Tax System - Economics, UPSC, IAS. | Indian Economy (Prelims) by Shahid Ali PDF Download

Tax System

Tax is a mode of income redistribution

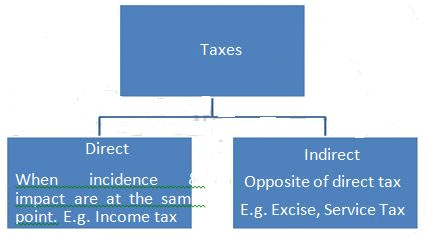

Incidence of Tax

The point where tax looks being imposed is known as the incidence of tax- the event of tax imposition.

Impact of Tax

The point where tax makes its effect felt is known as the impact of tax- the after effect of tax imposition.

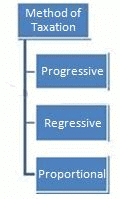

Types of taxes

Progressive taxation

- It increases with income.

- It is pro-poor

- Indian Tax system is an example

Regressive Taxation

- When tax decreases for increasing income

- More tax on poor and low producers

Proportional Taxation

- Fixed rate for every level of income

Important taxes

Personal income tax

- It is levied on the income of individuals, Hindu families, unregistered firms and other associations of people.

- It is a progressive tax

- For taxation purpose income from all sources is added

Corporation Tax

- It is levied on the income of registered companies and corporations.

- Progressive in nature

Custom Duty

- It comprised duty levied on imports and exports.

- It is an indirect tax

- It performs following major functions:

I. Raise revenue needed by the government

II. Regulate foreign trade of the country

III. Offer protection to local industries by imposing tariffs.

Excise Duty

- It is an indirect commodity tax levied on production

Sale Tax

- It is a tax levied on business transactions.

Minimum Alternate Tax (MAT)

- Came into effect from 1st April 1997

- MAT is applicable on the companies where the total income of the company (as computed under the income tax Act after availing the eligible deductions) is less than 30% of the book profit (the profit of the company as shown in its actual book of accounts).

- In such cases, the total income of the company shall be deemed to be 30%of the book profit and shall be charged accordingly.

MODVAT

It was introduced in 1986 on the recommendation of the Jha committee with the objective of nationalizing excise duty structure and reducing the cascading effect of excise duty.

Under it the manufacturer gets complete reimbursement of excise duty (only) paid by them on inputs like components and raw materials.

VAT on the other hand is a much more comprehensive tax which includes in its purview taxes like excise duties, sales tax, turnover tax etc.

Value Added Tax (VAT)

- VAT is an ad-valorem tax on domestic final consumption levied and collected at all stages between production and the point of final sale.

- It is a state level tax

- VAT method of collection of tax is different from non-VAT method in the sense that it is imposed and collected at different points of value addition chain i.e. multi-point tax collection. That is why it does not have a cascading effect on the prices of goods it does not increase inflation-and is therefore highly suitable for economy like India.

- It is a pro-poor tax system without being anti-rich because rich people do not suffer either.

- VAT has been successfully introduced by all the states. First introduced by Haryana in 2003 and UP was the last to adopt it in 1January 2008.

- Centre provided compensation to state government for first three years, for any los on account of introduction of VAT. 100% of the loss in first year 2005-06, 75% in second year 2006-07 and 50% in third year 2007-08.

Central Value Added Tax (CENVAT)

- It is a modified form of MODVAT involving single rate of 16% introduced in the Budget 2000-01 replacing the three ad-valorem rates of basic excised duty viz.; 8%, 16% and 24%

Goods & Services Tax (GST)

- It is a proposal of tax in India which will emerge after merging many of the state and central level indirect taxes. Some points are as follow:

- It will be a tax collected on the VAT method.

- It will be imposed all over the country with the uniformity of rate and will replace the multiple central and state taxes. ( central tax: CENVAT, service tax, sales tax, stamp duty; State tax: state excise ,sales tax, entry tax, lease tax, luxury tax, octroi tax, turnover tax, cess etc)

- The proposed tax has a single rate of 20% of which centre and state will have a share of 12% and 8% respectively.

Recommendation of the 13th finance Commission on GST

- Single 12% rate on all goods & services – 5% for centre and 7% for states

- All indirect taxes and cess

- to be subsumed in GST

- Railway fares and freight, electricity to attract GST

- High speed diesel, petrol, jet fuel to be brought under GST

- Only public services by govt, service transactions between employer and employee and health & education to be exempted from GST

- Export to be zero rated

- Import to attract GST

Service Tax

- A tax imposed on services

- Introduced in 1994-95 by the GoI

The tax was introduced with only 3 services liable for taxation, gradually extended to over 100 services by 2007-08.

- The rate of tax was also increased from 5% to 12% by 2006-07 which becomes 12.33% on account of the education cess.

|

2 videos|62 docs|78 tests

|

FAQs on Tax System - Economics, UPSC, IAS. - Indian Economy (Prelims) by Shahid Ali

| 1. What is the tax system? |  |

| 2. What is the importance of a tax system? | |

| 3. How does the tax system work in India? | |

| 4. What are the challenges faced by the tax system? | |

| 5. How can the tax system be improved? | |

mock tests for examination

,Free

,video lectures

,Exam

,UPSC

,IAS. | Indian Economy (Prelims) by Shahid Ali

,IAS. | Indian Economy (Prelims) by Shahid Ali

,Viva Questions

,MCQs

,Extra Questions

,Previous Year Questions with Solutions

,Tax System - Economics

,shortcuts and tricks

,past year papers

,UPSC

,ppt

,study material

,Semester Notes

,practice quizzes

,Tax System - Economics

,IAS. | Indian Economy (Prelims) by Shahid Ali

,Summary

,Tax System - Economics

,Objective type Questions

,UPSC

,Sample Paper

,Important questions

;

Tax System - Economics, UPSC, IAS. Free PDF Download

Importance of Tax System - Economics, UPSC, IAS.

Tax System - Economics, UPSC, IAS. Notes

Tax System - Economics, UPSC, IAS. UPSC Questions

Study Tax System - Economics, UPSC, IAS. on the App

|

© EduRev

|

Education Revolution

|

|