Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals | Accountancy Class 12 - Commerce PDF Download

PROBLEMS BASED ON FUNDAMENTALS

Q1. A, B, and C were partners in a firm having no partnership agreement. A, B and C

contributed Rs. 2,00,000, Rs. 3,00,000 and 1,00,000 respectively. A and B desire that the

profits should be divided in the ratio of capital contribution. C does not agree to this. How will

the dispute be settled?

ANS: C is correct because in the absence of a Partnership deed the profits are to be shared

equally.

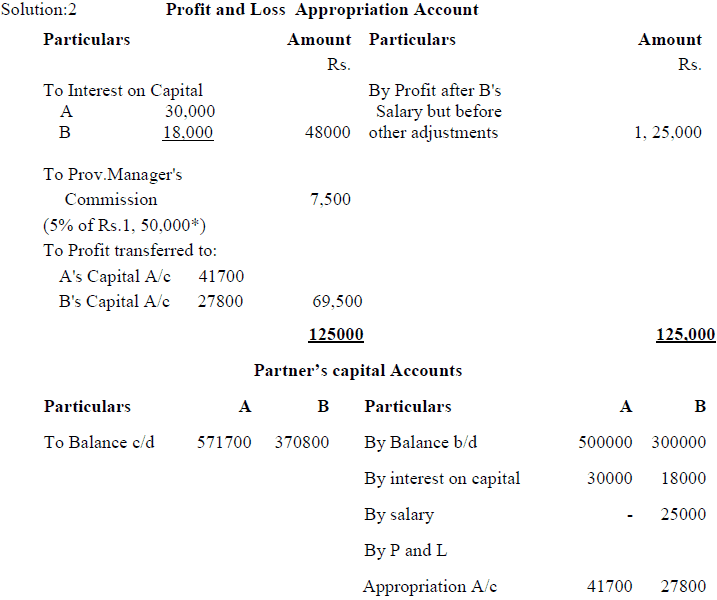

Q2. A and B are partners sharing profits in the ratio of 3: 2 with capitals of Rs. 5, 00,000 and

Rs. 3,00,000 respectively. Interest on capital is agreed @ 6% p.a. B is to be allowed an

annual salary of Rs. 25000. During 2006, the profits of the year prior to calculation of

interest on capital but after charging B's salary amounted to Rs. 1,25,000. A provision of

5% of the profits is to be made in respect of Manager's commission.

Prepare an account showing the allocation of profits and partners' capital accounts.

571700 370800 571700 370800

Q3. Give the answer to the following:

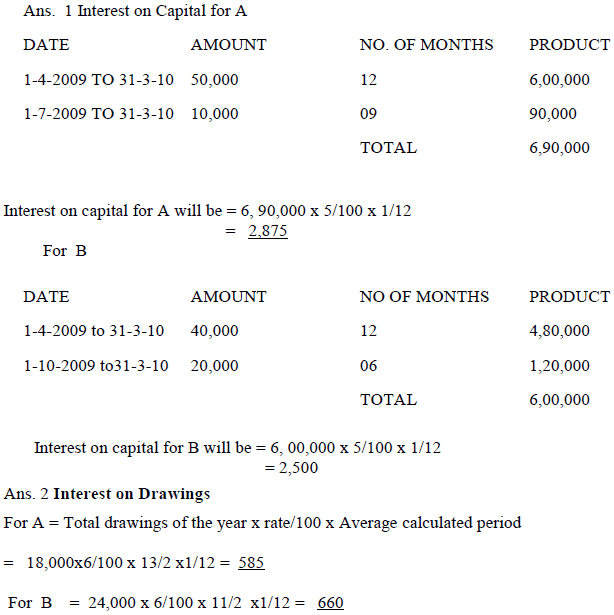

(1) P and Q are partners sharing profits and losses in the ratio of 3:2. On 1st April 2009 their

capital balances were Rs.50, 000 and 40,000 respectively. On 1st July 2009 P brought

Rs.10, 000 as his additional capital whereas Q brought Rs.20, 000 as additional capital on

1st October 2009. Interest on capital was provided @ 5% p.a. Calculate the interest on

capital of P and Q on 31st March 2010.

(2) A and B are partners sharing profits and losses in the ratio of 2:1. A withdraws Rs.1500 at

the beginning of each month and B withdrew Rs. 2000 at the end of each month for 12

months. Interest on drawings was charged @ 6% p.a. Calculate the interest on drawings

of A and B for the year ended 31st December 2009.

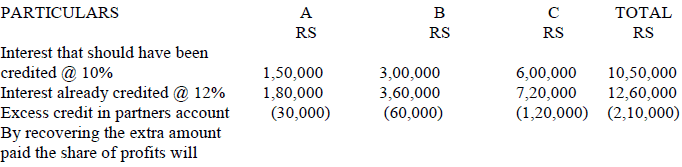

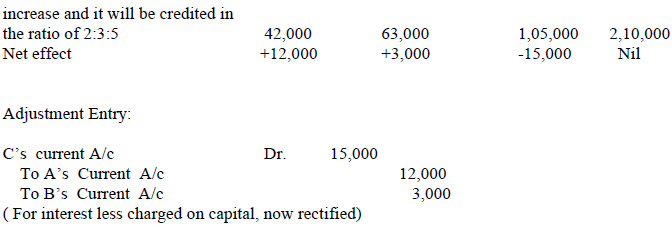

Q4. A, B and C are partners in a firm sharing profits and losses in the ratio of 2:3:5. Their

fixed capitals were 15, 00,000, Rs.30, 00,000 and Rs.6, 00,000 respectively. For the year 2009

interest on capital was credited to them @ 12% instead of 10%. Pass the necessary adjustment

entry.

Ans: TABLE SHOWING ADJUSTMENT

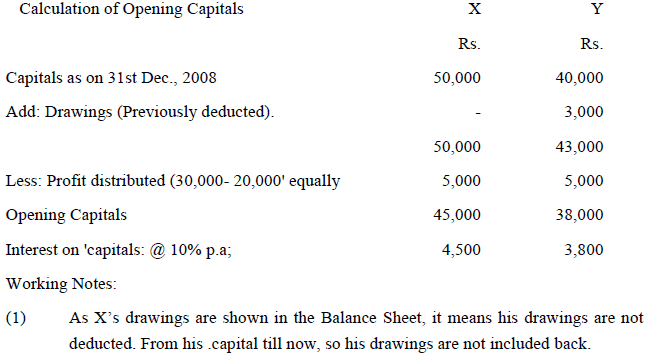

Q5. From the following balance sheet of X and Y, calculate interest on capitals @ 10% p.a.

payable to X and Y for the year ended 31st December, 2008.

During the year 2008, X's drawings were Rs. 10,000 and Y's Drawing were Rs. 3,000.

Profit during the year, 2008 was Rs.30, 000.

Ans :

(2) Profits for 2008 were Rs. 30,000 and profits of Rs. 20,000· are, shown in the

Balance Sheet, which means only Rs. 10,000 profits were distributed between the

partners.

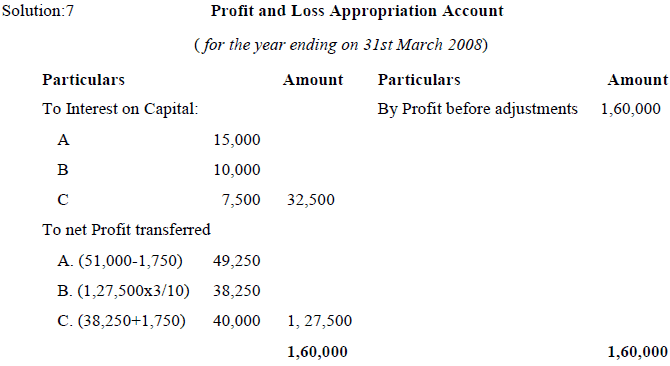

Q6. A, B and C entered into partnership on 1st April, 2008 to share profits & losses in the ratio

of 4:3:3. A, however, personally guaranteed that C's share of profit after charging interest

on Capital @ 5% p.a. would not be less than Rs. 40,000 in any year. The Capital

contributions were:

A, Rs. 3, 00,000;

B, Rs. 2, 00,000 and

C, Rs. 1, 50,000.

The profit for the year ended on 31st March, '2008 amounted to Rs. 1, 60,000. Show the

Profit & Loss Appropriation Account.

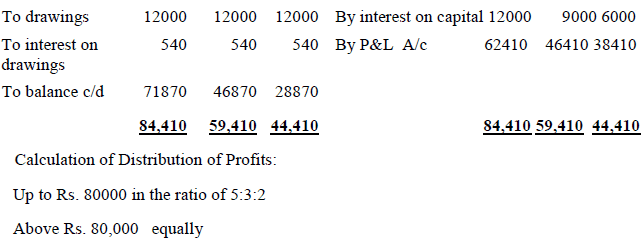

Q7. A, and C are partners with fixed capitals of Rs. 2,00,000, Rs. 1,50,000 and Rs.

1,00,000 respectively. The balance of current accounts on 1st January, 2004 were A Rs.

10,000 (Cr.); B Rs. 4,000 (Cr.) and C Rs. 3,000 (Dr.). A gave a loan to the firm of Rs.

25,000 on 1st July, 2004. The Partnership deed provided for the following:-

(i) Interest on Capital at 6%.

(ii) Interest on drawings at 9%. Each partner drew Rs. 12,000 on 1st July, 2004.

(iii) Rs. 25,000 is to be transferred in a Reserve Account.

(iv) Profit sharing ratio is 5:3: 2 up to Rs. 80,000 and above Rs. 80,000 equally. Net

Profit of the firm before above adjustments was Rs. 1,98,360.

From the above information prepare Profit and Loss Appropriation Account, Capital and

Current Accounts of the partners.

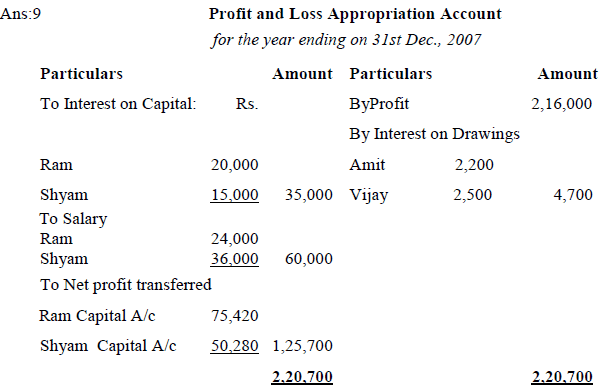

Q8. Ram and Shyam started a partnership business on 1st January, 2007. Their capital

contributions were Rs. 2,00,000 and Rs. 10,0000 respectively. The partnership deed

provided:

i. Interest on capitals @10% p.a.

ii. Ram, to get a salary of Rs. 2,000 p.m. and Shyam Rs. 3,000 p.m.

iii. Profits are to be shared in the ratio of 3:2.

The profits for the year ended 31st December, 2007 before making above appropriations

were Rs. 2,16,000. Interest on Drawings amounted to Rs. 2,200 for Ram and Rs. 2,500 for

Shyam. Prepare Profit and Loss Appropriation Account.

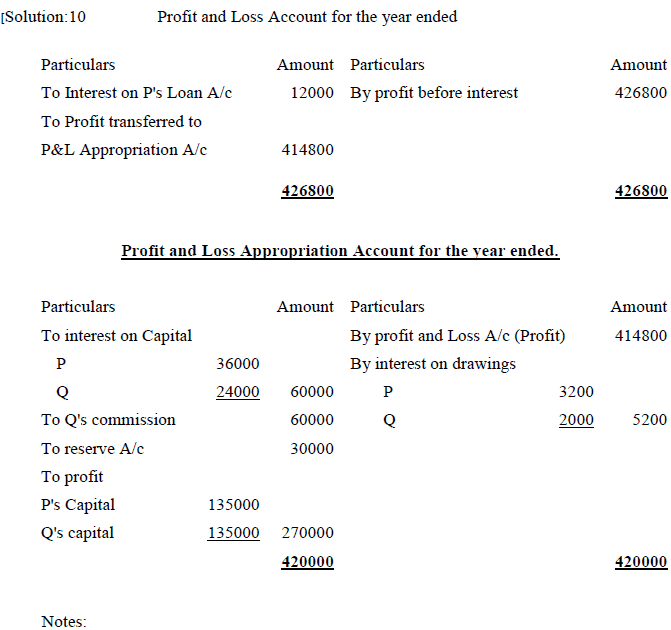

Q9. P and Q are partners with capitals of Rs. 6,00,000 and Rs. 4,00,000 respectively. The profit

and Loss Account of the firm showed a net Profit of Rs. 4, 26,800 for the year. Prepare Profit

and Loss account after taking the following into consideration:-

(i) Interest on P's Loan of Rs. 2,00,000 to the firm

(ii) Interest on 'capital to be allowed @ 6% p.a.

(iii) Interest on Drawings @ 8% p.a. Drawings were; P Rs 80,000 and Q Rs.

1000,000.

(iv) Q is to be allowed a commission on sales @ 3%. Sales for the year was Rs.

1000000

(v) 10% of the divisible profits is to be kept in a Reserve Account.

(i) If the rate of interest on Partners' Loan is not given in the question, it is to be wed

@ 6% p.a. according to the Partnership Act.

(ii) Interest on Partners' Loan is treated as a charge against Profit, so it is shown in the

debit of Profit and Loss A/c.

(iii) If the date of Drawings is not given in the question, interest on drawings will be

charged and average period of 6 months. .

(iv) Reserve Fund is calculated at 10% on Rs. 3,00,000 (i.e. Rs. 4,26,800 + Rs. 5,200-

12,000 - Rs. 60,000 - Rs. 60,000.

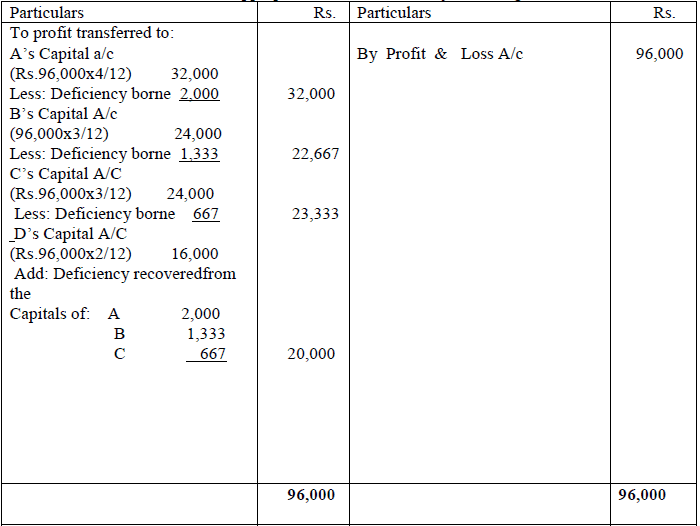

Guarantee of profit

A, B and C arte partners. They admit D and guarantee that his share of profit will not be less than

Rs. 20,000. Profits to be shared 4:3:3:2 respectively. Total profits were Rs. 96,000. It was agreed

that excess payable to D over his share will be borne by A,B and C in the ratio of 3:2:1.

Calculate share of profit for each partner.

Books of A,B and C

Profit and Loss appropriation account for the year ending………

|

42 videos|199 docs|43 tests

|

FAQs on Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals - Accountancy Class 12 - Commerce

| 1. What are the basic features of a partnership firm in accounting? |  |

| 2. How is profit-sharing determined in a partnership? | |

| 3. What is the significance of a partnership deed? | |

| 4. What is the process for admission of a new partner in a partnership firm? | |

| 5. What are the accounting entries for the dissolution of a partnership firm? | |

Exam

,Important questions

,ppt

,past year papers

,study material

,Summary

,Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals | Accountancy Class 12 - Commerce

,mock tests for examination

,Objective type Questions

,Extra Questions

,shortcuts and tricks

,Previous Year Questions with Solutions

,Free

,Viva Questions

,Sample Paper

,video lectures

,Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals | Accountancy Class 12 - Commerce

,MCQs

,Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals | Accountancy Class 12 - Commerce

,practice quizzes

,Semester Notes

;

Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals Free PDF Download

Importance of Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals

Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals Notes

Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals Commerce Questions

Study Problems Based on Fundamentals - Accounting for Partnership Firms: Fundamentals on the App

|

© EduRev

|

Education Revolution

|

|