Production: If the prices of the factors of production increase, assuming other factors remain constant, the profit margin for the firm declines. As a result, the firm may reduce the quantity supplied at the current price level.

- Technological Conditions: Improvements in production technology enable firms to increase supply at the current price level.

- Price of Other Commodities: When the prices of other commodities rise, producers may shift their focus to producing those commodities for higher profits. This can lead to a decrease in the supply of the existing commodity.

- Price of Related Commodities: If the price of a commodity remains stable while the price of its substitute rises, producers may opt to produce the substitute goods for higher profits. This can result in a decrease in the supply of the existing commodity.

- Taxes: Heavy taxes imposed by the government on the production of a particular commodity increase the cost of production. If the price remains constant, profits decrease. In such cases, producers may redirect their resources to produce commodities with lower tax burdens, leading to a decrease in the supply of the taxed commodity.

Law of Supply

The law of supply suggests that, all else being equal, when the price of a good rises, the quantity supplied of that good also increases. Conversely, if the price falls, the quantity supplied decreases.

Supply Schedule

- A supply schedule illustrates the positive relationship between price and quantity supplied.

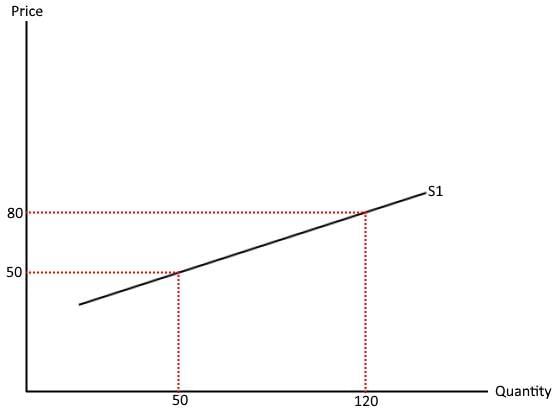

- For example, as the price of a good increases from Rs 5 to Rs 15, the quantity supplied increases from 100 to 300 units.

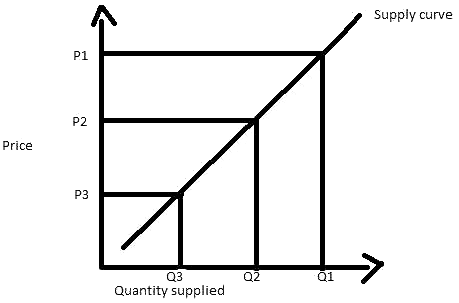

Supply Curve

- A supply curve graphically represents the supply schedule, showing various quantities of a commodity available for sale at different price levels.

- It highlights the positive relationship between the price of a commodity and the quantity supplied.

Individual Supply Curve

- Individual supply refers to the quantity of a specific commodity that an individual firm is willing to supply at a given price in the market.

Market Supply Curve

- The market supply curve is derived by horizontally summing the supply curves of all firms in the industry.

- It represents the total quantity of a commodity that all firms in the market are willing to supply at different price levels.

Ceteris Paribus Assumption

- The supply curve is constructed under the ceteris paribus assumption, which means that all other factors influencing the quantity supplied, such as input prices and technology, are held constant except for the price of the commodity.

Reasons for the Upward Sloping Supply Curve

Law of Diminishing Marginal Productivity: As more units of a variable factor are employed, the additional output produced from each unit decreases, leading to an increase in production costs. Consequently, suppliers are only willing to offer more quantity at higher prices to offset these rising costs.

Change in Stock: When the price of a commodity rises, sellers are inclined to sell more from their existing stock. Conversely, when prices fall, sellers may increase their stock levels to mitigate potential losses.

Profit and Loss: An increase in commodity prices incentivizes producers to ramp up production and supply in pursuit of higher profits.

Exceptions to the Law:

Perishable Goods: Sellers may be willing to sell more units at lower prices for perishable items.

Socially Distinct Goods: For goods with social distinction, supply may remain limited even at high prices.

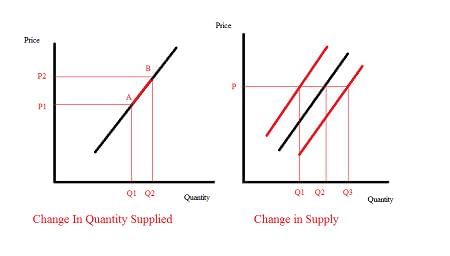

Difference between Change in Quantity Supplied and Change in Supply

Change in Quantity Supplied

- Refers to a movement along a specific supply curve due to a change in the price of the commodity.

- Indicates how much of a commodity is supplied at different prices, showing the relationship between price and quantity supplied.

- For example, if the price of apples increases, the quantity supplied at that price also increases, resulting in a movement along the supply curve for apples.

Change in Supply

- Involves a shift of the entire supply curve due to factors other than price, such as changes in production costs, technology, or number of suppliers.

- Indicates a change in the quantity supplied at all price levels.

- For instance, if there is a technological advancement in apple farming that reduces production costs, the supply curve for apples shifts to the right, indicating an increase in supply at all price levels.

In summary, a change in quantity supplied is about how price changes affect the quantity supplied at different prices, while a change in supply refers to shifts in the supply curve due to various factors other than price.

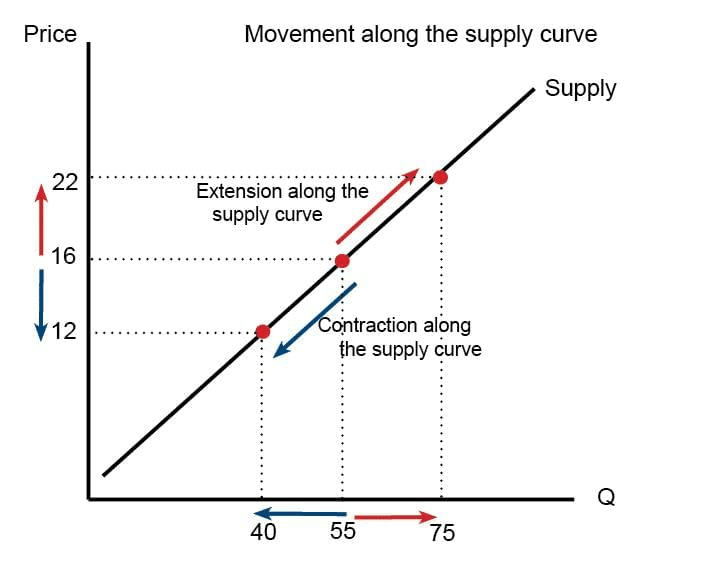

Movement along the Supply Curve

Movement along the supply curve refers to a change in the quantity of a commodity supplied due to a change in the price of that commodity, while other factors remain constant.

Key Points:

- When the price of a commodity increases, the quantity supplied also increases, resulting in a movement from the left to the right along the supply curve. This is known as an extension in the quantity supplied.

- Conversely, when the price of a commodity decreases, the quantity supplied decreases, leading to a movement from the right to the left along the supply curve. This is called a contraction in the quantity supplied.

Shift of the Supply Curve

The shift of the supply curve refers to a change in the supply of a commodity at a given price due to factors other than the price of the commodity.

Key Points:

- An increase in supply occurs when there is an improvement in factors such as technology, a decrease in input prices, a decrease in unit taxes, or a decrease in the prices of related goods, while the price of the good remains constant.

- An extension in supply happens when the price of the good increases, while the other determinants of supply remain constant.

- A decrease in supply is caused by factors such as an increase in input prices, an increase in unit taxes, an increase in the prices of related goods, while the price of the good remains constant.

- A contraction in supply occurs when the price of a good decreases, while the other determinants of supply remain constant.

Elasticity of Supply

Elasticity of supply, also known as price elasticity of supply, assesses how responsive the quantity supplied of a product is to changes in its own price. It is calculated as the percentage change in quantity supplied divided by the percentage change in price.

Formula: e = Percentage change in quantity supplied / Percentage change in price

Alternatively: s = e∆Q/∆P * P/Q

Where:

- P = Initial price

- ∆P = Change in price

- Q = Initial quantity

- ∆Q = Change in quantity supplied

Types of Elasticity

- Perfectly Inelastic Supply: Supply is perfectly inelastic when it does not respond to changes in price. This means that the quantity supplied remains constant regardless of price changes, even reaching zero price. In this case, the elasticity coefficient (Ep) is 0.

- Perfectly Elastic Supply: Supply is considered perfectly price-elastic when there is an infinite change in quantity supplied in response to a tiny change in price. This implies that even a minimal price increase leads to an unlimited increase in quantity supplied. Here, the elasticity coefficient (Ep) is infinite (α).

- Relatively Elastic Supply: Supply is relatively elastic when the percentage change in quantity supplied is greater than the percentage change in price. In this situation, the responsiveness of supply to price changes is high, and the elasticity coefficient (Ep) is greater than 1.

- Relatively Inelastic Supply: Supply is relatively inelastic when the percentage change in quantity supplied is less than the percentage change in price. This indicates that supply is less responsive to price changes, and the elasticity coefficient (Ep) is less than 1.

- Unit Elastic Supply: Supply is unit elastic when the percentage change in quantity supplied is equal to the percentage change in price. In this case, the elasticity coefficient (Ep) is equal to 1, indicating a proportional response of supply to price changes.

Factors Determining Elasticity of Supply

- Possibility of Shift in Production: If producers can easily shift from producing one product to another in response to price changes, the supply becomes more price elastic. For example, the supply of industrial products is often more elastic because producers can switch between different goods relatively easily.

- Time Horizon: The elasticity of supply also varies with time. In the short run, supply may be price inelastic because it is challenging to adjust quantities in response to price changes. However, over the long run, supply can become more price elastic as producers have more flexibility to adjust their output.

- Supply of Inputs: The availability and nature of inputs required for production play a crucial role in determining supply elasticity. If inputs are readily available and easy to source, the supply of the commodity tends to be more elastic. Conversely, if inputs are scarce or difficult to obtain, supply becomes relatively inelastic.

- Nature of the Commodity: The inherent characteristics of the commodity also influence supply elasticity. Perishable goods, such as fresh produce, have relatively inelastic supply because their shelf life is short, and they cannot be stored for long periods. On the other hand, durable goods, like electronics, tend to have more elastic supply as they can be produced and stored over extended periods.

- Cost of Production: The relationship between production costs and the level of output affects supply elasticity. If both average and marginal costs of production increase with higher levels of output, the supply of such commodities becomes relatively inelastic. This is because higher production levels are associated with rising costs, limiting the ability to increase supply in response to price changes.

Significance of Supply Elasticity

- Price Determination: The elasticity of supply plays a crucial role in price determination, particularly considering the time element involved. Prices are influenced by how responsive the supply of a product is to changes in demand.

- Taxation: The Finance Minister can strategically impose taxes based on the elasticity of supply. Goods with inelastic supply can bear higher taxes, while those with elastic supply can be taxed less. This understanding is beneficial for government revenue.

|

34 docs|7 tests

|

FAQs on Revision Notes: Theory of Supply - Economics for Grade 9

| 1. What is the theory of supply in economics? |  |

| 2. What are the main determinants of supply? | |

| 3. What are some exceptions to the law of supply? | |

| 4. How does technology influence supply? | |

| 5. How do expectations about future prices affect supply? | |

Previous Year Questions with Solutions

,shortcuts and tricks

,mock tests for examination

,Sample Paper

,study material

,past year papers

,Viva Questions

,Revision Notes: Theory of Supply | Economics for Grade 9

,Important questions

,Summary

,ppt

,MCQs

,practice quizzes

,Objective type Questions

,Revision Notes: Theory of Supply | Economics for Grade 9

,Semester Notes

,Free

,video lectures

,Extra Questions

,Exam

,Revision Notes: Theory of Supply | Economics for Grade 9

;

Revision Notes: Theory of Supply Free PDF Download

Importance of Revision Notes: Theory of Supply

Revision Notes: Theory of Supply

Revision Notes: Theory of Supply Grade 9 Questions

Study Revision Notes: Theory of Supply on the App

|

© EduRev

|

Education Revolution

|

|