Arun Sharma Summary: Profit , Loss & Discount

Introduction

Profit and Loss is one of the most practical topics in Arithmetic, forming the base for many real-life and exam questions. It deals with the difference between the Cost Price (CP) - the price at which an item is purchased, and the Selling Price (SP) , the price at which it is sold. This topic also introduces related terms like Marked Price (MP), Discount, and Profit/Loss Percentage, which are widely used in business, trade, and exams like CAT, XAT, SNAP, and NMAT.

Understanding these basics allows you to solve not only simple profit-loss questions but also advanced problems involving successive discounts, false weights, overhead costs, and break-even analysis.

Key Terms & Standard Language in Profit & Loss

1. Cost Price (CP)- The amount a seller pays to acquire or produce an item.

2. Selling Price (SP)

- The amount at which the seller sells the item to a buyer.

3. Profit (Gain)

- Occurs when the selling price is greater than the cost price.

- Formula: Profit = Selling Price - Cost Price.

- Example:

Selling price = ₹250,

Cost price = ₹200,

So ,Profit = ₹250 - ₹200 = ₹50.

4. Loss

- Occurs when the selling price is less than the cost price.

- Formula: Loss = Cost Price - Selling Price.

- Example:

Selling price = ₹180,

Cost price = ₹200, so

Loss = ₹200 - ₹180 = ₹20.

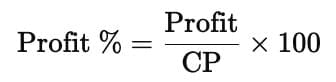

5. Profit Percentage

- The profit is expressed as a percentage of the cost price.

- Formula:

- Example:

Profit = ₹50 on Cost price = ₹200,

so Profit Percentage = (50 ÷ 200) × 100 = 25%.

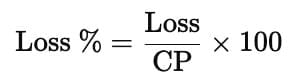

6. Loss Percentage

- The loss is expressed as a percentage of the cost price.

- Formula:

- Example:

Loss = ₹20 on Cost price = ₹200,

so Loss Percentage = (20 ÷ 200) × 100 = 10%.

7. Marked Price (MP) or List Price

- The labelled price printed on an item before any discount.

8. Discount

- Reduction allowed from the marked price when selling.

- Formula: Discount = Marked Price - Selling Price.

- Example: Marked price = ₹300, Selling price after discount = ₹270, Discount = ₹300 - ₹270 = ₹30.

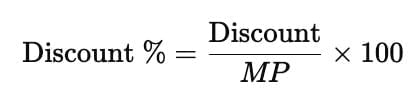

9. Discount Percentage

- The discount is expressed as a percentage of the marked price.

- Formula:

- Example:

Marked price = ₹300,

Discount = ₹30,

Discount Percentage = (30 ÷ 300) × 100 = 10%.

Profit & Loss( In Case of an Individual)

Profit: SP > CP,

Profit = SP - CP.

Loss: SP < CP,

Loss = CP - SP.

Percentage Profit/Loss:

- Percentage Profit =

- Percentage Loss =

Example: For an item with CP ₹100 and SP ₹120, profit = ₹20, percentage profit =

Profit & Loss as Applied to Commercial Transactions

1. Profit in Multiple Units of Products are Being Bought or Sold:

Total CP = CP per unit × number of units,

Total SP = SP per unit × number of units.

Profit = Total SP - Total CP

2. Loss in Multiple Units of Products are Being Bought or Sold:

If SP < CP per unit,

Loss = total CP - total SP.

Types of Costs

1. Direct Costs (Variable Costs)

- Variable costs (e.g., transportation) are proportional to the number of units. Total CP includes these costs.

- Example: For 10 pens at CP ₹5 each, variable cost ₹1 per pen,

Total CP = (₹5 + ₹1) × 10 = ₹60.

2. Indirect Costs (Overhead Costs or Fixed Costs)

- Fixed costs (e.g., rent) remain constant regardless of units sold. They are added to the total CP.

- Example: For 100 pens at CP ₹10 each, fixed cost ₹100,

Total CP = 100 x₹10 + ₹100 = ₹1100.

SP = ₹12 each,

Total SP = ₹1200,

Profit = ₹100.

3. Semi-Variable Costs

- Semi-variable costs combine fixed and variable components, increasing with sales volume.

- Example: A fixed rent of ₹500 plus ₹1 per unit transport for 100 units adds ₹100 variable cost,

Total CP = base CP + ₹500 + ₹100.

The Concept of the Break-Even Point

The break-even point occurs when total SP = total CP, resulting in no profit or loss.

Break-Even Sales: Total SP = Total CP.

Break-Even Units: Number of units sold where total revenue equals total cost.

Example: For 100 pens, CP = ₹8 each, total CP = ₹800. To break even at SP ₹10 each, sell

Profit Calculation based on Equating the Amount Spent and the Amount Earned

- Profit is determined by equating total CP (amount spent) and total SP (amount earned).

- Formula: Profit = Total SP - Total CP.

- Example:

For 100 pens, CP = ₹8 each,

SP = ₹10 each,

total CP = ₹800,

total SP = ₹1000,

Profit = ₹200,

Percentage Profit =

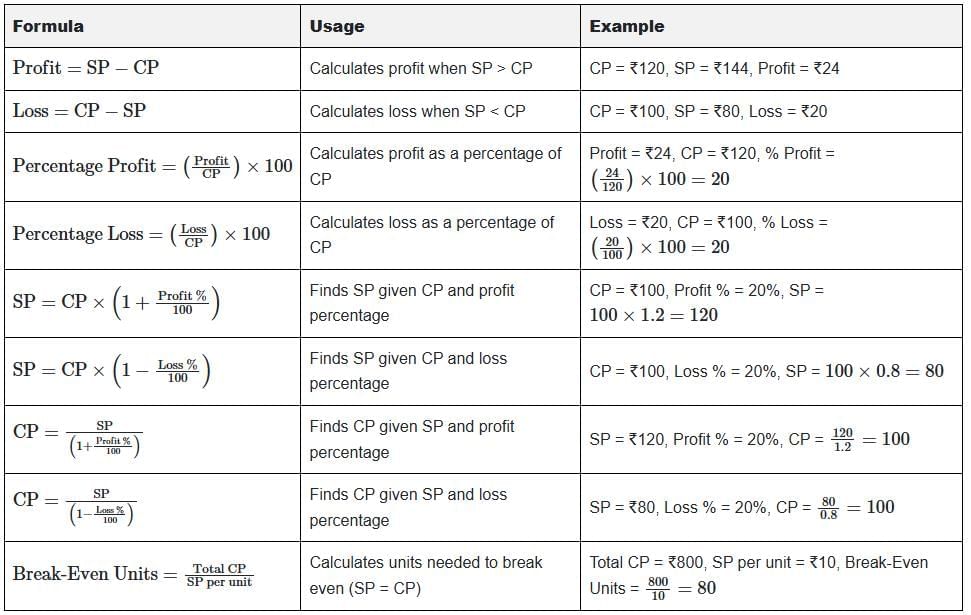

Table: Summary of Key Formulas and Examples

FAQs on Arun Sharma Summary: Profit , Loss & Discount

| 1. What is the difference between direct costs and indirect costs in profit and loss calculations? |  |

| 2. How do you calculate the break-even point in a business? | |

| 3. What are semi-variable costs and how do they affect profit calculations? | |

| 4. How can profit be calculated by equating the amount spent and the amount earned? | |

| 5. Why is understanding profit and loss important for businesses? | |