4. Monetary Policies, Indian Economy, Civil Services Exam | RAS RPSC Prelims Preparation - Notes, Study Material & Tests - RPSC RAS (Rajasthan) PDF Download

Monetary policy is the process by which the monetary authority of a country controls the supply of money, often targeting an inflation rate or interest rate to ensure price stability and general trust in the currency.

Objectives of Monetary Policies are:-

- Accelerated growth of the economy

- Balancing saving and investments

- Exchange rate stabilization

- Price stability

- Employment generation

Monetary Policy could be expansionary or contractionary; Expansionary policy would increase the total money supply in the economy while contractionary policy would decrease the money supply in the economy.

RBI issues the Bi-Monthly monetary policy statement. The tools available with RBI to achieve the targets of monetary policy are:-

- Bank rates

- Reserve Ratios

- Open Market Operations

- Intervention in forex market

- Moral suasion

Repo Rate- Repo rate is the rate at which the central bank of a country (RBI in case of India) lends money to commercial banks in the event of any shortfall of funds. In the event of inflation, central banks increase repo rate as this acts as a disincentive for banks to borrow from the central bank. This ultimately reduces the money supply in the economy and thus helps in arresting inflation.

Reverse Repo Rate is the rate at which RBI borrows money from the commercial banks.An increase in the reverse repo rate will decrease the money supply and vice-versa, other things remaining constant. An increase in reverse repo rate means that commercial banks will get more incentives to park their funds with the RBI, thereby decreasing the supply of money in the market.

Cash Reserve Ratio (CRR) is a specified minimum fraction of the total deposits of customers, which commercial banks have to hold as reserves either in cash or as deposits with the central bank. CRR is set according to the guidelines of the central bank of a country.The amount specified as the CRR is held in cash and cash equivalents, is stored in bank vaults or parked with the Reserve Bank of India. The aim here is to ensure that banks do not run out of cash to meet the payment demands of their depositors. CRR is a crucial monetary policy tool and is used for controlling money supply in an economy.

CRR specifications give greater control to the central bank over money supply. Commercial banks have to hold only some specified part of the total deposits as reserves. This is called fractional reserve banking.

Statutory liquidity ratio (SLR) is the Indian government term for reserve requirement that the commercial banks in India require to maintain in the form of gold, government approved securities before providing credit to the customers. It’s the ratio of liquid assets to net demand and time liabilities.Apart from Cash Reserve Ratio (CRR), banks have to maintain a stipulated proportion of their net demand and time liabilities in the form of liquid assets like cash, gold and unencumbered securities. Treasury bills, dated securities issued under market borrowing programme and market stabilisation schemes (MSS), etc also form part of the SLR. Banks have to report to the RBI every alternate Friday their SLR maintenance, and pay penalties for failing to maintain SLR as mandated.

Inflation & Control Mechanism

Inflation is a sustained increase in the general price level of goods and services in an economy over a period of time. When the price level rises, each unit of currency buys fewer goods and services.It is the percentage change in the value of the Wholesale Price Index (WPI) on a year-on year basis. It effectively measures the change in the prices of a basket of goods and services in a year. In India, inflation is calculated by taking the WPI as base.

Formula for calculating Inflation=

(WPI in month of current year-WPI in same month of previous year)

————————————————————————————– X 100

WPI in same month of previous year

Inflation occurs due to an imbalance between demand and supply of money, changes in production and distribution cost or increase in taxes on products. When economy experiences inflation, i.e. when the price level of goods and services rises, the value of currency reduces. This means now each unit of currency buys fewer goods and services.

It has its worst impact on consumers. High prices of day-to-day goods make it difficult for consumers to afford even the basic commodities in life. This leaves them with no choice but to ask for higher incomes. Hence the government tries to keep inflation under control.

Contrary to its negative effects, a moderate level of inflation characterizes a good economy. An inflation rate of 2 or 3% is beneficial for an economy as it encourages people to buy more and borrow more, because during times of lower inflation, the level of interest rate also remains low. Hence the government as well as the central bank always strive to achieve a limited level of inflation.

Various measures of Inflation are:-

- GDP Deflator

- Cost of Living Index

- Producer Price Index(PPI)

- Wholesale Price Index(WPI)

- Consumer Price Index(CPI)

There are following types on Inflation based on their causes:-

- Demand pull inflation

- cost push inflation

- structural inflation

- speculation

- cartelization

- hoarding

Various control measures to curb rising inflation are:-

- Fiscal measures like reduction in indirect taxes

- Dual pricing

- Monetary measures

- Supply side measures like importing the shortage goods to meet the demand

- Administrative measures to curb hoarding, Cratelization.

Money Supply

Money supply is the entire stock of currency and other liquid instruments in a country’s economy as of a particular time. The money supply can include cash, coins and balances held in checking and savings accounts.

- Money Supply can be estimated as narrow or broad money.

- There are four measures of money supply in India which are denoted by M1, M2, M3 and M4. This classification was introduced by the Reserve Bank of India (RBI) in April 1977. Prior to this till March 1968, the RBI published only one measure of the money supply, M or defined as currency and demand deposits with the public. This was in keeping with the traditional and Keynesian views of the narrow measure of the money supply.

- M1 (Narrow Money) consists of:

(i) Currency with the public which includes notes and coins of all denominations in circulation excluding cash on hand with banks:

(ii) Demand deposits with commercial and cooperative banks, excluding inter-bank deposits; and

(iii) ‘Other deposits’ with RBI which include current deposits of foreign central banks, financial institutions and quasi-financial institutions such as IDBI, IFCI, etc., other than of banks, IMF, IBRD, etc. The RBI characterizes as narrow money.

- M2. which consists of M1 plus post office savings bank deposits. Since savings bank deposits of commercial and cooperative banks are included in the money supply, it is essential to include post office savings bank deposits. The majority of people in rural and urban India have preference for post office deposits from the safety viewpoint than bank deposits.

- M3. (Broad Money) which consists of M1, plus time deposits with commercial and cooperative banks, excluding interbank time deposits. The RBI calls M3 as broad money.

- M4.which consists of M3 plus total post office deposits comprising time deposits and demand deposits as well. This is the broadest measure of money supply.

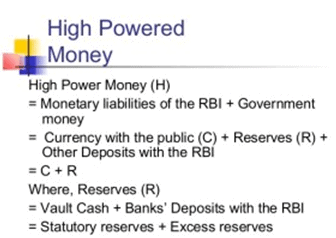

- High powered money – The total liability of the monetary authority of the country, RBI, is called the monetary base or high powered money. It consists of currency ( notes and coins in circulation with the public and vault cash of commercial banks) and deposits held by the Government of India and commercial banks with RBI. If a memeber of the public produces a currency note to RBI the latter must pay her value equal to the figure printed on the note. Similarly, the deposits are also refundable by RBI on demand from deposit holders. These items are claims which the general public, government or banks have on RBI and are considered to be the liability of RBI.

- RBI acquires assets against these liabilities. The process can be understood easily if we consider a simple stylised example. Suppose RBI purchases gold or dollars’ worthRs. 5. It pays for thr gold or foreign exchange by issuing currency to the seller. The currency in circulation in the economy thus goes up by Rs. 5, an item that shows up on the liabilityside of RBI’s Balance sheet. The value of the acquired asset, also equal to Rs. 5, is entered under the appropriate head on the Assets side. Similarly, the RBI acquires debt bonds or securities issued by the government and pays the government by issuing currency. It issues loans to commercial banks in a similar fashion.

Role of Commercial Banks

A Commercial bank is a type of financial institution that provides services such as accepting deposits, making business loans, and offering basic investment products

There is acute shortage of capital. People lack initiative and enterprise. Means of transport are undeveloped. Industry is depressed. The commercial banks help in overcoming these obstacles and promoting economic development. The role of a commercial bank in a developing country is discussed as under.

1. Mobilising Saving for Capital Formation:

The commercial banks help in mobilising savings through network of branch banking. People in developing countries have low incomes but the banks induce them to save by introducing variety of deposit schemes to suit the needs of individual depositors. They also mobilise idle savings of the few rich. By mobilising savings, the banks channelize them into productive investments. Thus they help in the capital formation of a developing country.

2. Financing Industry:

The commercial banks finance the industrial sector in a number of ways. They provide short-term, medium-term and long-term loans to industry.

3. Financing Trade:

The commercial banks help in financing both internal and external trade. The banks provide loans to retailers and wholesalers to stock goods in which they deal. They also help in the movement of goods from one place to another by providing all types of facilities such as discounting and accepting bills of exchange, providing overdraft facilities, issuing drafts, etc. Moreover, they finance both exports and imports of developing countries by providing foreign exchange facilities to importers and exporters of goods.

4. Financing Agriculture:

The commercial banks help the large agricultural sector in developing countries in a number of ways. They provide loans to traders in agricultural commodities. They open a network of branches in rural areas to provide agricultural credit. They provide finance directly to agriculturists for the marketing of their produce, for the modernisation and mechanisation of their farms, for providing irrigation facilities, for developing land, etc.

They also provide financial assistance for animal husbandry, dairy farming, sheep breeding, poultry farming, pisciculture and horticulture. The small and marginal farmers and landless agricultural workers, artisans and petty shopkeepers in rural areas are provided financial assistance through the regional rural banks in India. These regional rural banks operate under a commercial bank. Thus the commercial banks meet the credit requirements of all types of rural people. In India agricultural loans are kept in priority sector landing.

5. Financing Consumer Activities:

People in underdeveloped countries being poor and having low incomes do not possess sufficient financial resources to buy durable consumer goods. The commercial banks advance loans to consumers for the purchase of such items as houses, scooters, fans, refrigerators, etc. In this way, they also help in raising the standard of living of the people in developing countries by providing loans for consumptive activities and also increase the demand in the economy.

6. Financing Employment Generating Activities:

The commercial banks finance employment generating activities in developing countries. They provide loans for the education of young person’s studying in engineering, medical and other vocational institutes of higher learning. They advance loans to young entrepreneurs, medical and engineering graduates, and other technically trained persons in establishing their own business. Such loan facilities are being provided by a number of commercial banks in India. Thus the banks not only help inhuman capital formation but also in increasing entrepreneurial activities in developing countries.

7. Help in Monetary Policy:

The commercial banks help the economic development of a country by faithfully following the monetary policy of the central bank. In fact, the central bank depends upon the commercial

banks for the success of its policy of monetary management in keeping with requirements of a developing economy.

Issue of NPA

A non-performing asset (NPA) is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.According to RBI, terms loans on which interest or instalment of principal remain overdue for a period of more than 90 days from the end of a particular quarter is called a Non-performing Asset.

However, in terms of Agriculture / Farm Loans; the NPA is defined as under:

- For short duration crop agriculture loans such as paddy, Jowar, Bajra etc. if the loan (instalment / interest) is not paid for 2 crop seasons , it would be termed as a NPA.

- For Long Duration Crops, the above would be 1 Crop season from the due date.

- The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act has provisions for the banks to take legal recourse to recover their dues. When a borrower makes any default in repayment and his account is classified as NPA; the secured creditor has to issue notice to the borrower giving him 60 days to pay his dues. If the dues are not paid, the bank can take possession of the assets and can also give it on lease or sell it; as per provisions of the SAFAESI Act.

Reselling of NPAs :- If a bad loan remains NPA for at least two years, the bank can also resale the same to the Asset Reconstruction Companies such as Asset Reconstruction Company (India) (ARCIL). These sales are only on Cash Basis and the purchasing bank/ company would have to keep the accounts for at least 15 months before it sells to other bank. They purchase such loans on low amounts and try to recover as much as possible from the defaulters. Their revenue is difference between the purchased amount and recovered amount.

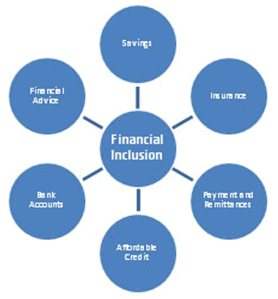

Financial Inclusion

Financial inclusion or inclusive financing is the delivery of financial services at affordable costs to sections of disadvantaged and low-income segments of society, in contrast to financial exclusion

Government of India has launched an innovative scheme of Jan DhanYojna for Financial Inclusion to provide the financial services to millions out of the regulated banking sector.

Various program’s for financial inclusion are:-

- Swabhimaan Scheme: under the Swabhimaan campaign, the Banks were advised to provide appropriate banking facilities to habitations having a population in excess of 2000 (as per 2001 census) by March 2012.

- Extention of the banking network in unbanked areas,

- Expansion of Business Correspondent Agent (BCA) Network

- Direct Benefit Transfer (DBT) and Direct Benefit Transfer for LPG (DBTL)

- RuPay, a new card payment scheme has been conceived by NPCI to offer a domestic, open-loop, multilateral card payment system which will allow all Indian banks and financial Institutions in India to participate in electronic payments.

Pradhan Mantri Jan-DhanYojana (PMJDY) was formally launched on 28th August, 2014. The Yojana envisages universal access to banking facilities with at least one basic banking account for every household, financial literacy, access to credit, insurance and pension. The beneficiaries would get a RuPay Debit Card having inbuilt accident insurance cover of Rs.1.00 lakh. In addition there is a life insurance cover of Rs.30000/- to those people who opened their bank accounts for the first time between 15.08.2014 to 26.01.2015 and meet other eligibility conditions of the Yojana.

FAQs on 4. Monetary Policies, Indian Economy, Civil Services Exam - RAS RPSC Prelims Preparation - Notes, Study Material & Tests - RPSC RAS (Rajasthan)

| 1. What is the role of monetary policies in the Indian economy? |  |

| 2. How do monetary policies impact the Indian economy? | |

| 3. What are the tools used by the Reserve Bank of India to implement monetary policies? | |

| 4. How do monetary policies affect the common man in India? | |

| 5. How does the Reserve Bank of India manage inflation through monetary policies? | |

|

4.74/5 Rating |

|

Dec 18, 2024 Last updated |

|

109 docs|21 tests

|

|

Explore Courses for RPSC RAS (Rajasthan) exam

|

|

Study Material & Tests - RPSC RAS (Rajasthan)

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,study material

,Indian Economy

,4. Monetary Policies

,Study Material & Tests - RPSC RAS (Rajasthan)

,Semester Notes

,Sample Paper

,Extra Questions

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,Exam

,Viva Questions

,mock tests for examination

,Previous Year Questions with Solutions

,Study Material & Tests - RPSC RAS (Rajasthan)

,past year papers

,ppt

,Free

,shortcuts and tricks

,4. Monetary Policies

,Summary

,Civil Services Exam | RAS RPSC Prelims Preparation - Notes

,MCQs

,Indian Economy

,Objective type Questions

,video lectures

,practice quizzes

,4. Monetary Policies

,Indian Economy

,Important questions

;

4. Monetary Policies, Indian Economy, Civil Services Exam Free PDF Download

Importance of 4. Monetary Policies, Indian Economy, Civil Services Exam

4. Monetary Policies, Indian Economy, Civil Services Exam Notes

4. Monetary Policies, Indian Economy, Civil Services Exam RPSC RAS (Rajasthan) Questions

Study 4. Monetary Policies, Indian Economy, Civil Services Exam on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|