NCERT Solution: Accounting for Partnership-Basic Concepts | Accountancy Class 12 - Commerce PDF Download

Short Question Answers

Q1: Define Partnership Deed.

Ans: Partnership Deed is a written agreement among the partners of a partnership firm. It includes agreement on profit sharing ratio, salaries, commission of partners, interest provided on partner's capital and drawings and interest on loan given or taken by the partners, etc. Generally following details are included in a partnership deed.

1. Objective of business of the firm

2. Name and address of the firm

3. Name and address of all partners

4. Profit and loss sharing ratio

5. Contribution to capital by each partner

6. Rights, types of roles and duties of partners

7. Duration of partnership

8. Rate of interest on capital, drawings and loans

9. Salaries, commission, if payable to partners.

10. Rules regarding admission, retirement, death and dissolution of the firm, etc.

Q2: Why is it desirable to make the partnership agreement in writing. Explain in 50 words.

Ans: Partnership agreement may be oral or written. It is not compulsory to form partnership agreement in writing under the Partnership Act, 1932. However, written partnership deed is desirable than oral agreement as it helps in avoiding disputes and misunderstandings among the partners. Also, it helps in settling disputes (as the case may be) among the partners, as written partnership deed can be referred to anytime. If written partnership deed is duly signed and registered under Partnership Act, then it can be used as evidence in the court of law.

Q3: List the items which may be debited or credited in the capital accounts of the partners when:

(i) Capitals are fixed

(ii) Capitals are fluctuating

Ans:

(i) When Capitals are fixed

The following items are credited in the Partner's Capital Account when capital accounts are fixed.

(a) Opening balance of capital

(b) Additional capital introduced during an accounting year

The following items are debited in the Partner's Capital Account when capital accounts are fixed.

(a) Part of capital withdrawn

(b) Closing balance of capital

(ii)When Capitals are fluctuating

The following items are credited in the Partner's Capital Account when capital accounts are fluctuating.

(a) Opening balance of capital.

(b) Additional capital introduced during an accounting year

(c) Salaries to the partners

(d) Interest on capital

(e) Share of profit

(f) Commission and bonus to the partners

The following items are debited in the Partner's Capital Account when capital accounts are fluctuating.

(a) Drawings made during the accounting period

(b) Interest on drawings.

(c) Share of loss.

(d) Closing balance of capital.

Q4: Why is Profit and Loss Adjustment Account prepared? Explain.

Ans: The Profit and Loss Adjustment Account is prepared because of the following two reasons.

1. To record omitted items and rectify errors if any- After the preparation of Profit and Loss Account and Balance Sheet, if any error or omission is noticed, then these errors or omissions are adjusted by opening Profit and Loss Adjustment Account in the subsequent accounting period without altering old Profit and Loss Account.

2. To distribute profit or loss between the partners- Sometimes, besides adjusting the items and rectifying errors, this account is also used for distribution of profit (or loss) among the partners. In this situation, this account acts as a substitute for Profit and Loss Appropriation Account. The main rationale to prepare the Profit and Loss Adjustment Account is to ascertain true profit or loss.

Q5:Give two circumstances under which the fixed capitals of partners may change.

Ans:

The following are the two circumstances under which the fixed capitals of partner may change.

(i) If any additional capital is introduced by the partner during the year.

(ii) If any part of capital is permanently withdrawn by the partner from the firm.

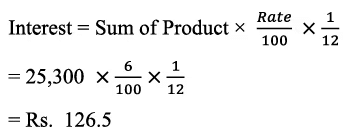

Q6: If a fixed amount is withdrawn on the first day of every quarter, for what period the interest on total amount withdrawn will be calculated?

Ans: If a fixed amount is withdrawn on the first day of every quarter, then the interest is calculated on the amount withdrawn for a period of seven and half ( )months.

)months.

Example: If a partner withdraws Rs. 5,000 in the beginning of each quarter and the interest is charged @ 10% on the drawings, then interest on drawings is calculated as:

Total drawings made by the partner during the whole year are Rs 20,000, i.e. Rs 5000× 4.

Interest on drawings =  Q7: In the absence of partnership deed, specify the rules relating to the following:

Q7: In the absence of partnership deed, specify the rules relating to the following:

(i) Sharing of profits and losses.

(ii) Interest on partner’s capital.

(iii) Interest on Partner’s drawings.

(iv) Interest on Partner’s loan

(v) Salary to a partner.

Ans:

(i) Sharing of profits and losses: If the partnership deed is silent on sharing of profit or losses among the partners of a firm, then according to the Partnership Act of 1932, profits and losses are to be shared equally by all the partners of the firm.

(ii) Interest on partner’s capital: If the partnership deed is silent on interest on partner’s capital, then according to the Partnership Act of 1932, no interest on capital should be given to the partners of the firm.

(iii) Interest on partner’s drawings: If the partnership deed is silent on interest on partner’s drawings, then according to the Partnership Act of 1932, no interest on drawing should be charged from the partners of the firm for the amount of capital withdrawn in form of drawings.

(iv)Interest on partner’s loan: If the partnership deed is silent on interest on partner’s loan, then according to the Partnership Act of 1932, the partners are entitled for 6% p.a. interest on the loan forwarded by them to the firm.

(v) Salary to a partner: If the partnership deed is silent on salary to a partner, then according to the Partnership Act of 1932, no salary should be given to any partner.

Long Question Answers

Q1: What is meant by partnership? Explain its chief characteristics? Explain

Ans: According to Sec 4 of the Partnership Act 1932, partnership is a mutual agreement between two or more partners who decide to enter into a partnership deed or agreement and share profit or losses as agreed upon. People who join hands together are known as partners and collectively it is called a firm. The important characteristics of partnership are:

- Two or more people: To enter into a partnership, there must be at least two or more people with a common goal. The maximum number of partners can be 20 for businesses other than banking and banking they must be 10.

- Partnership deed: A partnership relation is an outcome of an agreement between two or more parties. Certain terms and conditions bind the partners into a relationship. The document which contains the written agreement is called the partnership deed.

- Business: A partnership should be formed to carry out legal business because any type of illegality will not be a valid business.

- Profit and loss sharing: There is sharing of profits and losses equally or at a ratio agreed upon by the partners.

- Liability: There is unlimited liability under the partnership. If the partners are liable to pay to the third party, even their personal property would not be spared.

Q2: Discuss the main provisions of the Indian Partnership Act 1932 that are relevant to partnership accounts if there is no partnership deed.

Ans: There must be a partnership deed among the partners before entering into a partnership. However, the law has not made it compulsory to prepare a partnership deed for the creation of mutual agreement between the partners in a partnership. In the absence of a partnership deed, the below rules apply.

(i) Sharing of profits and losses: Partners are entitled to share equally the profits earned by the firm and contribute equally to the losses sustained by the firm.

(ii) Interest on partners’ capital: Partners are not entitled to any interest on capital balances. Sec 13, clause c provides that the interest on capital is payable out of profits only, where there is agreement for interest on capital payment.

(iii) Interest on Partner’s drawings: No interest is to be charged on partners’ drawings.

(iv) Interest on partner’s loan or advances: - Interest of 6% p.a. is allowed on any loan other than capital.

(v) Right to remuneration: Partners are not entitled to any salary or remuneration or commission for taking part in the conduct of the business or for services rendered.

Q3: Explain why it is considered better to make a partnership agreement in writing.

Ans: Partnership relation is an outcome of an agreement between two or more parties. Certain terms and conditions bind the partners into a relationship. The document which contains the written agreement is called the partnership deed. It is always desirable to make the partnership agreement in writing. It is safer and more prudent as the written agreement turns out to be helpful in case of disputes which can be referred to in the future. It ensures the smooth functioning of the business as it helps in settling the disputes if any. Partners might be sharing very good relations now but there is no guarantee the relations remain the same in the future. Hence, to keep up the good relations and give legality to the business it is always advisable to make partnership agreements in writing to make the terms and conditions clear.

Q4: Illustrate how interest on drawings will be calculated under various situations.

Ans: The interest on the drawing is an income for the organization as the drawings are referred to as the amounts which are withdrawn by the partners of the organization from the firm for their personal use. Thus, organizations are expected to charge the interest in the drawings which are made by the Partners. The method of calculation of the interest in the drawings is dependent upon the time and the frequency of the drawings. Following are the cases when the interest on the drawings is calculated by the organization:

- When the information about the amount, date and the rate of the interest on the drawing is mentioned.

- When the information of the Date or time is not given but the rate of interest p.a. and the amount is given. In such cases, the time is considered to be 6 months.

- When the fixed amount is withdrawn at regular intervals. This can happen at the beginning, middle or the end of each month. When the withdrawals are made at the beginning of the month then the annual interest is calculated for 6.5 months. similarly, for the withdrawals made in the middle of the month, the interest is calculated for 5.5 months, and the withdrawals made in the mid of each month are calculated for 6 months. Similarly, for the withdrawals made at the beginning of the quarter, the rate of interest is calculated for 7.5 months, for the withdrawals made at the end of every quarter the rate of interest is calculated at 4.5 months.

- When the different amount is withdrawn by the partner at different points of causes withdrawals at irregular intervals. Thus, in such cases, the drawings have to be calculated by the Product Method as per which the interest on the drawings is calculated by the sum of the products of the time and the drawings for one unit of time.

Q5: How will you deal with a change in profit sharing ratio among existing partners? Take imaginary figures to illustrate your answer.

Ans: The changes in the profit-sharing ratio of the partners occur during the admission, retirement or death of the partner of the organization. Furthermore, the general agreement between the existing partners of the organization may also change the profit-sharing ratio of the partners. This hence results in the loss of the other partners and the gain for one of the partners of the organization. Thus, the gaining partner must compensate the partners who experience the share in the profit and the loss sharing ratio.

The issues such as the calculation of the goodwill and change in profit sharing ratio among existing partners take place only in case of admission, retirement and death of a partner. A general agreement among the partners may also result in a change in the PSR. It results in gain to one partner and loss to another. Hence, the gaining partner must compensate the losing partner. Many issues must be looked into like goodwill, reserves, capital adjustment, profit or loss on the revaluation of assets or liabilities. In the case of goodwill, goodwill is calculated, and a proportionate amount is given by the partner who gains to the partner who loses. The gaining partner’s capital account is debited (gain) and the sacrificing partner’s capital account is credited (sacrifice amount). The gaining ratio and sacrificing ratio are calculated to distribute compensation from one to the other.

Example: X and Y share profits in the ratio of 3:1. They decided to share profits in the ratio of 5:3. The goodwill is valued at 2, 40,000. The following adjustment entry will be passed.

Old ratio = X is ¾ and Y is ¼

New ratio = X is 5/8 and Y is 3/8

Y gains by 3/8-1/4 = 1/8

X loses by ¾ -5/8 = 1/8

Y will pay X 1/8 of 240,000 =30,000

Journal entry will be:

Y’s capital account … Dr 30000

To X’s capital account …. 30000

Numerical Question Answers:

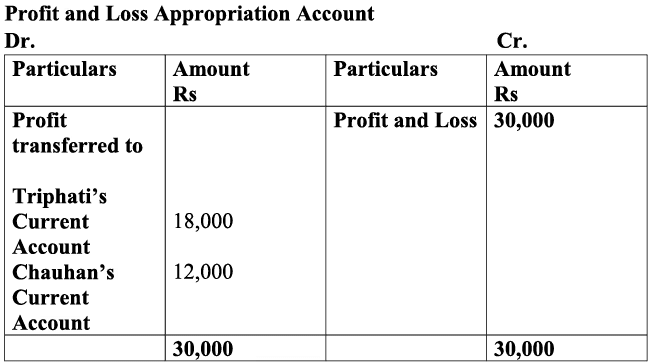

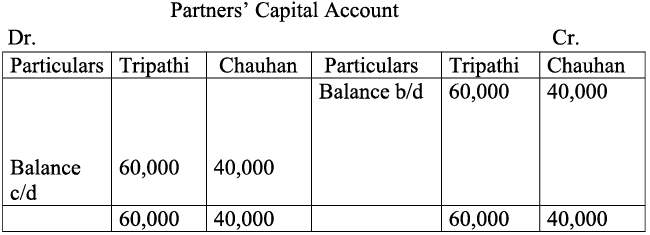

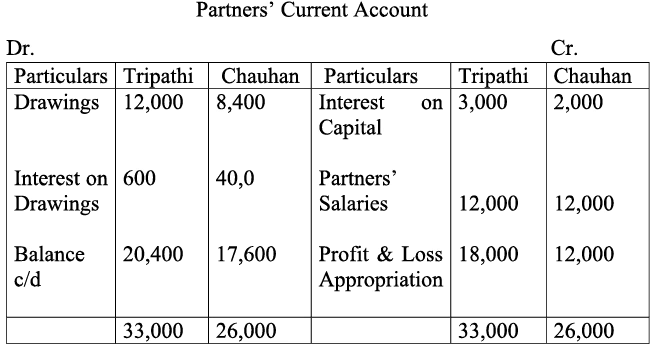

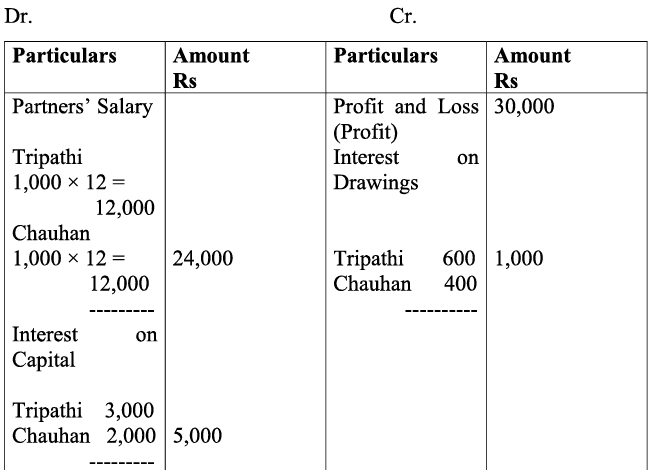

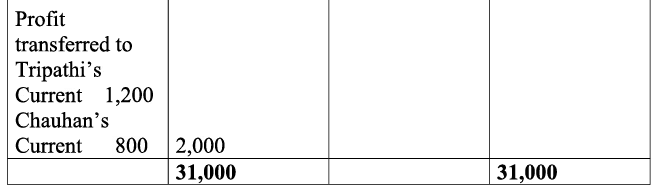

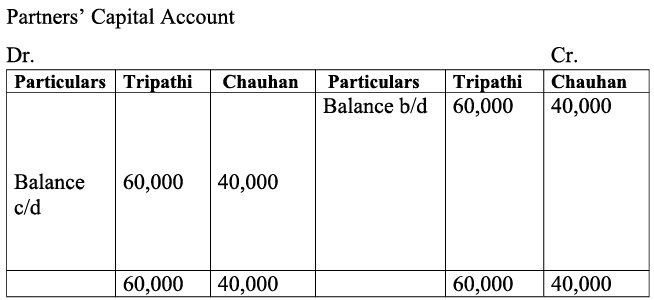

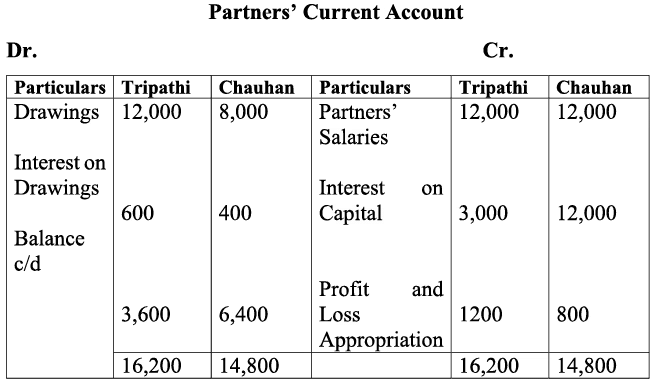

Q1: Triphati and Chauhan are partners in a firm sharing profits and losses in the ratio of 3:2. Their capitals were Rs. 60,000 and Rs. 40,000 as on January 01, 2005. During the year they earned a profit of Rs. 30,000. According to the partnership deed both the partners are entitled to Rs. 1,000 per month as Salary and 5% interest on their capital. They are also to be charged an interest of 5% on their drawings, irrespective of the period, which is Rs. 12,000 for Tripathi, Rs. 8,000 for Chauhan. Prepare Partner’s Accounts when, capitals are fixed.

Ans: a) If interest on Capital and Partners’ salaries and interest on drawings is charged against profit, the solution will be as:

b) If interest on Capital and Partners’ salaries and interest on drawings is distributed out of profit, the solution will be as:

As the question is silent about the treatment of Interest on Capitals, Salary, Interest on Drawings, so we have prepared the solution by following two methods, namely:

- Charge against Profits

- Out of Profits

This was done deliberately so as to make students aware-off the two above mentioned methods and also to match the answer with that of given in the NCERT. The appropriate answer to the question following Out of Profit Method should be as:

Tripathi's Current A/c balance Rs 3,600 and

Chauhan's Current A/c balance Rs 6,400.

In case no information regarding the treatment of above items is mentioned in the question, then we usually follow the Out of Profits Method.

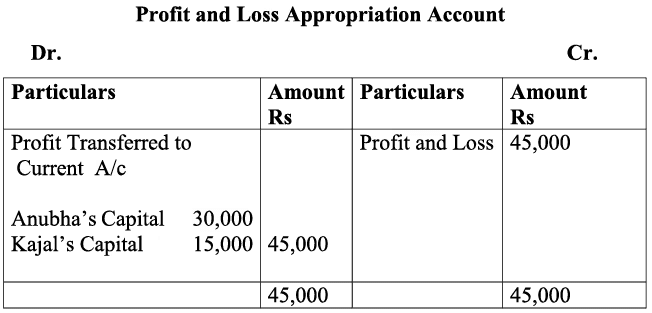

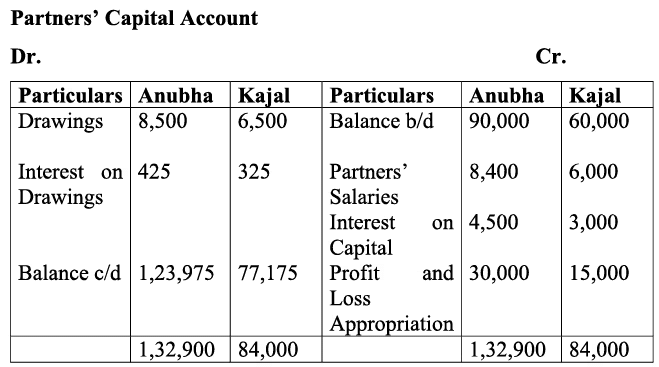

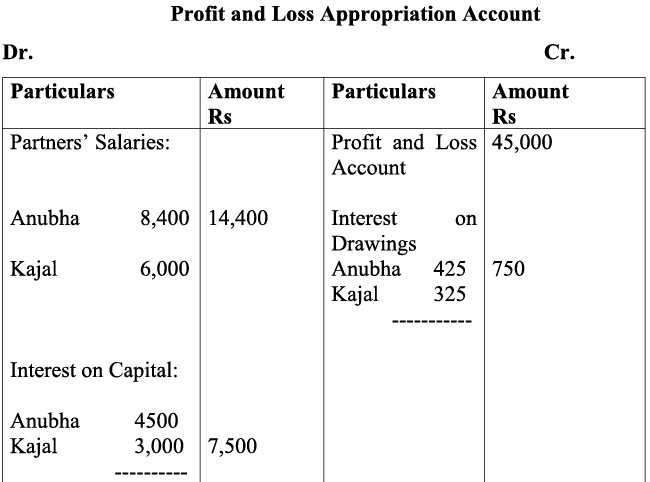

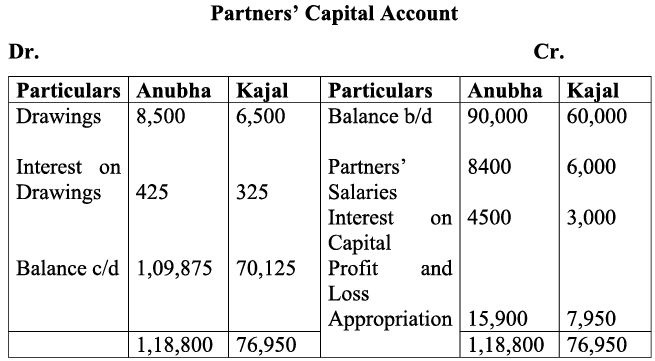

Q2: Anubha and Kajal are partners of a firm sharing profits and losses in the ratio of 2:1. Their capital, were Rs. 90,000 and Rs. 60,000. The profit during the year were Rs. 45,000. According to partnership deed, both partners are allowed salary, Rs. 700 per month to Anubha and Rs. 500 per month to Kajal. Interest allowed on capital @ 5% p.a. The drawings at the end of the period were Rs. 8,500 for Anubha and Rs. 6,500 for Kajal. Interest is to be charged @ 5% p.a. on drawings. Prepare partners capital accounts, assuming that the capital account are fluctuating.

Ans:

a) Note: If Partners’ Salaries, Interest on capital and Interest on Drawing are treated as these have already adjusted in Profit and Loss Account. The Solution will be as

b) Alternative

Note: If Partners’ salaries, interest on capital and interest on drawings adjusted in Profit and Loss Appropriation Account. The solution will be as.

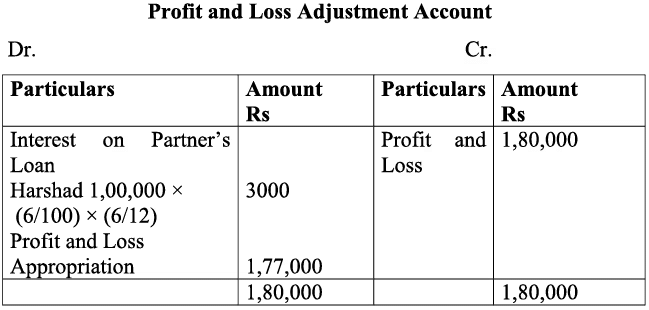

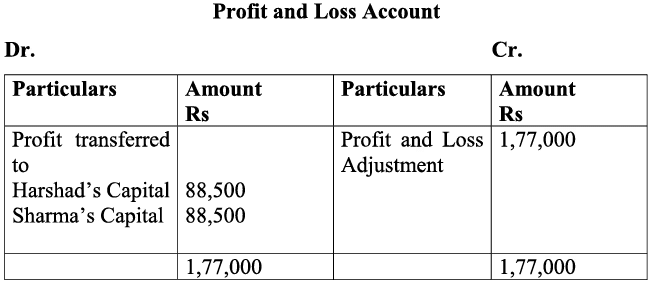

Q3: Harshad and Dhiman are in partnership since April 01, 2019. No Partnership agreement was made. They contributed Rs. 4,00,000 and 1,00,000 respectively as capital. In addition, Harshad advanced an amount of Rs. 1,00,000 to the firm, on October 01, 2019. Due to long illness, Harshad could not participate in business activities from August 1, to September 30, 2016. The profits for the year ended March 31, 2020 amounted to Rs. 1,80,000. Dispute has arisen between Harshad and Dhiman.

Harshad Claims:

(i) He should be given interest @ 10% per annum on capital and loan;

(ii) Profit should be distributed in proportion of capital;

Dhiman Claims:

(i) Profits should be distributed equally;

(ii) He should be allowed Rs 2,000 p.m. as remuneration for the period he managed the business, in the absence of Harshad;

(iii) Interest on Capital and loan should be allowed @ 6% p.a.

You are required to settle the dispute between Harshad and Dhiman. Also prepare Profit and Loss Appropriation Account.

Ans:

DISTRIBUTION OF PROFITS

Harshad Claims:

Decisions

(i) If there is no agreement on interest on partner’s capital, according to Indian partnership act 1932, no interest will be allowed to partners.

(ii) If there is no agreement on the matter of profit sharing, according to partnership act 1932, profit shall be distributed equally.

Dhiman Claims:

Decisions

(i) Dhiman claim is justified, according partnership act 1932 if there is no agreement on the matter of profit distribution, profit shall be distributed equally.

(ii) No salary will be allowed to any partner because there is no agreement on matter of remuneration.

(iii) Dhiman’s claim is not justified on the matter of interest on capital but justified on the matter of interest on loan. If there is no agreement on interest on partner’s loan, Interest shall be provided at 6% p.a.

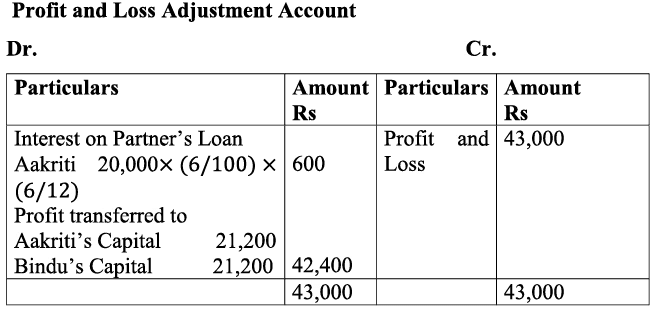

Q4: Aakriti and Bindu entered into partnership for making garment on April 01, 2019 without any Partnership agreement. They introduced Capitals of Rs. 5,00,000 and Rs. 3,00,000 respectively on October 01, 2019. Aakriti Advanced. Rs, 20,000 by way of loan to the firm without any agreement as to interest. Profit and Loss account for the year ended March 31 2020 showed profit of Rs, 43,000. Partners could not agree upon the question of interest and the basis of division of profit. You are required to divide the profits between them by preparing Profit and Loss Appropriation Account. Also give reasons in Support of your answer

Ans:

Reason:

a) Interest on partners loan shall be allowed at 6% p.a. because there is no partnership agreement.

b) Interest on capital shall not be allowed because there is no agreement on interest on capital.

c) Profit shall be distributed equally because profit sharing ratio has not been given.

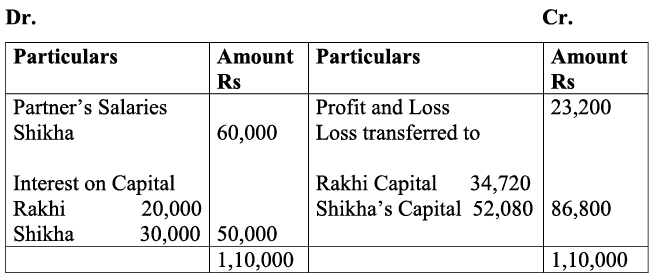

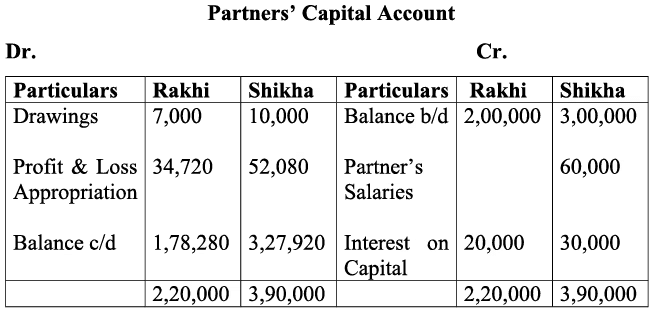

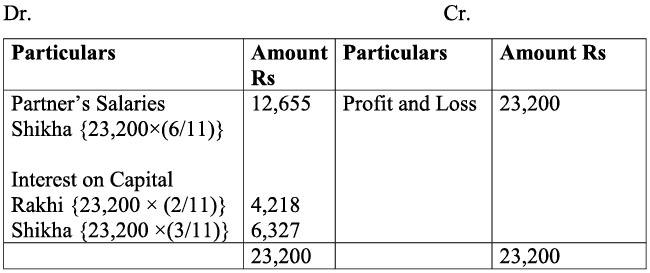

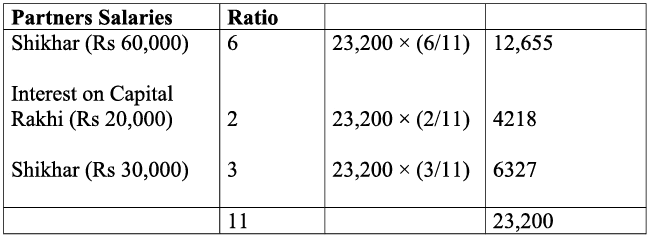

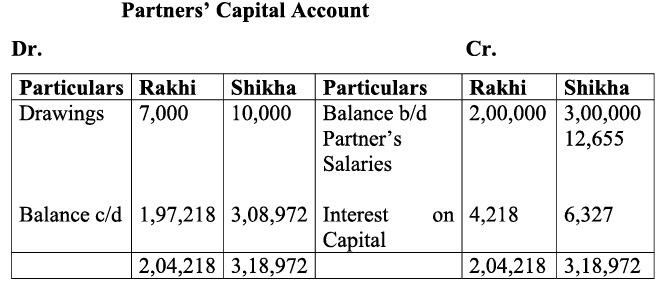

Q5: Rakhi and Shikha are partners in a firm, with capitals of Rs. 2,00,000 and Rs, 3,00,000 respectively. The profit of the firm, for the year ended 2016-17 is Rs. 23,200. As per the Partnership agreement, they share the profit in their capital ratio, after allowing a salary of Rs. 5,000 per month to Shikha and interest on Partner’s capital at the rate of 10% p.a. During the year Rakhi withdrew Rs. 7,000 and Shikha Rs. 10,000 for their personal use. As per partnership deed, salary and interest on capital appropriation treated as charge on profit. You are required to prepare Profit and Loss Appropriation Account and Partner’s Capital Accounts.

Ans:

If interest on capital and Partners’ salaries will be provided even if firm involves in loss.

If interest on capital and salaries will be provided out of profit Profit and Loss Appropriation Account

If interest on capital and salaries will be provided out of profit Profit and Loss Appropriation Account

If profit is less than the sum of distributable items, distribution shall be in proportion of items for distribution.

If profit is less than the sum of distributable items, distribution shall be in proportion of items for distribution.

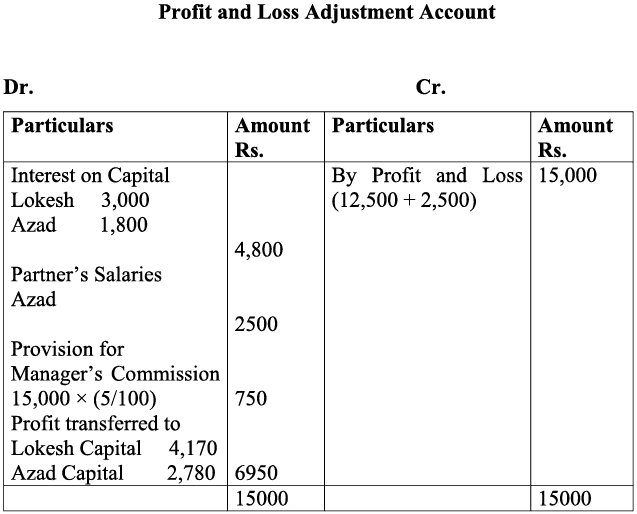

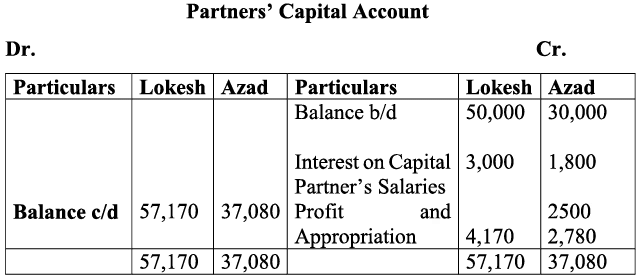

Q6: Lokesh and Azad are partners sharing profits in the ratio 3:2, with capitals of Rs. 50,000 and 30,000, respectively. Interest on capital is agreed to be paid @ 6% p.a. Azad is allowed a salary of Rs. 2,500 p.a. During 2016, the profits prior to the calculation of interest on capital but after charging Azad’s salary amounted to Rs. 12,500. A provision of 5% of profits is to be made in respect of manager’s commission. Prepare partner’s capital accounts and profit and loss Appropriation Account.

Ans:

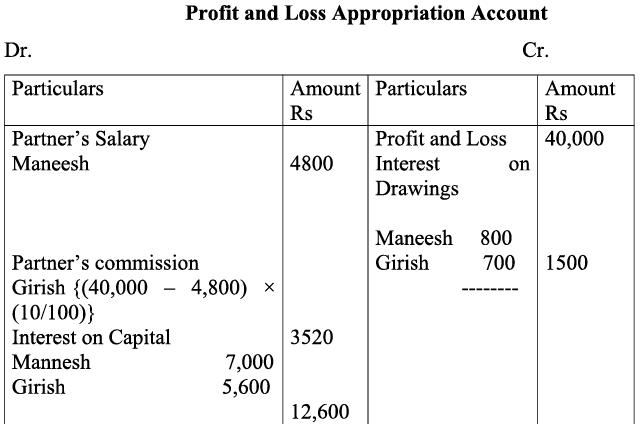

Q7: The partnership agreement between Maneesh and Girish provides that:

(i) Profits will be shared equally;

(ii) Maneesh will be allowed a salary of Rs. 400 p.m;

(iii) Girish who manages the sales department will be allowed a commission equal to 10% of the net profits, after allowing Maneesh’s salary;

(iv) 7% p.a. interest will be allowed on partner’s fixed capital;

(v) 5% p.a. interest will be charged on partner’s annual drawings;

(vi) The fixed capitals of Maneesh and Girish are Rs. 1,00,000 and Rs. 80,000, respectively. Their annual drawings were Rs. 16,000 and 14,000, respectively. The net profit for the year ending March 31, 2019 amounted to Rs. 40,000;

Ans:

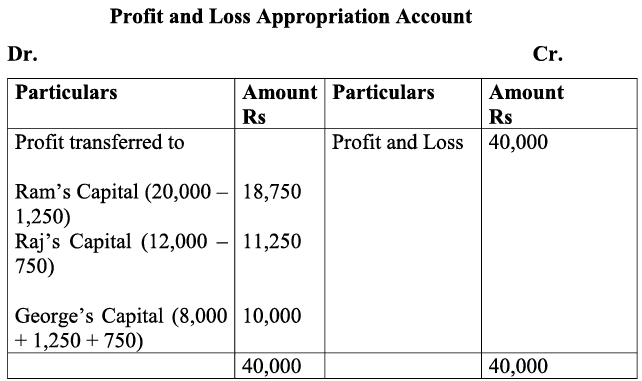

Q8: Ram, Raj and George are partners sharing profits in the ratio 5 : 3 : 2. According to the partnership agreement George is to get a minimum amount of Rs. 10,000 as his share of profits every year. The net profit for the year 2013 amounted to Rs, 40,000. Prepare the Profit and Loss Appropriation Account.

Ans:

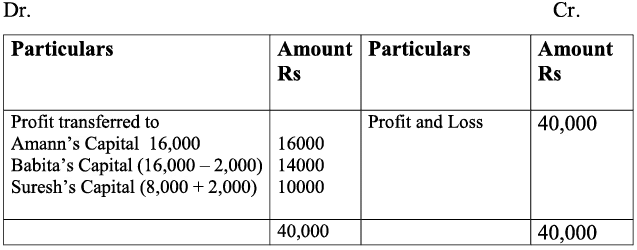

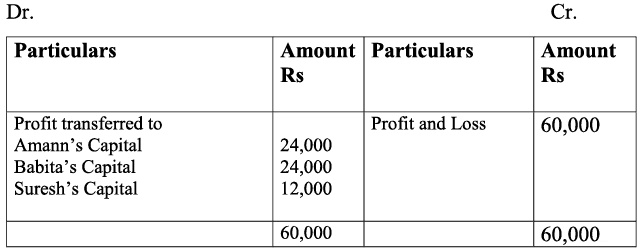

Q9: Amann, Babita and Suresh are partners in a firm. Their profit sharing ratio is 2:2:1. Suresh is guaranteed a minimum amount of Rs. 10,000 as share of profit, every year. Any deficiency on that account shall be met by Babita. The profits for two years ending December 31, 2019 and December 31, 2020 were Rs. 40,000 and Rs. 60,000, respectively. Prepare the Profit and Loss Appropriation Account for the two years.

Ans: Profit and Loss Appropriation Account for the year ended 31st March 2019 Profit and Loss Appropriation Account for the year ended 31st March 2019.

Profit and Loss Appropriation Account for the year ended 31st March 2019.

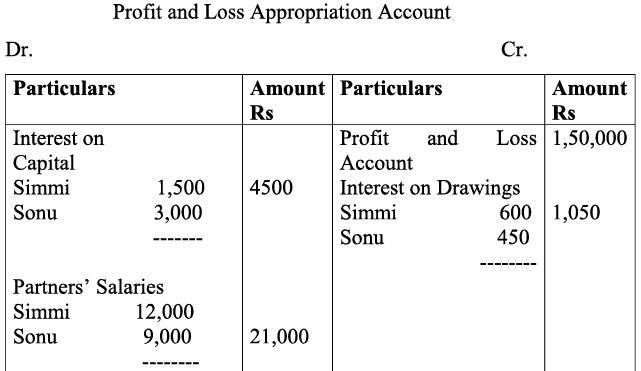

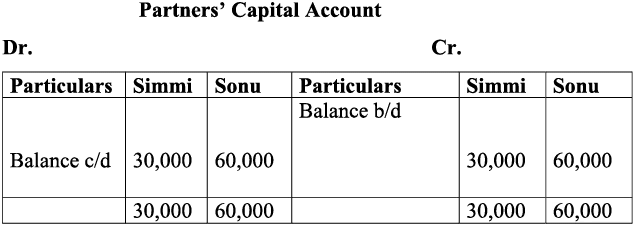

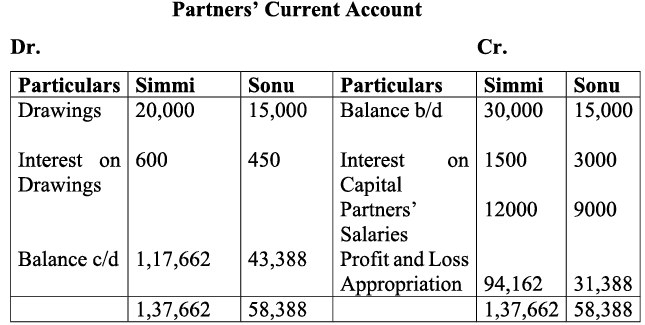

Q10: Simmi and Sonu are partners in a firm, sharing profits and losses in the ratio of 3:1. The profit and loss account of the firm for the year ending March 31, 2020 shows a net profit of Rs. 1,50,050. Prepare the Profit and Loss Appropriation Account and partners current account by taking into consideration the following information:

(i) Partners capital on April 1, 2019

Simmi, Rs 30,000; Sonu, Rs 60,000;

(ii) Current accounts balances on April 1, 2019;

Simmi, Rs 30,000 (cr.); Sonu, Rs 15,000 (cr.);

(iii) Partners drawings during the year amounted to

Simmi, Rs 20,000; Sonu, Rs. 15,000;

(iv) Interest on capital was allowed @ 5% p.a.;

(v) Interest on drawing was to be charged @ 6% p.a. at an average of six months;

(vi) Partners’ salaries : Simmi Rs. 12,000 and Sonu Rs. 9,000. Also show the partners’ current accounts.

Ans:

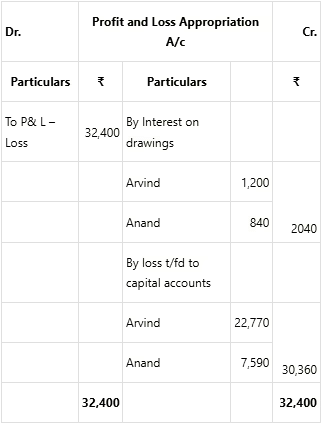

Q11: Arvind and Anand are partners sharing profits and losses in the ratio 8 : 3 : 1. Balances in their capital accounts on April 01, 2019 were, Arvind- Rs. 4,40,000 and Anand Rs. 2,60,000. As per their agreement, partners were entitled to interest on capital @ 5% p.a., and interest on drawings was to be charged @ 6% p.a. Arvind was allowed an annual salary of Rs. 35,000/- for the additional responsibilities taken up by him. Partners drawings for the year were, I Arvind Rs. 40,000 and Anand Rs. 28,000. Profit and loss account of the firm for the year ending March 31, 2020 showed a Net Loss of Rs. 32,400. Prepare Profit and Loss Appropriation Account.

Ans:

No salary and interest on capital will be allowed in case of loss. Interest on drawings:

Arvind = 40,000 × 6/100 × 6/12 = Rs. 1,200

Anand = 28,000 × 6/100 × 6/12 = Rs. 840

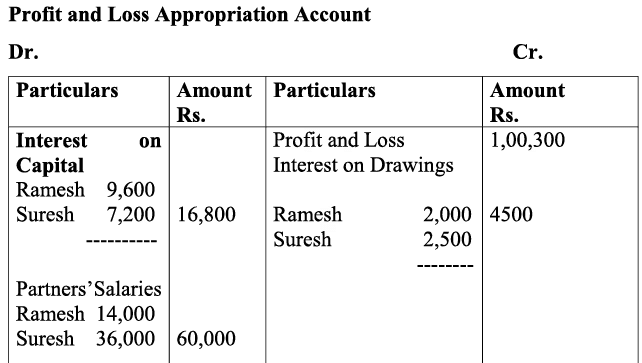

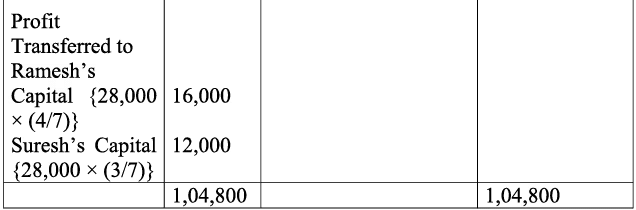

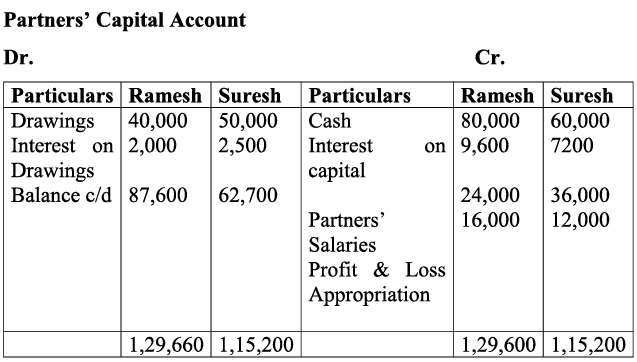

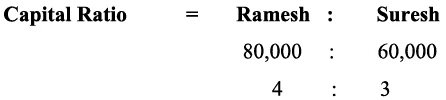

Q12: Ramesh and Suresh were partners in a firm sharing profits in the ratio of their capitals contributed on commencement of business which were Rs 80,000 and Rs 60,000 respectively. The firm started business on April 1, 2016. According to the partnership agreement, interest on capital and drawings are 12% and 10% p.a., respectively. Ramesh and Suresh are to get a monthly salary of Rs 2,000 and Rs. 3,000, respectively.

The profits for year ended March 31, 2017 before making above appropriations was Rs. 1,00,300. The drawings of Ramesh and Suresh were Rs. 40,000 and Rs. 50,000, respectively. Interest on drawings amounted to Rs. 2,000 for Ramesh and Rs. 2,500 for Suresh. Prepare Profit and Loss Appropriation Account and partners’ capital accounts, assuming that their capitals are fluctuating.

Ans:

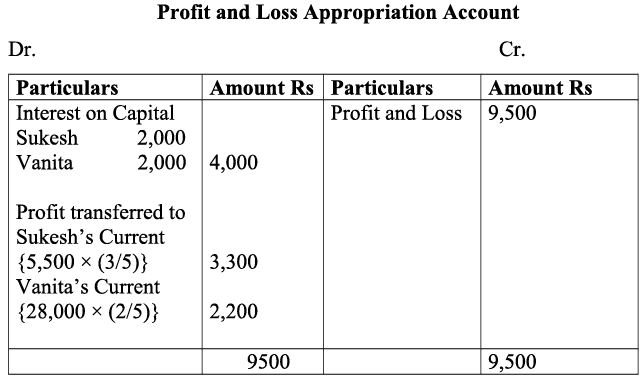

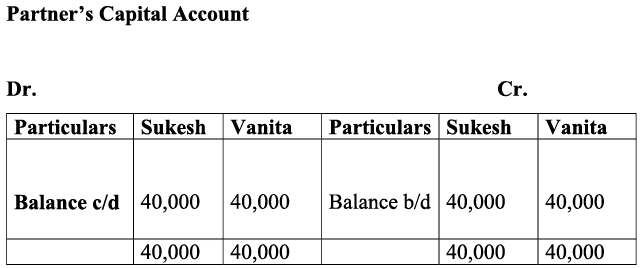

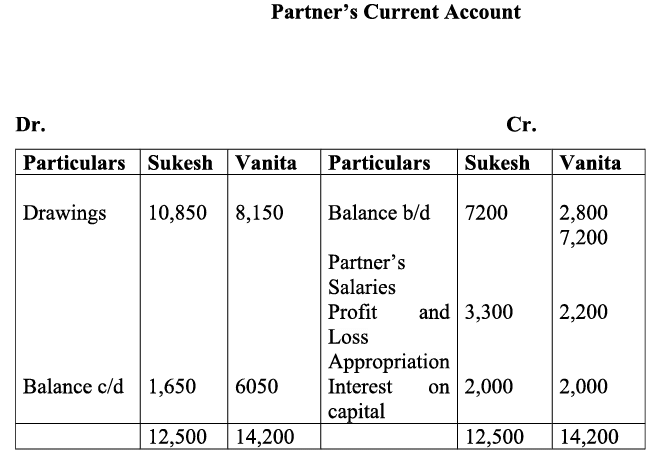

Q13: Sukesh and Vanita were partners in a firm. Their partnership agreement provides that:

(i) Profits would be shared by Sukesh and Vanita in the ratio of 3:2;

(ii) 5% interest is to be allowed on capital;

(iii) Vanita should be paid a monthly salary of Rs 600.

The following balances are extracted from the books of the firm, on December 31, 2017.

Net profit for the year, before charging interest on capital and after charging partner’s salary was Rs 9,500. Prepare the Profit and Loss Appropriation Account and the Partner’s Current Accounts.

Ans:

Q14: Rahul, Rohit and Karan started partnership business on April 1, 2019 with capitals of Rs. 20,00,000, Rs. 18,00,000 and Rs. 16,00,000, respectively. The profit for the year ended March 2020 amounted to Rs.1,35,000 and the partner’s drawings had been Rahul Rs. 50,000, Rohit Rs. 50,000 and Karan Rs. 40,000. The profits are distributed among partner’s in the ratio of 3:2:1.

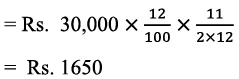

Calculate the interest on capital @ 5% p.a.

Ans:

Interest on Capital

Rahul = 20,00,000 × 5/100 = Rs 1,00,000

Rohit = 18,00,000 × 5/100= Rs 90,000

Karan = 16,00,000 × 5/100 = Rs 80,000

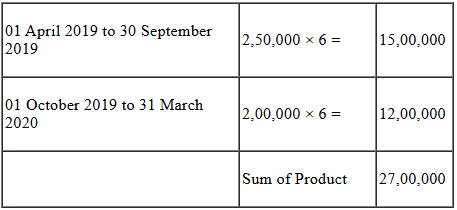

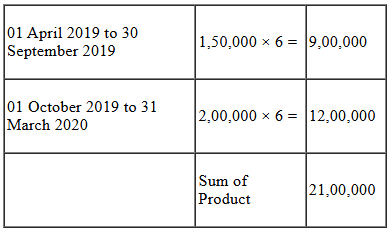

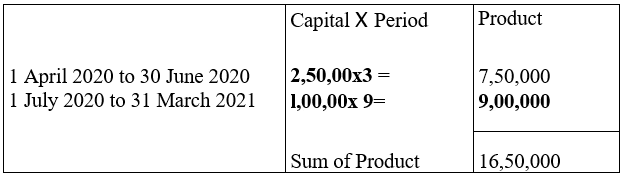

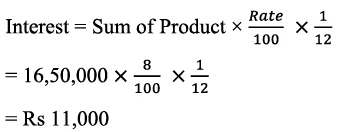

Q15: Sunflower and Pink Rose started partnership business on April 01, 20019 with capitals of Rs 2,50,000 and Rs 1,50,000, respectively. On October 01, 2019, they decided that their capitals should be Rs 2,00,000 each. The necessary adjustments in the capitals are made by introducing or withdrawing cash. Interest on capital is to be allowed @ 10% p.a. Calculate interest on capital as on March 31, 2020.

Ans:

Product Method

Sunflower

Pink Rose Interest on Capital =

Interest on Capital =

Interest on Sunflower's Capital =

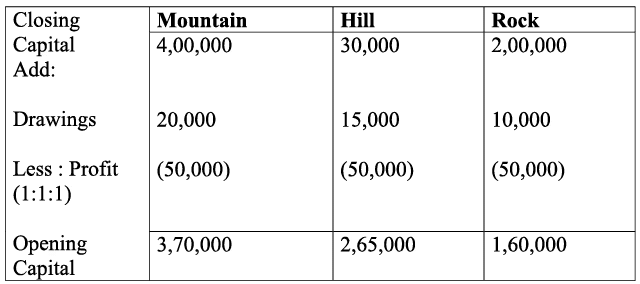

Interest on Pink Rose's Capital =  Q16: On March 31, 2017 after the close of accounts, the capitals of Mountain, Hill and Rock stood in the books of the firm at Rs. 4,00,000, Rs.3,00,000 and Rs. 2,00,000, respectively. Subsequently, it was discovered that the interest on capital @ 10% p.a. had been omitted. The profit for the year amounted to Rs. 1,50,000 and the partner’s drawings had been Mountain: Rs. 20,000, Hill Rs. 15,000 and Rock Rs. 10,000. Calculate interest on capital.

Q16: On March 31, 2017 after the close of accounts, the capitals of Mountain, Hill and Rock stood in the books of the firm at Rs. 4,00,000, Rs.3,00,000 and Rs. 2,00,000, respectively. Subsequently, it was discovered that the interest on capital @ 10% p.a. had been omitted. The profit for the year amounted to Rs. 1,50,000 and the partner’s drawings had been Mountain: Rs. 20,000, Hill Rs. 15,000 and Rock Rs. 10,000. Calculate interest on capital.

Ans:

Generally interest on Capital is calculated on opening balance of capital. If additional capital is not given.

Interest on Capital

Mountain = 3,70,000 X (10/100) = Rs. 37,000

Hill = 2,65,000x (10/100) = Rs. 26,500

Rock 1,60,000 X (10/100) = Rs. 16,000

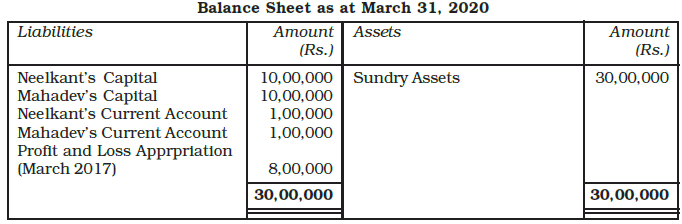

Q17: Following is the extract of the Balance Sheet of, Neelkant and Mahdev as on March 31, 2020:

During the year Mahadev’s drawings were Rs 30,000. Profits during 2019-20 is Rs 10,00,000. Calculate interest on capital @ 5% p.a for the year ending March 31, 2020.

During the year Mahadev’s drawings were Rs 30,000. Profits during 2019-20 is Rs 10,00,000. Calculate interest on capital @ 5% p.a for the year ending March 31, 2020.

Answer:

Interest on Capital

Neelkant's 10,00,000* (5/100)= Rs 50,000

Mahadev's 10,00,000 * (5/100)= Rs 50,000

Note: In this question, as the balances of both Partner's Capital Account and of Partner's Current Account are mentioned, so it has been assumed that the capital of the partners is fixed.

As we know, when the capital of the partners is fixed, drawings and interest on capital does not affect the capital balances of the partners. Rather, it would affect their current account balances. Therefore, in this case, capital at the beginning (i.e. opening capital) and capital at the end (i.e. closing capital) of the year would remain same. Thus, the interest on capital is calculated on fixed capital balances (given in the Balance Sheet of the question).

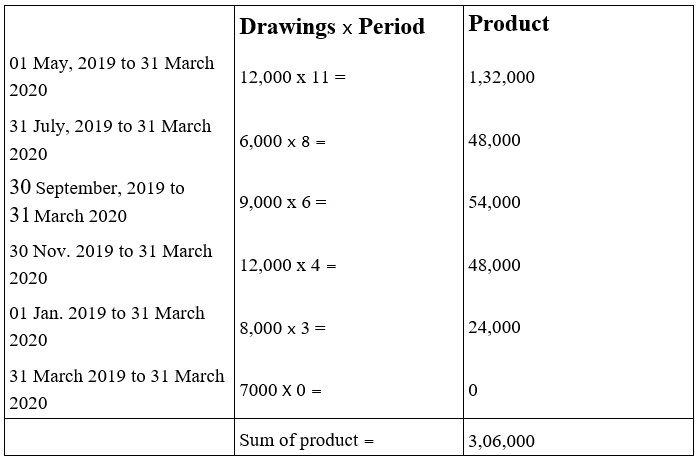

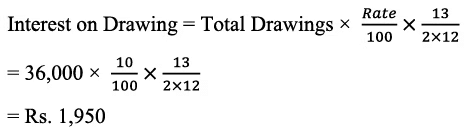

Q18: Rishi is a partner in a firm. He withdrew the following amounts during the year ended March 31, 2020.

May 01, 2019 - Rs. 12,000

July 31, 2019 - Rs. 6,000

September 30, 2019 - Rs. 9,000

November 30, 2019 - Rs. 12,000

January 01, 2020 - Rs. 8,000

March 31, 2020 - Rs. 7,000

Interest on drawings is charged @ 9% p.a. Calculate interest on drawings

Ans:  Here the formula will be

Here the formula will be

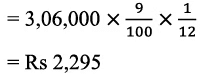

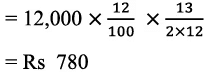

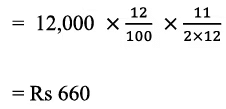

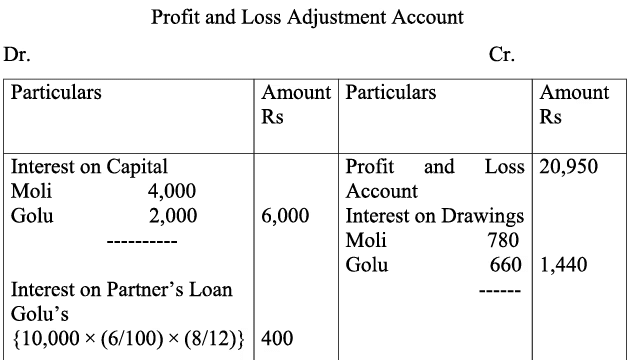

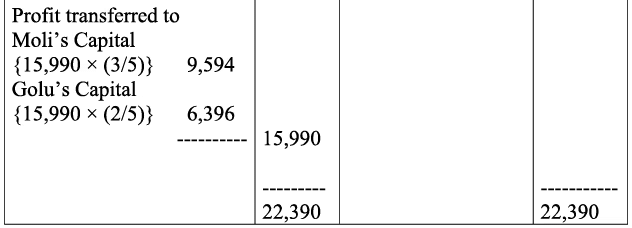

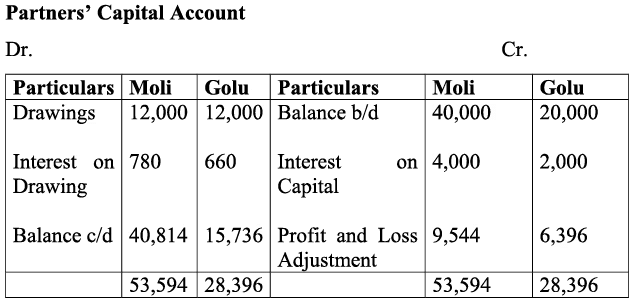

Q19: The capital accounts of Moli and Golu showed balances of Rs.40,000 and Rs. 20,000 as on April 01, 2019. They shared profits in the ratio of 3:2. They allowed interest on capital @ 10% p.a. and interest on drawings, @ 12 p.a. Golu advanced a loan of Rs. 10,000 to the firm on August 01, 2019. During the year, Moli withdrew Rs. 1,000 per month at the beginning of every month whereas Golu withdrew Rs. 1,000 per month at the end of every month. Profit for the year, before the above mentioned adjustments was Rs.20,950. Calculate interest on drawings show distribution of profits and prepare partner’s capital accounts.

Q19: The capital accounts of Moli and Golu showed balances of Rs.40,000 and Rs. 20,000 as on April 01, 2019. They shared profits in the ratio of 3:2. They allowed interest on capital @ 10% p.a. and interest on drawings, @ 12 p.a. Golu advanced a loan of Rs. 10,000 to the firm on August 01, 2019. During the year, Moli withdrew Rs. 1,000 per month at the beginning of every month whereas Golu withdrew Rs. 1,000 per month at the end of every month. Profit for the year, before the above mentioned adjustments was Rs.20,950. Calculate interest on drawings show distribution of profits and prepare partner’s capital accounts.

Ans:

Interest on Moli’s Drawing

Interest on Golu’s Drawings

Interest on Golu’s Drawings

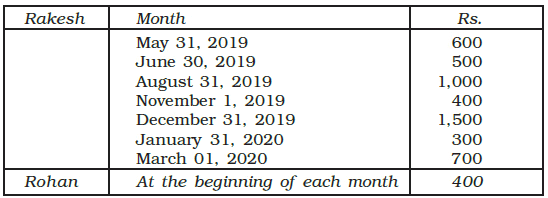

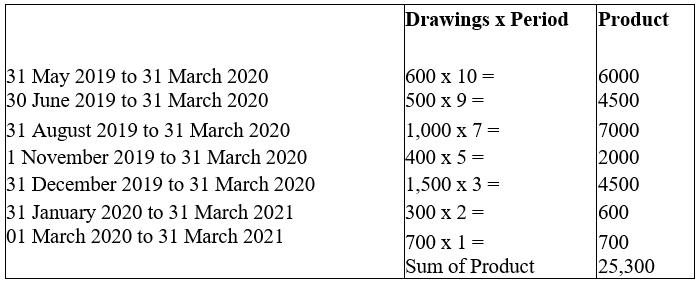

Q20: Rakesh and Roshan are partners, sharing profits in the ratio of 3:2 with capitals of Rs. 40,000 and Rs. 30,000, respectively. They withdrew from the firm the following amounts, for their personal use:

Q20: Rakesh and Roshan are partners, sharing profits in the ratio of 3:2 with capitals of Rs. 40,000 and Rs. 30,000, respectively. They withdrew from the firm the following amounts, for their personal use: Interest on drawings is to be charged @ 6% p.a. Calculate interest on drawings, assuming that book of accounts are closed on March 31, 2020, every year.

Interest on drawings is to be charged @ 6% p.a. Calculate interest on drawings, assuming that book of accounts are closed on March 31, 2020, every year.

Ans:

Rakesh’s Interest on Drawings

Interest on Rohan’s Capital

Interest on Rohan’s Capital

Q21: Himanshu withdrew Rs. 2,500 at the end of each month. The Partnership deed provides for charging interest on drawings @ 12% p.a. Calculate interest on Himanshu’s drawings for the year ending March 31, 2017.

Ans:

Total Drawing of Himanshu = Rs 2,500 x 12 = Rs 30,000

Q22: Bharam is a partner in a firm. He withdraws Rs. 3,000 at the starting of each month for 12 months. The books of the firm are closed on March 31 every year. Calculate interest on drawings if the rate of interest is 10% p.a.

Ans:

Total Drawing of Bharam = Rs 3,000 xl2 = Rs 36,000

Q23: Raj and Neeraj are partners in a firm. Their capitals as on April 01, 2019 were Rs. 2,50,000 and Rs. 1,50,000, respectively. They share profits equally. On July 01, 2019, they decided that their capitals should be Rs. 1,00,000 each. The necessary adjustment in the capitals were made by introducing or withdrawing cash by the partners’. Interest on capital is allowed @ 8% p.a. Compute interest on capital for both the partners for the year ending on March 31, 2020.

Ans: Interest on Capital

Raj

Neeraj

Neeraj

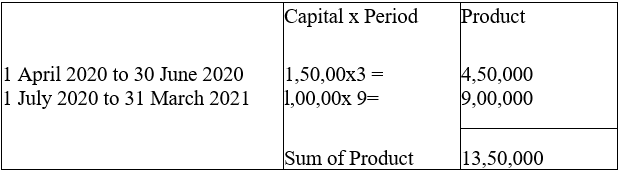

Q24: Amit and Bhola are partners in a firm. They share profits in the ratio of 3:2. As per their partnership agreement, interest on drawings is to be charged @ 10% p.a. Their drawings during 2019 were Rs. 24,000 and Rs. 16,000, respectively. Calculate interest on drawings based on the assumption that the amounts were withdrawn evenly, throughout the year.

Ans:

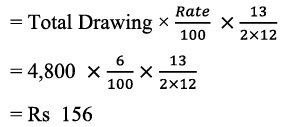

Q26: Menon and Thomas are partners in a firm. They share profits equally. Their monthly drawings are Rs. 2,000 each. Interest on drawings is to be charged @ 10% p.a. Calculate interest on Menon’s drawings for the year 2006, assuming that money is withdrawn:

(i) in the beginning of every month,

(ii) in the middle of every month, and

(iii) at the end of every month.

Ans:

(i) If they withdraw money in the beginning of each month Interest on drawing = Total Drawing x Rate x 13/ (2 x 12) Menon = 24000 x 10/100 x 13/ (2 x 12) = 1300

Thomas = 24000 x 10/100 x 13/ (2 x 12) = 1300

(ii) If they withdraw in the middle of every month Interest on drawing = Total Drawing x Rate x 6/12 Menon = 24000 x 10/100 x 6/12 = 1200

Thomas = 24000 x 10/100 x 6/12 = 1200

(iii) If they withdraw at the end of every month Interest on drawing = Total Drawing x Rate x 11/ (2 x 12) Menon = 24000 x 10/100 x 11/ (2 x 12) = 1100

Thomas = 24000 x 10/100 x 11/ (2 x 12) = 1100

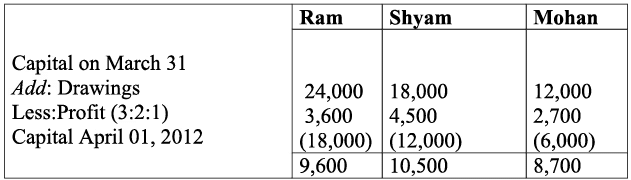

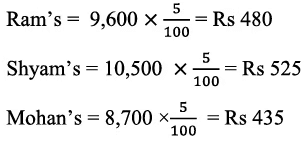

Q27: On March 31, 2017, after the close of books of accounts, the capital accounts of Ram, Shyam and Mohan showed balance of Rs. 24,000 Rs. 18,000 and Rs. 12,000, respectively. It was later discovered that interest on capital @ 5% had been omitted. The profit for the year ended March 31, 2017, amounted to Rs. 36,000 and the partner’s drawings had been Ram, Rs. 3,600; Shyam, Rs. 4,500 and Mohan, Rs. 2,700. The profit sharing ratio of Ram, Shyam and Mohan was 3:2:1. Calculate interest on capital.

Ans:

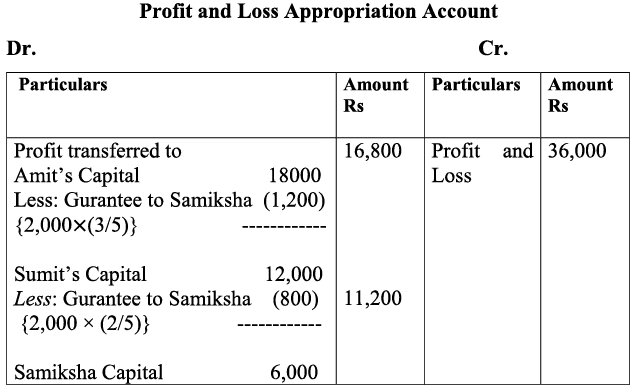

Here, Interest on Capital = Opening Capital x (Rate/100) Q28: Amit, Sumit and Samiksha are in partnership sharing profits in the ratio of 3:2:1. Samiksha’ share in profit has been guaranteed by Amit and Sumit to be a minimum sum of Rs. 8,000. Profits for the year ended March 31, 2017 was Rs. 36,000. Divide profit among the partners by preparing profit and loss appropriation account.

Q28: Amit, Sumit and Samiksha are in partnership sharing profits in the ratio of 3:2:1. Samiksha’ share in profit has been guaranteed by Amit and Sumit to be a minimum sum of Rs. 8,000. Profits for the year ended March 31, 2017 was Rs. 36,000. Divide profit among the partners by preparing profit and loss appropriation account.

Ans: Guarantee of Profit to the partners

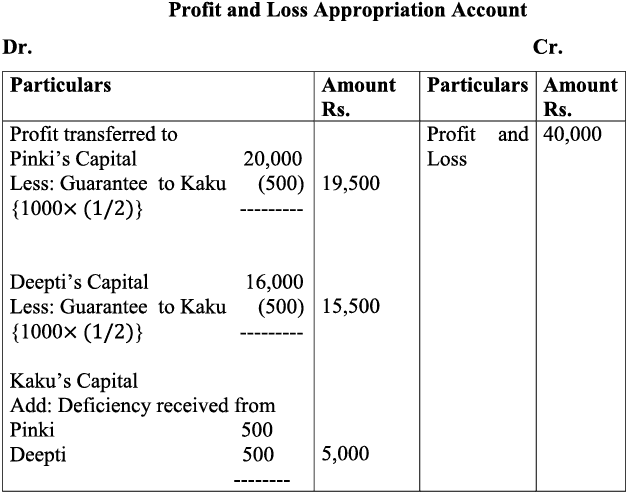

Q29: Pinki, Deepti and Kaku are partner’s sharing profits in the ratio of 5:4:1. Kaku is given a guarantee that his share of profits in any given year would not be less than Rs. 5,000. Deficiency, if any, would be borne by Pinki and Deepti equally. Profits for the year amounted to Rs. 40,000. Record necessary journal entries in the books of the firm showing the distribution of profit.

Ans:

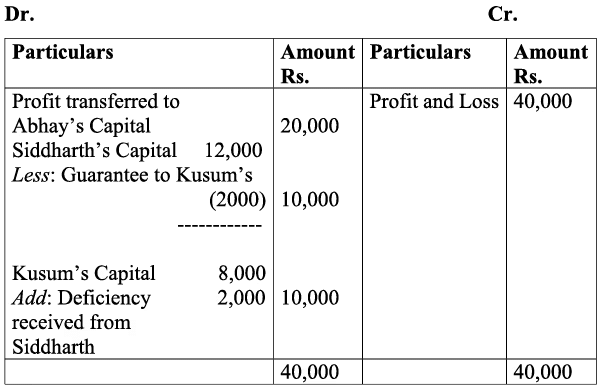

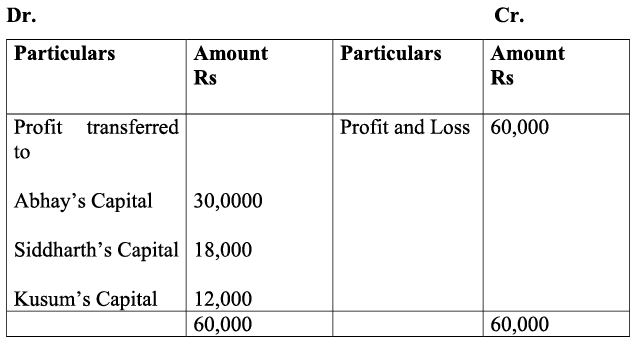

Q30: Abhay, Siddharth and Kusum are partners in a firm, sharing profits in the ratio of 5:3:2. Kusum is guaranteed Rs. 10,000 as her share in the profits. Any deficiency arising on that account shall be met by Siddharth. Profits for the years ending March 31, 2016 and 2017 are Rs. 40,000 and 60,000 respectively. Prepare Profit and Loss Appropriation Account.

Ans:

Profit and Loss Appropriation Account as on March 31,2016 Profit and Loss Appropriation Account as on March 31, 2017

Profit and Loss Appropriation Account as on March 31, 2017

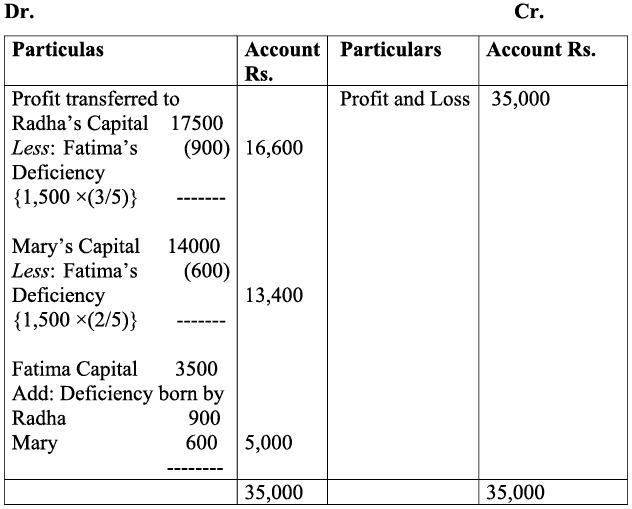

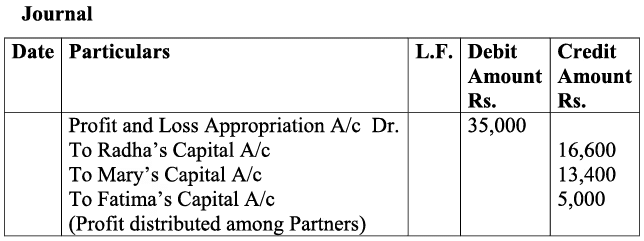

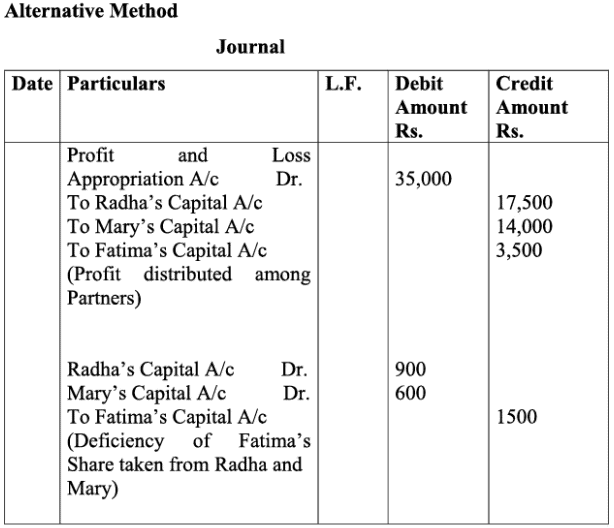

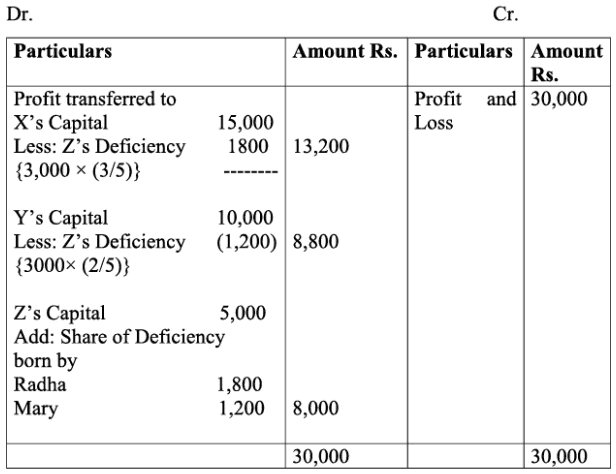

Q31: Radha, Mary and Fatima are partners sharing profits in the ratio of 5:4:1. Fatima is given a guarantee that her share of profit, in any year will not be less than Rs. 5,000. The profits for the year ending March 31, 2020 amounted to Rs. 35,000. Shortfall if any, in the profits guaranteed to Fatima is to be borne by Radha and Mary in the ratio of 3:2. Record necessary journal entry to show distributioin of profit among the partner.

Ans:

Profit and Loss Appropriation Account

Q32: X, Y and Z are in Partnership, sharing profits and losses in the ratio of 3 : 2 : 1, respectively. Z’s share in the profit is guaranteed by X and Y to be a minimum of Rs. 8,000. The net profit for the year ended March 31, 2020 was Rs. 30,000. Prepare Profit and Loss Appropriation Account.

Ans:

Profit and Loss Appropriation Account as on March 31, 2017

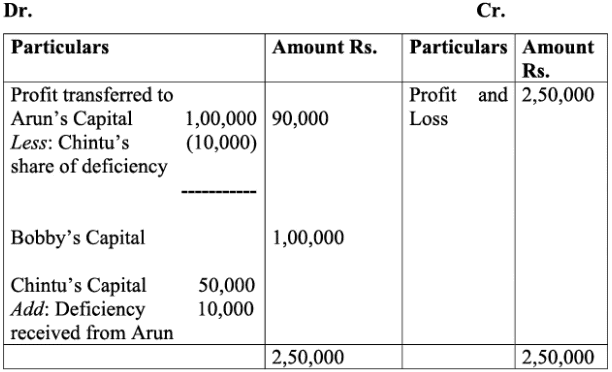

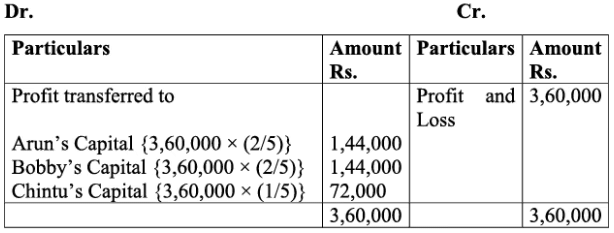

Q33: Arun, Boby and Chintu are partners in a firm sharing profit in the ratio or 2:2:1. According to the terms of the partnership agreement, Chintu has to get a minimum of Rs. 60,000, irrespective of the profits of the firm. Any Deficiency to Chintu on Account of such guarantee shall be borne by Arun. Prepare the Profit and loss Appropriation Account showing distribution of profits among the partners in case the profits for year 2015 are:

(i) Rs. 2,50,000;

(ii) 3,60,000.

Case (i) Profit and Loss Appropriation Account as on March 31, 2015

Case (ii) Profit and Loss Appropriation Account as on March 31,2015

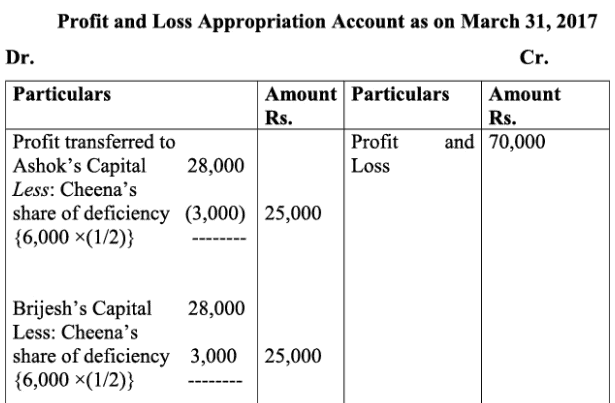

Q34: Ashok, Brijesh and Cheena are partners sharing profits and losses in the ratio of 2 : 2 : 1. Ashok and Brijesh have guaranteed that Cheena share in any year shall be Rs. 20,000. The net profit for the year ended March 31, 2017 amounted to Rs. 70,000. Prepare Profit and Loss Appropriation Account.

Ans:

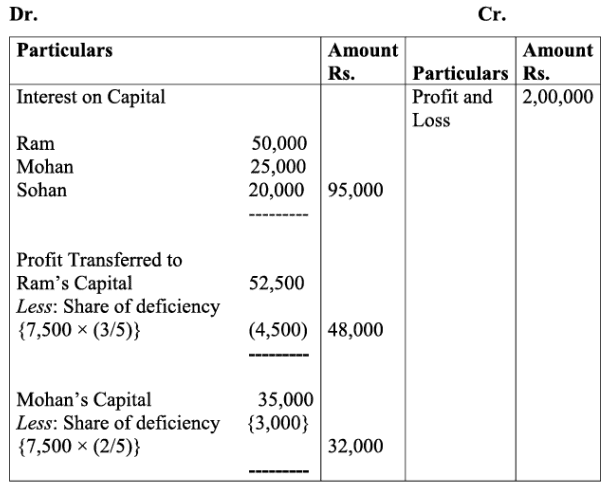

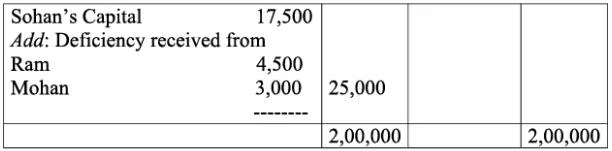

Q35: Ram, Mohan and Sohan are partners with capitals of Rs. 5,00,000, Rs. 2,50,000 and 2,00,000 respectively. After providing interest on capital @ 10% p.a. the profits are divisible as follows: Ram 1/2 , Mohan 1/3 and Sohan 1/6 . Ram and Mohan have guaranteed that Sohan’s share in the profit shall not be less than Rs. 25,000, in any year. The net profit for the year ended March 31, 2017 is Rs. 2,00,000, before charging interest on capital. You are required to show distribution of profit by preparing P & L Appropriation Account.

Ans:

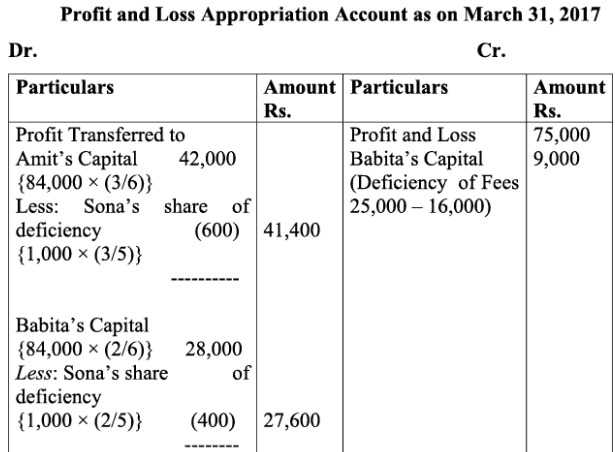

Q36: Amit, Babita and Sona form a partnership firm, sharing profits in the ratio of 3 : 2 : 1, subject to the following :

(i) Sona’s share in the profits, guaranteed to be not less than Rs. 15,000 in any year.

(ii) Babita gave guarantee to the effect that gross fee earned by her for the firm shall be equal to her average gross fee of the proceeding five years, when she was carrying on profession alone (which is Rs. 25,000). The net profit for the year ended March 31, 2017 is Rs. 75,000. The gross fee earned by Babita for the firm was Rs. 16,000. You are required to prepare Profit and Loss Appropriation Account.

Ans:

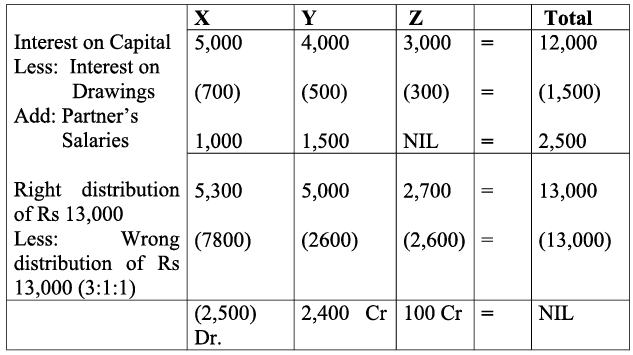

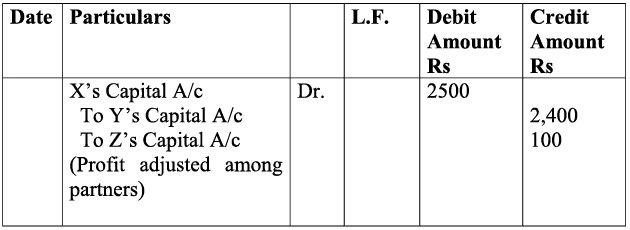

Q37: The net profit of X, Y and Z for the year ended March 31, 2020 was Rs. 60,000 and the same was distributed among them in their agreed ratio of 3 : 1 : 1. It was subsequently discovered that the under mentioned transactions were not recorded in the books :

(i) Interest on Capital @ 5% p.a.

(ii) Interest on drawings amounting to X Rs. 700, Y Rs. 500 and Z Rs. 300.

(iii) Partner’s Salary : X Rs. 1000, Y Rs. 1500 p.a.

The capital accounts of partners were fixed as : X Rs. 1,00,000, Y Rs. 80,000 and Z Rs. 60,000. Record the adjustment entry.

Ans:

Past Adjustment Explanation: Capital have credit balance if it deducted will be debited and if it is added it will be credited.

Explanation: Capital have credit balance if it deducted will be debited and if it is added it will be credited.

Here X wrongly taken excess Rs 2,500 hence Rs 2,500 will be deducted from X capital Account on the other hand Y and Z taken less amount as they should have been taken, hence capital account of Y and Z will be added.

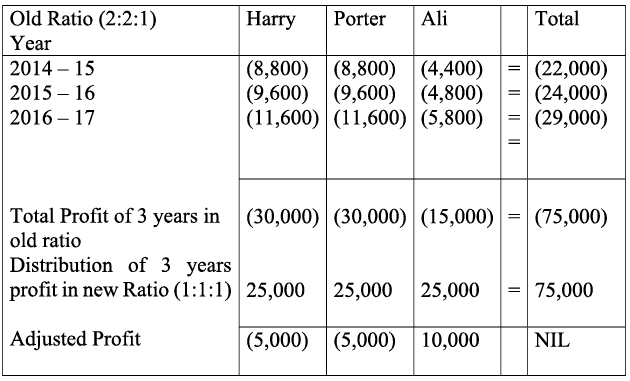

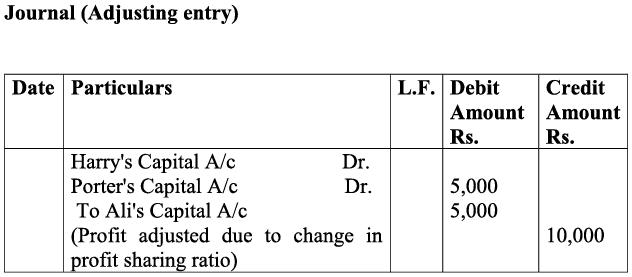

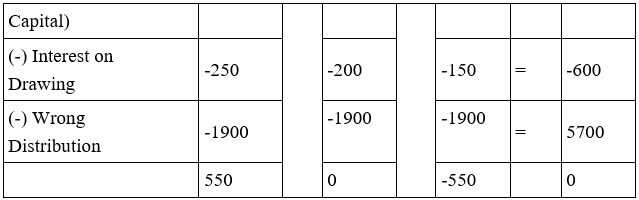

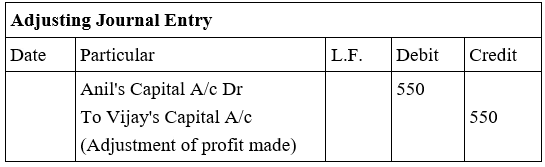

Q38: The firm of Harry, Porter and Ali, who have been sharing profits in the ratio of 2 : 2 : 1, have existed for same years. Ali wants that he should get equal share in the profits with Harry and Porter and he further wishes that the change in the profit sharing ratio should come into effect retrospectively were for the last three year. Harry and Porter have agreement on this account.

The profits for the last three years were:

Show adjustment of profits by means of a single adjustment journal entry.

Ans:

Distribution of Profit

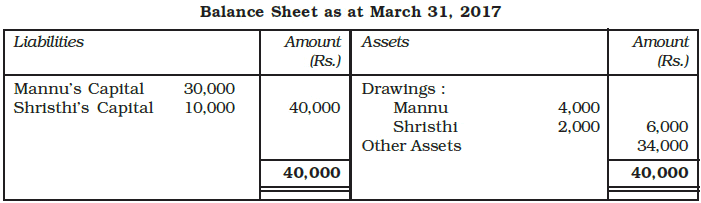

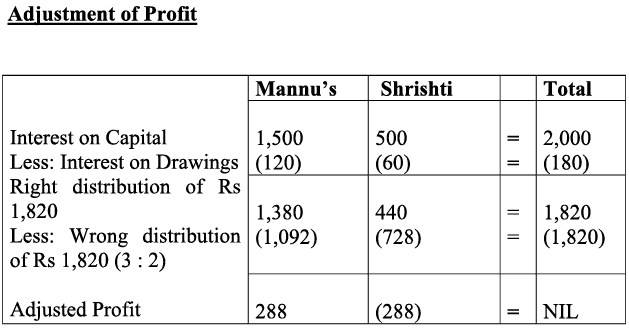

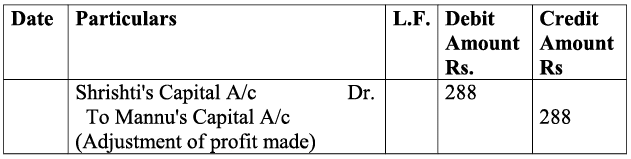

Q39: Mannu and Shristhi are partners in a firm sharing profit in the ratio of 3 : 2. Following is the balance sheet of the firm as on March 31, 2017.

Profit for the year ended March 31, 2017 was Rs. 5,000 which was divided in the agreed ratio, but interest @ 5% p.a. on capital and @ 6% p.a. on drawings was omitted. Adjust interest on drawings on an average basis for 6 months. Give the adjustment entry.

Ans:  Adjusting Journal Entry

Adjusting Journal Entry

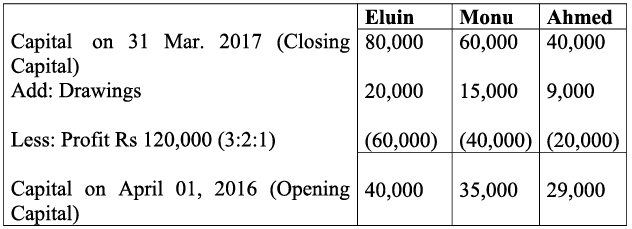

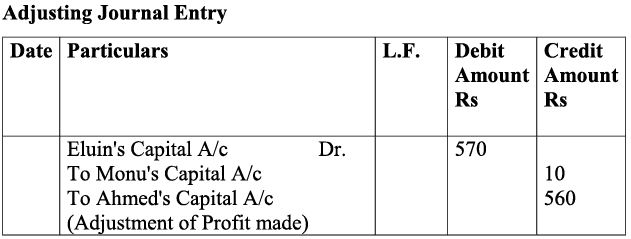

Q40: On March 31, 2017 the balance in the capital accounts of Eluin, Monu and Ahmed, after making adjustments for profits, drawing, etc; were Rs. 80,000, Rs. 60,000 and Rs. 40,000 respectively. Subsequently, it was discovered that interest on capital and interest on drawings had been omitted. The partners were entitled to interest on capital @ 5% p.a. The drawings during the year were Eluin Rs. 20,000; Monu, Rs. 15,000 and Ahmed, Rs. 9,000. Interest on drawings chargeable to partners were Eluin Rs, 500, Monu Rs. 360 and Ahmed Rs. 200. The net profit during the year amounted to Rs. 1,20,000. The profit sharing ratio was 3 : 2 : 1. Record necessary adjustment entry.

Ans: In this question interest on capital shall be calculated on opening capital Adjustment of Profit

Adjustment of Profit

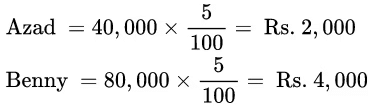

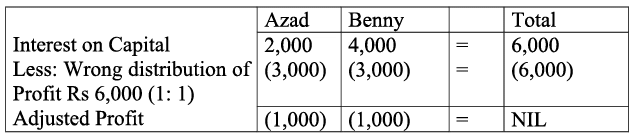

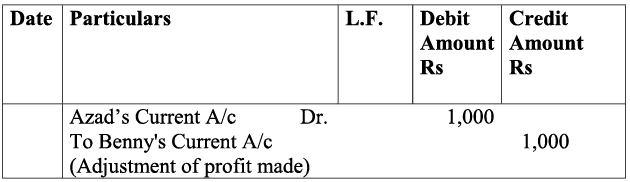

Q41: Azad and Benny are equal partners. Their fixed capitals are Rs. 40,000 and Rs. 80,000, respectively. After the accounts for the year have been prepared it is discovered that interest at 5% p.a. as provided in the partnership agreement, has not been credited to the capital accounts before distribution of profits. It is decided to make an adjustment entry at the beginning of the next year. Record the necessary journal entry.

Ans:

Interest on Capital Adjustment of Profit

Adjustment of Profit Adjusting Journal Entry

Adjusting Journal Entry

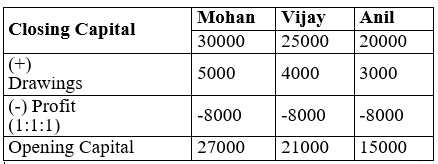

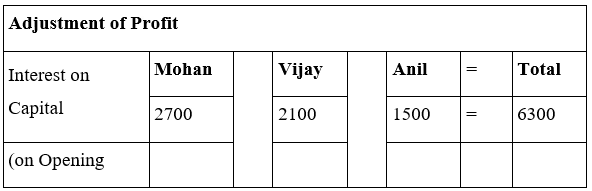

Q42: Mohan, Vijay and Anil are partners, the balances in their capital accounts being Rs. 30,000, Rs. 25,000 and Rs. 20,000 respectively. In arriving at these figures, the profits for the year ended March 31, 2017 amounting to Rupees 24,000 had been credited to partners in the proportion in which they shared profits. During the year the drawings of Mohan, Vijay and Anil were Rs. 5,000, Rs. 4,000 and Rs. 3,000, respectively. Subsequently, the following omissions were noticed:

(a) Interest on Capital, at the rate of 10% p.a., was not charged.

(b) Interest on Drawings: Mohan Rs. 250, Vijay Rs. 200, Anil Rs. 150 was not recorded in the books.

Record necessary corrections through journal entries.

Ans:

Interest on Capital shall be calculated on opening capital: Interest on Capital Mohan = 27000 x 10/100 = 2700 Vijay = 21000 x 10/100 = 2100

Interest on Capital Mohan = 27000 x 10/100 = 2700 Vijay = 21000 x 10/100 = 2100

Anil = 15000 x 10/100 = 1500

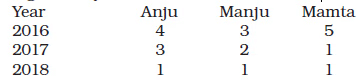

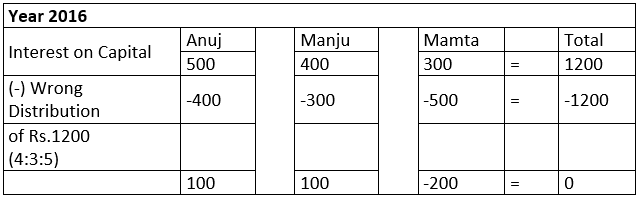

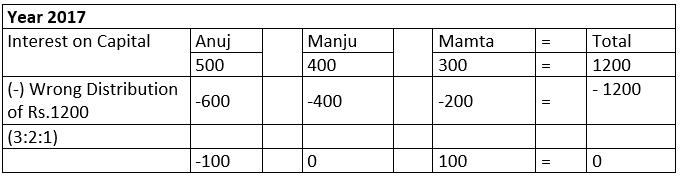

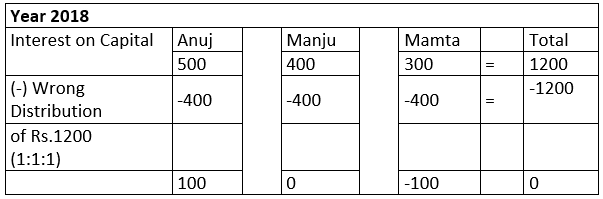

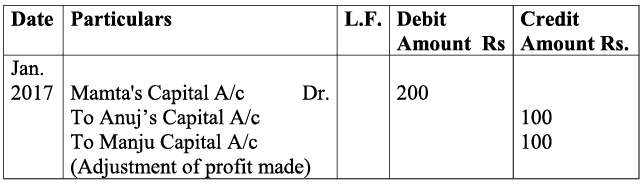

Q43: Anju, Manju and Mamta are partners whose fixed capitals were Rs. 10,000, Rs. 8,000 and Rs. 6,000, respectively. As per the partnership agreement, there is a provision for allowing interest on capitals @ 5% p.a. but entries for the same have not been made for the last three years. The profit sharing ratio during there years remained as follows:

Make necessary and adjustment entry at the beginning of the fourth year i.e. April 2019.

Ans:

Interest on Capital

Anuj = 10000 x 5/100 = 500

Manju = 8000 x 5/100 = 400

Mamta = 6000 x 5/100 = 300

Adjustment of Profit

Adjusting Journal Entry

|

42 videos|199 docs|43 tests

|

FAQs on NCERT Solution: Accounting for Partnership-Basic Concepts - Accountancy Class 12 - Commerce

| 1. What are the basic concepts of accounting for partnership firms? |  |

| 2. How is the profit-sharing ratio determined in a partnership? | |

| 3. What is the significance of maintaining capital accounts in partnership accounting? | |

| 4. How is goodwill treated in partnership accounts? | |

| 5. What are the accounting entries for admitting a new partner in a partnership? | |

Summary

,past year papers

,Previous Year Questions with Solutions

,Exam

,Free

,Viva Questions

,shortcuts and tricks

,Important questions

,NCERT Solution: Accounting for Partnership-Basic Concepts | Accountancy Class 12 - Commerce

,Semester Notes

,ppt

,mock tests for examination

,NCERT Solution: Accounting for Partnership-Basic Concepts | Accountancy Class 12 - Commerce

,Sample Paper

,practice quizzes

,Objective type Questions

,video lectures

,Extra Questions

,MCQs

,NCERT Solution: Accounting for Partnership-Basic Concepts | Accountancy Class 12 - Commerce

,study material

;

NCERT Solution: Accounting for Partnership-Basic Concepts Free PDF Download

Importance of NCERT Solution: Accounting for Partnership-Basic Concepts

NCERT Solution: Accounting for Partnership-Basic Concepts Notes

NCERT Solution: Accounting for Partnership-Basic Concepts Commerce Questions

Study NCERT Solution: Accounting for Partnership-Basic Concepts on the App

|

© EduRev

|

Education Revolution

|

|