Cost of Improvement,Expenses on Transfer - Taxation PDF Download

Cost of Improvement,Expenses on Transfer - Taxation

Cost of Improvement

It means any capital expenditure incurred for making any additions or alterations to the capital assets by the assessee or by the previous owner.

Note 1: Cost of improvement undertaken before 1-4-1981 is to be ignored otherwise it should be considered accordingly.

Note 2: The cost of improvement of following self generated assets shall be deemed to be nil.

• Goodwill of business.

• Right to manufacture, produce or process any article or thing. (Patent)

However COI of Brand name and trade mark is not applicable.

Note 3: There is no cost of improvement in case of securities.

Expenses on Transfer

1. It includes any expenditure incurred wholly and exclusively for the purpose of transfer of capital assets.

It means expenditures which are necessary to effect transfer.

e.g. Brokerage, stamp duty, registration fees, legal expenses, advertisement expenses or litigation expenses incurred for claiming enhancement of compensation.

2. Expenses on transfer are different from expenses on acquisition. Acquisition expenses are added to actual cost of the asset whereas transfer expenses are deducted from sale consideration.

Note 1: Securities transaction tax paid either on transfer of shares or acquisition of shares is neither treated as expenses on transfer nor expenses on acquisition of the asset. [fifth proviso to section 48].

Period of Holding

If asset is purchased then period of holding is counted from the following dates.

1. Immovable property: From the date of possession.

2. Movable property: From the date of delivery.

3. Shares: From the date of allotment.

4. Shares acquired from the market: From the date of broker’s note.

5. If the asset is acquired through gifts and Section 49(1) is applicable then period of holding is counted from the date the previous owner acquires the assets.

Note : If the asset is acquired through gifts and Section 49(4) is applicable then period of holding is counted from the date the donor acquires the assets.

Note : The day the asset is transferred is ignored for the purpose of calculation of period of holding.

Asset Acquired Through Gift ETC. is Subsequently Transferred

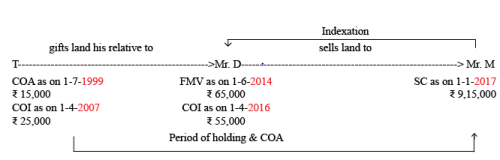

P1: Compute Capital Gain chargeable to tax for AY 2017-18.

How to Solve

1. Section 56(2)(vii) is not applicable since property is gifted to relative. Therefore Section 49(1) is applicable.

2. As per section 47, gift is not treated as transfer and hence transaction between T & D is not treated as transfer and hence no capital gain.

3. As per S 2(42A) period of holding shall be computed from the date the previous owner acquires the asset. [1-7-1999 to 31-12-2016]

4. As per section 49(1) since D has not acquired the land by paying a price, COA is cost to the previous owner who is T. COA = ₹ 15,000.

5. Indexation of COA is shall be done from M to D since D has acquired the asset on 1-6-2014. 6. Indexation of improvement done by T shall be from M to T and Indexation of improvement done by D shall be from M to D.

Solution

Computation of Capital Gain for the ay 2017-18

|

Sale consideration |

55,00,000 |

|

|

Less: Indexed cost of acquisition |

Index value of sale year 2016-17 [1125] .................................................................. x COA [4,04,000] Index value of acquisition year 1981-82 [100] |

(45,45,000) |

|

Less: Indexed cost of improvement |

Index value of sale year 2016-17 [1125] .......... x COI [18,000] Index value of improvement year 2010-11 [711] |

(28,481) |

|

Less: Expenses on transfer (0.15% of 55,00,000) = |

(8.250) |

|

|

LTCG |

|

9,18,269 |

1. When cost of acquisition is equal to indexed cost of acquisition?

2. In case of long term capital assets, ‘indexed cost of acquisition’ is deductible from sale proceeds to find out the amount of long term capital gain. Is there any provision in the Income Tax Act, 1961 under which ‘cost of acquisition’ (not indexed cost of acquisition) is deductible even in the case of long term capital asset ?

Solution

1. It will be equal in the cases where capital asset is acquired by the assessee after April 1981 by gift, will etc., in a particular year and transferred in the same year.

2. Transfer of long term capital asset being debentures or bonds in which indexation is not allowed.

Forfeiture of Advance Money

Advance money forfeited before 1-4-2014

The money forfeited by the transferer shall be deducted from the cost of acquisition or FMV as on 1-4-1981 whichever is higher.

Note 1: Where however advance money is forfeited before 1-4-1981, even then it should be deducted either from COA or FMV as on 1-4-1981 as the case may be.

Advance money forfeited on or after 1-4-2014

Section 56(2)(ix) provide for the taxability of any sum of money, received as an advance or otherwise in the course of negotiations for transfer of a capital asset. Such sum shall be chargeable to income-tax under the head ‘income from other sources’ if such sum is forfeited and the negotiations do not result in transfer of such capital asset. Section 51 provides that such sum has been included in the total income such amount shall not be deducted from the cost for which the asset was acquired in computing the cost of acquisition.

P1: (A) Compute capital gain chargeable to tax for the AY 2017-18.

(B) What if amount forfeited by D is Rs 75,000.

Ans : 4,33,873; 5,00,000.

Solution

|

Sale Consideration |

5,00,000 |

|

Less : Indexed cost of acquisition (1125 ^ 480 x 30,000) |

70.313 |

|

LTCG |

4,29,688 |

Note 1: Since transferer is Ms D, therefore, amount forfeited by Ms. D shall be deducted. COA = COA – amount forfeited by the transferrer = 70,000 – 40,000 = 30,000.

Note 2: Rs 10,000 forfeited by Ms. Taxcrazy is before 1-4-2015 is not taxable since capital receipt.

P2R: X received a house in March 2016 by way of gift from his father Y who had purchased the same in January 1980 for Rs 9,00,000. The cost of improvements incurred by Y were Rs 2,55,000 in March 1980 and Rs 3,40,000 in November 2002. The fair market value of the house as on April 1, 1981 was Rs 8,14,000. Before this house was gifted to X, Y had received an advance of Rs 3,00,000 in March 2014 towards sale of this house from Z but the sale did not materialise and the advance was forfeited by Y. Y also had received an advance of Rs 1,00,000 in Dec 2015 towards sale of this house from K but the sale did not materialise and the advance was forfeited by Y. The house was sold by X in March 2017 for Rs 48,00,000. Ascertain the capital gains chargeable to tax for the AY 2017-18.

Ans: Rs 1,00,000 charged under the head Income from Other Sources in PY 15-16 in the hands of Y.

FAQs on Cost of Improvement,Expenses on Transfer - Taxation

| 1. What is the cost of improvement in taxation? |  |

| 2. What are expenses on transfer in taxation? | |

| 3. How are expenses on transfer different from the cost of improvement in taxation? | |

| 4. Can expenses on transfer be claimed as a tax deduction? | |

| 5. Are there any exemptions or limitations on the cost of improvement deductions in taxation? | |

Cost of Improvement

,Cost of Improvement

,mock tests for examination

,Expenses on Transfer - Taxation

,Previous Year Questions with Solutions

,practice quizzes

,ppt

,past year papers

,Semester Notes

,Viva Questions

,Free

,video lectures

,Summary

,Expenses on Transfer - Taxation

,study material

,MCQs

,Important questions

,Exam

,Cost of Improvement

,Objective type Questions

,Sample Paper

,shortcuts and tricks

,Extra Questions

,Expenses on Transfer - Taxation

;

Cost of Improvement,Expenses on Transfer - Taxation Free PDF Download

Importance of Cost of Improvement,Expenses on Transfer - Taxation

Cost of Improvement,Expenses on Transfer - Taxation Notes

Cost of Improvement,Expenses on Transfer - Taxation Taxation Questions

Study Cost of Improvement,Expenses on Transfer - Taxation on the App

|

© EduRev

|

Education Revolution

|

|